We started the class with a discussion of risk free rates, exploring why risk free rates vary across currencies and what to do about really low or negative risk free rates. The blog post below captures my thoughts on negative risk free rates: http://aswathdamodaran.blogspot.com/

If you want to see my updated perspective on risk free rates, try my data post on the issue from earlier this year: https://aswathdamodaran.blogspot.com/

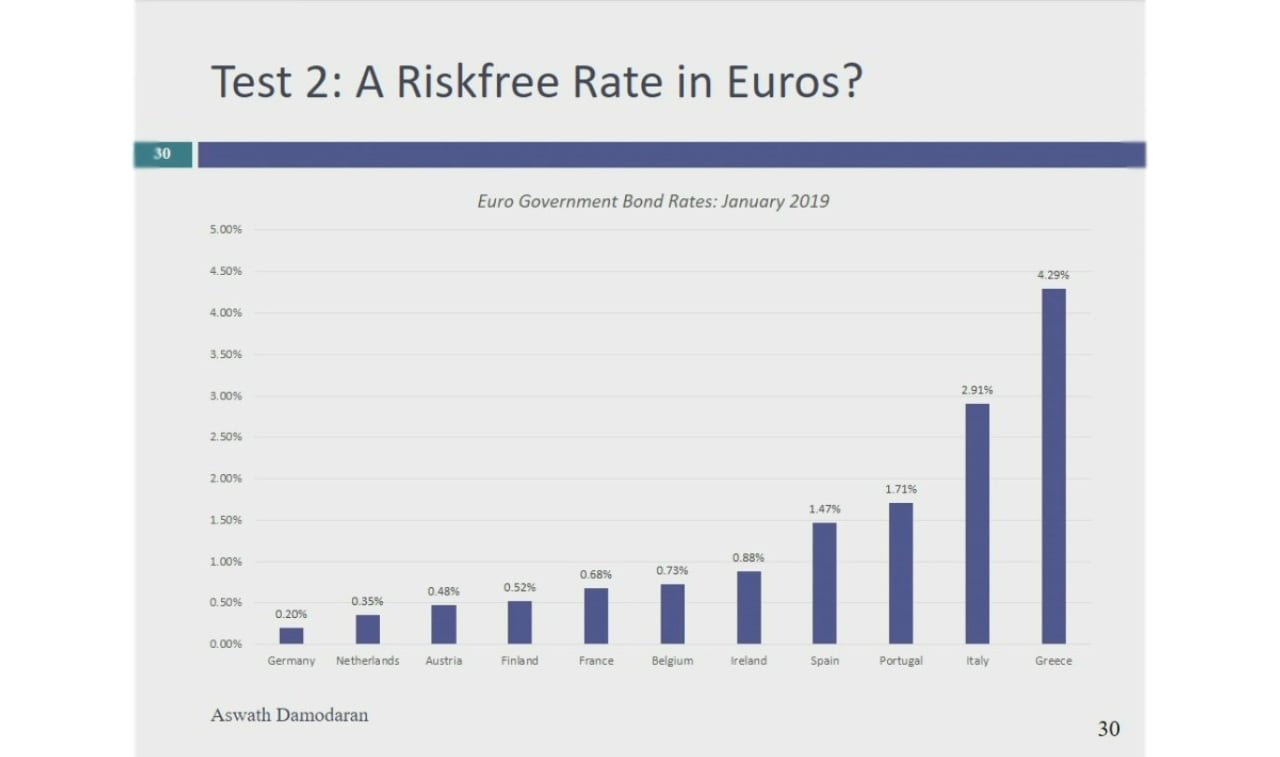

We just started on the discussion of equity risk premiums but the contours of the discussion should be clear. Historical equity risk premiums are not only backward looking but are noisy (have high standard errors). You can the historical return data for the US on my website by going to http://www.stern.nyu.edu/

Q4 hedge fund letters, conference, scoops etc

Click on current data, and look to the top of the table of downloadable data items. Start of the class test: http://www.stern.nyu.edu/

Slides: http://www.stern.nyu.edu/

Aswath Damodaran: First Steps On Discount Rates - Negative Risk Free Rates And ERP

Transcript

So let me start with the two questions again. Who is not part of a group yet. Anybody not in a group yet. Hey this is good everybody is in a group that. Second question. How many of you have not picked the company yet. Now when you get me on this I'm not going to pick on you. OK. Here's my advice. Pick a company soon. Don't sit there going back and forth. It's better to pick a company and change your mind and change the company later then do not pick a company at all. So you have that freedom to change your company. So pick a company soon. A couple other things.

One is as you now know as you probably saw in my e-mail yesterday the IPO valuation is live online and says I did the valuation about 20 minutes before I e-mail you asserted to be just as fresh as it can get. It was after close of trading yesterday so jump in and give it your best shot. As I said early on. You might say look I'm not comfortable yet. Okay change what you're comfortable changing. I think we're up to like 40 or 50 people already in the Google head scratching. So let's see if we can make it a couple of hundred at least. And the other is often today's class I'll send out my first weekly challenge. No I don't know whether I ever told you about this but this is where I'll push you to take what we've learned this week into something that is a little more testing to get the first weekly challenge. You can sign up for this right. Emad's every day I keep harassing you using over tens and drop the class if you want to but I will keep doing this. I'm not going to stop. So let's pick up with that started the class test just as I said I've lost guys and lost two classes we've started with the task let's start with the test and today we're going to talk about discreet rates.

So yes my first question let's say you're Ballingall Brazilian company and you have a choice of adding it either in Brazil Real or U.S. That risk free trade in Brazil real is seven and a half percent the risk free trade in U.S. dollars is two and a half percent to give it just curage and in which currency will you get a higher value for your company. Think about it for a moment. Same company have two different currencies US dollars our Brazil India. I'll give you the rest credit history that is much higher and drier than in dollars. You don't have to answer because late late in today's klise we're going to see the answer the question. Let's see if your answer matches up. So make your choice. In much of Latin America they have a choice to revalue the company nominal terms you build inflation into the numbers or in real Tuck's. If you're choosing to value your company in nominal terms. Which one will give you the higher value using real terms because you love an even lower yield was created in nominal terms because you know you're going to have inflation help you. Or maybe you should get the same value to different currencies nominal or real. So basically the point I'm asking you is we're changing currencies affect my value will going from real affect my value. Give it your best shot right now right now as I said I'm not looking for.

Now let's turn the page.

Lot of you are going to be valuing your company in U.S. dollars. Why because many of you are going to be doing us companies are going to use US dollars as a base of reference and the risk free rate as we would see in class today we're going to use the US Treasury rates and Woodies the team on the table. Drake today is about 2 points 6 3 percent. Yesterday it was at the close of trade yesterday.

That number is low relative to what relative to what it used to be for most of it doesn't sound low.

You know why. Because in your lifetime. This is all you've seen is 2 to 3 percent rates. I tell people you tell me what you think a normal indiscrete rate is I'll tell you how old you are because it's about 7 percent you've been around way too long.

You came to us in the 1980s. If you think it's about 5 percent you probably came around 2000 2001 but there are a lot of people.

This is actually something you will hear from older traders older investors the risk free rate is low and the culprit is always the same.

It's the Fed that did it. We talk about how empty that that argument is but because the Fed's been doing QE and QE 2 Titanic etc etc all the sudden are super liner's. Rates are low. True or false.

I don't think the Fairphone thing meeting is today but it's in the future. Say No let's suppose they get together and they've been talking about raising rates back to a more reasonable level.