Bud Labitan’s 9th book, Illustrated Valuations describes a step-by-step process (with pictures) of estimating the intrinsic value of a business’ stock.

Illustrated Valuations + Intrinsic Value Estimations & Bargain Hunting in the style of Warren Buffett and Charlie Munger by Bud Labitan

This book is carefully crafted and easy to read and understand. Illustrated Valuations begins by discussing the merits of evaluating a business’ qualitative factors as recommended by Warren Buffett and Charlie Munger. With picture images of calculations, read about a new valuation of Apple, (NASDAQ: AAPL), followed by valuation possibilities for Disney, (NYSE: DIS).

Q1 hedge fund letters, conference, scoops etc

Next, there is a discussion about the qualitative and quantitative values of the historical See's Candies purchase by Berkshire Hathaway. Then, read about the unique value of Coca-Cola's dividends, stock splits, and stock buybacks. For speculators, there is a thoughtful section on intelligent speculation using fundamental knowledge.

This is followed by the topic of value traps. The following chapter has an informative history lesson on Pan American World Airways, and why a great brand failed. The book ends with a useful section on value investing best practices.

For readers who are motivated to do their own valuation estimates, read about the StocksCalc software and where to purchase it at frips.com The StocksCalc Software is recommended to readers who wish to do their own intrinsic stock valuations.

"Illustrated Valuations" is now on Amazon.com and Lulu.com

Illustrated Valuations - Chapter 11: See’s Candies Valuation

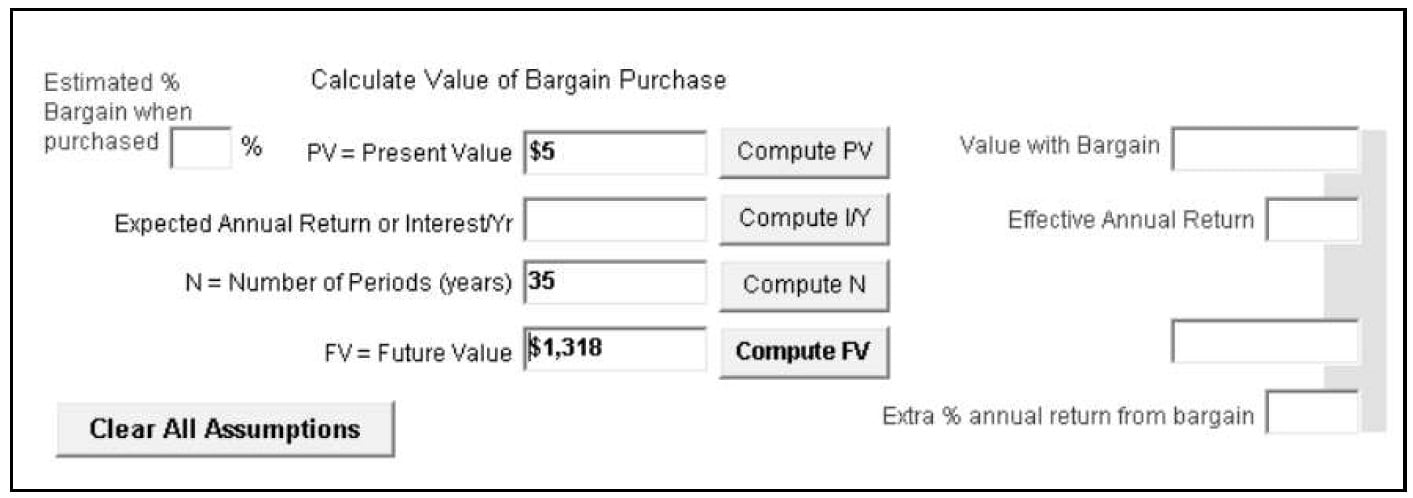

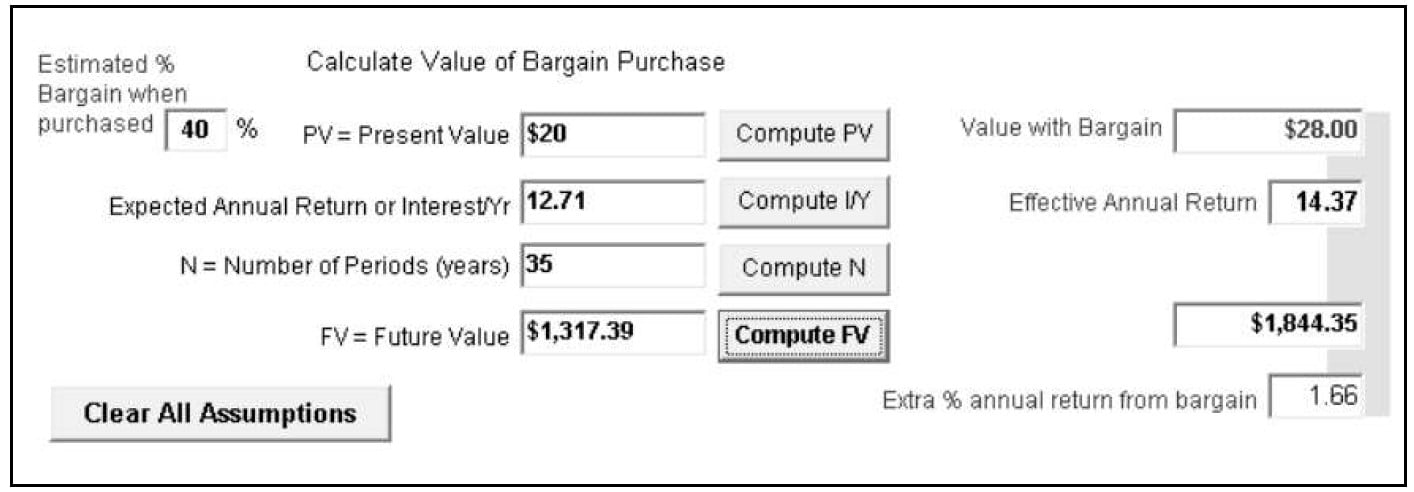

This is my rough estimate of See’s Candies returns based on pre-tax earnings growth from the years 1972 to 2007. See’s Candies is “The Wonderful Business,” the prototype of Buffett and Munger’s dream business. While the boxed-chocolates industry in which it operates is unexciting, See’s has excelled. Per-capita chocolate consumption in the U.S. is low and doesn’t grow. Many other brands have disappeared. Annual sales were 16 million pounds of candy when Blue Chip Stamps purchased the company in 1972. Buffett and Munger controlled the Blue Chip Company and later merged it into Berkshire Hathaway.

Buffett and Munger bought See’s for $25 million when its sales were $30 million ( 25/30 = 0.833 price/sales ratio ) and pre-tax earnings were less than $5 million. I will start this discussion by looking at the earnings growth from 1972 to 2007. See the image presented below, and think of $5 million as an approximation of the present value of earnings at the time of purchase, 1972. Next, I want to estimate their real annual earnings returns using the earnings data given in the letters to shareholders. (starting at around $5 million growing to a total of $1.318 billion) ( 2007 – 1972 = 35 years).

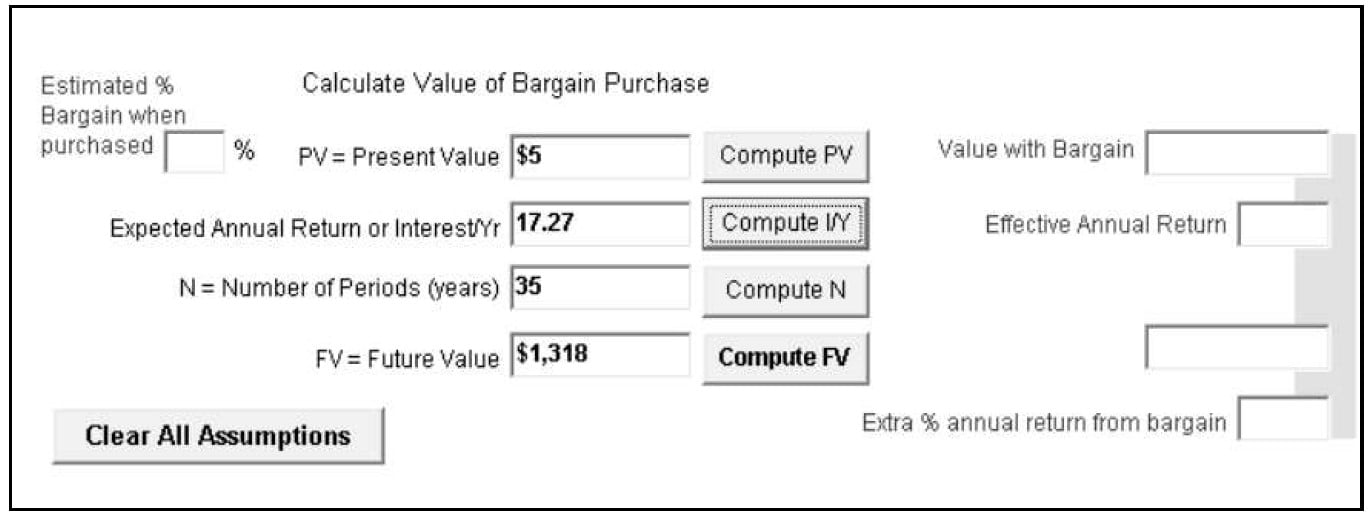

Now click and compute the Expected Annual return or Interest per year button.

Therefore, the annual return on earnings appears to be 17.27% The capital required to conduct the business was $8 million in 1972. Modest seasonal debt was needed for a few months each year. Consequently, the company was earning 60% pre-tax on invested capital that year. ( $5 mil earnings / $8 mil capital = 0.625 ).

In 2007, See’s Candies sold 31 million pounds, a growth rate of only 2% annually. But, in this first discussion, I want to estimate their real annual earnings growth rate. Note that my data is limited to the numbers mentioned in the annual letters.

See’s Candies durable competitive advantages produced extraordinary results for Berkshire. By 2007, See’s sales were $383 million, and pre-tax profits were $82 million. The capital, in 2007, required to run the business was $40 million. This means they had to reinvest only $32 million since 1972 in order to handle the modest physical growth of the business. Interestingly, pre-tax earnings as of 2007, totaled $1.35 billion. All of that except for the $32 million ( $32 mil + $8 mil original capital = $40 mil ) has been sent to Berkshire Hathaway. ( $1.35 Billion - $32 Million = $1.318 Billion. )

After paying corporate taxes on the profits, Buffett and Munger have used the rest of the money to buy other attractive businesses. Therefore, See’s has given birth to multiple new streams of cash.

Note that my initial assumption on this investment was that 20 of the 25 million might have been funded by insurance float. Later, I will discuss the average annual return rate if 20 million came from retained earnings. Why $20 million and not $25 million? The business was earning close to $5 million in 1972. ( 25 – 5 = 20 ).

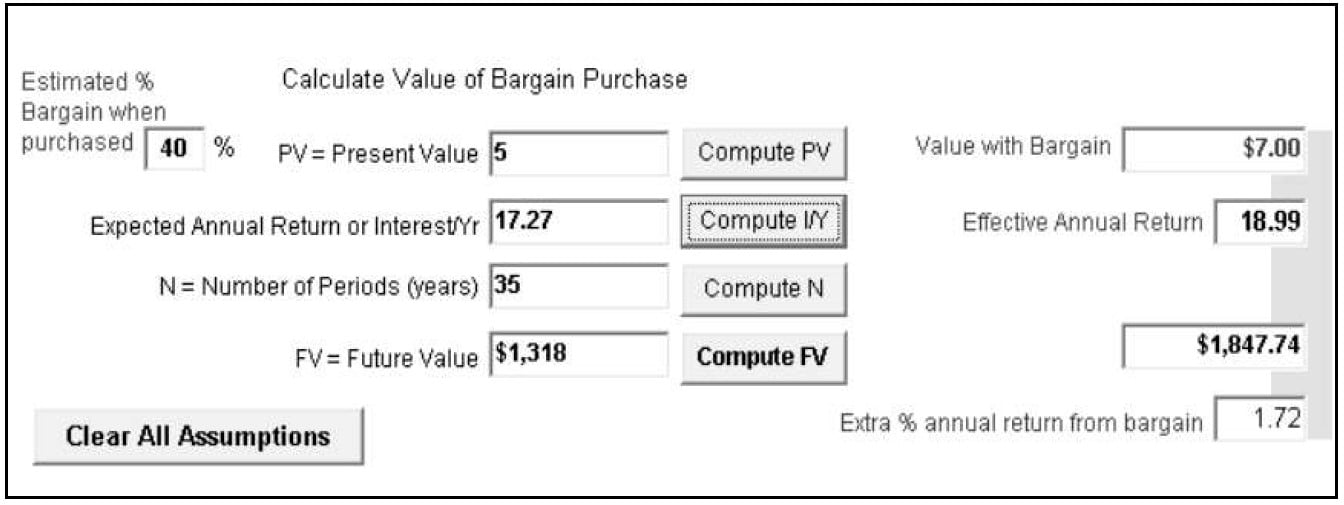

Next, I wondered what is the effective annual return Buffett and Munger obtained if I assume that the purchase in 1972 was made at a 40% bargain? My suggestion is 18.9% seen in the image below.

Two factors helped to minimize the funds required for operations. First, the product was sold for cash, and that eliminated accounts receivable. Second, the production and distribution cycle was short, which minimized inventories. Brand loyalty is discussed in my book “MOATS.”

In recent years See’s has encountered two important problems. The problem concerns costs. Raw material costs are largely beyond control since See’s Candies buy the finest ingredients, regardless of changes in their price levels. See’s Candies managers regard “product quality” as sacred. Other kinds of costs are more controllable. There have also been times when sales volume was flat. Despite the volume problem, See’s enduring competitive strengths are important over time. In the primary marketing area, the Western States, See’s candy is preferred by an enormous margin to that of any competitor.

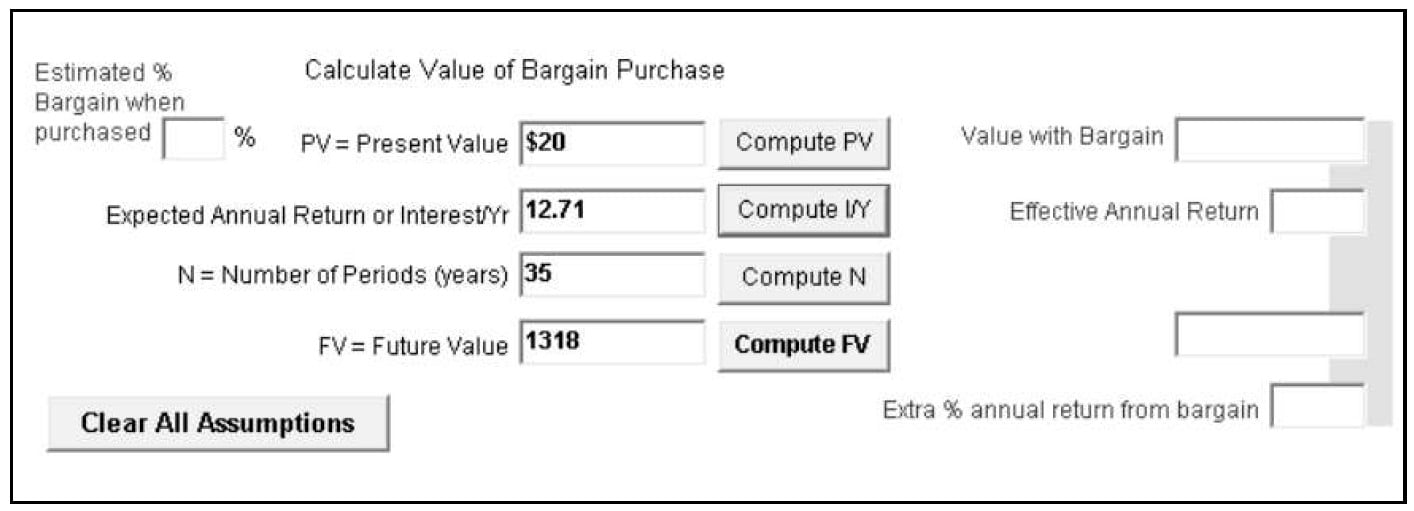

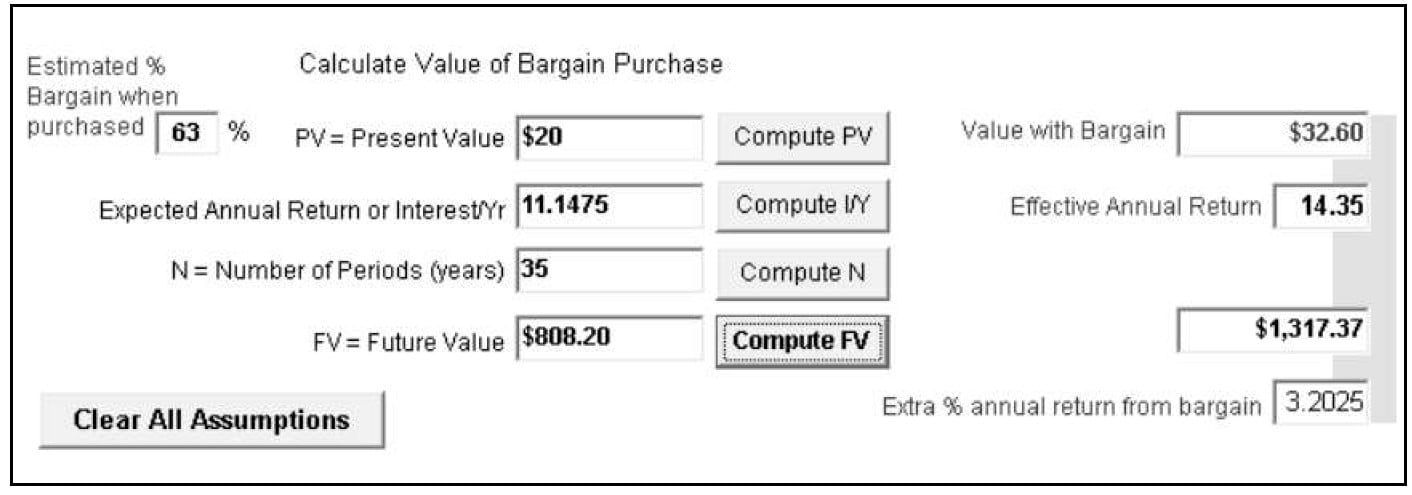

This next scenario assumes $20 million as the present value of investment in 1972 that produced a total of $1.318 billion by 2007.

Then, the following image imagines that investment purchased at a 40% bargain.

See’s Candies is a wonderful business because it is 1.Understandable, 2.Has enduring Competitive Advantages, 3. Run by Able & Trustworthy Managers, 4. Was probably purchased at a decent bargain price. ( Just look back at that 0.8 price/sales ratio ).

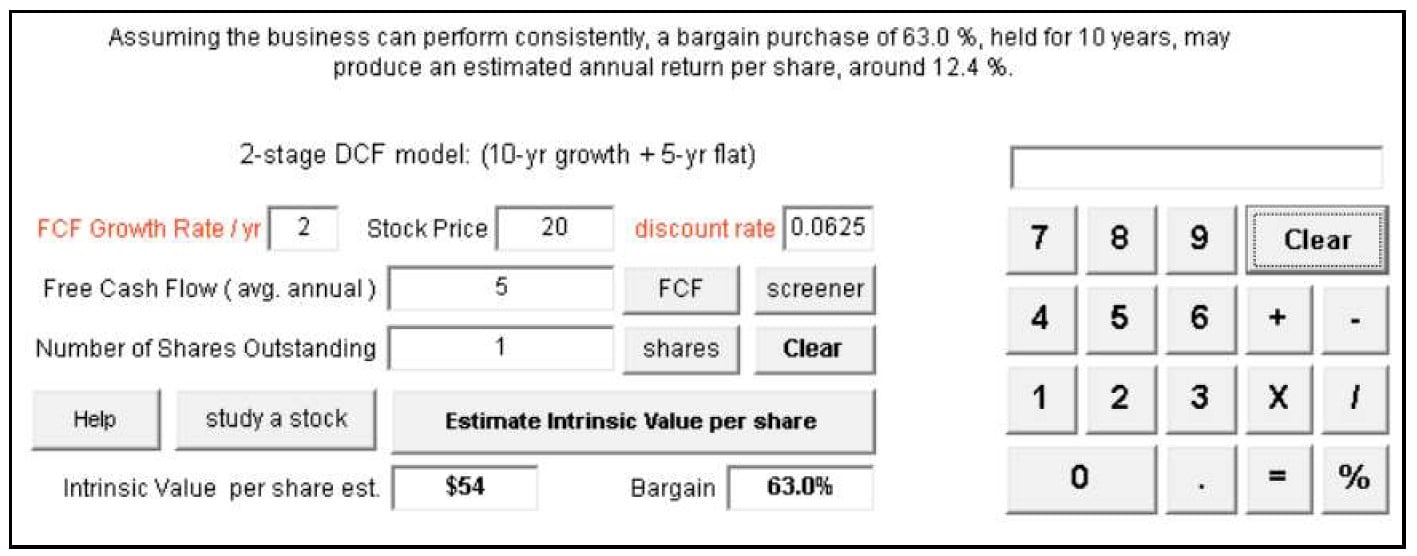

Next, let’s look at my valuation model to imagine an intrinsic value of See’s Candies in 1972 using my 2-stage DCF model. (2-stage DCF model consisting of 10 years growth and 5 years flattened out to use the cash flow from year 10 in years 11, 12, 13, 14, and 15.) In reality, See’s continued to grow with minimal needs for capital infusion.

The average yield on 10-yr treasury bond was 6.21 in 1972. The projected free cash flow growth rate I used was 2%. They paid around $20 million for a business that was earning a little less than $5 million (pre-tax), but I use the 5 as a nice round figure.

If you take my model back to 1972, it predicts an intrinsic value of around $54 million; and purchased for around $20 million. In this scenario, it was a 63% bargain.

Next, in the interest of testing my StocksCalc software, here is my imaginary scenario required to produce that 1.38 billion after 35 years, using my 63% bargain figure obtained above.

Back in 1972, Buffett and Munger probably did not think they were getting such a deep bargain. After all, who could predict the future? What did they know? See’s Candies was a profitable business with minimal capital reinvestment needs.

Charlie Munger said, “If See’s Candy had asked $100,000 more, in the purchase price, Warren and I would have walked - That’s how dumb we were. Ira Marshall said you guys are crazy - there are some things you should pay up for, like quality businesses and people. You are underestimating quality. We listened to the criticism and changed our mind. This is a good lesson for anyone: the ability to take criticism constructively and learn from it. If you take the indirect lessons we learned from See’s, you could say Berkshire was built on constructive criticism.”

Books by Bud Labitan

“The Four Filters Invention of Warren Buffett and Charlie Munger” book examines each of the basic steps Buffett and Munger use in "framing and making" an investment decision. It is a focused look into an amazing invention within "Behavioral Finance." In my opinion, the genius of Buffett and Munger's four filters process was to "capture all the important stakeholders" in a four cluster process. Imagine...Products, Enduring Customers, Managers, and Margin-of-Safety... all in one mixed "qualitative + quantitative" process.

“Quick Guide to the Four Investing Filters of Warren Buffett and Charlie Munger” book is a quick guide to understanding the four investing filters of Warren Buffett and Charlie Munger. It is a shorter version of his previous book and is designed to improve your investment thinking. How do you set a price for your stock purchases? In Chapter 4, I estimate an intrinsic value (of Apple stock). First, start by trying to understand the qualities of a first-class business. The four filters help you optimize your decision making. Warren Buffett said it best: "An investor cannot obtain superior profits from stocks by simply committing to a specific investment category or style. He or she can earn them only by carefully evaluating facts and continuously exercising discipline."

"Price To Value" is about Intelligent Speculation. It is about decision framing and using the "Decision Filters" of Charlie Munger and Warren Buffett. Readers benefit from this book if it stimulates better thinking into the most important factors crucial to decision making. These decision framing ideas can be applied across different asset classes. First, the book presents the four investing decision filters in simplified terms. Then, it extends these ideas by looking into the intelligent speculation ideal described by Benjamin Graham in his tenth lecture of 1946.

“Valuations” book offered 30 sample "intrinsic value per share" business valuations I performed in 2010. In each case the author tried to simulate an approach that Buffett & Munger might take to valuing a business. However, all of the growth assumptions used were my own. No consultation nor endorsement was sought with Mr. Buffett or his business partner Mr. Munger. The examples given are chosen for educational and illustrative purposes. The valuation cases are estimations written in a style that emphasizes a focus on free cash flow and the number of shares outstanding. Readers are also encouraged to think about the business' competitive position. In reality, these businesses may outperform or they may underperform any of my projections. Read it and then look at how my predictions actually turned out niine years later.

"Coach W Software" was crafted from my imaginary conversation with Mr. Warren Buffett. The real conversation never occurred. The software generated conversation did occur on March 5, 2011. The pseudo-A.I. Windows software was developed by me, and it is a useful tool in reviewing the concepts developed by Mr. Buffett, Mr. Charlie Munger, and Mr. Benjamin Graham. An easy read, this book starts out as an imaginary conversation filled with useful business and investing ideas generated by the software. Value? "Coach W Software" is an unauthorized experiment in positive suggestion that delivers valuable insights to the business thinking reader. It makes us think about how man and machine can communicate with each other. Do certain keywords help us become better investing thinkers? The book is structured to both enlighten and entertain. In this way it mirrors a feel-good guide to self-hypnosis in the field of investment thinking. It is important to point out that there is no association or endorsement from Mr. Buffett or Berkshire Hathaway. "Coach W Software" is useful to readers who are new to value investing, and readers who wish to review these great business investing concepts.

“Sports & Stocks” describes ideas about investing in the stock of a winning business. A fun read, it is written from the point of view of a sports fan. Mixing sports talk with investing talk may stimulate your thinking about better investing. The Goal is to find HQB, High Quality (Business) Bargain. I present an entertaining read on how to find HQB using the sports ideas of Offense, Defense, and Special Situations. This book includes three stock valuation examples from 2017.

“MOATS” may be the best business book that describes the competitive advantages of profitable businesses. MOATS describes the nature of 70 selected businesses purchased by Buffett and Munger for Berkshire Hathaway Inc. It is a useful resource for investors, managers, students of business. MOATS also looks at the sustainability of these competitive advantages in each of the 70 chapters.

Thanks to Professor Phani Tej Adidam, Ph.D. Chair of the Department of Marketing and Management at University of Nebraska at Omaha; many of his students contributed to the research for this book. Also, thanks are extended to Richard Konrad, CFA, Dr. Maulik Suthar, and Scott Thompson, MBA for sharing their thoughts, analysis, and feedback.

“A Fistful of Valuations in the Style of Warren Buffett & Charlie Munger” (Third Edition, 2015). This book offers five sample intrinsic value per share business valuation estimations that were first performed in 2010. In each case presented, I simulated an approach that Buffett and Munger might take to valuing a business, based on what they have written and talked about. However, all of the growth assumptions used are my own. No consultation or endorsement was sought with Mr. Buffett or Mr. Munger. How is this portfolio of five businesses doing after five years? If the reader had invested an equal amount of money in all five businesses in 2010, the average annual return would be 42 percent by the end of 2015.

If you like my books and audiobooks, share this file with your friends.

Thank You.

{kind=link}