Logos LP commentary titled, “How did we do in 2019? Sell in 2020?”, discussing the goal of the quiet ego approach.

Stocks rose slightly on Friday as Wall Street wrapped up a nice weekly performance that featured new record highs for the major indexes amid strong global economic data and a solid start to the earnings season.

Q4 2019 hedge fund letters, conferences and more

Friday’s gains came after Chinese industrial data for December topped expectations overnight, with production rising 6.9% on a year-over-year basis. The overall Chinese economy grew by 6.1% in 2019, matching expectations.

In the U.S., housing starts soared nearly 17% in December and reached a 13-year high. That data follows Thursday’s release of better-than-forecast weekly jobless claims and strong business activity numbers from the Philadelphia Federal Reserve.

Stocks are gaining to start the year with bullish investor sentiment on the rise and the naysayers in sync with calls of an “overbought” market “ripe” for a fall (more than three months have gone by since the S&P 500's last decline of 1% or more back on October 9th).

Meanwhile hedge fund billionaires David Tepper and Stanley Druckenmiller are confident in the current bull run.

Tepper told CNBC’s Joe Kernen in an email: “I love riding a horse that’s running.” Tepper, meanwhile, told Kernen in a separate email he is still bullish in the “intermediate term” in part because of the Federal Reserve’s current monetary policy stance.

A solid start to the corporate earnings season has also provided a supportive backdrop to the market as more than 8% of the S&P 500 have reported quarterly results thus far and of those companies, 72% of companies gave posted better-than-expected earnings.

Our Take

With indexes trading at record highs, the S&P 500 up 13 of the past 15 sessions and with stocks trading at historically high levels versus earnings, expected profits and sales, it is understandable that investors might feel uncomfortable putting more money to work.

Furthermore, as Nick Maggiulli reminds us, investors are faced with the common refrain that markets are “due” for a pullback. The reality is that markets are never “due” for anything. After studying the historical data Nick demonstrates that there is little to no relationship between prior 10-year returns and growth over the next 10 years.

For example, if you look at how the S&P 500 performed over its prior 10-years (starting in 1936) and then look at how it grew in the future, you won’t see much of a pattern.

Interestingly, Nick demonstrates that “while the prior 10 years show little to no relationship with future returns, this is not necessarily true if we look at returns over the last 20 years. Typically, if U.S. markets did well over the prior 20 years, they did poorly in the next 10 years, and vice versa.”

Nick’s research suggests that if history were to repeat itself in some meaningful way, the S&P 500 would be 4x higher by 2030 than where it is today.

Is this such an outrageous prediction given where we stand with persistently low borrowing costs and inflation?

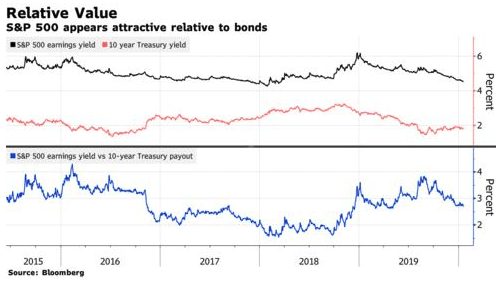

Sarah Ponczek in a recent piece in Bloomberg explored this “new regime for stocks” and found that stock prices have the potential to rise a lot more before reaching valuations that are justified by bond rates. Some suggest as high as 30 times earnings on the S&P.

Near 3,330, the S&P 500 currently trades at 22 times recorded earnings. Getting to 30 times would place the benchmark close to 4,500, a gain of more than 35%.

There is no doubt that buying a quality asset at a low/reasonable price is more attractive than purchasing it a higher price. Yet the more interesting point to be gleaned from the above is that divesting or not investing at all based on the simple adage that ‘The market’s expensive therefore I’m a seller’ rarely works. The market historically has been rewarded with higher valuations when interest rates and inflation are subdued.

Although there are no laws which guarantee the market will follow this historical trend and/or for how long, it is interesting to consider that those predicting a poor decade for stocks ahead may not have the data/evidence on their side…

Stock Ideas

For some of our picks for 2020 please find them on Yahoo Finance here.

Musings

For our thoughts about 2019, our portfolio composition headed into 2020, and our outlook for 2020 please find a copy of our 4Q annual letter to our partners on ValueWalk accessible here.

Charts of the Month

Logos LP December 2019 Performance

December 2019 Return: -0.06%

2019 YTD (December) Return: 37.62%

Trailing Twelve Month Return: 37.62%

Compound Annual Growth Rate (CAGR) since inception March 26, 2014: +15.77%

Thought of the Month

"The world is ruled by letting things take their course.” – Lao-Tzu

Articles and Ideas of Interest

- Banks that shun risky borrowers offer rosy view of the U.S. Consumer. With most U.S. households spending more and paying their bills on time, their creditors are feeling more confident than ever. To hear the CEOs of the nation’s largest banks tell it this week, rarely has the American consumer been in better shape. Nevertheless, these banks may reflect the fact that banks have focused more on the wealthy and those with excellent credit as Nationwide, four in 10 adults don’t have the cash to cover an unexpected $400 expense, according to a 2018 survey by the Federal Reserve.

- Ten charts that tell the story of 2019. The power of a good chart or map lies in its ability to inform the debates and decisions that lie ahead. Here are 10 graphics published by the Financial Times in 2019 where the real story is often about what happens next — in the years, decades and centuries to follow.

- 19 big predictions about 2020, from Trump’s reelection to Brexit. Will Biden win the nomination? Will Netanyahu hang on in Israel? Will global poverty see a decline? The staff of Future Perfect forecasts the year ahead. The future perfect team at Vox weighs in.

- The pressing need for everyone to quiet their egos. Scott Barry Kaufman for the Scientific American suggests why quieting the ego strengthens your best self. We are more divided than ever as a species with anxiety and depression at record highs. What is the answer? The quiet ego approach. The goal of the quiet ego approach is to arrive at a less defensive, and more integrative stance toward the self and others, not lose your sense of self or deny your need for the esteem from others. You can very much cultivate an authentic identity that incorporates others without losing the self, or feeling the need for narcissistic displays of winning. A quiet ego is an indication of a healthy self-esteem, one that acknowledges one’s own limitations, doesn’t need to constantly resort to defensiveness whenever the ego is threatened, and yet has a firm sense of self-worth and competence.

- Why doing good makes it easier to be bad. In an age where corporate “do-goodism” / “corporate social responsibility” is en vogue, you might wonder how people who seem so good in public could be so bad in private. The theory of moral licensing could help explain why: When humans are good, it says, we give ourselves license to be bad.

- What makes a good life? Lessons from the longest study on happiness. What keeps us happy and healthy as we go through life? If you think it's fame and money, you're not alone – but, according to psychiatrist Robert Waldinger in this TED talk, you're mistaken. As the director of a 75-year-old study on adult development, Waldinger has unprecedented access to data on true happiness and satisfaction. In this talk, he shares three important lessons learned from the study as well as some practical, old-as-the-hills wisdom on how to build a fulfilling, long life.

- Why you will marry the wrong person. Alain de Botton for the NYT suggests that though we believe ourselves to be seeking happiness in marriage, it isn’t that simple. What we really seek is familiarity — which may well complicate any plans we might have had for happiness.

- Reports of value’s death may be greatly exaggerated. Many investors are reexamining their exposure to the value style given the extraordinary span—over 12 years—of underperformance relative to growth investing. Given the long historical record of value investing, and its solid economic foundations (dating back to the 1930s and, less formally, dating back centuries), it is unlikely that the period up to 2007 was a result of overfitting. The three other explanations, however, deserve a deeper examination. It is likely that no one story accounts for the underperformance; it is probably a combination of all three. Rob Arnott for Research Affiliates digs in.

- What powered such a great decade for stocks? This formula explains it all. This is a nice follow up to our last newsletter entitled “Haters Gonna Hate”. Market Returns = Dividend Yield + Earnings Growth +/- Changes in the P/E Ratio. Contrary to popular belief, Ben Carlson demonstrates that a vast majority of the gains over the past decade can be explained almost exclusively by improving fundamentals. Yes that's right the market isn’t a ponzi scheme a product of financial engineering, stock buybacks and central bank money printing! Earnings growth and dividends explain nearly 97% of the annual returns for the 2010s. Many would argue the only reason earnings growth has been so strong is because of the massive stimulus we’ve received from low interest rates. Ben isn’t saying valuations haven’t risen in this time (they have). It’s just that they’ve risen in concert with corporate profits.

Missed a Post? Here's the Last 5:

- What Are We Wrong About Today

- Haters Gonna Hate

- Man's Inability To Sit Quietly In A Room Alone

- The Disciplined Pursuit of Less

- These Halcyon Days

{kind=link}

{kind=link}

{kind=link}

{kind=link}