In this video, hedge fund managers, Kevin Smith and Tavi Costa, share their current macro views. Today is far and away the biggest speculative mania and most over-valued US stock market ever.

Are We In A Speculative Mania? – Crescat’s Macro Trade of The Century

Q4 2019 hedge fund letters, conferences and more

Transcript

We're here today really to talk about the marco, what we call the macro trade of the century, it's going to be about a 45 minute presentation. And I want to emphasise that I've been in industry for 28 years, and I've managed money through the tech run up and the tech bust through the housing bubble and the global financial crisis.

And today is far and away the biggest speculative mania and the most overvalued US stock market in history that I have ever seen, certainly in my career, and in history, as our data is going to show here in this presentation. At the same time, we have the biggest debt bubble ever in any country in history in China today, and it's one that we believe has already started to implode.

And that will, that will be globally contagious. And and the really the third leg of our macro trade of the century that we're going to be talking about here is precious metals, and we believe that precious metals represent an incredible value opportunity today. So I'ma turn it over here to Tavi to talk about our macro model.

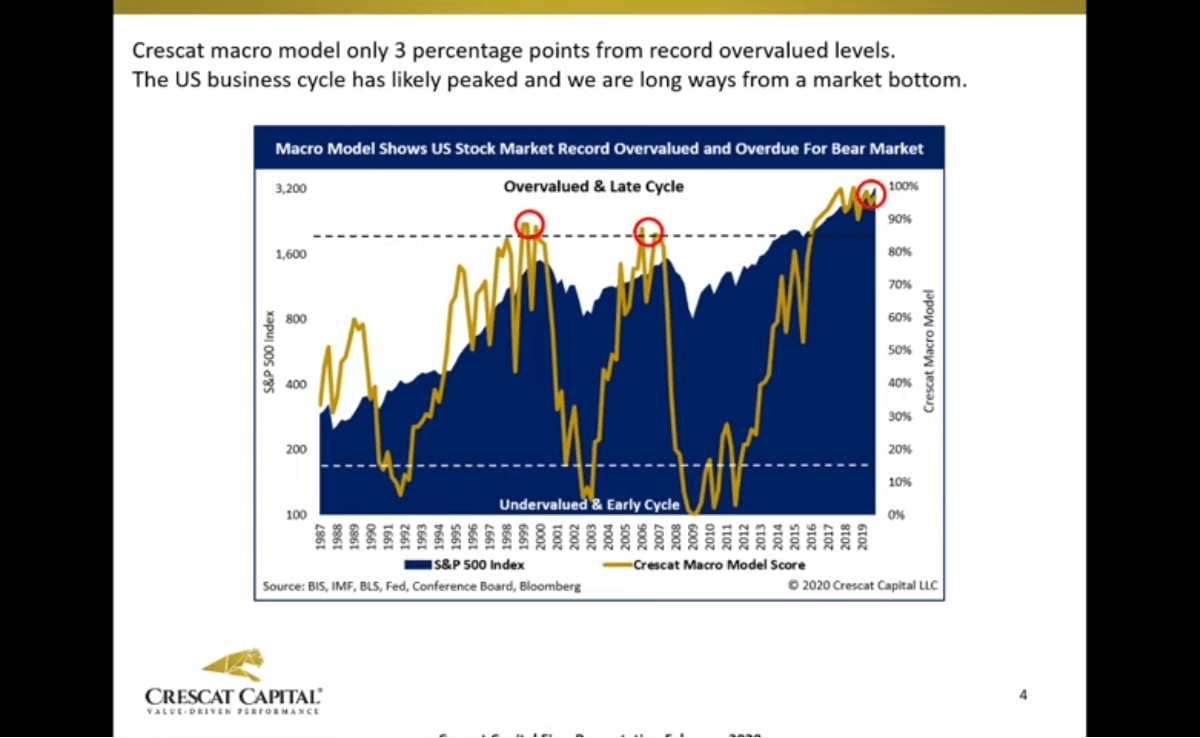

Yeah. So this is a 16 factor macro model that we created a few years ago. That's on your yellow line there back testing all the way to the 1980s. As you can see, it really includes a lot of macro indicators and fundamental factors and a few tackling because it's actually fairly simple model. The idea here is that this model kind of predicted the peak in the bottom of previous cycles as you can see there in the chart too.

But this time, we reached the overvalue in late cycle levels in late 2015. Right when emerging markets are bursting and you saw a tonne of, of oil prices are declining significantly, and then the Federal Reserve raised interest rates in December and equity markets fell apart.

And this this model didn't really predict the recession this time for a few reasons. We didn't have backing in that in those days in late 2015 that the level of yield curve inversions that we have today and some other cracks in the labour market. markets and consumer confidence as well that we would like to discuss today.

What this model really got is that macro indicators since then have been deteriorating significantly. And business fundamentals have weakened also significantly and valuations now are truly have truly reached record levels. And we think that this disconnect between asset prices in this disruptors in an economy are really unsustainable.

So I'd like to talk here about we about eight fundamental measures that we track some of the two of these go back to the 1800s. And, and when you look at the composite of all eight fundamental valuation measures for the US stock market at large and and for the s&p 500, we are at the most overvalued stock market that we've ever had.

It is truly a speculative mania. And you know, whether it's median EV to sales us total market cap to GDP, these measures are higher than the tech bubble. We believe they're higher than 1929. You can look at cyclically adjusted D which is the Shiller cape ratio or, or john husband's margin adjusted cape ratio, which all which, you know those to go back tonight to the 1800s. And we have. So what we have is is literally a mania today in valuations.

But it's not just that it's not just the mania valuations, it's it's all the timing cycles that go along with it, which we'll be getting into. This, this chart here shows that the EV to sales for the median stock in the s&p 500 and it is twice as high as it was at the at the tech bubble peak.

Market valuations are red

And at the peak of the housing bubble in 2006. Median EV to sales, it shows the breadth of the overvaluation and enterprise value includes debt and the capital structure of the firm. A lot of people just look at the P e ratio and the ease don't even factor in in debt. So anyway, this is just one one factor. I'm gonna turn this over here to Tobi.

Yeah. This is another chart that you can see this sort of overvaluation on the breakfast side of the market overall. And this is just looking at aggregate EV to sales. But now, you know, you're looking at more selective into into sectors. And there's 11 sectors today. And if you look back and how different this is today is that the tech bubble We've had a few sectors are very overvalued, like they had the technology sector, you had the communication services sector, the industrials. The hhousing bubble was more of the home builders you got some banks are very overvalued.

Stock market bubble

And today what we have is is is actually eight out of 11 sectors are above the 90 percentile historically of easy to sales. Important think with the V to say is why we like to look at EV is because is because those companies have a lot of leverage. They have a lot of debt. And that's important to include an evaluation basis here when you're comparing throughout history.

I'll turn this over to Kevin again. So one of the factors in our macro model here is Is is consumer confidence and consumer confidence is a contrarian indicator A lot of people think, oh, the consumers doing so well that means the economy is great. Well, at the peak of every cycle consumer confidence is that a cyclical high. And one thing we like to look at is two components of the Consumer Confidence Index, which is the future expectations versus the present situation.

Speculative mania driving growth

And when that that future expectations component starts to slip and diverged. From the present situation, it's been an uncanny indicator for the peak of its stock market and the top of a business cycle. As you can see that the s&p 500 on that panel below, the recession's are shaded, and in every time you get it as strong divergence, where as we are today, it is literally the peak of a cycle.

Now let's talk about what holds the key of the business cycle in general and that is the consumer confidence in the labour market. Those two things have not really correct Yeah, least into 2019 even though a lot of other fundamentals macro has been deteriorating since then. And I think this is an important chart because it's looking at the ratio of the two. And and those are very contrarian indicators. If you think about it a very reliable throughout history, consumer confidence tends to be at its peak at the peak of the cycle and labour market tends to be very strong at the peak of the cycle or unemployment rate tends to be very low. We're close to a 50 year low unemployment rate today.

And now when you look at this ratio between the consumer confidence of Conference Board relative to unemployment rate, the youth unemployment rate, we're now retesting the peaks of the tech bubble and the 1970s recession, you know, How good can it get? That's I think that's the idea of this chart in a way.

Speculative mania driving debt

So one thing that you want to that we're looking at here is that when you look at pre tax corporate earnings for the economy as a whole, this is the corporate earnings that goes into the GDP numbers. They have been essentially flat for the last five years and now and now they've started to dip so yeah We had the tax cuts in 2018. And and that helped the bottom line but the overall underlying fundamentals and when in terms of corporate earnings for the US economy has been flat for five years and it's now declining. At the same time as as the stock market has just raged to to new all time highs and multiples have gone to it to record levels.

Align with that with the earnings picture here for companies overall, I think this chart is incredibly important because it goes back to looking at the cracks in the labour market. And you can see here, just a more broad way of looking at equity markets looking at Russell 3000 aggregate of epcs year over year change and you can see there there's now earnings are not growing anymore on that base, it's actually starting to contract in you can see how that follows us job opening so closely and us job openings as we've been pointing out for a few months already. It's been plunging. It also follows GDP Growth very closely, and also suggests is a massive deceleration in GDP growth.'

Speculative mania in economy

But the labour market, there's other cracks that we see in the labour markets. Look at this one just looking at continuing jobless claims, year over year change that recently just went above zero. In other words, it's now rising. And it's the first time that that happens since the Great Recession, that we've had a few false signals signals. But you know, when you start aggregating all the signals of showing the things that that have happened prior to other recessions or prior to other downturns, you have to start getting more concerned.

This this indicator actually follows unemployment rate very closely the changing unemployment rate, which is extremely important. We haven't seen you three unemployment rate going positive on a year over year basis. Yeah.

And this has a point 97 correlation with with the unemployment rate and I think this is about a change here very soon. And another thing that has been happening with the cheap money caused by central bank's policies overall And, and so forth. It's been you know, as being kind of flooding the markets of venture capital and private equity overall.

Speculative mania in venture capital

And Bloomberg does a great job looking at venture capital barometer that that looks at financings for for those companies activity is in terms of exits of those deals and, and volume of those deals as well. And it has been plunging actually really peaked in June of 2019.

It's down over 40% since then, and coincidentally, actually, and Mark exactly the peak when, when the war situation began to kind of unfold if you all remember, that was also the time when you had a bunch of sort of the bus IPOs of you know, Uber lift, beyond me and so forth.

It was actually at the same time but we're seeing here is not a one company factor. It's not just because of we work, you can see volumes drying up significantly. And again, that has to tie it up back to to to labour markets. Because if you have startups, activities slowing down or falling apart in a big way well that's that's going to have an impact in labour markets as well.