Hayden Capital commentary for the fourth quarter ended December 31, 2018, and Carvana memo.

Dear Partners and Friends,

The past few months were tough on our portfolio. Out of the 50 months we’ve been in business, our worst and second worst monthly performance came in December and October respectively. While we don’t manage the portfolio with short-term monthly, quarterly, or even a single year’s performance in mind, it’s important that our partners understand the context for these last few months.

Q4 hedge fund letters, conference, scoops etc

Starting in October, it felt like the bottom fell out of the market. Suddenly issues that the market was serene about just a few weeks prior, were causing investors to panic. There were concerns the Fed was raising rates too quickly, fears that the US economy would slow, US-China trade tensions escalating, China’s consumer confidence declining leading to a slowing economy, fears that the yield curve would invert, and more. During the dark days of December, there were routinely times where we’d see our more volatile investments fluctuate 10 - 15% in a matter of hours! Smaller, more illiquid stocks on our watchlist had trouble even catching a bid.

It just goes to show that trying to predict what Mr. Market’s mood will be next, is next to impossible. Instead, our goal is and always will be to optimize for long-term wealth creation, and part of the trade-off is short-term volatility along the journey.

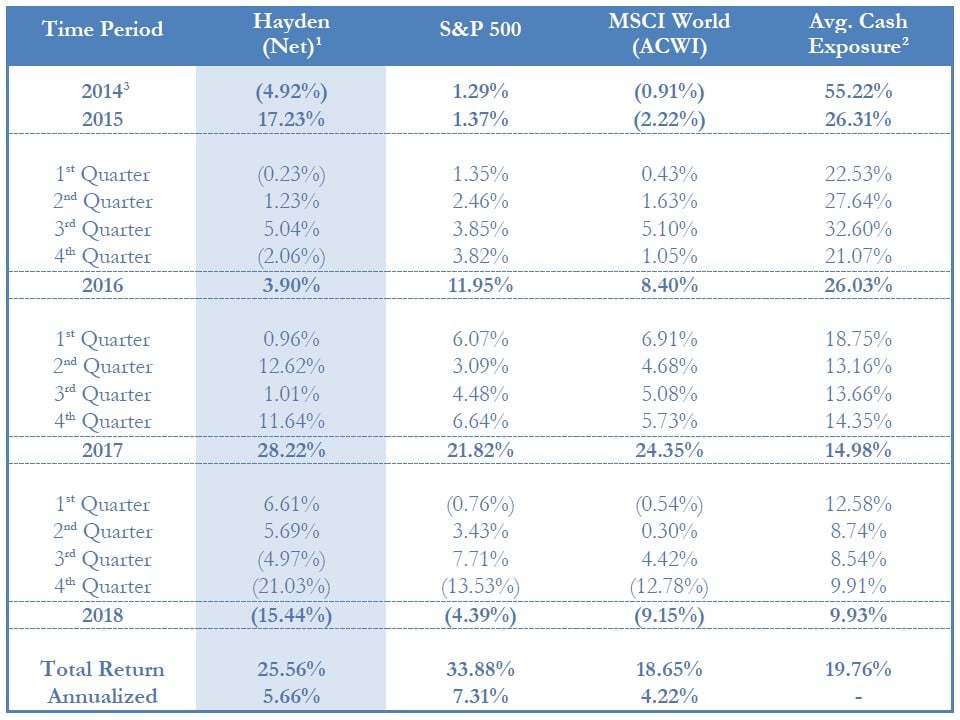

During the fourth quarter, our portfolio declined -21.0% (net of fees) versus -13.5% for the S&P 500 and - 12.8% for the MSCI World Index. We finished 2018 down -15.4% for the full year, while in comparison the S&P 500 was down -4.4%, and MSCI World Index was down -9.2%. Ouch.

Astute partners will note that our overall cash position has seemingly ticked up slightly, when in periods like these, we’d expect to be net buyers. I can assure you while the overall cash balance looks unchanged on the surface, there were quite a few moving pieces underneath.

The largest change this quarter, was the decision to make one of the tracking positions mentioned last quarter (Carvana, discussed below), into a full-fledged position. Second, we’ve been steadily increasing our investments in our highest-conviction companies. In order to fund these purchases, we sold the last of our Markel stake early in the quarter (outlined in our Q3 2018 letter, LINK), as well as trimmed another long-time holding which is nearing maturity4.

When deciding whether to use our existing cash balance vs. selling these two positions to fund the new purchases, I felt the optionality of cash was preferable to keeping capital committed in these near-fully valued companies. What’s remaining of the second position will continue to be a source of cash, as needed. And in fact, as of this writing, our cash balance is already quite a bit lower.

There's A War Going On Out There

“In business, there are two ways to make money. You can bundle, or you can unbundle.” – Jim Barksdale, CEO of Netscape (LINK)

“CAC is the new rent.” – Daniel Gulati, Partner at Comcast Ventures (LINK)

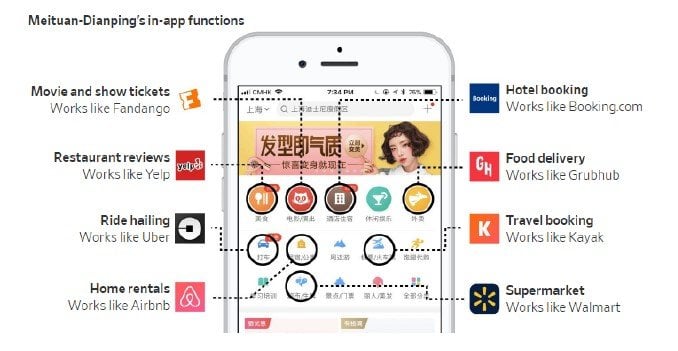

There’s been an interesting trend among certain technology companies lately – expanding into business lines that seemingly are outside of their core competency. For example, why is Amazon moving into video streaming? Or more extreme, that of Meituan Dianping, a $30BN food delivery & restaurant review company in China. What the heck does hotel bookings, movie tickets, ride-sharing, and bike-sharing have to do with delivering lunch?

The trend was originally puzzling for myself (and I’m sure many other investors), since traditionally we’ve been taught that diversification away from the core business typically signals 1) limited room to grow in the core business and so expanding into new business lines is a necessity, and 2) given the lack of expertise in these new fields, diversification typically results in di-worsification.

Meituan Dianping's "Super App"

From WSJ, “Meituan Wants to Be the Grubhub of China (and the Yelp, and the Groupon, and the Kayak)” (LINK)

So why are companies going down this path? A major rationale seems to be rising Customer Acquisition Costs (CAC), or the cost to market to and convince new customers to buy something from you. Due to rising costs, competitive advantages are starting to evolve around having a captive customer (demand-side).

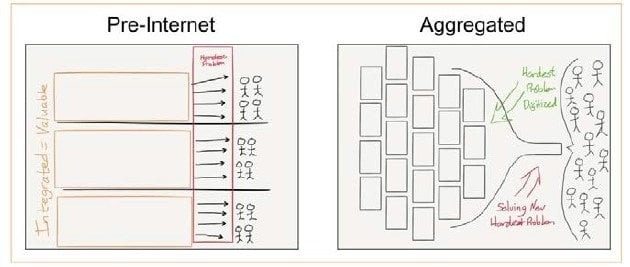

Stratechery's Aggregation Diagram

From Stratechery, who has an excellent article on the topic (LINK)

I’ve discussed how the internet has created unlimited shelf space, and has enabled anyone with a website to sell their products directly to customers, in prior letters. Having distribution and strong relationships with retailers to carry your product used to be a competitive differentiator – an advantage that is now eroding by the day. On top of this, capital has flooded the Venture Capital industry (as investors sought higher returns in longer-duration assets, during a period of low interest rates), thus encouraging an even greater fragmentation of the supply-side. Much of this fresh funding landed in the hands of Direct to Consumer (DTC) brands, which ultimately ended up in the hands of Google & Facebook5.

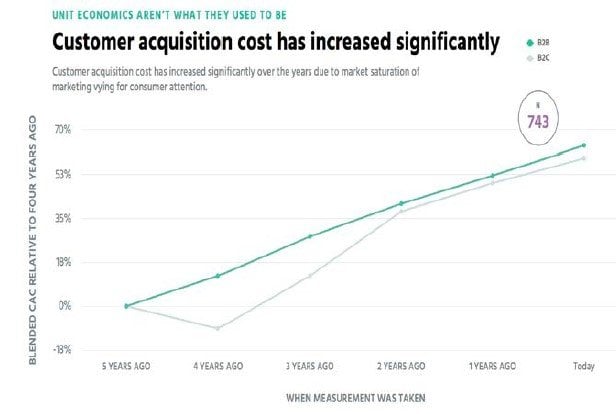

Rising Customer Acquisition Costs

From Tomasz Tunguz; ProfitWell Survey of 743 companies (LINK)

While it’s tough to find comprehensive studies on general CAC trends (as it varies widely by industry), my conversations with both start-ups and larger corporations reinforce my belief that this is a real issue. For example, a survey found that over the span of a decade (2005-16), their participants’ Google AdWords Cost- Per-Click rose ~460% or +17% annually (LINK). Even though this was partly offset by improved conversion rates, it wasn’t enough to prevent Cost-Per-Conversion rising ~220% or +11% annually.

And it’s not just Google… you can see the same trends across Facebook, Instagram, Baidu, Amazon Sponsored Products, etc. The prices on these ad marketplaces are largely determined via auctions, with participants bidding on advertisement “slots” or inventory. Is it any surprise, when both variables of [# of

brands looking to advertise in a category] x [the amount of capital at their disposal] increases, the competition (and thus cost) for a finite number of advertising slots increases as well?

In fact, Customer Acquisition Costs have risen so much, that it’s reached a tipping point where companies are finding its actually cheaper to find new customers the old-fashioned way – in brick & mortar retail and physical ads. Ironically, Amazon Books, Warby Parker, Everlane, and other online DTC brands have launched physical stores in an effort to find cheaper methods of getting in front of customers and promoting their brands. In fact, just take a walk around NYC’s Soho neighborhood and see for yourself (LINK). Even NYC subway advertisement costs have risen ~700% in the last 5 years, due to these consumer technology startups (LINK).

**

So just how did we reach this point, such that there’s an outright war over acquiring new customers? Can’t a company be just as successful finding a way to monetize their existing customers at higher margins, rather than fighting an expensive battle of finding new ones?

It seems the answer is increasingly “no”. Given the lower barriers to entry for a new brand, incumbent companies aren’t able to monetize their customers to the same extent as before. If margins are too high, it’s there’s a real risk nowadays that a new startup will come in and try to undercut the incumbent. This was a lower concern in prior decades, where even if a new company could undercut on price, they still had to deal with the high hurdle of getting distribution. It doesn’t matter if your startup can sell shaving razors for 1/5th the price of P&G, if customers have no where to buy it. But the game has since changed, and companies have found they need to keep margins low to fend off the competition, hoping to make up for it on volume. This model in turn feeds the oft-quoted “winner take most” dynamic, and where scale is required to stay in business.

Within an industry’s profit pools, value typically accrues to the company controlling the scare resource (i.e. where the bottleneck is). With distribution methods and shelf space increasing, the “bottleneck” has shifted to the next scarce resource: customer’s attention and time. Last year, Netflix’s CEO even claimed its competition isn’t other video streaming platforms – it’s other uses of your time like sleep (LINK).

Concurrent with this, companies like Amazon figured out a decade ago, that by aggregating consumers and making them happy (versus finding ways to squeeze every last dollar out of them), they could control this scarce resource, and at the same time grow to unprecedented levels. This is because the ultimate limitation on a company’s size and degree of control over an industry, was and still is, anti-trust (i.e. monopoly) regulations.

What Amazon and similar companies capitalized upon, is that US anti-trust laws exist for the “benefit of consumers”, not their competitors. Simplistically, as long as consumers were in an equal or even better situation, versus if there were increased competition, the US Government has generally been okay with this. Incentive-wise, it also helps that politicians are elected by consumers, not competing businesses.

So logically they said, “Why don’t we flip the traditional business model around? If what’s limiting us from growing larger is that we can’t screw over excessively monetize customers, why don’t we find a way to charge

our suppliers more instead? If we fence-in all the customers and control their habits, the suppliers won’t have any other choice but to pay us.

In pursuit of amassing the largest customer base, we’ll bend over back-wards for our customers, provide free shipping, have suppliers compete against each other to offer the lowest possible prices, and as a bonus get to say to the government ‘Look! Our customers love us, and they’ll surely throw a fit if you try to shut us down (oh, and good luck with getting re-elected in that case)’”.

Fast forward a decade later, and many other companies have figured out this playbook. Combined with the rise of the internet / information transparency, plenty of venture funding, and various new channels to acquire customers (Instagram, Google AdWords, social media influencers, sponsored blog posts, etc.), we’ve entered a new arms war for consumers. There’s a “land-grab” for attention, which has resulted in plenty of discounts, free shipping, membership programs, and even casino-like gamification / addiction features to keep users hooked (LINK).

**

Naturally, this intense competition results in the rising CACs described above. The biggest barrier to success, has become having a captive user base. And once you spend an exorbitant amount of money acquiring a customer, why let such a valuable commodity slip away when they need something that you don’t provide?

Even if they have to temporarily leave your ecosystem, how do you get them to come back, and better yet at an increasing frequency? It’s a fact of business, that keeping a customer is much cheaper than trying to acquire a new one – and worse yet, likely at a much higher priced CAC than you paid years ago for the original customer you’re trying to replace.

Improving Retention Rates

In terms of customer retention, there are several methods to keep customers engaged with the business and coming back. For instance, some businesses launch email campaigns, loyalty programs, or promo codes encouraging customers to come back to the platform more often.

Companies like Shopee (a $4.5 Billion, Southeast Asian E-Commerce company) even launched a feature similar to “HQ Trivia”, where 1 - 2x a day, shoppers receive a notification to log onto the app to participate in a fun trivia game (LINK). Winners receive “Shopee Coins”, which can be used towards future purchases.

However, these types of initiatives aren’t a long-term solution. Like steroids, they only offer a temporary boost, and may even risk cannibalizing demand from the future. For example, in the case of a company like Zooplus, if I order a giant bag of pet food this month because I got a 10% off coupon, it’s likely I’ll just skip my order next month.

Instead, it’s better to have naturally high-frequency business lines to create the engagement and remain “top of mind” for customers. The goals of the high-frequency, low (or even zero) margin services, is to keep the customers addicted and continuously coming back. For instance, food delivery is only 12% gross margins for Meituan (making almost no net profits), but it keeps 21 million orders coming in every day (LINK).

Like the milk & eggs in the back of a grocery store, these offerings don’t make the business much money, but it gets customers in the door with the goal of selling them something else of higher-margin on the way out. And similar to department stores back in the day, they recognize the hardest part is convincing a customer to visit the store in the first place. Once there, they aim to be a one-stop shop for customers, so they never need to go anywhere else.

Shopee Quiz

Instructions for playing (LINK)

Monetize via Other Businesses

For Meituan specifically, their hope is you’ll pick up some high-margin products such as hotel & travel (89% gross margins; LINK) on your way out. And the surprising part, is it’s working! Meituan surpassed Ctrip (the long-time incumbent OTA, with a similar model to Priceline), in terms of hotel nights booked in China early last year (LINK). By having a “free” base of customers to market to, they significantly lowered the barriers to success for themselves, when launching a completely un-related business line. And it worked extremely well.

Additionally, the high-frequency nature of these products has the added benefit of creating new, potentially cheaper, channels to acquire customers. This too seems to be proving itself out (well, sort of). For example, it was revealed that Amazon Prime Video’s CAC was an astoundingly low ~$60 for popular shows, vs.

~$250-400 to acquire a new Prime member using other methods (our estimates). Since most US households watch almost 3 hours of television, in some form every day, Prime Video has the potential for a very sticky / high-frequency product (LINK).

But given Amazon’s Prime Video is barely monetized at the moment, it relies on the other business lines to recoup this $60 CAC. It does this by 1) lowering the customer’s Prime subscription churn rate, 2) getting the customer to use an Amazon product more frequently, and / or 3) encourage those who’ve never used Prime before to give it a try (and since Prime members spend $50 more per month vs. non-Prime members on average, they’ll likely order more stuff too). If a customer simply pays for one extra month of Prime, because they want to finish the latest season of The Man in the High Castle, that’s an incremental ~$30 of high- margin revenue for Amazon already.

Rent Out Your Customers to Other Brands

For platform / market-place companies, there’s another “bonus” source of profits: packaging up all your customers, and then selling access to this captive group to suppliers (i.e. Amazon Prime + Marketplace).

This is possible, because there are benefits to scale within CAC’s too. Amazon can afford to pay more for customers, since they have multitudes of methods to monetize the customer. Comparatively, a small fashion brand can only offer the customer one category of products.

The opportunity, is for Amazon to simply “bundle” up all its customers, and then “rent out” these customers for a far lower price than if the brands were to go out and “buy” customers themselves. These brands & suppliers are increasingly willing to pay up, since the supply-side is getting more competitive and fragmented, which results in the aforementioned rising cost and difficulty of attracting new customers. In this way, Amazon turned a high fixed cost into a variable cost for these brands. And as long as the supply-side keeps getting more competitive, it’s the platform companies that sit in that bottleneck that will benefit.

**

Out of everything that I’ve described above, notice that nothing is “brand new”. As our partners know, at Hayden we don’t tend to invest in new products (this is riskier, since the demand for that new product is unproven). Instead, our investments usually involve companies delivering old products in a new way.

In the above dynamic, the basic framework for these businesses are the same as they’ve been for millennia – there are still producers of goods, middlemen or distributors whose job is to get in front of the customer to sell the goods, and customers who buy them. The only difference is that as technology and business models evolve, the point of “scarcity” changes – most recently from the supplier-side to the demand-side. It’s simply “flipping” the old business model, and charging your suppliers (who have lower bargaining power due to their industry’s fragmentation) and treating your customers like royalty (because their attention is the scarcest resource of all).

Obviously, this trend is just one piece of the changing consumer retail landscape, and certainly isn’t applicable for every company out there. However, it’s affecting a large enough chunk of our investment universe, that this shift in business models is going to continue to cause some uncertainty and confusion for investors for quite some time.

It’s during these periods that we can add value as active investors, utilize our historical & geographical knowledge base to hone these types of frameworks, and capture some of the value in the process for Hayden’s partners.

Note, even though I’ve chosen Meituan and Amazon as the primary examples in this section, there are plenty of other companies following this model. Another example that comes to mind is Grab, in Southeast Asia, which hopes to be a lifestyle one-stop shop offering Ride-sharing + Mobile Payments + Food Delivery + more in the future (LINK).

In a way, these “super-apps” are turning into this century’s “new conglomerates” – except instead of having advantages in distribution or national branding, their advantages lie in their customer’s trust and attention. The lessons from this section should be equally applicable, when studying these types of firms.

I’d also like to point out that I write these musings, not necessarily because they’re immediately actionable. Rather, it’s like basic research vs. applied science. By having these theories and observations, they provide building blocks for our investment theses.

When looking at a new company, we can draw upon these theories for how the world is developing, and see if our target company is on the “right side” of change.

Portfolio Updates

Carvana (CVNA): Carvana is a name we’ve been studying on and off for the better part of a year. It originally came on my radar towards the end of 2017, and we started digging in over the following months. But as we conducted this research, the stock ran away from us (up an eye-popping +220% over the course of the next few months). Deemed too rich, I decided to put the work on the shelf for another day.

In the fourth quarter, we got another shot at it. The shares had declined almost 50% from their highs, while the company had impressively grown their quarterly unit sales by an impressive 116% y/y since our initial research. There were fewer questions as to the viability of the business, the unit economics were starting to come into focus, and break-even was that much closer – all resulting in a reduction in business model risk, in our view. We refreshed the research on it and really dove in, trying to fill in any missing pieces. During the fourth quarter, we began buying shares at an average price of ~$43.

In the appendix, partners will find a copy of a short memo outlining the high-level thesis, written by Philip. It does a good job of explaining the attractive qualities we see – both quantitatively and qualitatively. Car- buying has never been a “fun” experience in the United States, and Carvana is aggressively aiming to solve that. The soft-aspects – company culture, social media engagement, branding, employee satisfaction – are all very impressive. Customers immediately feel that this is a better experience than your stereotypical slimy used car salesman. It’s no surprise that customers are voting with their wallets.

Carvana doubled the number of markets they’re in during 2018, resulting in revenues increasing 130% y/y. More importantly, they’re finally seeing their fixed investments in logistics and brand-based advertising pay off. The evidence is in the cohort data, where each new market has generally shown accelerated KPIs versus older markets.

At some point we may produce a more in-depth research report, diving into the specific economics of the business and the calculations behind it. But for now, I’ll let Philip explain the high-level rationale behind the investment and the opportunity we see, below. If partners would like to discuss the investment further, I’m always available to chat in more depth.

JD.com (JD): On December 21st, we finally received some good news regarding Richard Liu’s sexual assault case. The Minneapolis District Attorney announced that they didn’t have enough evidence to prosecute, and subsequently dropped the case.

If you recall back to our letter last quarter, I thought that the most likely outcome was a civil settlement (which is still possible), while the criminal proceeding would be dropped (LINK). Several parties we spoke to, along with rumors in the media, believed that the Minneapolis DA was already leaning in this direction. They were simply waiting for the “right time” to make this announcement, given the publicly around the case, and their desire to keep the media attention to a minimum. If you notice, the announcement was made on December 21st, on a Friday afternoon, the weekend right before the Christmas holiday… all of which seems to line up with this theory.

In either case, it’s fortunate that the overhang on the stock is largely removed. We can now focus our attention back on the fundamentals, and the vastly more important issue (in terms of long-term value creation) of fending off the competition from Alibaba and other rivals. I’ve outlined our thesis on JD’s business ad nauseam in prior letters, so I’m sure our partners are fairly well-versed in the key points.

At the current price levels, I continue to be optimistic about our investment and will continue to monitor any competitive developments as they arise.

Conclusion

This semester, Tim Teresczuk will be joining us as a research intern. Tim is currently a first-year student at Columbia Business School, and had previously studied finance at Boston College for undergrad. In between, he spent several years in both valuation work and sell-side research, prior to starting his MBA program. We welcome Tim to the team, and am excited to get started working on a few research projects together.

Next week, I’ll also be in Los Angeles for the Daily Journal Annual meeting. Charlie Munger, a hero to many in the investment community, turned 95 this year. Although Charlie is still as sharp as ever, it’s growing more likely that these meetings will come to an end at some point. It seems worthwhile to spend a few days in sunny Southern California, soak up any lessons from a man with an extraordinary lifetime of investing wisdom, and while also checking off a life-long goal of mine.

At the end of March, I’ll also be spending some time in London and a few other European cities, for the annual Zooplus Capital Markets Day. I’ve spoken about the company several times in the past, and it remains a very large position for us. Zooplus is executing well, and is on track to becoming the #1 pet specialty retailer over the next couple years. I’m looking forward to hearing about the company’s strategic plans for 2019 and beyond.

I’m always interested in meeting smart fellow investors, entrepreneurs, or those simply looking to understand what we’re trying to do at Hayden. After all, it’s the collaborative nature of this industry, and the willingness to share notes or insights that makes the job so enjoyable. I’ve met many smart individuals through these coffee chats, who have helped to expand our investing frameworks (and hopefully in the process, I’ve been able to offer them a new angle of looking at these topics too). If anyone is interested in grabbing a coffee in Los Angeles or London, please let me know.

As a reminder, it’s also tax season and our partners will be able to find their tax forms available via the Interactive Brokers portal over the next few weeks. I’d encourage partners to consult their tax advisors, and also reach out if there are any questions or issues with accessing this information.

**

This quarter’s results were volatile, but such is the nature of investing in public equities. As investors, it’s our job to use this volatility to our advantage, and do all that we can to avoid the hefty “get me out of here now” tax that so many market participants pay, during times of turmoil and in the face of mark-to-market losses.

While it’s never fun to report losses, this shouldn’t distract from our focus on the long-term intrinsic value growth of our companies. So long as our portfolio companies continue providing more value to customers, work to eliminate friction / address their customers’ pain points, and in the process attract ever-more loyal customers to the business, I’m confident our portfolio’s returns over time will be very satisfactory.

As always, it’s a pleasure and honor to serve our partners, as we work diligently to grow your hard-earned assets. I genuinely couldn’t ask for a better group of partners. I’m always available via email if you need me, or please drop by the office sometime if you’re in NYC.

I look forward to writing to you next quarter, and hope you have a great start to 2019. Sincerely,

Fred Liu, CFA

Managing Partner

Appendix: Carvana Memo (NYSE: CVNA)

Note: This was originally an internal memo written by Philip Kor at Hayden Capital. It’s been republished here, for the benefit of our partners.

We’ve always been impressed by portfolio managers who were able to successfully bet on what were early- stage companies on their way to disrupting whole industries. For example, Nicholas Sleep of Nomad Investment Partnership’s writings on Amazon from the early 2000s comes to mind. With hindsight, the business case for Amazon and e-commerce may seem obvious. But back then, at less than $7 Billion in revenues, Amazon’s ability to challenge the likes of Barnes and Noble or Walmart was uncertain at best.

Was the investment purely a bet on Jeff Bezos? Was the total addressable market just large enough to take the chance? Was this decision more along the lines of a venture capitalist than a value investor? Is this a type of bet that one can get good at and therefore repeat over time?

These were the questions we had to answer for Carvana (CVNA), our long thesis today. This is a company that intends to disrupt the $764B used car industry by using an e-commerce model. The used car industry is highly fragmented and its biggest player, CarMax, has only a market share of ~1.9%. Over 90% of the used car dealerships are still owned by small mom & pop businesses. We think Carvana is well-positioned to consolidate this industry.

With Carvana’s e-commerce model, there is now no need for each market to be served only by local inventory (what the dealership can buy and display). When coupled with a nationwide logistics network, Carvana is able to deliver the nation’s inventory to any individual market. This lowers the capital required to build inventory in each market.

Carvana is able to keep all its 15,000+ inventory of cars in just four locations (IRCs mentioned below), versus CarMax which has ~350 cars per location. A pooled national inventory improves inventory turns as supply and demand can be more accurately matched nationwide. This lowers working capital and boosts margins as there is less depreciation with quicker turnarounds.

A typical dealership costs at least $20 million to build and set up, including sizeable real estate to hold their inventory. In Carvana’s case, all they need in each new market is $500K: consisting of an optional 10-car hauler, a small office space, and a few flatbed trucks. Even their car vending machines cost just $5m, considerably cheaper than a traditional dealership, and has the added PR value and helps legitimize the brand in consumer’s eyes.

The low capex requirement for expansion along with the lack of a need to build inventory in each new market gives Carvana a scaling advantage that traditional car dealers do not have.

Carvana currently has 91 markets opened, with four (soon to be five) regional Integrated Reconditioning Centers (IRCs) that serve as the “hub” to each market’s “spoke”. Centralized reconditioning processes allows car quality standards to be kept consistently high.

Carvana is on track to sell ~95,000 vehicles this year, about an eighth of CarMax’s unit sales. Growth has been explosive, with unit numbers by end 2018 estimated to be double last years’, and 2017 numbers 2.4x higher than 2016’s unit sales. We expect sales numbers to grow at a moderated, although still rapid, 46% CAGR over the next few years. We expect to Carvana to sell approximately 650K units in five years. If we are right, Carvana will realize over $1 Billion in net profit, and we’ll realize a 23% IRR on our investment.

Below, we’ll describe why we believe the company has a high probability of achieving this. The e-commerce model is clearly superior, so why hasn’t this been done before?

Carvana’s CEO and founder is Ernie Garcia III, whose father founded DriveTime Automotive, one of the largest auto-dealerships in the country. The younger Garcia graduated from Stanford and worked in DriveTime for a few years before starting Carvana, an online version of his father’s business. After growing Carvana internally for two years, it was finally spun off to stand on its own in 2012.

We believe Carvana’s unique relationship with DriveTime from its founding years is one of the reasons why previous online-only car dealerships have not had the same success. Building IRCs is capital intensive, but Carvana was able to lease space from DriveTime’s existing infrastructure. The partnership turned what would have been a significant total $100 Million fixed cost, into a variable cost. This provided it an unfair advantage versus competitors, who didn’t have access to the same terms. In addition, other start-ups would not have had the advantage of industry relationships and know-how that Carvana was able to benefit off DriveTime.

On the other hand, existing auto dealerships would not be able to enter the online world so easily as they face the typical “Innovator’s Dilemma” problem: the internal start up would have faced cultural hurdles from the old guard, and would find it hard to attract required engineering or marketing talent required to scale a technology-enabled company targeting the millennial customer.

Ernie’s unique position as the son of Drivetime’s founder puts him in a better position to push for change within a more traditional establishment. His educational background, relative youth, entrepreneurial drive, and having the personal network required to recruit qualified co-founders, enabled the disruption from within DriveTime. When would be the next time we find a big auto retailer with a son possessing the required qualifications and ambition?

Current competitors to Carvana sell at a fraction of the volume, and face the exact hurdles mentioned above. While they have received investments from brick and mortar car retailers, we don’t expect the integration or sharing of assets to be easy.

At a higher level, we also think consumers’ preferences and trust needed to evolve before the idea of buying cars online was commonplace. It takes a while for e-commerce to disrupt industries dealing in tangible, high- value items. We’ve seen this happen with diamonds, furniture, and clothes, defying sceptics along the way.

Millennials are also more open to buying items from the internet, and Carvana is able to capitalize on this trend and tailor their marketing accordingly. The time is right for a purely online model for cars.

The negative experience of the current car shopping process is a big factor in this push online too. Carvana, as the biggest online retailer, is now in the game of changing consumer behavior. They know this, and it shows in their laser focus on the customer experience and brand-based marketing.

Bringing Silicon Valley to Detroit (or Phoenix): Management’s ability to craft a superior brand.

Everyone dislikes the current car buying process of haggling, visiting dealer after dealer, and wondering just how the salesperson is going to take advantage of you when your guard is down. Carvana’s vertically integrated e-commerce model offers a much better alternative, where you can shop from home and fill up paperwork any time of the day. We like to back a company where the customer themselves would want the company to succeed.

Management has repeated their principle of placing customers first, and from details like how customer service deals with customer complaints, to their social media engagement, to their sales process and policies, we believe the customer-centric philosophy has spread through the organization.

Reviews online have generally been positive. All Net Promoter Score numbers and crowd-sourced review sites have Carvana rated significantly higher than their competitors. We take these numbers with a pinch of salt, but it does offer at least a directional sense and helps rule out extremes. Certainly if a company is hated, they will clearly rank low, and this is not the case for Carvana.

Carvana is being compared and ranked alongside other technology start-ups, which alone is a compliment for any auto-dealer. Do check out their Instagram account (and #carvana hashtag) to get a sense of the employee culture and customer response.

Carvana is very conscious of every touch point with the customer, starting from viewing cars on their site where they have a unique 360-degree car viewing technology for both the exterior and interior of the car. They quote you a trade-in price within seconds for your current car. Financing and conditional approvals are all done online. The whole process takes 10 minutes. Delivery is done on one of their Carvana branded trailers, your traded-in car is picked up, and you even receive a goody-bag of Carvana swag. You have 7 days to test drive the car and return it if you choose to (yes, Carvana will even come pick it up again). Painless and easy.

Ernie, along with his co-founders Ryan Keeton and Ben Huston, are more like successful Silicon Valley founders who just happen to have had the natural advantage of a relationship with an existing large used-car dealership, and therefore found their start-up opportunity. Ernie’s involvement in a previous start up with co-founder Ben Huston called Looterang, all while still working at DriveTime, shows his inherent entrepreneurial drive to do something more.

Delivering a service well adds to the brand of Carvana. But the conscious crafting of a brand uplifts the experience even further. The founders were able to attract top notch creative talent. Carvana’s Chief Creative Officer Paul Keister, for example, spent nine years at Crispin Porter Bogusky, renowned for their BMW Mini campaigns. This fact is easy to take for granted, but we do not think many used car retailers are able to attract such talent.

From leveraging social media, to their ad campaign tie-ups with Disney’s movie Ralph Breaks the Internet, and the exciting vending machines deployed, we believe making the car buying experience fun and having customers feel an emotional attachment to the brand is important. Carvana’s customers skew young, and have better credit than the average used car customer.

Carvana has 15 vending machines, as of the end of 2018. Each vending machine costs $5m to build and may at first come across as gimmicky. In fact, they do contribute positively to sales, as there is an uplift in each market of 2x each time a machine is built. It also legitimizes the brand, so the company doesn’t just exist within a few webpages. Collecting a car via vending machine is chosen by 50% of customers, showing its popularity. The car collection process also automatically produces a video for you, which is meant to be shared on social media, and results in organic referrals. The vending machine ranks high on virality and is great for branding.

Carvana has suggested that the ease and positive experience of buying cars online may prompt people to change cars more frequently, growing the market. We may not go as far, but at the very least, having a strong brand and customer experience will help make sure Carvana is top of mind. This is a moat that not many other auto retailers own.

The numbers: Losses today, but scale and profits to be achieved in two to three years.

Carvana is expected to make a loss of about $240M for 2018, off a revenue of $2B, or a 11.3% EBITDA loss. That has improved from a 16.9% loss a year ago. Thus far, all metrics point to scaling advantages being realized. We expect breakeven in 2020 and profits in 2021. We project $300M of operating losses over the next two years, which we think is comfortably supported by the current $440M cash reserve. There are additional levers the company can pull to conserve cash, if needed.

Carvana aims to be in 200 markets, covering most of the US population, and are currently are about halfway there at 91 markets opened (as of January 2019). Carvana even provides cohort data, which gives a level of transparency that is useful for sales projections. Atlanta was opened in 2013 and went from 0.04% of market share to ~1.9% today. Subsequent cohort years show similar rates of growth. By blending new market openings and maturing of existing markets, we conservatively estimate ~650K units sold in 5 years, or by 2023.

Current GP per unit (GPU) is around $2,200, with half coming from financing and other fees. A typical brick and mortar retailer has a GPU of $3,000. But due to the cost advantages of an online model, we think Carvana is able to hit a GPU of $3,600 at scale. The increase in GPU will come from a combination of sourcing directly from consumers instead of through car auctions, improving time taken to turnaround inventory as scale is achieved, and increasing fees from financing and extended warranties, which have been under-monetized (low cross-selling rates).

Currently, total costs per unit sold are at $4,400. We think that can drop by half in 2022, or to $2,200. One indication of how costs scale is the cohort data for marketing. In the most mature markets marketing spend is at $440 per unit, which is almost three times less than the current cost of $1,181 per unit. To put our costs- scaling assumptions in perspective—as we see a 6.5x increase in units sold (~100K to 650K) in 2023, we only build in a halving of costs.

With $3,600 GPU and $2,200 of costs per unit, this gives a profit per unit of $1,400. At sales of 650K units, that’s $910M of EBITDA. We do think Carvana’s higher growth and low capital requirement should deserve a higher multiple than any other auto retailer today. But to be conservative, we assign CarMax’s (KMX) historical EV/EBITDA multiple of around 16x, and that gives an EV of $14.6B in 2023.

Carvana is trading at $5.3B EV today, which is a 2.8x gain over 5 years, or an IRR of 23%. If the outlook is so great, then why is short interest at over 90% of the float?

There are those that are bearish on the auto market in general and Carvana being loss-making and having the highest EV/Sales ratio seems like the best way to short the theme. However, we believe this is ignoring Carvana’s specific business qualities and unit economics.

There is a risk of ride-sharing and autonomous vehicles shrinking the market for used vehicles, and while we agree that less people in the future may find the need to own cars, especially in dense urban areas, we think Carvana’s ability to capture market share starting from a very small base today will far out-pace the speed of decline of used car sales.

A quick look at auto dealership stocks will reveal how unkind the market has been over the past year, with most trading in mid to high single digits PE multiples today. Compressed margins due to off-lease vehicle supply and rising costs are reasons for this bearish view, and this has led to more M&A between dealerships. We do feel Carvana is best positioned as the industry goes through consolidation due to its lower-cost and lower-capex model, with these saving being passed back to consumers regularly at a +$1,000 discount to competitors. A downturn in the industry in fact gives Carvana a better chance in gaining market share.

Shorts are also concerned with Ernie’s dad, Ernie Garcia II. Ernie senior was embroiled in a savings and loan scandal in 1990 and was fined and placed under probation after pleading guilty to a charge of fraud. The predecessor to DriveTime Automotive was a company called Ugly Duckling, where in 2002, Garcia had taken private after the stock price crashed from $25 to $2.50. DriveTime Automotive deals in the subprime market and was also fined by the Consumer Financial Protection Bureau in 2014. Basically, Garcia II has not had a good track record reputation-wise.

In 2014, Carvana was spun out of DriveTime and Ernie Garcia II is not a director in the company nor does he hold any management responsibilities. He does still, along with his son, own close to 70% of the company, and 97% of voting power.

There are shorts out there that look at the non-straight forward financials of Carvana through the lens of Garcia II’s past actions and feel something is not right. We have dug into the financials and are comfortable with what we see. In fact, the apparent messiness and the fact that the name doesn’t screen well is an opportunity for us.

We also do not think it’s fair to form a judgement on a father’s business history and assume that culture continues to his son. Ernie checks out well, and is very much running Carvana, not his dad. From what we gather, we find Ernie to be thoughtful, driven, and has shown the leadership required to pull together a strong senior team with low turnover. In September, to celebrate 100,000 cars sold, Ernie even gifted $35 million worth of his own stock to his employees.

Let’s not forget that Carvana is very much shaped by the other co-founders too, who have had a hand in creating what we feel is a customer-oriented and employee-engaged organization (from Glassdoor reviews, ability to attract non-automotive industry talent, etc.).

What is the bet here, exactly?

Carvana is a bet on the management team and their ability to execute a business that has shown tremendous growth, a clear path to positive unit economics, attacking a large addressable market, and possesses a strong brand and culture that wins both talent and customers.

Typically, culture clashes impede the growth of an internal start-up. However, we see Carvana as a positive example of Clayton Christenson’s “Innovator’s Dilemma”. The old economy world of DriveTime is incentivized for the new economy version of themselves to succeed, not just due to shared ownership, but also for the simple reason that this is family business, where there could be a hope for the senior generation to witness a “succession plan” that could be even bigger than themselves. With a large ownership stake in Carvana, we estimate Garcia senior’s holdings to be valued at multiples of his Drivetime stake. In this sense, the son has overtaken the father. DriveTime is therefore incentivized in giving Carvana the start it needs with its facilities, relationships and know-how.

An investment in Carvana is a chance to put money behind a growth start-up story, that uniquely also comes with old-economy industry support.

Without an earnings track record, a strong balance sheet backstop, and with execution uncertainty, Carvana sits in a riskier category within a typical value manager’s portfolio; a term we use broadly with the belief that “value” can be found in all places. We attempt to mitigate this risk by holding a smaller than standard position, and to diversify by making sure to limit positions that have similar risk profiles of being earlier in a company’s growth cycle.

Is being early worth it?

The question is: if we project profitability in two years, why not wait till then to invest? The simple answer is that we fear it would be too late. Once the success of the business model is obvious, it’s likely this will be already reflected in the market’s valuation.

We never know when the tipping point of attention will be reached for any stock, and when the multiple may expand. Anecdotally, the name seems to be getting more attention from investors, so the story isn’t entirely unknown at this point. By being early, we are being compensated for taking a view when the rest of the market is still uncertain.

We estimate that ~$1.8B of capital has been already been put into the business, to get it to where it is today. This can be thought of as the approximate tangible replacement cost for the business, and doesn’t even include the qualitative advantages Carvana benefits from, as described above. If our analysis and thesis is correct, we expect to make multiples of our investment within just a few years, as customers and the market alike recognize the advantages of this business.

This article first appeared on ValueWalk Premium