Blue Tower Asset Management letter to investors for the first quarter ended March 31, 2019, discussing their investment thesis in Charles Schwab Corporation.

In this letter we discuss our first five years of performance and explore our investment thesis in Charles Schwab, in which we have recently initiated a position.

Q1 hedge fund letters, conference, scoops etc

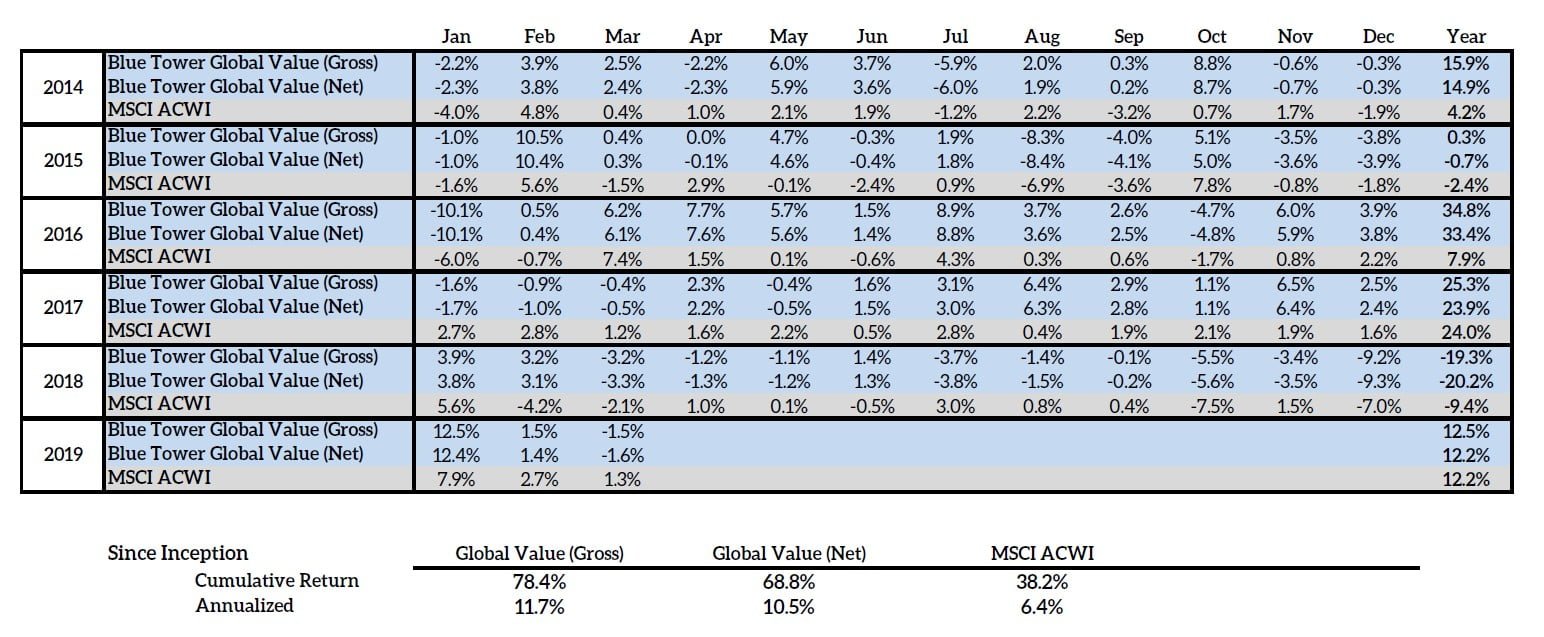

Now that other firms have uploaded their 2018 composite data to performance databases, we can compare our performance to theirs. Taking a longer view of performance is important as the longer the time period the more instructive the performance numbers are for evaluation. If a strategy were to report a one-year gain of 82%, that may be impressive. But if it followed a 45% loss the previous year, then the total gain is zero.

Morningstar has a database of separate account managers who self-report the composite numbers of their managed account strategies to Morningstar’s SMA database. Morningstar then makes a style box where they sort composites or funds into categories based on the market capitalization and growth and value factors of the composite portfolio’s securities. They currently classify the Blue Tower Global Value strategy as “small value”.

It is my pleasure to report that for the 5-year period of 2014-2018, Blue Tower Global Value had the best annualized gross performance out of the 129 small value strategies in their database that had data for all years in this time period. Our gross performance was 9.7% annualized (8.5% net) while the equally-weighted average of the small-value composites returned 3.7% gross of fees. We aim to continue this track record by focusing on the potential downsides of our investments as much as their upside. Historically, our upside capture ratio relative to our global benchmark has been higher than our downside capture.

Charles Schwab Corporation

The Charles Schwab Corporation revolutionized equity trading by becoming the first electronic brokerage in 1971. Prior to this equity trades were conducted over the phone and recorded on paper. Now as of Dec. 31, 2018, Charles Schwab held $3.25 trillion in client assets, with a total of 11.6 million active brokerage accounts making it the second largest stock broker in the US after Fidelity Investments.

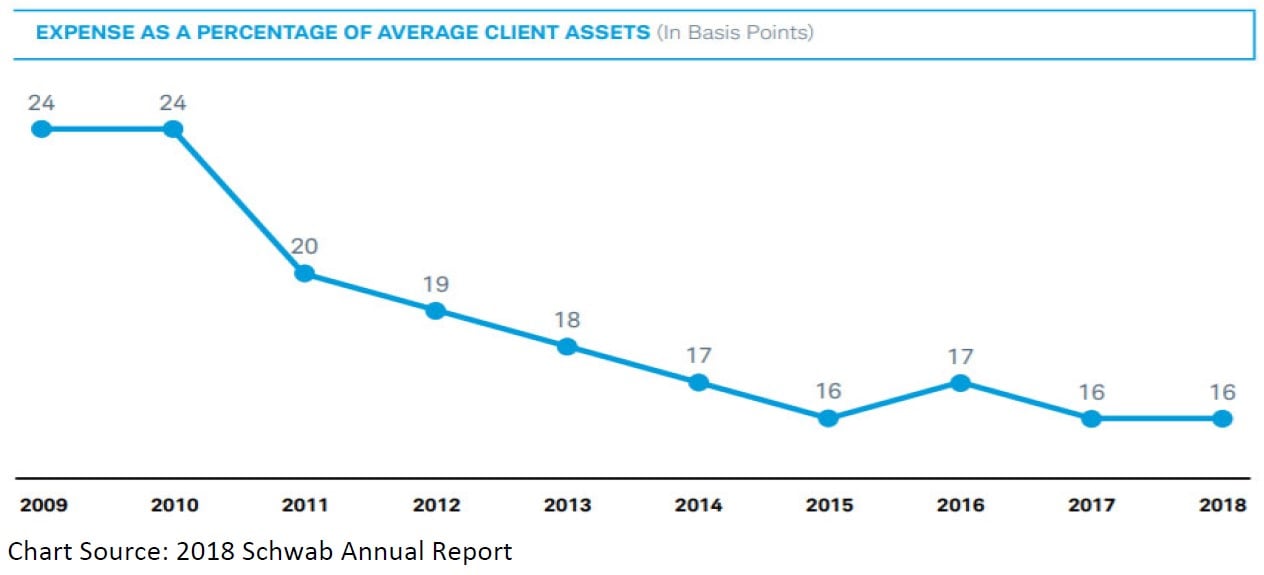

While many of our investments have been small caps ignored by the market, in some industries scale is an advantage. In equity brokerages, this is certainly the case as much of the costs of the developing and operating the business are fixed. Larger firms can then out compete smaller ones on cost giving them a sustainable advantage. Financial brokerages are currently an oligopolistic market dominated by a few large firms and as such it is possible for the industry as a whole to deliver high returns on equity. Schwab is a relatively more automated, technological brokerage than most of their major competition which makes their cost structure more fixed. We can see this with Schwab where their cost per unit of client assets has steadily declined as they have grown in size.

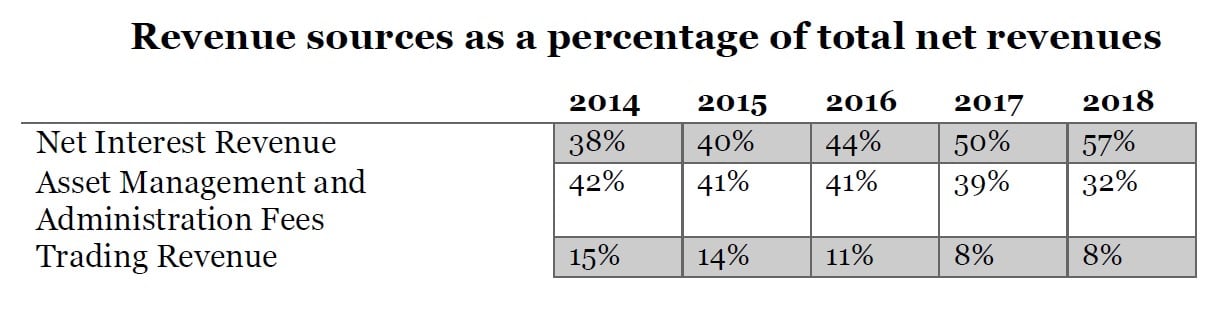

Schwab makes their money from three main sources: net interest revenue, asset management fees, and trading commissions. The net interest revenue is increasingly the main source of the company’s income. When clients invest their money at Schwab’s brokerage or keep money in Schwab Bank, they collect a small interest from Schwab on their cash balances. These clients are fairly yield insensitive as they are storing their money at Schwab primarily for the convenience and the overall utility and service of the platform. As a result, there are several hundred billion dollars of client cash collecting an interest rate of 27 basis points. This money could easily be reinvested by clients into a money market fund at a much higher interest rate, but they do not care to do so. This effect gives Schwab a significant funding advantage over other financials.

Schwab has built up a large collection of internal ETFs that are free to trade on their platform. They also have commission free mutual funds where Schwab collects a portion of the management fee which represents the plurality of their management fees. Now that interest rates have recovered and they have ceased money market fund fee rebates, they make significant profits from their money market funds as well.

Trading has become a relatively smaller source of revenues for the company over time. While there are new brokerage startups such as Robinhood that offer free stock trading, Schwab’s fees are still low enough that there is likely not much client attrition. Interactive Brokers has better price execution and lower fees for equities and option trading, but for investors who are less active, Schwab’s ETF and mutual fund offerings, and user-friendly customer service make up for it. The only thing that could potentially make Schwab go to free trading would be if their chief rival Fidelity were to offer it. Until then, they have little reason to engage in irrational price competition.

Sensitivity to rates

The financial assets of Schwab yield more in a higher interest rate environment. This sensitivity to rates can be seen in the recent increase of their net interest margin. From 2015-2018, there were nine Fed Funds rate hikes, expanding their net interest margin from 1.57% in the third quarter of 2015 to 2.29% in 2018. Schwab estimates that currently a gradual increase in the federal funds rate of 1% would increase their net interest revenue by 4.4% over the next twelve months and the reverse would decrease it by 4.9%.

Why this opportunity exists

When a stock appears cheap, it is useful to ask why. In the case of Schwab, it is likely due to fears that the market has reached its peak and that a recession may be coming due to the interest rate curve inversion. The interest rate inversion, also called a negative yield curve, is an environment where the yields on short-term debt instruments are higher than those of longterm debt instruments. Investors are willing to buy more to lock in yields for a long period as they are expecting that the returns on capital would be significantly lower upon the maturity of short-term instruments. Historically, they have usually preceded an economic recession which would impact Schwab’s asset management and trading revenues.

Just because the interest rate curve has become inverted does not necessarily mean that it is time to exit the market and go to cash. It is possible that the market may continue to amble along and appreciate in value while paying out dividends for months and even years to come before the next crash. For example, in 1998 the market gained over 55% from the point of the interest rate curve inversion to the market high before the correction. Someone who exited to cash when the yield curve inverted would have regretted the decision. In recent history, US equity markets have appreciated over 30% from the yield curve inversion to the market top.

In a recession, the profitability of Schwab may be impacted from the company having their net interest market compressed due to interest rate cuts as well as their fund management fees compressed due to the lower market value of the securities making up their funds which charge an asset-based fee. However, since customers would be moving their asset mix towards cash in a market selloff, Schwab has the opportunity to make additional revenue off of those cash balances. The overall effect of these flows is that the increased reliance on net interest revenue will make Schwab a less cyclical business during a recession than it has been in the past. The market appears to be missing this change.

Rationale for investing

2018 was an excellent year for Schwab but a terrible one for their stock price. Last year, the company grew net revenues by 18%, customer accounts by 9%, and net income by 53%. In line with their 20-30% dividend payout ratio target range, they also expanded the dividend. Despite all of this, their share price fell by 19.2%. We are happy to be able to take advantage of this value.

It is not very productive to attempt to forecast interest rates several years into the future as consensus forecasts tend to be quite inaccurate and therefore our investment in Schwab is not based upon any prediction on rates. Currently, the consensus forecast as seen in the futures market is that the federal funds rate will decrease over the next twelve months. However, there is always the possibility that interest rates could one day return to historically higher levels. The federal fund rates level of 5% in 2006 led to Schwab having a net interest spread of 4.33% at the end of 2007. In a bull case where their interest spread returned to these levels, Schwab’s earnings would roughly double.

Schwab has a significant base of independent financial advisors who operate separately managed account businesses custodied with Schwab. These advisors once custodied with a brokerage are a fairly sticky client base as they do not want to inconvenience their client base with a custodian change and suffer the resulting loss of business which might occur. Schwab is using some of its profits to reinvest in its balance sheet and build up equity in order to stay within their Tier 1 Leverage Ratio target range of 6.75-7.00%. They are also paying dividends (payout ratio target is 20-30% of earnings) and buying back shares. Regardless of what happens to interest rates in the near term, Schwab will be a dominant brokerage and asset management platform for years to come.

Valuation

Schwab has traded around 25x forward earnings in the years of 2013-2016. If they were to return to those levels at the current analyst consensus earnings-per-share estimate of $3.06, its share price would be $76.50, a 66% premium over the current price.

Another way to view stock investments is to view them through their forward rate of return combining the cashflow generated by the business and its long-term organic growth rate rather than any static stock price target. This works best when the investment thesis is based on a company organically compounding over the long-term rather than some shorter-term catalyst such as an asset spin-off. Schwab has grown their number of active brokerage accounts from 9.386 million in year-end of 2014 to 11.593 million in 2018, a four-year compound rate of 5.4%. Client assets grew by 7.4% annually over the same time period. Schwab’s estimated forward EPS divided by its current share price ($46.10) gives an earnings yield of 7%. Therefore, at current prices with no change in interest rates we conservatively estimate that Schwab has a forward rate of return of about 14% which is adequate for the current opportunity set we have in the market.

Thank you for your trust and loyalty, and please never hesitate to call if you have any questions or concerns.

Best regards,

Andrew Oskoui, CFA

Portfolio Manager