We started class today by looking at how to estimate the beta for a bank and then why you may want to adjust the beta for a private company. We also looked at what makes debt different from equity, and using that definition to decide what to include in debt, when computing cost of capital. Debt should include any item that gives rise to contractual commitments that are usually tax deductible (with failure to meet the commitments leading to consequences). Using this definition, all interest bearing debt and lease commitment meet the debt test but accounts payable/supplier credit/ underfunded pension obligations do not. We followed up by arguing that the cost of debt is the rate at which you can borrow money, long term, today.

Slides: http://www.stern.nyu.edu/

Q4 hedge fund letters, conference, scoops etc

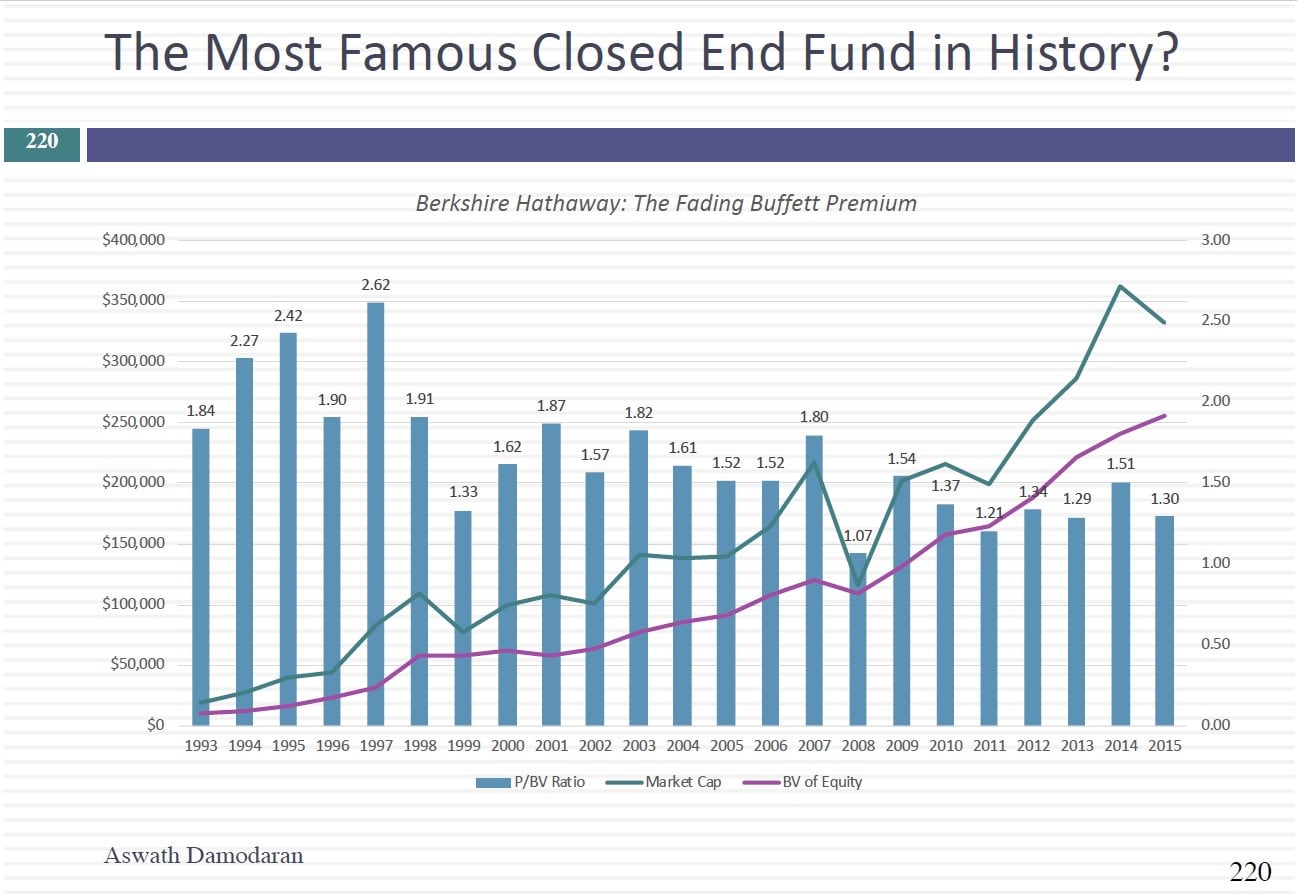

Session 11: Cost of Capital & First Steps on Returns

Transcript

We're talking about the cost of debt. Let me back up though what I say what are the three criteria said you should look for debt. Somebody help me out. Yulia since I now know your name I'm going to pick on you. What are the three criteria. Tax deductible is one. That's actually one criteria you might actually not need in some parts of the be tax deductible most of the word are getting contractual commitment. Excellent. That's good. And if you don't make that payment that's punishment of not punishment something bad happens you fixed payment taxes. We said Using those criteria. Looking at a balance sheet the items that automatically make the list are all interest bearing debt. Bank loans corporate bond short term as well as long term. And we said any kind of contracts with commitment like least common but should be debt. I did not talk about what would not be debt. So let's look at a balance sheet. We talked about what should be that what else is on the liability side of the balance sheet that I do that would not be debt accounts payable supplier credit deferred this deferred that none of that stuff is going to be debt. Why not. Because you don't owe them money but because you don't have an explicit interest payment. Think about the concept. How does it work. You buy stuff from a supplier. He says you can pay me right now wait 60 days straight. But he's not stupid to get paid right now. What does he offer are usually discussed. So when you use accounts payable you have an implicit interest expense but because it's not made explicit we're going to leave accounts payable alone doesn't mean it doesn't affect is in corporate friends it affects the cash flow through working capital.

But it will not show up as debt. And the final thing I said before the end of the class was we need a cost of debt and I told you what I was going to look for. I needed a cost of borrowing money long term today. And I said I'm OK with the short term debt or long term debt. I'm going to bundled up and I'm going to try to estimate the cost of borrowing money today which effectively means I'm going to start with the discrete rate and try to estimate a default spread for you as a company. So let's start easy in terms of estimating default spreads and build up to that are the easiest companies to estimate the default but we can get an updated cost of companies that are bonds outstanding because of bonds outstanding that are traded. Let me add that qualifier because a lot of companies have bonds that never trade they go into somebody's portfolio and they stay in there for the rest of the year onto maturity. But if they're traded what can I observe I can observe the price and the bond in the year to maturity in the book. So if you're a company that is bonds outstanding this seems like an easy solution take a board. Look up the interest rate the yield to maturity in the bond. Use that as your cost of debt. Others tell you that while that is an easy solution it's a very dangerous one and here why.

Can a risky company issue a safe bond yes. Right. And how would you do it. It basically takes its safest assets and backs up the board with the safest asset. That's why if you look at ratings agencies ratings agencies rate both the company and the bond. And you can have actually have different ratings. You can have a single AAA rated company issue or double later in the board or vice versa. The danger of focusing on a board and the yield to maturity is you have no idea whether you're catching a typical Bond a safe bond or a risky bond. But you do have bonds outstanding. You get a bonus with most companies with bonds outstanding also have available on them that you could use to estimate how much default risk you have on them. They have a corporate rating. Actually let me step back. Are you required to get a bond rating to issue a corporate bond. It's actually not required but almost every company does it using why. I'm going to break the mold as a company. I'm going to issue bonds and refused to get rated. You can't. Or what do you think will happen. Investors will look at you guys. Why did this guy refuse to get rated. They will assume the worst about you. So in a sense it is in your best interest to get that rating. And S&P Moody's etcetc. Are there like that and in fact this has now gone global you've got ratings agencies that are country specific that do that within the country attached to rein in it to a great. And S&P and Moody's it goes from Triple J which basically means you are the safest corporation. It's not default free for corporations because with corporations there's always default rates. But AAAS as close to safe as you can get. Going all the way down to D which is you're in default. So it goes triple A doubling and your pluses minuses et cetera. So you've got a whole layer of rate testing how does it help me if you know your company has a triple B rating. I can guess.

{kind=link}