Logos LP commentary for the month of March 2020, titled, “COVID-19 – It Will Pass”, discussing the investment implications for the long-term investors and fears occupying the markets.

The Covid-19 virus has emerged as the black swan no one saw coming. Investors are rattled and many are still adjusting to a world of uncertainty. Three main fears are preoccupying investors: first, that the virus will (and may already have) spread widely across America and the rest of the world. Second, that fear of Covid-19 and measures to stem its spread, like advising workers to stay home and shutting down air-travel, will have severe consequences for economic activity. And third, that policymakers may be unable to keep short-term disruption from becoming long-term damage.

Q4 2019 hedge fund letters, conferences and more

We believe all of these fears are well founded. Think of what is happening as a major paradigm shift for economies, institutions and social norms and practices that, critically, are not wired for such a phenomenon. It requires us to understand the dynamics, not only to navigate them well but also to avoid behaviors that make the situation a lot worse.

As we suggested in our last newsletter, the data was weakening even before the outbreak of Covid-19 and thus we believe that a recession in the coming months is more probable than not (we may already be in one). Investors are already pricing this in.

The bottom line is that the economic disruptions we are experiencing and those ahead will be more severe and widespread than the ones experienced by the bulk of the population in advanced countries.

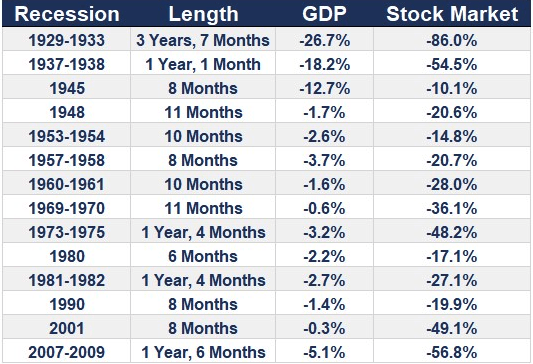

Drawdowns Are An Opportunity For The Long-Term Investor

Nevertheless, for the long-term investor drawdowns are an opportunity. Were share prices to fall exactly in line with the value of lost profits, they would be no cheaper. But in recessions, stocks tend to fall by a lot more than that. Consider the following:

These numbers are gut wrenching but recessions are typically not the end of the world. The last cycle lasted 11 years and many have forgotten that economic downturns are (or should be) a fact of life for investors.

Charlie Munger has said:

“I think it's in the nature of long term shareholding of the normal vicissitudes, in worldly outcomes, and in markets that the long-term holder has his quoted value of his stocks go down by say 50%. In fact, you can argue that if you're not willing to react with equanimity to a market price decline of 50% two or three times a century you're not fit to be a common shareholder, and you deserve the mediocre result you're going to get compared to the people who do have the temperament, who can be more philosophical about these market fluctuations."

Downturns eventually give way to recoveries from which those who have prepared for, and persevered through can profit from.

Recent lessons for long-term investors

Many shareholders cannot look past drawdowns and this panic is all too human. Big drawdowns affect people deeply as the pain of loss is felt far more intensely than the joy of gain. Suddenly, risks seem to be everywhere- to your job, to your business, to your pension, to your loved ones, to your dreams about the future.

Mohamed A. El-Erian has rightly pointed out that:

“We live in a global economy wired for ever deepening interconnectivity; and we are living through a period in which the current phase of health policy — emphasizing social distancing, separation and isolation — runs counter to what drives economic growth, prosperity and financial stability. The effects of these two basic factors will be amplified by the economics of fear and uncertainty that tempt everyone not just to clear out supermarket shelves but sadly also reignite terrible conscious and unconscious biases.”

It is important to emphasize the impossible benthamite conundrum governments face. On the one hand preserving life and public health is of critical importance, yet on the other, the short, medium and long-term costs of full economic shutdown are immense. What decision will maximize utility, or happiness, for the greatest number of people?

Right now it is impossible to ascertain how much worse things may get. We are being yanked out of our comfort zones making it increasingly difficult to focus on life after containment and reversal. Nevertheless, extreme fear like we are seeing cannot last indefinitely. The pendulum will eventually swing back and humans will carry on as they have after every one of the recessions listed above. Every crisis is also an opportunity.

At times like this the prudent long-term stockpicker will have a watchlist ready of quality company shares which have been and will continue to be priced below a reasonable estimation of their future long-term profits.

What specifically are we doing?

We consider the impending recession to be a 1 in 10-year opportunity for the long-term investor to tactically rebalance the portfolio for the next decade. In previous letters and newsletters, we mentioned that we expected future returns to be lower, but as we get deeper into the current selloff, we are becoming more optimistic about the probability of attractive annualized returns over the next 5 years – 10 years.

At present, we have been selectively initiating positions in stocks clustered under 3 key core themes that we believe have a high likelihood of delivering large earnings and revenue growth with rising returns on invested capital over the next 10 years. These themes are:

- The rise of the emerging market Millennial/Gen Z: YY, BZUN;

- The continued expansion of the ‘virtual’ economy as effective work-from-home policies are likely to stick (fintech, video, e-commerce, virtual purchasing, gaming, esports betting): ADBE, TTD, ATVI; and

- Mission critical cloud computing and related applications as well as advanced artificial intelligence for the enterprise: NOW, ZS, INTU, AYX.

We think these core themes will shape the investment landscape over the next decade.

For Long-Term Investors why now?

Since 1950 there have been eight periods on the U.S. S&P 500 when there has been a decline of at least 15% in a 30-day period. Picking the absolute bottom is a guess each time, but at the end of that 30-day period of declines, the immediate and mid-term future was almost always positive.

These are returns without dividends, so they underestimate the actual returns.

Even without dividends, we can see the following:

- Next 20 trading days (roughly 1 month) — the average return was 9.0 per cent and 7 of 8 were positive.

- Next 40 trading days (roughly 2 months) — the average return was 12.3 per cent and 8 of 8 were positive.

- And the next 60 trading days (roughly 3 months) — the average return was 10.6 per cent and 7 of 8 were positive.

- Next 260 trading days (roughly 1 year) — the average return was 28.7 per cent and 7 of 8 were positive.

- Next 720 trading days (roughly 3 years) — the average cumulative return was 50.1 per cent and 8 of 8 were positive.

Watching history unfold over the past few weeks (the market has gone from 52 week highs to 52 week lows in 20 days for the fastest bear market ever) and fielding questions about what to do reminds us of an old zen proverb:

A student went to his meditation teacher and said, “My meditation is horrible! I feel so distracted, or my legs ache, or I’m constantly falling asleep. It’s just horrible!”

“It will pass,” the teacher said matter-of-factly.

A week later, the student came back to his teacher. “My meditation is wonderful! I feel so aware, so peaceful, so alive! It’s just wonderful!’

“It will pass,” the teacher replied matter-of-factly.

In a recent post about the current carnage Nick Maggiulli remarked that:

“In bear markets, stocks return to their rightful owners.”

We like you have found the speed of this drawdown to be particularly distressing, but we believe that it will pass. Life will go on. Humanity will prevail and we will thus take our chances in becoming one of the rightful owners.

Every economic shock leaves a legacy. Covid-19 will be no different.

Missed a Post? Here's the Last 5:

- Late-Capitalism and Gratitude

- How did we do in 2019? Sell in 2020?

- What Are We Wrong About Today

- Haters Gonna Hate

- Man's Inability To Sit Quietly In A Room Alone

- The Disciplined Pursuit of Less

Keep healthy, stay safe and best wishes to you and your loved ones during these trying times.

Logos LP

Interdisciplinary Value Investing.

www.logoslp.com/