According to FINRA’s 2015 NFCS survey, 40% of people spend less than they earn, while 38% live from paycheck to paycheck. They can live within their means. But 18% spend more than they make and therefore live in debt.

And the numbers say it all. The Federal Reserve’s Consumer Credit G.19 Report (March 2019) has stated that total consumer debt is a whopping $3.999 trillion ($12,169 per capita).

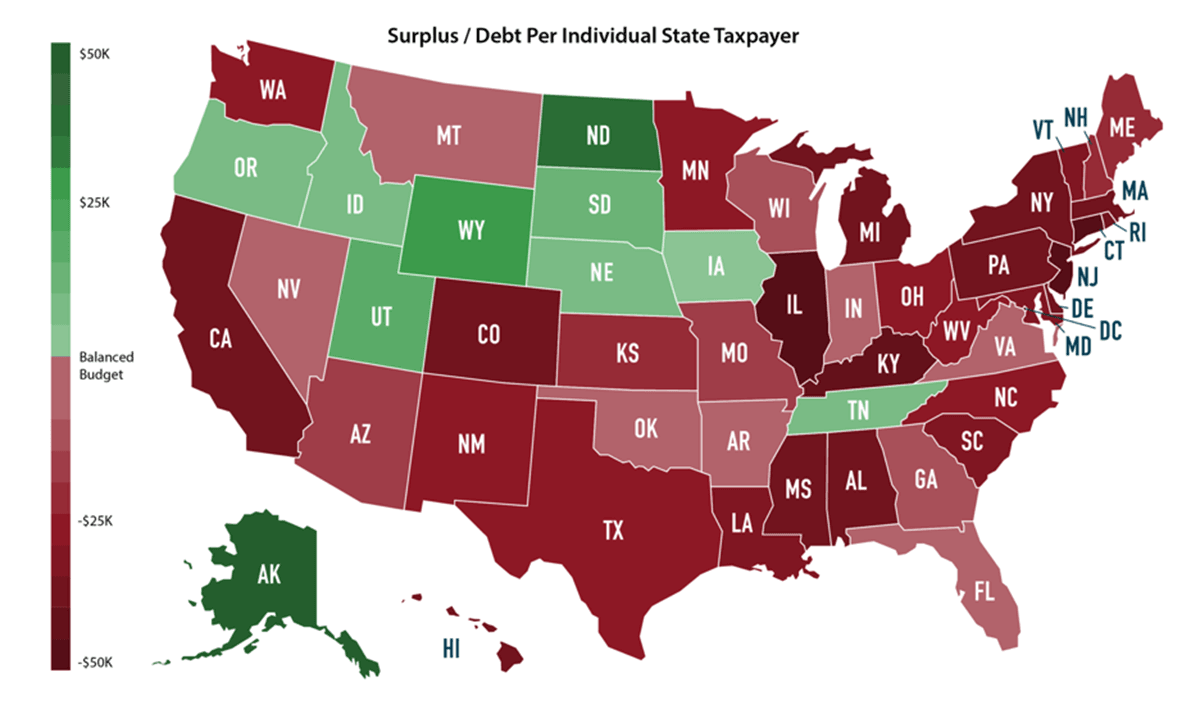

Q2 hedge fund letters, conference, scoops etc

No matter how hard you may try to ignore it, your debt will not magically disappear. So you will always owe money unless you repay the debt.

So how long before debts are written off? Well, that depends on what type of debt you’re dealing with and where you are living.

Source

Types of debt

There are four categories. Each has a set of individual rules, so you should consider which type you are dealing with.

- Oral agreements: As the name implies, there is nothing in writing about the debt, just a verbal agreement.

- Written contracts: Typically, this is the case with most debts. The borrower and the creditor sign a contract. Terms and conditions are written, including the amount, monthly payments, and interest rate, if any. e.g., medical debt

- Promissory notes: A written agreement to repay a debt in installments within a certain date at a specific interest rate. e.g., student loans or mortgages

- Open-ended accounts: This is an account with a revolving balance you can repay and then borrow again. e.g., credit cards or in-store credit

What is a write-off?

Like they all say, “Knowledge is power,” so you need to have adequate information to know where you stand legally. The objective is to get debt-free and stay that way.

Once you acquire a debt, it’s there until you pay it off. It never really gets wiped off, even when you come across the term ‘written off.’ Simply speaking, it just becomes unenforceable.

‘Write off’ is an accounting term that the lender denotes to the money you owe. Because you have no intention of paying any time soon, it is no longer an asset of the company. The financial statement will reflect this change as a loss. Businesses must write off these bad loans so as not to mislead potential investors.

What happens next?

In essence, your debt has been written off from the lender’s books- it isn’t forgiven, nor is it forgotten. It still exists. The following is most likely to happen:

The lender may no longer try to contact you to collect the amount. They probably transferred the case to a commercial debt collection agency.

The lender will report the write off to credit rating agencies. It will remain on your credit report for seven years. Acquiring a loan will now be difficult because of your score.

What if I decide to pay off the debt?

The time to repay a debt varies depending upon which you reside in and the type of debt. Remember that there are going to be additional fees and interest added onto the initial amount. So it’s best to check with a state agency or hire an attorney to handle all the paperwork.

If you decide to settle the debt before the statute of limitations, make sure to get everything in writing. It should clearly state that you are no longer responsible for the debt as well as interest or penalties.

What if the company decides to forgive the debt?

Well, that’s great news. But the only way to be sure that the debt is pardoned is if you are issued a 1099-C (a forgiven debt form) or the company provides a letter that declares that the debt has been resolved.

How can I stop debt collectors?

There’s not much you can do to stop them from coming as long as they’re within the law. However, collectors must abide by the Fair Debt Collections Practices Act. You can, however, request them to stop contacting you. And they must comply.

If you are close to the statute of limitations, you may just want to wait for it to run out and hope that they don’t sue afterward.

What is the statute of limitations?

It is the amount of time the lender has to recollect the debt. The time for the statute of limitations starts from the last date of activity on the account. It ranges between 3 to 15 years, depending on which state you were living at the time the debt came into existence and the type of debt it is.

Though it may seem as the court keeps track of the statute on your debt, in reality, you must take it upon yourself to prove that the debt has passed its statute of limitation.

What happens if debt gets old?

When the debt gets old, the statute of limitations expires. In most states, the Limitations Act states that debt can become statute-barred after six years. Again, this varies from state to state.

If you refrain from acknowledging the debtor if the lender does not go to court before the six years are up, the debt collector may not be able to sue you. Once the time for the statute of limitations is over, the collection agency can’t take you to court. But they may continue their efforts to collect the debt, either by calling, writing, or coming in person.

Remain cautious when dealing with old debt. If you are not careful, you restart the statute’s “clock.” This inadvertently extends the time that the lender can successfully sue.

Final thoughts

People must learn to manage their income. Most get caught up in maintaining a lifestyle that is beyond their means. Ideally, they need to commit to spending less than they earn. More importantly, they need to learn how to save.

Remember, don’t mix up the statute of limitations of your debt with the amount of time a negative mark stays on your credit reports. According to the law, a lender has a deadline if he wants to recover any money.