Hidden Value Stocks newsletter for the second quarter ended June 30, 2019, featuring an interview with Mitchell Scott, the portfolio manager and founder of Choice Equities Capital Management. An in-depth excerpt below and readers can find the full issue at this link.

Welcome to the June 2019 (Q2) issue of Hidden Value Stocks. This issue has the usual interviews with two fund managers as well as updates from Stanphyl Capital, McIntyre Partnerships, and Choice Equities.

Q1 hedge fund letters, conference, scoops etc

The first interview is with Christian Olesen, CFA, Fund Manager of the Olesen Value Fund. The Olesen Value Fund follows a disciplined value investing philosophy, focusing on areas with significant market inefficiencies such as underfollowed small and micro-cap companies as well as special, complex or unusual situations. The fund has returned around 14% per annum since inception.

In the second interview of the issue, Brian Laks, CFA, a Portfolio Manager at Old West Investment Management discusses why the firm has decided to launch a new fund targeting investments in the uranium sector and highlights two of the companies Old West holds in the recently launched Old West Opportunity Fund.

At the end of this issue, there’s also a table of all the stocks profiled in previous issues of Hidden Value Stocks.

We hope you enjoy this issue of Hidden Value Stocks, and if you have any questions or comments, please feel free to contact us at [email protected].

Check out the full issue right here

Sincerely,

Rupert Hargreaves

& Jacob Wolinsky

UPDATES FROM PREVIOUS ISSUES

Catch Up With Mitchell Scott, CFA - Choice Equities

In the summer 2018 issue of Hidden Value Stocks, Mitchell Scott, the portfolio manager and founder of Choice Equities Capital Management highlighted Drive Shack (DS) and Reed’s (REED) as his two favorite undervalued small caps at the time. One year on we asked him for an update on these two companies. Mitchell was also kind enough to answer some questions on a new top position for the firm, the Rubicon Project, Inc. (RUBI).

The Choice Equities Fund returned up +15.9% and +12.1% on a gross and net basis, respectively in 2018, substantially outperforming the Russell 2000 and S&P 500, which finished the year in the red at -11% and -4.4% respectively. For the first quarter of 2019, the Choice Equities Fund returned 10.5% net.

Mitchell Scott on Reed's, Inc. (NASDAQ:REED)

Reed's Inc. has outperformed the market over the past 12 months by around 15%. What’s been the primary factor behind the company’s progress?

Management has executed well. They have successfully converted the business to an asset-light operational model that outsources manufacturing to relationships with co-packers. This move has spurred a 12% increase in gross margins to the 30% level and freed up capital which they can direct to brand building and marketing initiatives.

Their two category-leading brands Reed's and Virgil’s have both gotten a packaging refresh and marketing support for the first time in ages. Virgil’s refresh came late last year which also included the new Zero Sugar soda line which is performing quite well. As a result, Virgil’s is now in Target and Wal-Mart and saw a big spike of 46% volume growth in 1Q. The Reed's brand just got its refresh this past spring and they have seen their door count expand as well. In this case, they redesigned the packaging but have also made the product available in cans which has led to new relationships with big box stores like Costco.

“As a result, Virgil’s is now in Target and Wal-Mart and saw a big spike of 46% volume growth in 1Q. The Reed's brand just got its refresh this past spring and they have seen their door count expand as well. In this case, they redesigned the packaging but have also made the product available in cans which has led to new relationships with big box stores like Costco.”

The last time we spoke you mentioned that the firm had a lot of work to do to re-build relations with suppliers following disruption in 2015 and 2016. Is the company making progress here? Has Reed's managed to maintain its competitive advantage?

Very much so. The current management team knew they had work to do in this area and they’ve done it. In some cases, they said they had to go back to their distribution and supplier partners and apologize for the past missteps of the prior team and also prove they could deliver on their promises going forward. I’m sure it helped that the current ownership team has strong relationships in this industry from their prior endeavors in this area, but they’ve also proven their new operating model is capable of delivering on the increased volumes. I think wins with big customers like Target, Wal-Mart and Costco give them some credibility here.

As far as the competitive advantage goes, both brands have maintained their strong positions with Reed's still a category leader and Virgil’s coming in at #4. It’s also a great sign that the brands have responded well to increased marketing and new packaging. Virgil’s looks to be making great progress in closing in on a leadership position, especially considering how sleepy this category is. There has been very little innovation in the craft soda segment, even despite the fact the category continues to grow very well.

The CEO had only been at the business for around a year when we spoke last year. How would you rate the new manager’s performance since joining now that he’s had two years to get to grips with Reed's?

I don’t see any reason not to give him an A. They’ve done exactly what they said they would so they have a good deal of credibility with us.

You initially suggested that the company “could potentially double sales in three to five years.” Do you still believe this is possible?

Yes, and I’d say that outcome looks even better now than it did last year. As noted above, they’ve picked up a lot of new doors in some strong channels, like the big boxes, that can really move volume. And they’ve also expanded relationships with several brokers, so they can better target the convenience store and bar and restaurant channels which were largely unpenetrated before.

Perhaps more interestingly, just this month they unveiled a Reed's CBD infused ginger beer offering which has gotten a very warm reception in test audiences. Next quarter, they’ll begin a pilot of their Reed's Ready to Drink Mule which is a pre-mixed Moscow mule and their first entry into the fast-growing Flavored Malt Beverages category. And lastly, later this year they’ll be launching a ginger shot line which will look like a Five Hour Energy shot, only it’ll be good for you. All have the potential to be $10 million+ sized sales opportunities if they take off and with ~50% level gross margins. We’re using a high degree of conservatism in putting these into our current forecasts just because they’re so new, but all three have a lot of potential.

“With core brand growth of 25% into 2020 and a $5 million contribution from new products, a 3.5x EV/Sales multiple would suggest a share price approaching $5. Looking out a little further, a $7 to $8 or better takeout price seems suitable, especially if these new products grow and support a sales base into the $70 - $80 million range.”

And you put a price target of $5 to $8 on the stock. Do you think that range is still suitable?

Yes, and the low end of that range looks achievable, potentially as soon as next year. With core brand growth of 25% into 2020 and a $5 million contribution from new products, a 3.5x EV/Sales multiple would suggest a share price approaching $5. Looking out a little further, a $7 to $8 or better takeout price seems suitable, especially if these new products grow and support a sales base into the $70 - $80 million range.

Finally, any further comments?

It’s been nice to watch management soundly execute on their operational plan to reinvigorate these two leading brands. Reed's and Virgil’s had not gotten the attention they deserved and now that they are getting some support they are responding well. And the new products have been very well received to date. While we don’t quite know what to expect here, it’ll be interesting to see how they do. And who’s to say there won’t be more behind them. We think this management team is just starting to hit their stride.

Mitchell Scott on Drive Shack Inc (NYSE:DS)

Since our last interview, Drive Shack shares have crumbled 40%. What went wrong?

Well, it’s certainly natural to ask the question given the share price performance. But I don’t think it’d be entirely accurate to say things have gone wrong. It is true things have developed a little slower than originally anticipated - which of course some on Wall Street may view as wrong. Even so, on balance I think the changes on net have been a long term positive.

But to your point, a few things have happened. Of the negatives in the short term, the biggest is probably that the open dates on several of their projects have been delayed. So, they are now expecting their second and third locations to open a few months from now, which is behind the original schedule. Another thing that happened, is that their first opening which was in Lake Nona last year, hasn’t presented the strongest operating metrics. This is something we anticipated because the entire complex where the facility is located is only just being built out and is nowhere near full capacity. So, while it has the hallmarks of a great site on a long term basis, it doesn’t present a good look for the first site to trail its peer TopGolf on a lot operating metrics. The last thing specific to the company that happened was there was a change in leadership at the CEO level. We view the hiring of former TopGolf CEO Ken May as a huge positive given his prior success there and obvious understanding of the concept.

And then finally, all this stuff happened to an orphaned security in the middle of a pretty rough market environment. The company is in transition, financials don’t screen well, and there’s only one analyst covering the stock. Fortunately, we anticipated much of this and managed our position size accordingly. But all in all, the long term opportunity remains, and given the new leadership, we think the case is even stronger than it was a year ago.

What is the company doing to fix things?

Well, the biggest thing obviously is the hiring of Ken May. He comes from TopGolf where he helped get the concept off the ground to the 40+ sites it has today and was a former direct report of Fred Smith at FedEx. He is intimately familiar with the operations of their largest competitor and has a keen understanding of how to design a location with good economics built around the fun entertainment experience consumers love.

“Lastly, the heavy lifting in rightsizing the American Golf business looks nearly complete as they have sold or are under contract for all but 2 of the 13 owned courses they had put up for sale. They continue to lease 37 courses and will end this year with 22 or more courses under a management contract at year end. All in, this should drive another $25 million+ of annual EBITDA to the company with very little capital associated capital spend.”

Along those lines, the company has recently unveiled plans for a smaller 72 bay box format versus the standard 90+ bay version we’ve seen thus far. It’s a little smaller and costs less to build, so it’s suitable to more markets. They expect it to expand their total addressable market from 50+ sites for the 90 bay version to 100+ for the smaller version.

Lastly, the heavy lifting in rightsizing the American Golf business looks nearly complete as they have sold or are under contract for all but 2 of the 13 owned courses they had put up for sale. They continue to lease 37 courses and will end this year with 22 or more courses under a management contract at year end. All in, this should drive another $25 million+ of annual EBITDA to the company with very little capital associated capital spend.

The last time we spoke you said the company’s moat was “emerging.” Has the competitive advantage continued to grow as you expected?

I guess I’d say it’s mostly status quo. The company had a few things to straighten out as it got set up to focus on its Drive Shack concept. Those things now look to be behind them as they are set to hit their stride this year and next with some attractive new sites they have targeted for new openings.

In June of last year, you suggested a bear case of ~$5 if the company’s growth did not play out as expected. As the stock is currently below this level and has been for some time, what’s your new downside case?

It remains around that same level today based on a sum of the parts analysis. We put a 7x multiple on the golf course management cash flows and assign a 75% value to replacement costs for the new Drive Shack entities. After deducting net debt and preferreds we get to ~$5 of NAV/share.

You also put an upside target of $10 on the stock in the bull case. Do you still think this level is possible? If so, why (or why not)?

Yes, this long term upside target remains very much in play in a three year look forward scenario. After next year when we expect about eight stores in total to have been opened, the company is targeting a pace of five to 10 new sites per year. Taking the low end of this range we can envision 20 sites in operation by then. We put a 12x EBITDA multiple on the Drive Shack concept and a 7x EBITDA multiple on the cash flows from the American Golf business. In that scenario, we see shares trading around $11-12.

“We put a 12x EBITDA multiple on the Drive Shack concept and a 7x EBITDA multiple on the cash flows from the American Golf business. In that scenario, we see shares trading around $11-12.”

Any final thoughts on Drive Shack’s trajectory over the past 12 months?

Not really. It’s been a bit of a bumpy ride for this orphaned security as the business model transitions, but we continue to like the concept and particularly the new leadership team.

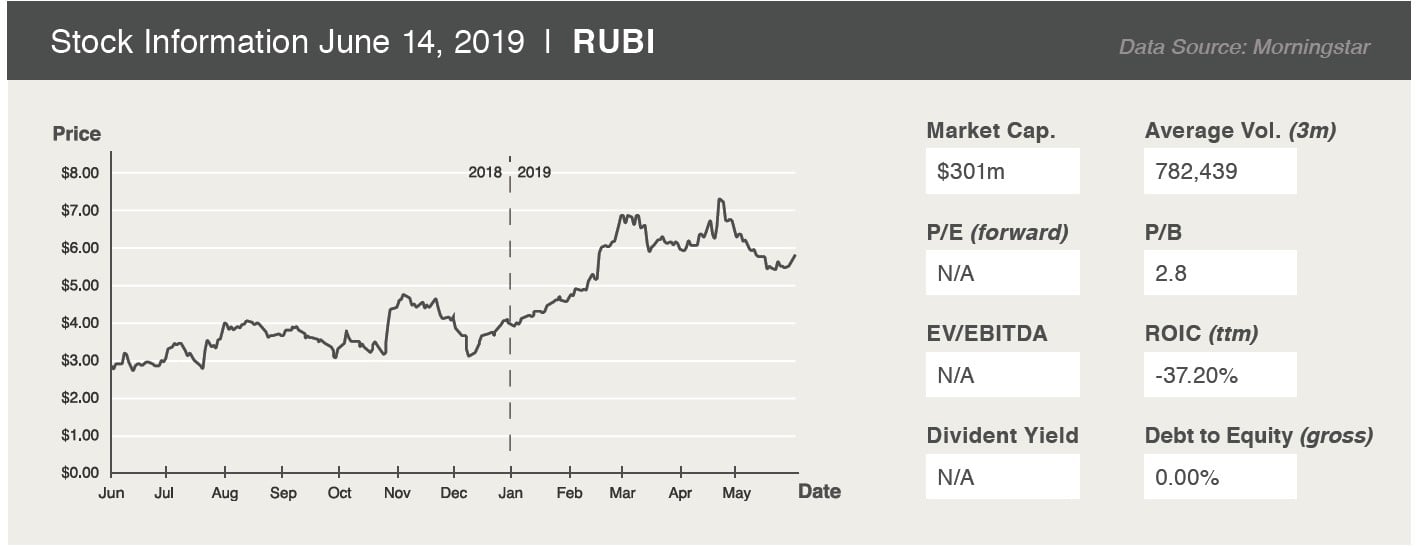

Mitchell Scott on the The Rubicon Project Inc (NYSE:RUBI)

You also believe the Rubicon Project is another undervalued small-cap that could have hidden value. What does this company do?

Rubicon Project is an independent ad exchange platform that focuses on automating the process of buying and selling digital ads. As a supply side exchange, the company’s principal focus is on matching the ad inventory of its content publishing customers with brands and advertisers who are looking for digital real estate for their ads. Given the thousands of miniature auctions that take place to match a buyer and seller to create an impression (i.e. a successfully matched ad), the company relies on algorithms to match the best bids with the appropriate content all in a way that places ads quickly, so the content is displayed without delay.

The ad-tech industry has been criticized for poor controls and high levels of fraud. How is the Rubicon Project trying to change this?

That’s exactly right and that’s actually part of the thesis as we see it. Since coming on board as CEO in 2017, Michael Barrett has been quite focused on improving transparency both inside Rubicon and in the ad tech space more broadly. In the past, advertisers weren’t clear where exactly their advertising dollars were going. Were the clicks and impressions real? Were they being charged appropriately? The industry faced a lot of questions.

As recently as last fall, one of their peers got in a lot of hot water for the process of bid caching or selling second-tier inventory while charging for first tier inventory (e.g. selling an impression on the second page of a search to someone that bid for the first page). So, against this backdrop Rubicon has been leading the charge for cleaning up the industry, which should be good not just for them but also the entire space. As a case in point, last year they launched a product called EMR or estimated market rate which helps ad buyers better understand the pricing of all ads in an auction so they can bid more appropriately and win bids more often. With initiatives like these, the company appears well positioned to capture share in the industry from less transparent peers as industry players continue to develop trust with Rubicon.

How is the business coping with new data privacy laws, particularly GDPR in Europe?

GDPR has been implemented for a little over a year now and Rubicon has seen a limited impact to their business or revenue growth. Advertising budgets are still getting spent – the targeting is just a little less efficient in affected regions.

And how does the company score on your ‘4 M’ criteria?

Quite well. We really like the management team, their competitive positioning, and the industry outlook.

“In this case, Rubicon has set its sights on becoming the largest independent supply side ad exchange player in the marketplace. And they are focused on doing it by winning with a low cost offering that is both transparent and efficient to use, a formula other exchanges have used successfully in other industries.”

What is the moat?

The company operates as a marketplace, so we think typical exchange and network type dynamics will be at play. In this case, Rubicon has set its sights on becoming the largest independent supply side ad exchange player in the marketplace. And they are focused on doing it by winning with a low-cost offering that is both transparent and efficient to use, a formula other exchanges have used successfully in other industries. As they continue to attract more supply to their platform, their ability to offer the broadest, lowest cost access to programmatic advertising inventory should increase thereby attracting more buyers, all along passing more revenue over a fixed cost base that should reinforce their ability to remain the low-cost provider.

How is the company competing against the Facebook/Google duopoly?

The “open web” outside of Google and Facebook and increasingly Amazon offers a lot of white space. While it’s true the three behemoths dominate the space and get about two-thirds of ad web spend, the market excluding these three is still about $70 billion in size and growing leaving a lot of opportunity for other players. And there are other avenues of growth too including mobile, video, programmatic audio and connected TV which offer a lot of runway in coming years.

Do you see the moat expanding?

Yes. AT&T offered an assist when it bought peer AppNexus last fall (at what we think was about an 8x multiple of sales) which removed a chief competitor. But more importantly, the company’s moves over the last two years to become the low cost and transparent provider have paid dividends. They have been especially successful against the smaller remaining players who are struggling to compete with Rubicon’s competitive take rates and scaled efficient offering. They are also capitalizing on the industry trend of Supply Path Optimization which is basically ad tech’s version of supplier consolidation as the publishers and marketing agencies consolidate the number of exchanges on which they will buy from something that used to number in the 60s or higher to what is now about 20 and likely to go to just three to five.

In addition, early feedback on the recently launched Demand Manager platform has been quite positive. It comes with a SaaSlike function called Prebid-as-a-Service that enables customers to develop better visibility and measurement of ROI on their advertising spend. If it’s as successful as the last two recent offerings like nToggle and EMR, the company will be in very good shape. And just this past week they announced a partnership with MediaMath and Havas that will run through the platform, so it looks like it’s off to a great start.