What is the best stock market investment strategy to deploy money is the ultimate question to be answered, if you have money of course. Most people think about whether to deploy it all immediately (LUMP SUM INVESTING) or to stage the purchases over a period of time (DOLLAR COST AVERAGING). Vanguard and other research shows that you’ll do better with a lump-sum investment in 70% of cases and better with dollar cost averaging in 30% of cases. So, it is up to you what kind of odds do you wish to bet on.

Q1 2020 hedge fund letters, conferences and more

However, you know I will not give you just the stock market investing statistics. By discussing the difference between investing and speculating; the difference between lump sum investing where you invest when you have the money and when a financial instrument fits your required return and dollar cost averaging, where you are more concerned about the market as you try to time it we will also touch on what really matters for the long-term.

Another point is discussing the importance of buying the bottom in the market - some stocks are up 50% since March 22, but how much does that change their investment quality? You'll be surprised how important it is! The importance of timing the market will also give you the answer when it comes to investing it all in a lump-sum or dollar cost average over time.

Dollar Cost Averaging vs. Lump Sum Investing

Transcript

Good day fellow investors. How to buy stocks in a volatile market, if you have some cash when to deploy, spread it over 12 months, or put the whole lump sum in immediately. I've done some research from Vanguard some research papers, and then I'll share also my own experience. And I hope by the end of this video, you'll have a clearer idea of how and when to deploy your money during this environment.

So if you've got some cash with I don't know rainfall, a bonus, stimulus, or whatever, and you want to deploy some cash or debt or you have been waiting for a crash to deploy some cash. Now the question is how to deploy that? So there are two strategies. One is to dollar cost average to make a systematic investment over time, the other is to simply put in the lump sum. We're going to show historical results of that set of both strategies to see which one is best and how, maybe best fits you, then we're going to discuss something very close to this, which is investing versus speculating.

I'm going to share with you the importance of buying at the right moment in the market, what's the best time to buy really to nail the bottom, how important that is when it comes to investing. And then I've also share my experience over the last 20 years that I have been investing, how I did it during one crash the dotcom, the end of the dotcom crash that I caught 2009, the Great Recession crash and the current and the 2015 and the 2018 crash and how I dealt with those.

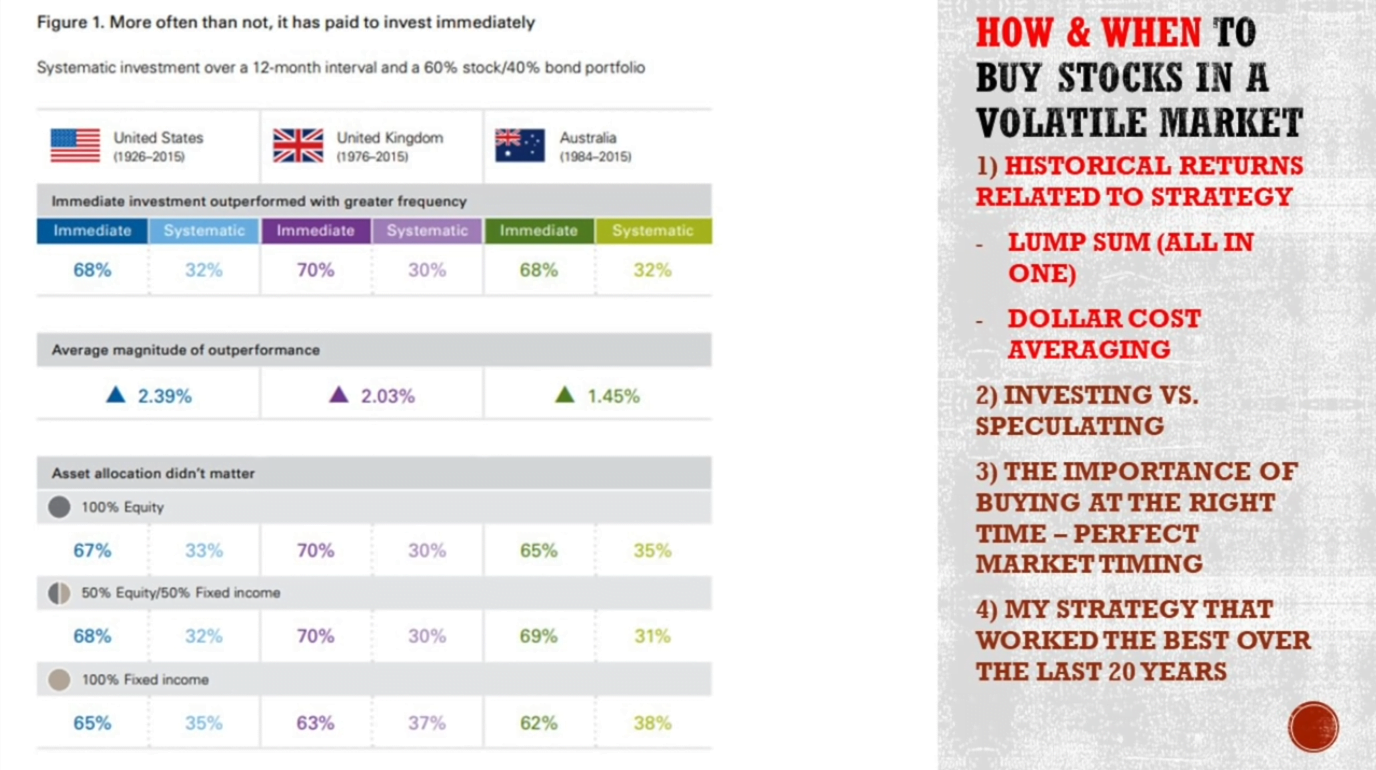

Let's start with the content. So let's say you've got $100,000 that you received this morning. Now what to do, should you invest immediately all the money or should you spread the investments over 12 months, I've gone to Vanguard and they've done the research so a lot of research has been done no need to spend a lot of time I'm on it but you have a systematic the dollar cost averaging, investment where you invest over 12 months and if you invest immediately all the money and they have made the analysis from 1926 to 2015 in the United States, United Kingdom and Australia, there is a 68% chance that you do best when you invest it all at one go and the 32% chance that you do better with dollar cost averaging.

So when you start investing, let's say seven out of 10 times you will be better with a lump sum. Three out of 10 times you will be better with the dollar cost averaging strategy. Thus, it is up to you whether you want to bet on the odds of 7 out of 10 or 3 of 10.

As we cannot time the market we cannot know what will happen in the market. The last month have been has been full of negative news the market is up 25% so you cannot time that and now you have to see what odds do you like lump sum, 7 out of 10 odds of doing good or dollar cost averaging systematically investing over a period of 12 months? 3 out of 10, you do good. I think this gives the answer, but we'll have a lot more to discuss and some nuances on that.

Why does the lump sum portfolio outperform? Well, it always boils down to investing versus speculation. Investing is a positive sum game. When you are dollar cost averaging a lump sum you time the markets you try to time the market.

And we all know that time in the market, the businesses that growth, the development, the dividends, that is what gives you long term returns, and that is what skews the odds 70% for the lump sum investment when you have the money against the dollar cost averaging or systematic spreading if the investment. Now dollar cost averaging here isn't I have 1000 every month and that's what I have and that's investing. That's a different kind of dollar cost averaging. We are talking here about what to do if you have the money now.

Just a story here I have started with really social media financial writing analysis research in 2015. So we are now five years in and I got constant emails from people waiting for a crash 2015, 2016 there was a crash there. And everybody said I'm selling everything, I'm waiting for a 50% crash and waiting for 2009 lows.

Still with the current situation, just the market and many other stocks are much much higher, the market is up 48% since then, so this is the cost of waiting for a better entry point. Similarly, missing the 25 best days of the S&P 500 since 1970 would change 100 dollar investment from return that we are now with dividends even more than 2000 something 3000 to just what $400.

So by staying invested and not missing 25 days, the 25 best days in the market, you make 7 times more money. And investing is about owning businesses dividends, growth, value and wealth accumulation. The best days are usually after the worst days. As you cannot time when the best days will come when is the bottom then it's better to stay invested not to miss the best days in the market.

Dollar Cost Averaging

And where does the real divergence create between 2800 points of the S&P 500 of the 100 investment and $400? The divergence always comes in the recovery. 1987 look at this all similar and then boom, you have a big divergence after the second day after Monday crash was already a great day, those that missed that. Then everything stable, bam 2003 recovery, huge divergence after the crash and then the ballistic divergence after 2009. So it's better to stay in that because then you are also getting a share of the market that is going up.

Now timing the market jumping in and out of the market everage annual total return for the S&P 500 index from 1999 to 2019, fully invested 6% annual return just 10 days, which we're somewhere March 2009, October 2009. Bam, you are down 4% annually. That's a huge difference in returns. Missing more 20 days I'm not even going to mention how detrimental that can be to your portfolio.

Now also when they is a crash where the S&P 500 fell by 20% or more if you stay fully invested a year later, two years later, and three years later, the cumulative returns are always higher. If you tried to time the market in any month or three months or even worse six months, if you're out of the market, six months out of investing, you are losing a lot because that is how investing works.

Now let me tell you about buying perfectly about perfectly timing the bottom and how important that is all this media frenzy about stocks going down 5-10 percent, 3% up, pre market, after market, how important that really is. So you might think it would be great to nail this bottom to have bought everything the 22nd of March 2020. You will be now up what 25% and you would be a great investor because that's what great investors do. Right? Well, let me show you this.

Lump Sum Investing And Market Crashes

This is a stock from December 1981. It was $590. It fell 28% in nine months. So in August 16, 1982, it was down to 430. So you might think, oh my God, if you bought in 1981 you would feel terrible for not buying in 1982 or if you missed the bottom of 1982 you would feel terrible for having to buy it later at 600 or something right? Well, you have to be smart and buy at the bottom is what everybody is trying to sell. Right? Well, let me show you this. You'll be pleasantly surprised.

Company is a textile company no moat, terrible business called Berkshire Hathaway run by a certain now he's now 90 years old, you better stay away from that. But if you invested with the stock level at 590 or 430, the difference is making if you paid 590, 482 times your money, and if you're paid for 430, 661 times your money. Now if you make 500 times your money, do you complain whether it is 482 or 661?

No, you don't and the annualised return, the difference in the annualised return between buying at the bottom and at the top 1981 1982 is less than 1%. The bottom point it's 90 basis points. So there is practically long term no difference when it comes to that. So this is my answer to all those that want to try to time the market. You should spend that energy on focusing on finding a great business that will give you compounding returns of 15, 10-15% over the very long term that will grow, that will have a good business and moat, good management. And that will deliver your returns. Your returns will not come from you buying and selling frenetically. Actually, your returns will go away if you do that.

Valuation Metrics And Lump Sum Investing

So stay invested. Keep investing when you find a good business doesn't really matter what price you buy it. And that's something Charlie Munger often says, but few understand him. Let me explain this a little bit more in detail. Now this week, I bought a little bit of Facebook for my learning portfolio. And everybody said, oh Sven, you should wait for 150 to buy it.

You should have bought it 140 or it's too early, it will go lower because of advertising prices going down so revenue will go down there will be better buying opportunities but let me show you something that investors keep in mind, if Facebook keeps compounding its book value, book value not the stock price is book value at 20% like it did last year, for the next 20 years, the book value per share will be $1,358. That increase in year 20 will be $226. That's 20% growth on the book value in year 19.

A price earnings ratio, earnings per share, that is 226. Put the price earnings ratio of 15 onto that Facebook's stock price. If they compound, I'm not saying they will unlikely, but just an example of what investing really is. At a PE ratio of 15. You are at a stock price of 3390. So the difference in annual returns over 20 years. It's either 18.1% or 16%. So that's 2.1% difference. So the difference is actually just 54 bucks, 54 bucks between buying Facebook and 174 or at 120. Compare the 54 bucks cost to the 3390 that you could get out, or that is just 1.5% of the sum.

So next time when you start freaking about buying something 20% higher, 20% lower or you missed the bottom, or fear of missing out, just think about buying great businesses. And I have a PhD on investing where I use GARCH, Arch, EBITDA, weighted average cost of capital, all those formulas, Beta, I analysed it all to get my PhD. I've worked for Bloomberg did research there, corrected their data. I was an accounting professor. And that's all the work class because that's all about those short term prices.

EMH

You simply follow what my grandmother used to tell me. When you have the money, you buy What's good, that's it. And if you follow your grandmother's advice, probably the same advice, call your grandmother, then you hear that's investing. In something's good, you buy it. That's it. And that's what I do when I have the money. I look at little bit of research a little bit and then I deploy it when I find something that I'm happy with.

Let me show you. So I have three portfolios, four portfolios that I manage on my research platform, pretty similar portfolios, but on one portfolio when I add 1000 each month, and then you see here two purchases on March and I didn't make a February purchase, I made it on the second of March and on 16th of March. However, the lump sum portfolio I keep that 20% in cash for great opportunities based on market volatility. And you can see here how sometimes I take profits.

So portfolio trades up 10% in three months, so took profits there. Then again one portfolio transaction where I took some profits and then I was 20% in cash going into this crisis and then you see my purchases, 3 March, 14 March, 20 March, 6 April, and 6 April. Now I'm 100% invested and I'm looking to invest invest a little bit more on safe leverage because I really like the investments in there.

Also, I had some money that we gained from our real estate purchase, decided not to invest in real estate because I can get better returns here. And here you can see my personal money that I transfer where the opportunities are, also purchases 16 March, 8 March, 8 April, so I buy something when they return on investment is good for me, when it fits my requirements and that's it. So when you have the money when you find something good. You put it in there and you forget about it.

Lump Sum Investing: Conclusion

That's all there is about investing, timing the market. That's just media and don't get fooled by the media. I'm really shocked when I say this when CNBC does its annual interview with Warren Buffett constantly over the whole two hour interview. It's always talking about the daily moves of the market. And Warren Buffett, poor Warren Buffett constantly discusses long term investment, how he doesn't know where the market will be in the next month, year and they constantly change implied open, where will be the open, where will it go? Where will it go?

Because that's what the media is selling you. And what I'm trying to tell you is just focus on finding good businesses that fit your investment requirements. Put your money in there and forget about it, go do something else. Go spend time with your family, the business will work do the work what it is supposed to do. So focus on businesses not that much on stock prices. The only outcome of focusing on stock prices is that you go crazy sooner or later sell in panic, lose a lot of money, and you never want to look at stocks again. Then you unsubscribe for this channel, you don't want to listen to me. You don't want to have fun on this channel. You don't want to invest in good businesses. And you do yourself a financial disservice for eternity.

So subscribe, click that notification bell. I'm looking forward to comments. Is this shocking? This mindset, this real investment mindset. Let me know in the comments, thank you check everything what I do as always on my website, and I'll see you in the next video.