McLain Capital letter to investors for the first quarter ended March 31, 2020.

McLain Capital Performance and Positioning Summary

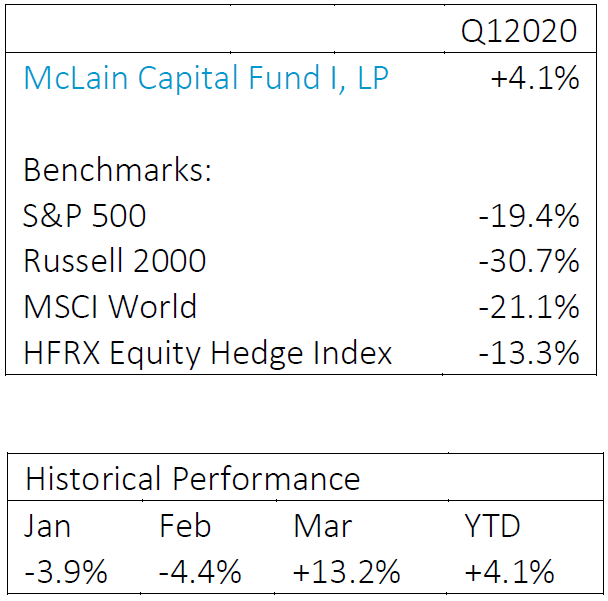

For the first quarter of 2020, McLain Capital Fund I, LP returned +4.1%, net of all fees, outperforming our benchmark, the S&P 500, by approximately 25 percentage points. Throughout the first quarter, the fund’s net market exposure ranged from 20% to 35%, net long, with the fund initially positioned with gross exposures of 95% of capital long, 60% short. Given the extraordinary level of volatility in markets and the severe underperformance of many value-oriented strategies, I’m pleased with last quarter’s performance and continue to see a highly favorable opportunity set given the current dislocation across markets.

Q1 2020 hedge fund letters, conferences and more

After our quarterly rebalance/repositioning during the last few days of March, we are currently positioned 35% net long, our long-term target net exposure, with gross positioning at approximately 77% long, 42% short. The fund’s long portfolio is roughly equal-weighted and is positioned across 33 issuers with no single position occupying more than 3% of capital; the short portfolio is currently positioned across 52 issuers with no single position occupying more than 1.5% of capital.

What Happened?

Over the past six weeks we’ve witnessed the fastest sell-off in stocks in our country’s history, with a 34% sell-off in the S&P 500, from February 19th to March 23rd, only to rally 16% into quarter end. Last month’s price action brought the VIX volatility index to historically unprecedented levels, surpassing those seen during the height of the Great Financial Crisis in late 2008. Incredibly, during the lows seen on March 23rd, the median NYSE-listed stock was down over 50% from the highs. The volatility was hardly contained to just equities, as both investment grade & high yield credit experienced the largest one week sell off in history. The ICE BofA US High Yield Index widened over 700 basis points from the February 17th tights of 357 basis points to March 23rd wides of 1087bps, a truly enormous move. It seems a combination of extremely low levels of liquidity and margin calls/forced deleveraging of some participants was a large driver behind much of the price action during some of the more chaotic sessions over the past month.

COVID-19 and its tertiary effects will likely prove to be the most acute disruption the global economy has experienced over the past 100 years. Jobless claims in the United States for the last 2 weeks of March have already totaled 10 million, a staggering and unprecedented shock to labor markets. Fortunately, COVID-19’s impact on public health, the economy, and the financial system have been met with extraordinarily proactive measures by governments around the world. On the monetary policy front, the dizzying array of actions by the Federal Reserve have provided much-needed liquidity to bank balance sheets, US dollar currency swaps, the commercial paper market, and what was briefly a highly dysfunctional market in US treasuries. By stepping in early as a lender of last resort & liquidity provider, the Fed’s actions have effectively unclogged the plumbing of the financial system and funding markets, allowing for the uninterrupted free flow of payments and credit while corporate borrowers have drawn over $200 billion in revolving lines of credit. In terms of fiscal policy, Congress’s extraordinary actions have provided a much-needed stopgap for the American public as parts of our economy go offline. All politics aside, there can be no perfect bill or one size fits all response by the federal government, yet the recent bipartisanship in the face of a severe crisis is highly reassuring in that the United States Government is both willing and able to take effective steps to arrest the dual crisis in public health and the economy.

“Investment markets follow a pendulum-like swing between euphoria and depression, between celebrating positive developments and obsessing over negatives, and thus between overpriced and underpriced.” Howard Marks, Oaktree Capital

Where Do Markets Stand Now?

As tumultuous as markets have been, I believe it’s all the more important for investors to step back, examine the larger picture, and remind themselves 1) that what we are currently experiencing is inherently temporary, and 2) that the intrinsic value of a business is the present value of its future cash flows in perpetuity, and that several quarters of poor earnings doesn’t dramatically affect a companies true worth based on its long term earnings potential.

As of the close on April 1, the S&P 500 stands at 2470, translating to an Enterprise Value/EBITDA multiple of 11x, and a free cash flow yield of 6%, both of which are roughly in line with their respective long-term averages. By these metrics, one could argue that large cap US equities are fairly priced. Yet, given that interest rates stand well below long-term averages, another could reasonably hold that stocks at current valuations look quite attractive relative to treasury yields; over the past 100 years the 10-year Treasury yield has averaged 4.5% and currently stands at a measly .58%.

A very bullish (and highly suspect) argument could sound something like this: US equities have produced annual rate of return of roughly 10% over the long term, providing an excess return of approximately 5.5% over 10-year Treasuries. With a simple assumption that earnings continue to grow at their long term average of 4% per annum, and rates remain “lower for longer” a bull could state that the market should trade at a free cash flow yield of 2-3%, which would equate to the market trading at a level more than twice as high as we currently stand. If this sounds ridiculous, its important to note the market was trading at a sub 3% FCF yield for a few years during the height of the tech bubble in the late 1990s and early 2000s, a time when 10-year Treasuries were yielding approx. 6%, 500+ bps higher than current levels. Alternatively, someone with a very bearish point of view could state that, given we are experiencing the largest economic shock in modern history, we ought to be trading in line with 2009 trough valuations of 8x EBITDA: translating to the S&P 500 at 1600, 35% lower than current levels. Obviously, both of these scenarios are extreme and are just an illustration of how difficult it is to handicap whole market equity risk and how challenging it is to use valuation to time the market.

In bull markets or bear markets we’re never short of prognosticators who assert opinions on short term market direction, year-end price targets, etc. Many of whom, dubbed “strategists”, have no real skin in the game themselves or any real accountability to the forecasts they make to their clients. To quote the economist John Kenneth Galbraith, “We have two classes of forecasters: Those who don’t know – and those who don’t know they don’t know.”

Most pertinent to us, the recent volatility has caused valuation spreads (the degree of dispersion in valuations across the market) to reach unprecedented levels – surpassing those seen during the height of the dotcom bubble. This has occurred in not only US stocks, but in foreign developed and emerging markets as well. Statistically speaking, the current backdrop and opportunity set for value-oriented long/short equity managers has never been better. Currently, our long positions carry an average free cash flow yield of 26% and EV/EBITDA of 2.1x. By comparison, the S&P trades at a FCF yield of 6% and EV/EBITDA of 11x. Importantly, all of our long positions are strong credits with healthy balance sheets - most of which are carrying net cash (more cash than debt) or negligible amounts of net debt and are well-equipped to navigate a credit constrained environment.

Why Does Our Approach To Investing Give Us An Edge?

First and foremost, there’s nothing particularly ground-breaking about how we approach markets. We simply believe that markets often misprice individual securities due to ignorance, overoptimistic expectations, or irrational fear, and, thus, are “inefficient”. Our value-add as an investment manager is in highly disciplined, data-driven, “bottom-up” stock selection designed to capitalize on these mispricings. To do so effectively often requires a willingness to bear a contrarian outlook. A value investor seeking the best opportunities – that is, stocks with compellingly low valuations - will often find himself venturing in overlooked markets, in unpopular industries, looking at companies surrounded by negative sentiment or possessing unglamorous businesses. All of which may sound counter-intuitive for an ideal investment. Yet, pessimistic market sentiment or general disregard on the part of investors often forces market valuations well below a conservative estimate of intrinsic value, creating opportunities for the investor willing to stray from the herd. In order to outperform the market, one has to assemble a portfolio that looks meaningfully different than the market. Outlined below are a variety of reasons that we believe set us apart and give us an “edge” in our approach.

“For a value investor, price has to be the starting point. It has been demonstrated time and time again that no asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough… No asset class or investment has the birthright of a high return. It’s only attractive if it’s priced right.” Howard Marks

First, I believe that an objectively disciplined & repeatable idea generation and investment process is imperative in delivering sustainable outperformance. The primary intent of which is to remain focused on the most predictive factors of long-term performance: valuation & capital efficiency. A heavily quantitative approach to security selection insulates our decision-making by removing subjectivity, emotion, and behavioral bias. We don’t try to imbue our process and strategy with complicated macro narratives, dogmatic views on the short-term direction of markets, or conjecture of specific companies’ future earnings growth. Instead, we use an empirically supported security selection process and proprietary model that’s designed to reflect the relative attractiveness of every company in our 6000+ company database. Our model is driven by ten fundamental metrics, roughly half of which are valuation focused, the other half “quality” or capital efficiency focused. We’re obviously not going to bat 1.000, nor always outperform, but I firmly believe an efficient, data-driven, and broadly applicable investment process combined with strict risk management gives us a discernable edge. This may sound like an overly prescriptive approach to markets, but as the last several weeks have demonstrated, a clear and coherent investment process is incredibly important when navigating volatile market environments. We can’t control outcomes, but we can meaningfully tilt the probabilities in our favor by sticking to the right process.

We have a defensive investment mindset and a strong emphasis on capital preservation. Sound risk management is imperative in any investment approach - we have no way of consistently predicting the short-term performance of any particular company, sector, or market. We don’t try to, and never will. As the past several weeks have demonstrated, we must be equipped to deal with all kinds of challenging markets and event risk. I believe the best way to mitigate the myriad list of risk factors is through diversification and low net market exposure. I don’t anticipate positioning much less than 30 longs, and 50 shorts, with no single long position being greater than 4% of capital, and no single short position exceeding 2% of capital. We put sensible limits on net exposures to specific sectors and view diversification as imperative to sustainable long-term performance. With a target beta of zero, our intention is to construct a portfolio immunized as much as possible from overall market volatility and produce returns that are uncorrelated to the broader market.

We’re small. As a small & nimble fund, we’re able to navigate much further down the market cap spectrum, where other large manager’s sheer scale and asset size precludes them from doing so. This presents us with a much larger universe of investment opportunities than those limited to large cap stocks. Small and mid-cap issuers are typically much less covered by sell-side research analysts and have lower levels of institutional ownership. These factors lead to a less competitive, and more inefficient market where mispricings are more commonplace and more dramatic.

We invest globally. Rooted in our belief that opportunity set is as important as skill set, we look beyond US equities and cast a wide net across global markets – our investable universe encompasses over 6,000 issuers, the vast majority of which are in developed markets. In our view, foreign markets are more often overlooked by investors and, consequently, are less efficient & less competitive than US markets, presenting lower hanging fruit. As a whole, foreign markets currently present much more compelling valuations than the US. It’s worth noting that, on average, each year out of the past 10 years, 74% of the top 50 performing stocks have been have non-US stocks. By including non-US equities, we expand our list of investment candidates more than four-fold. This wide net approach meaningfully tips the probabilities in our favor of identifying strong outperformers and generating alpha.

Moving Forward

As a nation, we have the resources, know-how, and capability to not only tackle this crisis head on, but emerge as a stronger, more resilient, and more unified country. We remain the destination of choice for the world’s best and brightest and the world leader in technological innovation. The past 100 years have hardly been without crisis in our country, yet we’ve seen living standards rise more than six-fold during that period, despite the many challenges we’ve faced. Equipped with an extraordinarily innovative market system, a highly effective rule of law, and a dynamic entrepreneurial spirit, I have no doubt in our ability to navigate and overcome the challenges we currently face.

Thank you for entrusting me with your hard-earned capital. Please don’t hesitate to reach out with any questions or comments.

Sincerely,

Dave O’Harra

Managing Partner