RGA Investment Advisors commentary for the second quarter ended December 31, 2019.

Q4 2019 hedge fund letters, conferences and more

2019 saw the S&P register a 30% total return. In isolation, this looks like a banner year, and it sure was; however, when we take a step back and look at the market’s two-year stack the reality is far more normal. Thus is the nature of markets: moves happen in lumps and one must zoom out to find some semblance of an orderly trend. Instead of thinking about the 30% return, we can look at the annualized return since the start of Q4 in 2018. From that lens, the S&P has returned an annualized 10.82% since the first day of Q4 2018. This level of return is consistent with the long-term price trend of the index. All that truly changed along the way was sentiment.

Markets across the world looked awful heading into 2019, despite a brief reprieve that commenced promptly on Christmas Eve 2018. At one point, the S&P was within one fifth of one percent of a “Bear Market.” Alas, those who live on proclamations such as “this is the longest bull market in history” can still make the claim because of a mere twenty basis points.[1] This is the second time in the Bull Market that started in March of 2009 where the S&P came within one percent of hitting “Bear Market” territory (the first having been 2011’s -19.4% peak to trough move). Just imagine how different today’s narratives would be had things moved slightly further in the wrong direction one random afternoon.

Labels, as such, are great for selling headlines but have little value for us investors. Does the longevity of the Bull Market mean anything in and of itself? Had we registered a 20% correction in 2018 instead of a 19.8% correction would prognosticators bemoan the “maturity” of this Bull Market? Another common refrain is about how expensive stocks look today. We concluded our end of 2018 introductory section with the following point that is worth repeating today:

In the end, 2018 marks one of the biggest one-year declines in the forward P/E in the past few decades fueled by a combination of strong realized earnings growth and a decline in the stock market. Some of the earnings growth was the sugar rush from tax cuts, though a healthy amount was realized via higher revenue growth. While one might call the early 2018 levels “the upper end of fair value,” today is on the lower end of the fair value range. Yes, we have been below these levels, but they were in far different environments. This makes now a compelling time for long-term investors to put money to work.[2]

While last year ended at the low-end of the valuation range, 2019 saw the pendulum swing back to the high side when looking just at the market’s P/E (what we have lovingly called “Mr. Market’s mood indicator” in the past). Even looking at P/Es can be a little misleading however, given the following visual which is especially helpful in contextualizing where things stand:

[3]Yes, when we look at traditional valuation metrics (like P/E), stocks do appear expensive on an absolute basis. However, pay attention to the bottom two lines in the above table for the one relative (in contrast to absolute) valuation metric: stocks are on the historically cheap end of the spectrum relative to the 10-year Treasury yield. Importantly, stocks are exactly in the middle of the long-term range with respect to “free cash flow yield.” The contrast between P/E ratios checking in at the 88th percentile and free cash flow yield at the 53rd percentile is one of the most interesting realities of markets today. This contrast speaks far more to the nature of today’s leading businesses and the composition of earnings than it does what the market itself is doing. Over the past decade, companies like Circuit Cities, Countrywide Financial, Lehman Brothers, RadioShack and KB Home have been replaced in the S&P by the likes of MasterCard, Intuitive Surgical, Salesforce, Booking and Blackrock. Is it any wonder that while earnings might appear lower on a per share basis overall that cash flows are much better? The S&P is built to evolve with the times. As older industries struggle, shrink and inevitably perish they get replaced by the younger upstarts, with better growth dynamics and different business models. These compositional changes tend to happen gradually; however, the financial crisis accelerated the pace of change. Today we are witnessing the consequences.

New Business Models, New Opportunities

The last time we called out a group of companies who shared similar traits was in our January 2016 commentary entitled “Robust Networks for the Long Term.”[4] We see something similar developing today. On the one hand, the market has been enthusiastic about new business models, rewarding them with rich valuations, while on the other hand, a certain subset of companies with distinct properties seem neglected. Two kinds of companies stand out for stellar performance last year:

- Companies with no earnings and rapid growth.

- Companies with low growth, high free cash flow and high repurchase yield alongside perceived “safety.”

In the middle is a third type of company that got left in the dust. In some respects, the Dow Jones Internet Composite Index holds many companies evincing these traits. In 2019, the composite as represented by the First Trust Dow Jones Internet Index (FDN) returned 19%, well less than the market’s 30% returns. This index includes 40 holdings listed below:

[5]Some of these companies have unique problems, while others are strong. By and large, the traits that bind these companies together beyond the “internet” being core to their business model are as follows:

- Descent though not other-worldly growth rates (think high single digits up to 20%)

- High and growing operating margins (>15%)

- High free cash flow yield (the consolidated index boasts a 4.5% free cash flow yield, greater than the S&P at 4.1%)[6]

- Over-capitalized balance sheets

Taken all together, you have an index with faster growth than the market and lower valuations, operating in the new economy, yet with somewhat extreme underperformance. Clearly this space looks like fertile hunting grounds for investors with a growth at a reasonable price (GARP) bias. Several companies in the FDN ETF have been in our portfolios for years, though we added a few more of these kinds of companies in the last quarter (most are in the actual holdings list above, the exception we are adding boasts all of the same traits but cannot be included due to its low float). Here are the companies in alphabetical order:

- Alphabet (GOOGL)

- ANGI Homeservices (ANGI)

- Dropbox (DBX)

- eBay (EBAY)

- Grubhub (GRUB)

- PayPal (PYPL)

- Twitter (TWTR)

For the remainder of this letter we will dive into four of these positions, two of which because they are new to our portfolio and two because they suffered especially poor returns in the fourth quarter, deserving some attention and reflection.

ANGI: The House Isn’t The Only Thing Getting Fixed

Barry Diller and IAC have an incredible history of nurturing and growing companies who are digitizing the offline world including stalwarts like Ticketmaster, Match.com, and Expedia.[7] In 2004, IAC acquired ServiceMagic before rebranding the company to HomeAdvisors in 2012. In May 2017, HomeAdvisor acquired Angie’s List and the company (“ANGI”) was listed publicly with IAC retaining ownership of over 80% of the combined company. ANGI provides digital marketplaces for home services. It connects service providers (“SP”s) with homeowners in need of service requests (“SR”s).

Each marketplace match performed by ANGI throughout the years has provided a datapoint for a price on a specific job in a specific geography. ANGI currently has the largest database for job pricing in the United States. Although ANGI was not initially sure what the benefits of this database would be, the company is now deploying this information to offer transparency and in some cases, a fixed, fair price for projects in 133 specific verticals in certain zip codes, leveraging a strong data moat into a unique offering for homeowners. ANGI’s CEO William Ridenour explains:

So one of the opportunities I see, and this is a huge area of concern for homeowners and consumers, be — the fear of not getting a fair price. … And the difficult part is nobody knows what a fair price is. … So we think that there’s an opportunity to actually, as a brand and as a service, become this reference point for home services pricing, with the idea that before you buy, check to make sure you’re getting a fair price, an easy, fast, digital way to see what you can get that service for.[8]

This strategy is a key building block for ANGI’s efforts to increase mobile app usage, create a fixed price booking platform, and ultimately increase the number of service requests per customer. As the product improves, customer loyalty improves, adding to ANGI’s already lush cash flow generating capabilities. ANGI is currently investing significant cash flow into customer acquisition and earning slightly above a 10% free cash flow margin despite these considerable investments. If ANGI can use improved loyalty to migrate customers onto the mobile app and away from the rising toll Google charges for traffic, the company could generate considerable leverage on the over 50% of revenue it invests in sales in marketing (40% of that S&M expense goes directly to customer acquisition).

In addition to customer acquisition, sales and marketing investments are funding the growth of the SP network. As ANGI evolves from lead generation, to a managed marketplace, to a fixed price platform, the importance of growing SP supply only increases. ANGI currently has the largest supply of SPs in the market which creates a challenging barrier for competitors to overcome. A fixed price platform with price transparency should catalyze SP engagement since it would lower barriers for SPs to land jobs in a cost-effective, time-saving way.

Platforms provide network effects as they grow, and network effects would grow margins meaningfully. Even if margins only expand by 200 basis points per year and sales growth is less than half of what management expects over the next five years, ANGI should be valued at $12.60 a share based on a DCF, 60% above the price at which we made ANGI a position in our portfolio independent of our holding in IAC. ANGI is at least a couple years away from an adoption inflection in the fixed price platform given the early stages of implementation. As such, the exciting benefits of the fixed price platform were not baked into the base case and left as an asymmetric source of upside. In our base case DCF for ANGI, we use a 16% CAGR on the top line for 6 years (well below the company’s 20-25% target range) and a terminal EBITDA margin of 26% (decently below the company’s 35% long-term target). These assumptions result in a value for ANGI of $16.00 per share, over twice the price we initiated the position at.

Dropbox-Storing Files and Saving Time

We have long admired Dropbox for how it facilitated the operations side of our business at RGAIA. As many of you have experienced, we can securely share files, with HIPAA/HITECH compliant encryption, password protection and links that expire, without ever attaching sensitive documents to an actual email. Many people were first exposed to Dropbox through the free, limited space offering that spread virally amongst certain peer groups. Through virality alone, Dropbox has built up a universe of 600 million users, 360 million of whom are “potentially monetizable” in either their personal or business capacities. The virality of the product affords Dropbox a major advantage in customer acquisition.

Dropbox is a classic example of a company that stayed private for too long only to come public when growth was slowing and questions about competition intensifying. Some contend that the cloud storage space has been commoditized by Google, Microsoft, Apple and Amazon offering competing services to Dropbox, bundled into broader suites and as such, “free” to the customer. Although there is some merit, especially in the retail photo-sharing and saving market, these concerns miss how valuable Dropbox’ suite of services with greater power and flexibility have become in the workflow of small and mid-size businesses. We have often expressed an affinity for pure-plays against large, well-capitalized competitors due to the contrast of having a product be one’s essence versus one’s unit. This further helps Dropbox vis-à-vis the technology giants as the company’s engineering-centric culture further iterates and improves its product suite while competitors rely on free being “good enough” for the customers who use it. In the storage market, there is room for both.

There is a misperception due to the viral origins of the product that most users are individuals, when in fact 80% of Dropbox users deploy the product primarily for work, with the remainder personal. On the surface, competing with free looks like a losing battle; however, in reality,Dropbox’ suite ends up priced as a tiny cost in a typical business’ operating budget and its better UI/UX as a product saves time in quantifiable ways. Its robust tools for control are crucial to businesses in regulated industries and its fluidity in sharing is a true differentiator from mere “storage” in collaborative industries like architecture, sales, engineering and inventory management. In the third quarter, Dropbox reported that the average user paid $123.15. While this number is clearly more expensive than free, it can be contextualized as follows: according to the BLS, the average worker in the US earns $28.32 per hour of work, while the average information worker earns $42.34 an hour.[9] If the advantages of Dropbox over the competition save the average worker 4.3 hours in an entire year or the average information worker 2.9 hours in a year, Dropbox pays for itself. With a better product suite, the bar is not too high for Dropbox to deliver a demonstrable benefit over the large scale, unfocused challengers.

The greatest evidence that Dropbox is meeting the needs of its customers stems from both its ability to raise prices as a growth lever alongside declining churn in aggregate. Dropbox recently raised the price of its Plus plan by 20% and while the company suggested it might slow net new customer additions for the next several quarters, there has only been a modest uptick in churn.[10] Customers already onboard clearly recognize the value. To make the price increase more palatable, they executed the price hike intelligently, along with doubling storage capacity and adding functionality like restoring folders and/or files to past dates. Dropbox benefits from multiple growth levers, including the aforementioned pricing power, along with opportunities to lower churn, improved conversion of free to paid and more products like Paper and New Dropbox.

With net revenue retention in the mid-90s and customer retention in the mid-to-upper 80s (probably higher but think mid-90s less mid single digits ARPU lift), at today’s $6.6 billion enterprise value, assuming a 7 year average customer lifespan, you are buying the value of the existing customer base with any growth essentially free on top. If that lifespan drops to five years, there would be 15% downside; however, given that the company will have grown its user base in the low teens in 2019 and users will grow base case in the high single digits in 2020, we see a margin of safety in the churn assumption. Dropbox is a Rule of 40 SaaS company[11], with a commitment to the market of expanding margins as growth moderates. If growth reaccelerates, they will be able to maintain margin. When adjusting free cash flow for duplicative headquarter expenses that will end in 2020, the trailing free cash flow yield here is over 5.4%. Rarely does one find companies growing so much faster than the market with a higher free cash flow yield. Founder Drew Huston showed what he thinks of the stock this fall, buying $10 million worth on the open market.With an over-capitalized balance sheet and some clear frustration with the stock’s performance, perhaps the company considers commencing a largescale repurchase program in the coming year.

Grubhub-Eat or be Eaten, The Story of an Upset Stomach

We revisited our thesis on Grubhub in our Q1 2019 commentary and events have not played out as hoped. We want to take this as an opportunity to share some lessons learned and our reassessment of the thesis from here. We simplified our thesis in Grubhub with an intense focus on “economic parity” which we explained as follows: “ Grubhub could reach what they call “economic parity” between marketplace and delivery orders as measured by EBITDA per order, leaving the platform agnostic, the diner indifferent and the restaurant empowered to choose the model that best fit its own needs.” Unfortunately while Grubhub did achieve a number nearing economic parity in Q3 2019, the level of parity was well below where the marketplace had been trending largely a consequence of growth slowing well below management’s and our expectation. Such is the nature of businesses with serious operating leverage. In the future, we will focus our simplification efforts on situations where there is a distinct qualitative tie-in to the customer relationship. This means we will either isolate on a revenue driver (as we did with engagement on PayPal) or a margin item with a direct customer nexus.[12]

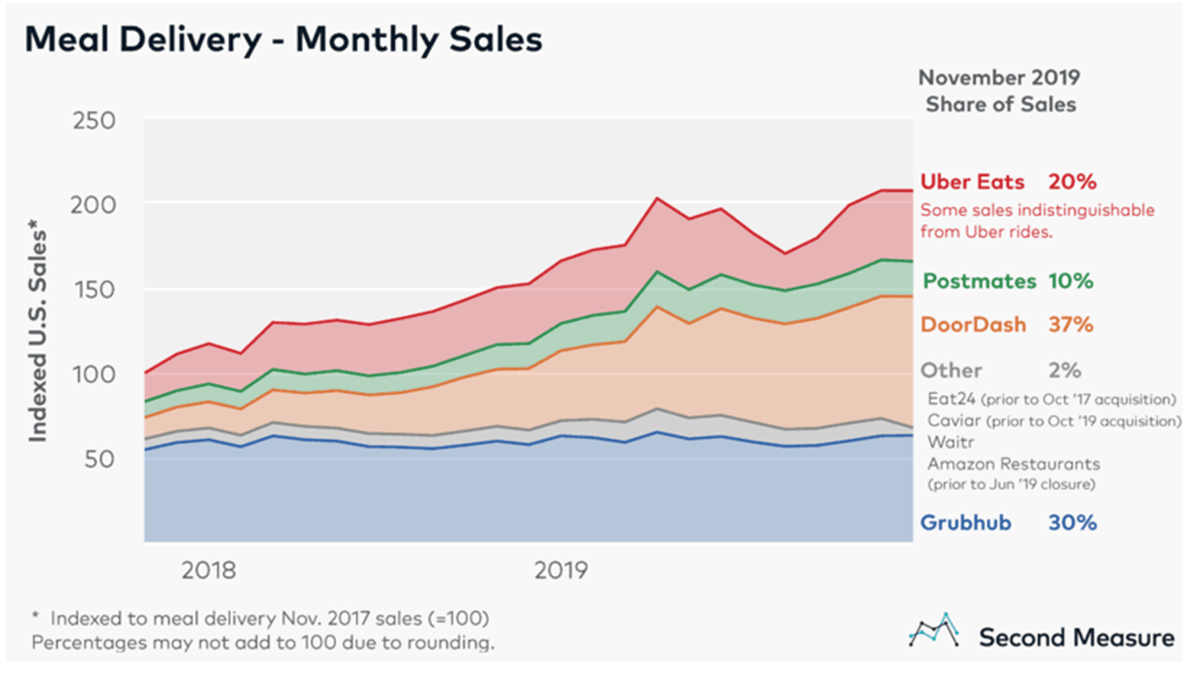

Alongside the disappointing results, management issued a unique shareholder letter analyzing the history of the nascent online delivery industry and the competitive landscape today, blaming increasingly “promiscuous” behavior from diners due to promotional activity at competitors for the problems. In response, management made the case to shareholders for pursuing a “scorched Earth” strategy whereby Grubhub would spend (invest?) its own cash flows just at the moment when competitors like UberEats and Doordash were attempting to delivery on promises to its current and prospective investors for a path to profitability. It is difficult to determine whether the Grubhub move is offensive or defensive in nature. It is offensive insofar as the company is attempting aggressively to win diners; however, it is defensive for how it aims to keep competitors in a grinding battle defending their core markets instead of spending more aggressively to fight Grub on its own turf. Essentially the battleground in this delivery war has been primarily second and third tier cities—the new frontiers of growth—while marketshares in the Northeast have remained largely stable for Grubhub.

[13]Upon hitting “send” on this letter, whether they knew it or not, management commenced a tectonic shift in the food delivery landscape. In Europe and around the world, a wave of consolidation is taking place in the industry, while the US has thus far been mostly immune (Doordash taking over Caviar aside). With the sharp reset in Grubhub’s stock price, the economic accretion available to those with larger market caps in the industry looks increasingly attractive. Taking a glance at the city-by-city breakdown shows the clearest opportunity in Grubhub’s stock today: With 67% of New York City marketshare (with an over-representation to Manhattan itself), whoever acquires Grubhub between Uber and Doordash will own 80% of the single most valuable delivery marketplace in the country. 80% is a magic number first noted by Italian economist Vilfredo Pareto in what is now known as the “Pareto Principle.” If one player achieves 80% share in NYC they will likely generate over 100% of the EBITDA in that one key geography. At the October 30th closing price of $34/share, Grubhub was trading for a discount to the standalone NYC value. NYC alone generates upwards of $250m in EBITDA which gets reinvested within the company to other growth initiatives. What choice do those with broad aspirations in the sector have but to give an acquisition a look?

The list of potential acquirers is deeper than just the two main US competitors. Prosus, a Naspers carve-out with a focus on the food delivery space has large, global ambitions.[14] Strategic acquirers range from big tech companies to super market companies. Most logically we think someone already in the industry, who is bleeding cash but wants to grow, will find the ridiculously high cash flow margins of the core marketplace business a crucial piece in achieving their own aspirations for profitable, cash flowing growth. While the recent path in this stock has been turbulent, we still remain sanguine on a constructive outcome.

Twitter: Will this bird finally set sail?

In many respects, Q3 2019 should have been cause for a chest-thumping victory lap at TWTR. Account growth, as measured by year-over-year monetizable daily active usage (mDAUs) slowed to the single digits in the second-half of 2018. In Q3 2019 this number registered 17% year-over-year growth, the fastest rate of mDAU growth in at least three years. With pure inertia it will end the year closer to 20%. Notably, this acceleration happened without any major events or catalysts to spark engagement, on top of a tough comp with the World Cup having occurred in the same quarter, last year. Historically, the stock has moved based on the trend in mDAUs; however, this past quarter’s report came with a new problem. Twitter was inappropriately using data for personalization on accounts who had opted out of data collection and Twitter shared data with mobile application promotion (MAP) advertisers it should not have shared.[15] These problems collectively stem from a lack of investment in revenue product while the company was laser-focused on enhancing the user experience.

MAP in particular is a big revenue product in Japan, which is Twitter’s second largest market after the US. ARPU in Japan was thus down meaningfully, dampening the impact of the mDAU acceleration. Our analysis shows that while the US ARPU will actually be up somewhere around 5% in 2019, International will be down 3.4% and Japan in particular will be down over 12%. In a loose sense, it might be fair to suggest these problems are isolated and they open up intriguing possibilities. Improving the demand response product is a major opportunity that will now get the attention it deserves:

But what can we do around direct response and bringing more advertisers to the service? So our MAP work should lead to more direct response-type opportunities over time. And in terms of bringing more advertisers to the service, we have a nice business where we help smaller advertisers in reaching their customers on Twitter, but that’s not an area that we have prioritized improvements around in the recent past. It’s a place where we know that there’s millions of small businesses throughout the service, where we could help them more in reaching their customers on Twitter. But we’ve got to do the engineering work and make the case to them better than we are today. And right now we’ve chosen to prioritize other things first.[16]

Twitter has a fair reason for putting off the redevelopment of direct response revenue products. The platform is well-established for brand building and product launches; however, that might have been at risk had the company not achieved measurable progress on safety and user growth first. If they put demand response ahead of user experience as a priority, they might have lost this crucial support (and budget) in the advertising community and considerable revenue, which would have rendered any progress futile. Now that the company has a growing user-base story once again, we think it is only a matter of time for revenue to follow.

From a valuation perspective, the Twitter only needs modest ARPU growth in order to support today’s prices. We like backing into the market’s implied expectations and using 2.7% ARPU up-lift per year, for eight years (well below the trend of the last three years) Twitter’s user growth would need to track the yellow line in the following chart in order to justify today’s market cap:

Importantly, the yellow line today is in the process of accelerating and it is rare that these things so swiftly reverse. This is especially so with 2020 being an Olympic and a US election year.

Meanwhile, the opportunity on ARPU remains relatively untapped. We think one of the single biggest opportunities for Twitter is launching paid feeds whereby instead of merely “following” another user, someone could “subscribe” to a feed and Twitter could take their cut for building the infrastructure to make it all work. There are companies who do this over Twitter’s rails, like Premo Social, for an all-in take rate of about 13%.[17] This would be an intriguing revenue opportunity considering most Internet revenue at the giant Internet companies comes from advertising. A subscription-based take rate would be far less volatile, far more consistent and open the door to all kinds of serendipity for the platform.

The hurdle for success on the existing business here is set very low. Should the acceleration in mDAUs persist, the stock would be worth upwards of $60 without any ARPU recovery. If ARPU recovers its swoon and returns to a 5% growth trend, this is upwards of a $70 stock. New paths to monetization are pure optionality. Taken as a whole, Twitter is one of the most compelling risk/reward opportunities we have seen.

Where it all goes from here:

It is impossible to know what the market will do from year-to-year and what kinds of stocks the market will take a liking to. What is knowable is that over the long run, stocks are worth the discount of their future cash flows. These companies we discussed today all share many common traits that lend themselves to good future returns including: 1) low starting valuation; 2) high margins and 3) good growth tailwinds. While these companies in many respects share a lot of similarities, importantly, the key drivers of their revenues are all unique. ANGI connects homeowners and service professionals, Dropbox is a service for small and mid-sized businesses, Grubhub connects diners and restaurants and Twitter is the modern associated press and interest network for the masses. In other words, none of these companies will be reliant on the same macro forces to drive their profitability, while all are in advantaged areas ready to move key offline processes to the digital world.

These companies also share another important trait with respect to their institutional imperative. Companies with no profits and rapid growth are incentivized to pull the growth lever and gear their organizations accordingly. In effect, one can say the objective of such companies is to grow. These companies we are highlighting do exhibit growth; however, their institutional imperative is far more balanced: they are incentivized to deliver both growth and profitability. Companies that understand the tradeoff between growth and profitability gear their organizations towards achieving profitable growth. Growth then becomes about scaling proven unit economics instead of goosing the top line at all costs. It is important for management teams to effectively communicate how they think about these tradeoffs to their shareholder base.

One reason Grubhub has been so volatile is how poorly the company has managed communication with a shareholder base focused on margin, in a competitive landscape dominated by companies whose owners are pushing for growth at all costs. Grubhub’s institutional mandate put the company at odds with the demands of its industry; however, the company’s profitability in core markets provides the financial lifeline necessary to know life will persist even when the regime shifts. Market regimes will inevitably shift the extent to which they reward growth and that will be painful for companies who have not yet created pathways to profitability with talent and staff who understand the precise balance between the underlying levers that drive the tradeoff.

Growth-at-all-cost companies can prove their ability to grow, though they cannot explain, nor can investors determine whether they are merely growing, or scaling proven unit economics. When companies exhibit both growth and profitability, there is implicit evidence the unit economics do work and that scale can deliver more profit long-term. Further, profitable growth companies have the added financial flexibility and runway necessary to experiment with ways to improve their offerings and accelerate their growth in out-years while profitless growth companies will spend their time figuring out how to turn $1 of revenue into some degree of margin.

Thank you for your trust and confidence, and for selecting us to be your advisor of choice. Please call us directly to discuss this commentary in more detail – we are always happy to address any specific questions you may have. You can reach Jason or Elliot directly at 516-665-1945. Alternatively, we’ve included our direct dial numbers with our names, below.

Warm personal regards,

Jason Gilbert, CPA/PFS, CFF, CGMA

Managing Partner, President

Elliot Turner, CFA

Managing Partner, Chief Investment Officer

[1] https://www.cnbc.com/2019/11/14/the-markets-10-year-run-became-the-best-bull-market-ever-this-month.html [2] http://www.rgaia.com/2018-year-end-investment-commentary-easy-come-easy-go/ [3] Eye on the Market Outlook 2020, JP Morgan Private Bank. [4] http://www.rgaia.com/robust-networks-for-the-long-term/ [5] Bloomberg [6] Free cash flow yield as of 12/31/19 https://www.ftportfolios.com/retail/etf/etfsummary.aspx?Ticker=FDN [7] https://moiglobal.com/elliot-turner-201806/ is a link to a presentation on IAC we gave in 2018 [8] ANGI HomeServices Inc at Credit Suisse Technology, Media & Telecom Conference [9] https://www.bls.gov/news.release/empsit.t19.htm [10] https://www.theverge.com/2019/5/31/18647053/dropbox-storage-increase-price-plus-watermarking-smart-sync-rewind [11] Rule of 40 in SaaS is defined as Sales Growth + EBITDA margin exceeds 40%. [12] http://www.rgaia.com/wp-content/uploads/2019/01/PYPL-and-ROKU-Best-Ideas-2019.pdf, Slide 12. [13] https://secondmeasure.com/datapoints/food-delivery-services-grubhub-uber-eats-doordash-postmates/ [14] https://finance.yahoo.com/news/prosus-still-chasing-food-deals-133837837.html [15] https://adexchanger.com/data-exchanges/limits-on-targeting-hurts-revenue-just-look-at-twitters-unfortunate-q3-earnings/ [16] Ned Segal, Twitter Q3 Earnings Call, 10/24/19, Sentieo. [17] https://premosocial.com/

Past performance is not necessarily indicative of future results. The views expressed above are those of RGA Investment Advisors LLC (RGA). These views are subject to change at any time based on market and other conditions, and RGA disclaims any responsibility to update such views. Past performance is no guarantee of future results. No forecasts can be guaranteed. These views may not be relied upon as investment advice. The investment process may change over time. The characteristics set forth above are intended as a general illustration of some of the criteria the team considers in selecting securities for the portfolio. Not all investments meet such criteria. In the event that a recommendation for the purchase or sale of any security is presented herein, RGA shall furnish to any person upon request a tabular presentation of: (i) The total number of shares or other units of the security held by RGA or its investment adviser representatives for its own account or for the account of officers, directors, trustees, partners or affiliates of RGA or for discretionary accounts of RGA or its investment adviser representatives, as maintained for clients. (ii) The price or price range at which the securities listed.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}