Blue Tower Asset Management commentary for the first quarter ended March 31, 2020, discussing value stocks continue to trail growth stocks, the spread of the Covid-19 disease, Fed’s loans to repo markets and USD exchange rate fluctuations.

[klamran]Q1 2020 hedge fund letters, conferences and more

There are rare times when one feels that they are witnessing history being made as the world we knew quickly transforms itself into something totally unfamiliar, and the current situation certainly feels as one of those times.

The two most salient features of the current bear market were the sheer speed with which the economy declined, with the S&P 500 falling 33.9% from February 21st to March 23rd and the accompanying extreme volatility of the markets. Following this decline, the S&P 500 proceeded to have a gain of 24.8% over the next three weeks. The S&P 500 saw three consecutive days of percentile changes greater than 9%, an event that had not been observed since 1929. On March 16th, the CBOE Volatility Index reached 82.69, eclipsing 2008 for the highest closing level ever.

The decline in economic activity and some of the stresses visible in financial markets exceeds what was seen in the first months of the 2008 global financial crisis. US Treasuries are among the most liquid markets in the world. However, at one point in March, the bid-ask spread for off-the-run 10-year US Treasury notes was as high as 50 basis points. For some of our lower-volume Japanese securities, the illiquidity reached extremes we have never seen before with bid-ask spreads in some cases expanding to over 20% of the share price.

While we were aware of the Covid-19 virus in January, we did not anticipate the level of economically disruptive policy response we have seen which far exceeds other deadly viral pandemics in the recent past such as the influenza pandemics of 1957 or 1968 which both killed over a million people globally. This current turmoil is not due purely to the direct effects of the virus. The world is also facing a rapid collapse in oil prices, significant geopolitical tensions, and high corporate leverage ratios (US corporate debt has increased from $6.2 trillion, 42% of GDP, at the end of 2009 to $10.1 trillion, 47% of GDP, at the end of 2019).

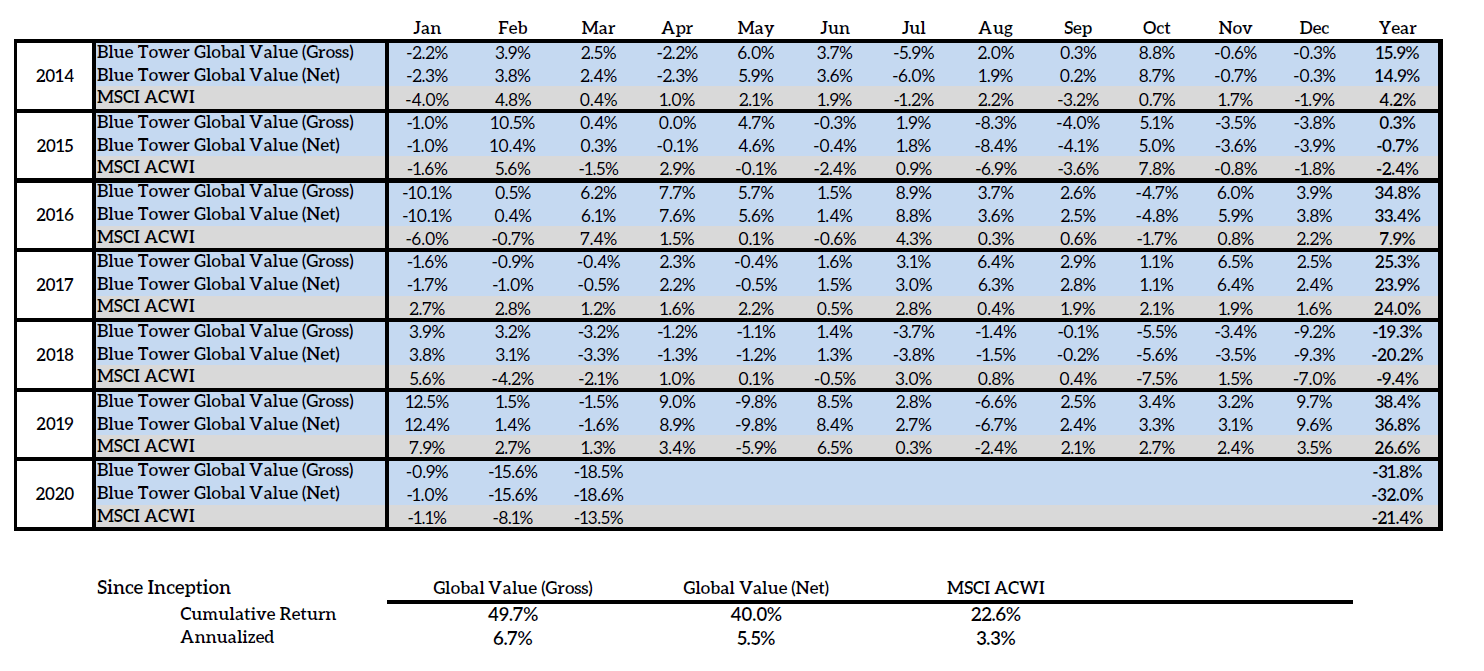

The Blue Tower Global Value strategy declined by 31.97% net (31.78% gross) in the first quarter of 2020. This quarter’s performance, our worst on an absolute and relative basis, follows Q4 2019, our best quarter performance. Quarterly results are not particularly meaningful as our performance should be judged over multi-year periods. Our long-term performance will reflect the quality and value of our portfolio.

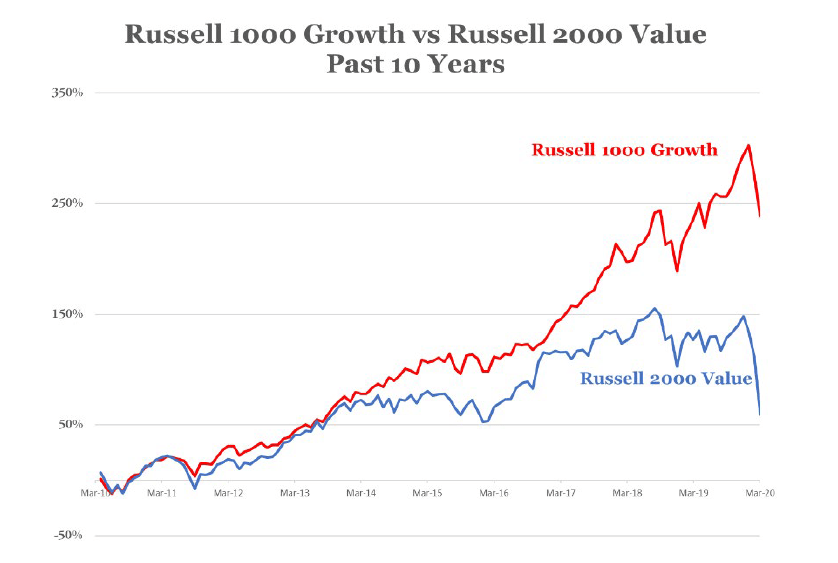

At the beginning of this quarter, over 75% of our portfolio was comprised of small-caps and a majority of the portfolio was invested outside of the US. So far this year, low-volume small-cap stocks, value stocks, and international companies have sold off far more than the overall US stock market. The Russell 2000 value index ended the quarter down 35.7%, its worst quarterly return in history (also the worst quarter for the overall Russell 2000 index). The relatively lower volumes of small-cap securities may have accelerated their decline due to the forced liquidations occurring in the present market. While the value factor has outperformed over the long-term, its outperformance has always been cyclical. During the recovery phase of a financial crisis, small cap value has tended to outperform the overall market.

Value Continues to Trail Growth

One of the paradoxes of value investing is that it offers its best prospective returns when its recent trailing returns makes it the least persuasive as an investing approach.

In many ways, it seems like rational pricing has disappeared from equity markets. Our portfolio has been no exception to this. Joban Kaihatsu (Tokyo:1782), a profitable dividend-paying company in our portfolio, ended Q1 at a share price of 4670¥ despite holding 5843¥ per share of cash net of debt and having a portfolio of marketable securities that at the end of December 2019 was worth 1793¥ per share. It is hard to believe a profitable company is worth less than the cash in their bank and brokerage accounts. Many of our other holdings have also been buffeted by large irrational price moves.

Price paid for investments is in most cases the most important determinant of future returns and at these prices, value appears to offer some of the best prospective future relative returns in its history.

While this year will be anything but normal, we estimate that our current portfolio at April 10th prices under normalized circumstances would offer a free-cash-flow yield of 18 to 19%. This is the highest prospective FCF yield we have ever estimated for our portfolio.

Covid-19 Crisis Potential Outcomes

The most important determinant of investment returns in 2020 will be the spread of the Covid-19 disease and the policy actions taken to counter it. The uncertainty in both of these is a root cause of the volatility we have been seeing this year. Additionally, there are unknowns of the long-term health effects of Covid-19 infection, the number of asymptomatic patients, and the efficacy of current candidate therapeutics to treat the disease.

As I expect that most people have consumed vast amounts of information on the current coronavirus pandemic, I will keep discussion of the virus itself brief. The optimistic view is that this virus will have a death toll similar to the seasonal flu with a higher basic reproduction number (a measure of contagiousness) and shorter epidemiological profile. Severe cases may suffer permanent lung damage or fibrosis, but the vast majority of the infected will make full recoveries. The more pessimistic views are for large percentages of the world to be infected with a death toll an order of magnitude higher than the flu and many of the survivors having considerable disabilities. WHO Director-General Tedros Adhanom estimated a case fatality rate of 3.4% for Covid-19

1 and the most pessimistic estimates from epidemiologists of potential global population infection rates range from between 60 to 80%.

This crisis, the government-mandated lockdowns, and individuals engaging in protective sequestrations of themselves and their families will all have extreme effects on the reported financials of businesses. As long as companies are able to weather this storm without dilutive financing or bankruptcy, the long-term effect on their prospects should be minimal. Equity investors will likely ignore the reported results of 2020 and focus on the long-term prospects of companies in their valuations with the expected loss from this year being removed from their normalized model of the company’s enterprise value.

While some of our portfolio positions will have their 2020 earnings impacted, this one-year hit to earnings does not dramatically change their future earnings ability.

USD Cash Crunch

The current crisis has caused a massive drive for US dollars causing large fluctuations in exchange rates and appreciation of the dollar against a basket of foreign currencies. The US dollar has become a global currency despite its issuance being firmly under the control of the US Federal Reserve. Roughly, half of global trade is invoiced in dollars and foreign nonfinancial corporations collectively have issued $12.1 trillion of US-denominated debt2. At the same time leveraged investors facing decreasing security prices and large asset managers facing redemptions have been forced into liquidating their positions in order to meet their liquidity needs.

Foreign corporations with dollar-denominated debt are in essence short the dollar as their domestic markets provide them with local currency. In order to get the dollars that these companies need to meet their dollar financial liabilities, they need to sell their products and services into the international market. When there is a demand shock and decrease in global trade as was created by this viral pandemic, their supply of dollars from serving customers dries up. They must therefore liquidate their domestic holdings or exchange domestic cash reserves for US dollars to meet bond interest payments and other dollar liabilities which do not get put on hold despite their business slowdown. All of these companies going for dollars at the same time causes this drive for dollar liquidity. The Federal Reserve has engaged in several interventions aimed at stabilizing the value of the dollar in the midst of the current crisis.

US Government Programs: Loans To Repo Markets

The US Government has engaged in monetary and economic interventions at a level never before seen in history. These include loans to repo markets, special grant programs, interest rate cuts, and asset purchases. The alphabet soup of recent Federal Reserve programs is too long to comprehensively analyze in this letter (ESF, PMCCF, SMCCF, TALF, MMLF, VRDNS, and CPFF).

The Federal Reserve’s loans to repo markets have the goal of maintaining the federal funds rate within the target range. Repo markets can be thought of as a global marketplace for short-term liquidity and operate in a manner similar to pawn shops. Borrowers offer up collateral which is typically highly liquid and safe securities such as treasury bills. The less safe or liquid the collateral, the greater the percentage difference between an asset’s market value and the amount that can be used as collateral, known as a “haircut”.

The Fed has also eased the terms of their currency swap lines to foreign central banks. The swap lines that the Federal Reserve has are with 5 central banks; the Bank of Canada, European Central Bank, Bank of England, Bank of Japan and Swiss National Bank. However, there are many other central banks that will need to provide dollar liquidity to their financial sector due to the slowdown in international commerce. The traditional way of this occurring is by the central banks liquidating their reserve of US treasuries on the open market in order to collect dollars for domestic use. However, this may send the prices of the treasuries down and their yields up, the precise thing that the Federal Reserve is attempting to avoid. In order to prevent this, the Federal Reserve has created yet another program, the Foreign and International Monetary Authorities repurchase agreement facility (FIMA Repo Facility) which provides lending liquidity to an international repo market of treasuries. By doing this, the foreign central banks that are not part of these swap line relationships with the Federal Reserve can borrow dollars for their domestic markets without needing to dispose of their treasuries.

At over $2 trillion of various loans and grants, the CARES Act coronavirus relief program passed by Congress is the largest stimulus rescue package in history. This will blunt much of the impact of the Covid-19 crisis and will have downstream effects on consumer behavior that are difficult to predict. I encourage any US investors affected by the crisis who are self-employed or are business owners to look into the programs offered by this Act, especially the EIDL and PPP loans, to see what aid they may qualify for.

All of this stimulus and monetary intervention will have long-term effects on the value of the dollar. M2 money supply increased 8.6% just in Q1 2020 compared to 0.7% in Q1 20193. In normal circumstances, inflation is created from the interaction between aggregate supply and aggregate demand, but lockdowns mess with both sides of the equation. The significant risk of deflation due to the rapid decrease of economic activity this quarter was the motivation for expanding dollar liquidity. When this crisis passes, economic activity and aggregate demand will return, and the increased M2 money supply may lead to accelerated dollar inflation down in the future. Individual investors and institutions should be cognizant of how inflation will affect their ability to meet their spending requirements. Further, companies with pricing power will be better equipped to pass on these inflation increases to their customers.

Our Strategy Going Forward

The most important thing in evaluating businesses for investment today is the impact of the virus and the government response on their business model going forward. We face a similar situation to past financial crises in that historical financial statements and analyst consensus estimates both have reduced utility in evaluating the future prospects of equities.

We will need to rely on logic and qualitative evaluation of businesses to predict which companies are likely to be more impacted by the rapidly shifting situation. All of our portfolio companies in our portfolio and the vast majority of those not in our portfolio have decreased in price since the beginning of the year. When every stock has a rapid and symmetrical decrease in price, it does not offer much in the way of opportunities to trade around positions to reallocate to bargains. However, some companies deserve price decreases more than others as their fundamental value has been impaired to a greater degree by the crisis. We will trade around our positions as some of them recover in price back towards their fundamental value and others remain at depressed valuations.

The panic and selloff in equity markets may be a great positive for long-term equity investors like us. Low stock prices are a positive, because several of our holding companies are buying back their shares at cheaper prices. We receive dividends from several of our companies which we will now be able to reinvest at higher rates of return. For investors in the accumulation phase of their financial life, they will now be able to invest their new capital at these same higher rates of return. We plan to take full advantage of this opportunity.

It is my hope that researchers can develop a vaccine and effective therapies for critical cases as quickly as possible. Every day this epidemic continues results in more death and suffering.

Please do not hesitate to contact me with any questions.

Best regards,

Andrew Oskoui, CFA

Portfolio Manager