In 2018, we saw the fiercest battles amongst the top e-commerce players in the region. This was evident as we saw an increased investment on online and offline marketing initiatives from e-commerce players. One of them were Lazada, who organised an extravagant Singles’ Day offline show in Malaysia, Thailand, and Vietnam and broadcasted it more than 5 million viewers. Similarly, top players such as Tokopedia, Shopee, Tiki and others each initiated big promotional campaigns during vital sale periods for Singles’ Day, Hari Raya Aidilftri, Lunar New Year, and 12.12 Sale in a bid to become the biggest player in the region.

Further fuelling the competition were the assistance of investors to fast-track the competition. Top e-commerce platforms in the region such as Tokopedia received a US$1.1 billion huge boost from Alibaba and SoftBank, Bukalapak, became Indonesia’s fourth Unicorn, while Lazada, received US$4 billion to fast track its development as well.

[REITs]Q4 hedge fund letters, conference, scoops etc

However, who came out as the most successful e-commerce platforms in Southeast Asia?

Most e-commerce companies would attempt to announce their results by announcing the total gross merchandise value (GMV) transacted through its platforms. This was commonly used by Chinese e-commerce giants as well such as Alibaba who declared they broke its previous year’s record by amassing US$30.8 billion in GMV on Singles’ Day in 2018. But some considered GMV as a really vague figure as it only takes into account the total value of transactions without factoring in any returns or cancellation. The GMV does not paint a representative picture of its actual revenue.

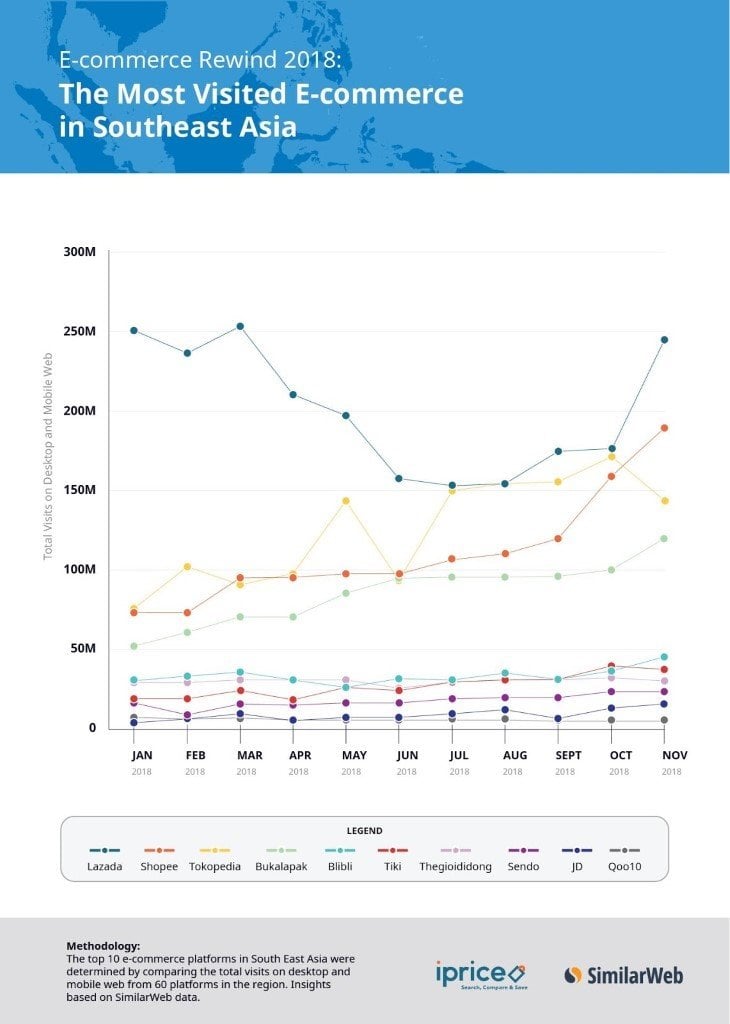

We conducted a study to paint a better picture and see who were the top e-commerce players in Southeast Asia 2018 with a more reliable data source. That data is the total visits garnered by each e-commerce platforms from desktop and mobile web. While we would love to get our hands on data such as the total revenue by each e-commerce platforms, this data is usually not available publicly.

With the help of SimilarWeb, we analysed the total visits (desktop and mobile web) garnered by 42 e-commerce companies which consisted of 60 e-commerce platforms from six major markets in Southeast Asia (Indonesia, Philippines, Vietnam, Thailand, Malaysia, and Singapore) between January and November 2018. The companies selected for this study were amongst the 10 most visited platforms (on desktop and mobile web) in their respective countries from our study, The Map of E-commerce.

From here, we ascertained the top players of 2018 and data that would serve as a prediction of what is about to come for 2019 and beyond.

Top E-commerce Platforms In Southeast Asia In 2018

The 42 e-commerce companies analysed in this study saw an average 54% growth in its total visits on both desktop and mobile web. We saw this increase by comparing the total visits between Q1 and Q4 2018. This mirrors Google’s recently revamped report in November 2018 stating that the internet economy’s growth was faster than expected and is predicted to garner an additional US$40 billion, amassing a total US$240 billion in gross merchandise value (GMV) by the year 2025.

Commanding the biggest market share in total visits amongst the top 10 companies in 2018 were Lazada at 27%, Tokopedia at 17%, Shopee at 15% and Bukalapak at 12%. Lazada maintains its market-leading position despite facing stiff competition from Tokopedia and Shopee throughout the year.

Nevertheless, Shopee overtook the Indonesian e-commerce to become Lazada’s closest competitor by the end of the year. Shopee experienced a 66% growth in its total visits (desktop and mobile web) between Q1 and Q4 2018 (Indonesia, Malaysia, Philippines, Singapore, Thailand, and Vietnam. Visits from its Taiwan domain was not included).

The Fight for the Top Step

Lazada’s dominant position in the region began pretty swiftly, leading the pack as early as 2014 as the most searched e-commerce platform in countries such as Malaysia just two years after its establishment. Since then, Lazada consistently grew its market share to become Southeast Asia’s most visited e-commerce platform.

In 2019, Lazada’s dominant position was almost overtaken by Tokopedia in July and August 2018. The margin between the two players were at its smallest point in August, where the Indonesian e-commerce platform just needed an additional 44,600 in of total visits (desktop & mobile web) to claim the top spot in the region.

Tokopedia was highly impressive in 2019 especially in its ability to sustain significant growth in its online traffic even after its major Ramadan and Hari Raya sale campaign in May 2018.

The Ramadan and Hari Raya period (16 May till 14 June 2018) was the most important festive season in Indonesia. It is a popular sale period as consumers will actively purchase gifts, apparels, and decorative items to prepare for the occasion in June. Among the many successful efforts initiated by Tokopedia to maintain its increased total visits on desktop and mobile web after Hari Raya was with its 9th-anniversary sale, which was held in August 2019.

The Fastest Growing Companies in 2019

E-commerce platforms with the most remarkable growth figures were JD at 246%, Shopee 158%, and Tokopedia at 94%. This percentage was obtained by comparing the percentage of growth in total visits on desktop and mobile web between January and November 2018 to see who grew the most by the end of the year.

JD.com’s exponential growth was due to its continued its expansion into Southeast Asia recently launching its e-commerce platform JD Central in Thailand in October 2018 and has made great progress in Indonesia as well. This was evident as they grew the fastest from 5.4 million in January to 12.7 million in November in total visits on desktop and mobile web.

Two Key Predictions For 2019 And Beyond

A New E-commerce Leader as Early as Mid-2019

We may see a new e-commerce leader in Southeast Asia by August 2019. Leading the charge to the top step would most likely be Tokopedia. The Indonesian e-commerce company was hugely particularly impressive as it was able to challenge for the top spot though it was only available in a single country.

Its success received further validation as Tokopedia quadrupled its sales in the past year and recently raised $1.1 billion from Softbank in December 2018 to become Indonesia’s most valuable startup, valued at about $7 billion. 2019 will be ‘crunch time’ for the online marketplace which has extensive plans to broaden its scale and reach by investing in technology and infrastructure in Indonesia. As such, Tokopedia is well positioned to fast-track its development to take hold of the title as the most visited e-commerce platform in the region.

Although Tokopedia almost overtook Lazada mid-2018, Shopee is also well positioned to capture the top spot as well. Its gains during the Singles’ Day sale boosted its position from 3rd to 2nd to become Lazada’s closest competitor in November 2018. Shopee is expected to receive an additional boost on its annual birthday sale in March 2019 that will run across seven countries where they operate.

Will Lazada be able to fend off its competitors? We’ll find out by end 2019.

The Rise of Non-Regional E-commerce Players

Almost everyone is talking about globalisation and the importance of venturing across multiple countries. However, 2019 could see the continuous rise of non-regional players who are solely focused on a single market. Indonesian e-commerce platforms such as Tokopedia, Bukalapak, and Blibli are good examples of the possibility of thriving in a single market.

Also remarkable in the regional level were Vietnamese e-commerce platforms Thegioididong and Tiki with the average total visits on desktop and mobile web at 29 million and 26 million respectively. Both e-commerce platforms were only available in the Vietnamese market.

This prediction is highly possible as these single-market players still have much potential for improvement in its respective markets. Take Indonesia for example. Statista states that the share of active paying customers from the total population of Indonesia (e-commerce penetration rate) in 2018 was at 40%. A similar figure can be seen in Vietnam, where its penetration rate was slightly higher at 53% in 2018. The e-commerce penetration rate for both countries is expected to rise to 51% in Indonesia and 57% Vietnam by the year 2023.

Taking note of this potential are e-commerce players like Sendo from Vietnam who are investing significantly in new regions to increase its reach within the country. Echoing a similar tune is Tokopedia who obtained US$1.1 billion from Alibaba and Softbank to be a key driver in Indonesia’s economic development and financial inclusion in the country.

In other countries, we see Singapore and Malaysia introducing the digital tax where it aims to level the playing field and provide local players a stronger footing to compete with international players. This is highly significant as international e-commerce players usually escape taxation if they do not have a physical operations centre in the country. As such, this creates an unfair level of competition between international and local players. This initiative by the two countries will probably serve as a role model and inspiration for other countries to follow suit and implement a localised version of the digital tax. This might would definitely create fertile ground for existing and new players to thrive in the expanding internet economy.***

All data on the total visits on desktop and mobile web in this study were taken from global traffic figures from the respective regional sites. Insights by iPrice Group and based on SimilarWeb data.

Article by iPrice Group