Logos LP’s monthly commentary for the month of April 2020, titled, “Crystal Balls and Bottom Calling,” discussing the accelerated technological adoption, jobless claims and their take on the market.

Q1 2020 hedge fund letters, conferences and more

Stocks surged on Friday after a report said a Gilead Sciences drug showed some effectiveness in treating the coronavirus, giving investors some hope there could be a treatment solution that helps the country reopen faster from the widespread shutdowns that have plunged the economy into a recession.

Stocks tumbled from record highs in February into a bear market a month later as the spread of the coronavirus roiled market sentiment and the economic outlook. More than 2 million cases have been confirmed worldwide, including over 650,000 in the U.S., according to Johns Hopkins University. Governments urged people to stay home, effectively shutting down the global economy.

But the stock market has rallied since March 23 as new coronavirus cases in the U.S. and globally showed signs of plateauing. President Donald Trump said Thursday that “our experts say the curve has flattened and the peak … is behind us.”

He also issued guidelines to open up parts of the U.S. Thursday night, which identify the circumstances necessary for areas of the country to allow employees to start returning to work. The decision to lift restrictions will ultimately be made by state governors.

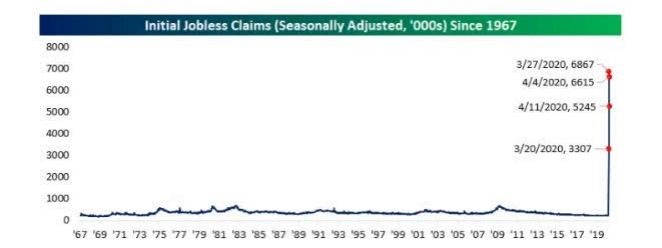

To be sure, the outbreak has already dealt a huge blow to the economy. In four weeks, about 22 million Americans have lost their jobs as the US economy has erased nearly all the job gains since the Great Recession (a 35 sigma event). The human suffering (physical, psychological, economic) brought on by the outbreak is tragic.

Our Take

It is no secret that markets rolled over this past quarter with the outbreak creating what looks to be the deepest recession since 2008-09. As a result, Q1 was by far the most active period in the history of our fund as we experienced what we believe to be one of the greatest buying opportunities for the patient long-term investor since the Great Recession of 2008-2009 and perhaps one of the greatest buying opportunities in the history of the capital markets.

Although it is an impossible task to time markets, understanding the temperature of the market and thereby making informed inferences as to the market’s probability of swinging from one extreme of the pendulum to the other is possible. It is during these times of great short-term pricing dislocations brought on by sudden economic shocks that high quality stocks trading at what we believe to be below their intrinsic value can be identified. While we have found several data points suggesting a possible near-term bottom, the following represent a list of those we found of most interest (courtesy of our friends at Sentiment Trader and Tom Lee from Fundstrat) during the Q1 selloff:

- Over 23 days in the past 7 weeks we have seen the S&P 500 move more than +/- 3%. The previous records were Oct. 1932 and Nov. 2008. In those 2 cases, the S&P 500 staged rallies of +40% and +27%, respectively, over the next 12 months.

- MSCI Emerging Market Index price-to-book ratio hit under 1 on April 2nd, 2020. The only other times the index hit those levels were bottoms in 2002 and 2008.

- March 2020 saw the 2nd largest one month change in aggregate cash holdings in AAII survey history.

- On March 31st, 89% of S&P 500 stocks have triggered a MACD buy signal, which at the time was the highest in recorded history. This has only occurred 10 times in the last 30 years and every time this happened, the Nasdaq Composite has rallied 6 months later by a median of +18%.

- As of March 20th, the average 5-week percentage change of 21 developed markets was -31.3%. This was the worst 5 weeks ever for global stock investors, beating 2008-09 Great Recession.

- On March 25th, more than 90% of NYSE issues were positive. The S&P 500 is up 100% of the time over the next year by a median of +29% every time this happened.

- The S&P 500 is at 2,845 (which is well above 50% retracement loss level). In the 1987, 2003 and 2008 crashes, “bear market rallies” fail at 33% retracement decline. For all three previous bear markets, the bottom was confirmed with a 50% retracement.

Does this mean that we have hit a bottom and things go straight up from here? Unlikely, as we have to consider the current situation in the context of unprecedented uncertainty and the weakness of analogies to the past.

Furthermore, the answer to this question of whether we have hit a bottom should not overly pre-occupy the patient long-term investor. Why?

We never know when we have hit a bottom as a bottom can only be recognized in retrospect. As Howard Marks has recently written:

“The old saying goes, “The perfect is the enemy of the good.” Likewise, waiting for the bottom can keep investors from making good purchases. The investor’s goal should be to make a large number of good buys, not just a few perfect ones.”

“So it’s my view that waiting for the bottom is folly. What, then, should be the investor’s criteria? The answer is simple: if something’s cheap – based on the relationship between price and intrinsic value – you should buy, and if it cheapens further, you should buy more.”

Successful long-term investing isn’t about buying only at bottoms and selling only at tops. It is instead about the gradual re-adjustment of one’s portfolio as a function of the significant price movements of individual stocks.

This is precisely the approach we have tried our best to stick with during these unprecedented times. We were able to re-position the fund into stocks that we have been monitoring for some time at what we believe to be good prices. The future is uncertain, the economic shutdown remains a very fluid situation and the amount of unprecedented fiscal and monetary action that has occurred in such a short period of time is unlike anything we have ever seen in human history (balance sheets of G4 central banks – the Bank of England (BOE), the Bank of Japan (BOJ), the Federal Reserve (FED), and the European Central Bank (ECB) – have expanded to 40% of gross domestic product). We don’t know what the precise long-term implications of this shutdown will be past 2020, but one thing we can predict with a degree of certainty is that certain businesses will continue to thrive long after the dust has settled. Ultimately investors who stay with their plan will be rewarded.

Stock Ideas

Currently, there are 22 names in the portfolio with our top 10 making up 65.17% of the fund’s net asset value and software now makes up over 85% of the fund’s industry exposure. Our portfolio has become more concentrated and we have now been able to take a shot at some of the highest potential growth stocks that have been on our watchlist for over 2 years. Below you will find the top 5 names in the portfolio:

- ALTERYX INC. (AYX)

- SERVICENOW INC. (NOW)

- TRADE DESK INC. (TTD)

- JOYY INC. (YY)

- ZSCALER INC. (ZS)

Musings On Technological Adoption

Over the past few weeks we have seen the typical torrent of crystal ball forecasting with predictions flying around on just about everything from personal consumption habits to global supply chains. It reminded us of a great quote:

“He who lives by the crystal ball will eat shattered glass.” - Ray Dalio.

Looking back at all the predictions that were made during and after the crisis of 2008 that things would “never be the same” and that “things would change forever” it is important to recall one of the great lessons of this current crisis: humility has been in short supply for a while now.

Who could have predicted much of what has occurred? Just like who can predict much of what will occur?

Instead, we will be modest with our outlook and focus only on one high-conviction trend we believe will have a large impact on the post COVID business climate: the accelerated adoption of new technologies. The planet is currently having a crash course in remote working, digital productivity and automation, e-commerce, digital payments and online social interaction. Technological adoption in such areas is still quite low and thus the growth in these areas which were fueling the bull market pre COVID still has plenty of room to run.

As mentioned in our COVID-19 update on March 19th, 2020 we are thinking of this accelerated technological adoption through the following 3 key themes:

- The rise of the emerging market Millenial/Gen Z -- ie. Joyy Inc, Baozun, MasterCard, Baidu etc.;

- The continued expansion of the ‘virtual’ economy as certain transformative digital workflows are likely to stick (fintech, video, e-commerce, virtual purchasing, cloud networking, IT management) – ie. Atlassian, Adobe, Paycom, Zscaler, Trade Desk etc.;

- Mission critical cloud computing and related applications as well as advanced artificial intelligence (and quantum computing) for the enterprise – ie. Alteryx, Anaplan, ServiceNow, F5 Networks etc.

After this period of “forced” adoption or large-scale “testing” of such technologies, individuals from managers, shareholders, employees to citizens will realize that they had much more to offer than previously thought. Restrictions put in place during the SARS outbreak of 2003 helped accelerate China’s embrace of e-commerce and COVID is having a similar effect globally. The pandemic will highlight the convenience and ease of online life and will expose opportunities for cost savings through increased technological adoption that will be too difficult for managers and shareholders to ignore.

Charts of the Month

Jobless claims have been a 35 sigma event.

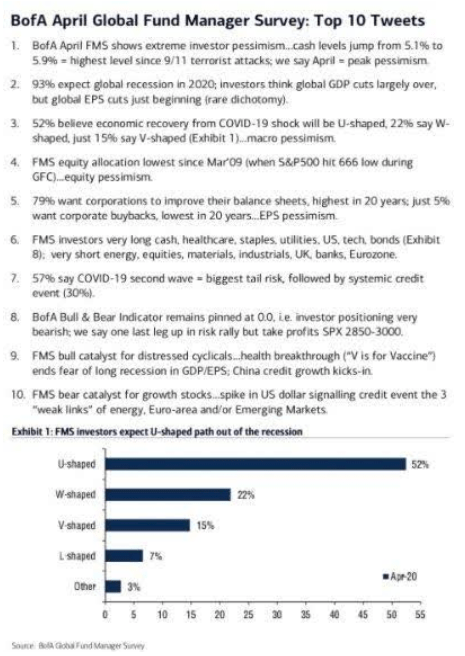

BoFA stats suggesting that pessimism is still the consensus view along with a U-shaped recovery

Thought of the Month

"Nature does not hurry, yet everything is accomplished.” — Lao Tzu

Articles and Ideas of Interest

- The Coronavirus in America: The Year Ahead. There will be no quick return to our previous lives, according to nearly two dozen experts. But there is hope for managing the scourge now and in the long term. One of the more interesting predictions is “Goodbye America First” as global collaboration will be more of a must. Seems a bit contrarian…

- An artificial intelligence arms race is coming. It is unlikely to play out in the way that the mainstream media suggest, however: as a faceoff between the United States and China. That’s because AI differs from the technologies, such as nuclear weapons and battleships, that have been the subject of arms races in the past. After all, AI is software—not hardware. Because AI is a general purpose technology—more like the combustion engine or electricity than a weapon—the competition to develop it will be broad, and the line between its civilian and military uses will be blurry.

- Software stocks emerge as downturn winners. Share in cloud groups prove more resilient then overall market - and some have risen to new records. Investors accustomed to looking to history as a guide have had to think again. In the meltdown that followed the 2008 financial crisis, the revenue multiples on software stocks contracted by 75 per cent. This time, according to Goldman Sachs, they had fallen back only about 30 per cent by the time the market bottomed in the middle of March — before a rebound over the next three weeks that saw them expand again by 18 per cent.

- Once safer than gold, Canadian real estate braces for reckoning. Canadian housing once seemed so infallible that the head of the world’s biggest asset manager in 2015 described Vancouver condos as a better store of wealth than gold. The coronavirus is putting that theory to the test. While lockdowns, job losses and uncertainty are roiling property markets from the U.K. to Australia to Hong Kong, Canada’s situation is more precarious than most. As its oil sector shriveled in recent years, Canada’s economy became ever more driven by real estate, an industry now in a state of paralysis. Nearly one in three workers have applied for income support. What’s more, its households are among the world’s most indebted, poorly placed to weather the storm. Bloomberg digs in with a well researched piece.

- The price of the Coronavirus pandemic. When COVID-19 recedes, it will leave behind a severe economic crisis. But, as always, some people will profit. Interesting piece from the New Yorker outlining the stories of those who are profiting handsomely from the chaos.

- WeWork’s lessons for US real estate in a post-Covid-19 world. The company’s troubles hint of what is to come - a long period of falling property prices in global cities. The Financial Times digs into the broader lessons WeWork’s travails provide — especially for a post-Covid-19 world. Among them: debt matters; corporate valuations were unsustainable even before the crisis; nobody is going to be rushing to lease office space anytime soon; and real estate in many parts of both the residential and commercial sectors has far, far further to fall.

- Time alone (chosen or not) can be a chance to hit the reset button. Steadily, slowly, research interest in solitude has been increasing. Note, solitude – time alone – is not synonymous with loneliness, which is a subjective sense of unwanted social isolation that’s known to be harmful to mental and physical health. In contrast, in recent years, many observational studies have documented a correlation between greater wellbeing and a healthy motivation for solitude – that is, seeing solitude as something enjoyable and valuable.

- The woman who lives 200,000 years in the past. As we confront the reality of COVID-19, the idea of living self-sufficiently in the woods, far from crowds and grocery stores, doesn't sound so bad. Lynx Vilden has been doing just that for decades, while teaching others how to live primitively, too.

- Cal Newport on surviving screens and social media in isolation. A computer scientist on why the quality of your quarantine may come down to how you use your technology. Right now, for so many people self-isolating in the face of the escalating coronavirus pandemic, technology is the main link to the outside world. It’s allowing us to maintain crucial contact with friends, family, and coworkers, and providing information and much-needed outlets for joy, amusement, and creativity in a rather bleak time. However, it can also be the source of deep anxiety and distraction: never has it been easier to stress-refresh your Twitter timeline looking for the latest Covid-19 numbers, or pick up your phone to text a friend only to fall into a mindless internet black hole.

We hope that you and your families are safe and healthy and that optimism and hope for the future remains strong. On our end this health crisis has reminded us that we all too often try to insulate ourselves against any discomfort before it even arrives. We seek to avoid pain by trying to control our external conditions to suit our comfort zones. This perception of control is alluring yet we risk losing the potential joy of discovery and the freedom of finding that we can learn and even be happy, within a much greater range of experiences than we thought. This period of pain has been challenging for us, but we are confident that we will look back upon it fondly as a period of exceptional personal growth.

All the best for a month filled with resilience, equanimity and gratitude,

Logos LP

Interdisciplinary Value Investing.

www.logoslp.com/

Missed a Post? Here's the Last 5:

- COVID-19 - It Will Pass

- Late-Capitalism and Gratitude

- How did we do in 2019? Sell in 2020?

- What Are We Wrong About Today

- Haters Gonna Hate