Logos LP commentary for the fourth quarter ended December 30, 2018, titled, “The Stock Market of 2018.”

“Most of the change we think we see in life is due to truths being in and out of favor.” – Robert Frost, “The Black Cottage” 1914

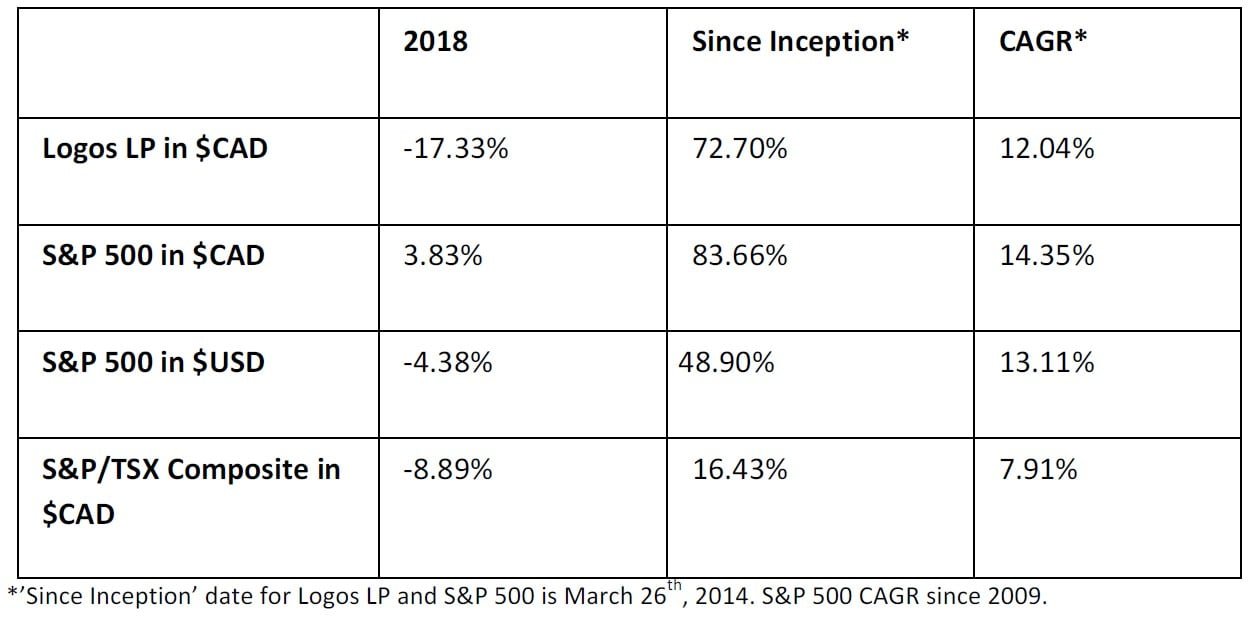

The following table represents Logos LP’s 2018 total return compared a basket of relevant indexes. The current price per unit (as of January 18th) is $22.73 compared to $20.74 as of December 30th, 2018:

Q3 hedge fund letters, conference, scoops etc

Annual Performance and Expected Returns

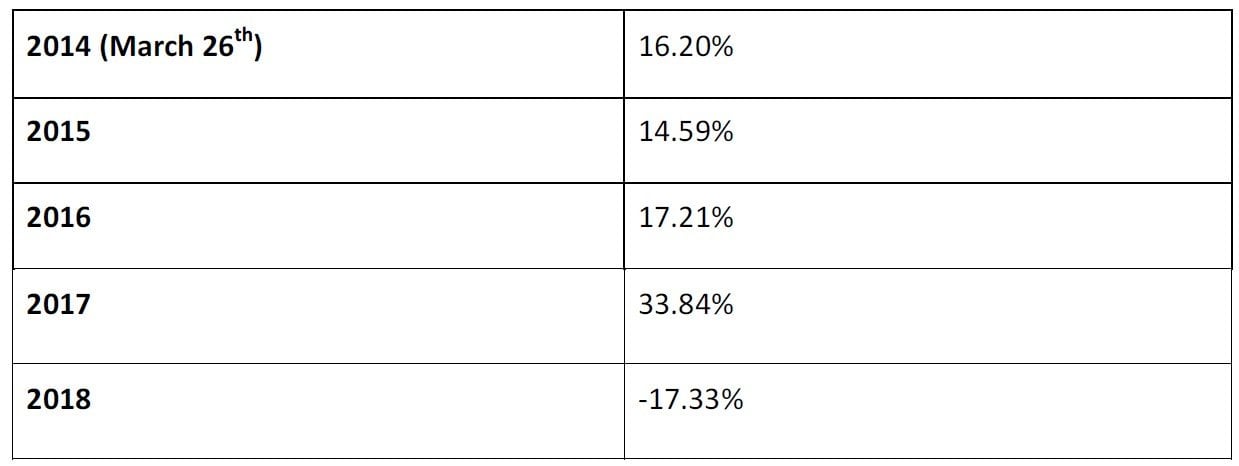

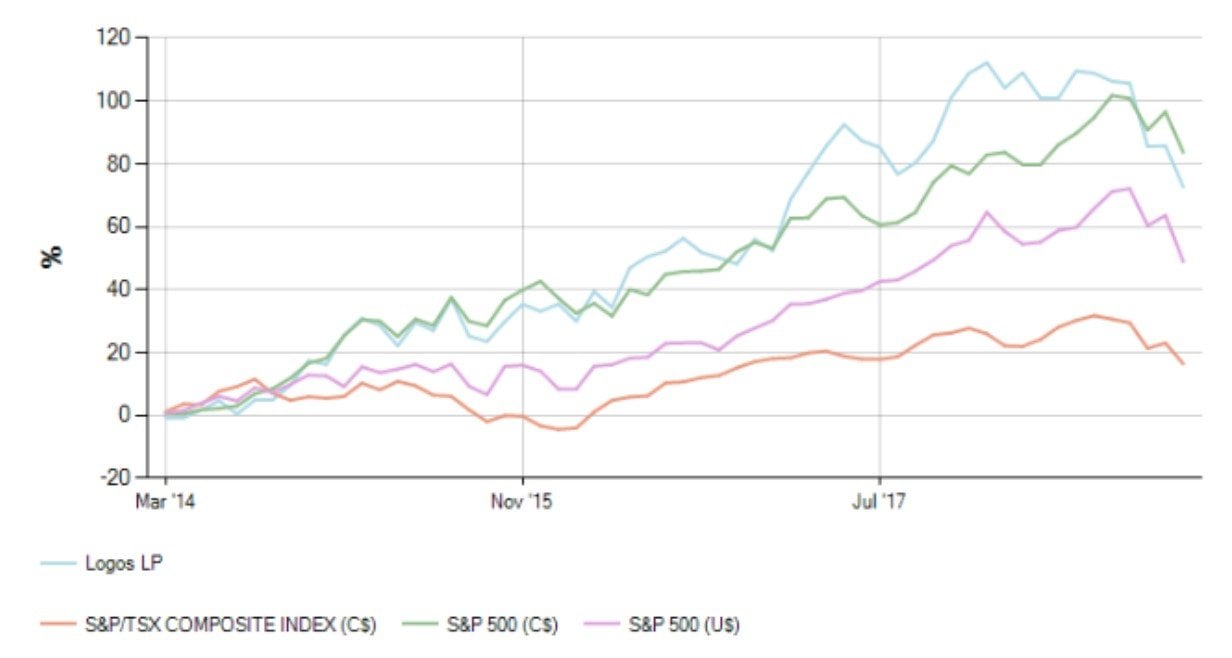

The following table represents the annual performance for the portfolio over the past 5 fiscal years. The graph below also shows the total cumulative performance of the fund versus various indexes:

Annual Returns:

Performance versus Various Indexes:

As indicated in the last quarterly letter, 2018 has been a challenging year for the fund and we were greeted with tremendous volatility in the last quarter of the year, with December ultimately being the worst month for the fund (ever) as well as the overall stock market since 1931. Part of the decline in performance was due to enhanced market risk as new positions were initiated, which increased volatility, particularly in the last 2 months of the fiscal year. Moreover, certain core positions (stocks we are bullish on for the long-term) declined due to macroeconomic factors that were inescapable in the short-term. One example of such a stock was Lassonde Industries (one of two of the largest private label juice companies in North America). This year its stock price declined over 21% due to margin contraction linked to rising transportation, raw material and packaging costs. The same story applied to Richilieu Hardware earlier in the year (a name we sold in mid-2018) as it faced a tougher housing backdrop, trade tensions and a rising interest rate environment.

Despite the seemingly painful declines in the last quarter of the year, there was a silver lining for 2018. It was twofold: 1) the fund closed the year with its highest cash position since inception; and 2) the fund was given what we believed to be one of the best buying opportunities since the 2016 panic. The immense volatility starting from mid-September to the first week of January (a span of over 110 days) presented us with a variety of buying opportunities which we were happy to take advantage of. As Charlie Munger reminds us:

“Patience combined with opportunity is a great thing to have. My grandfather taught me that opportunity is infrequent and one has to be ready when it strikes. That’s what Berkshire is.”

Such opportunities presented themselves as several stocks on our conviction watchlist fell well below our desired price thresholds despite earnings growth and rising intrinsic value. The week of December 24th, was a period of peak fear and pessimism as the market appeared to be pricing in a recession contrary to our belief that no recession is likely in the near term. In fact, the immense volatility experienced throughout this period may have lengthened the bull market as expectations went from 20% earnings growth on the S&P 500 to recessionary earnings growth in a matter of a quarter. Many analysts and managers have been and are still pricing in a recession within the next 2 years but there are few who are pricing in a 15 to 20-year bull market starting from 2009 (or a bull market like the 1981-2000 period) and many experienced investors are still suffering from recency bias living in the shadows of 2008.

Interestingly, the S&P 500 headed into 2019 with a P/E ratio right in line with its historical average going back to 1929. Furthermore, if you look at the last 30 years going back to 1990, its forward P/E suggests a discount to its historical average (not to mention that we still have a 2-handle on the 10 year). As such, coming into 2019 the balance of probability appears to be to the upside.

Although we made our purchases with a long-term investment horizon in mind (think decades), some of the purchases have already begun to pay off as the fund as of this writing is up just shy of 10% for the year. A few names we purchased during this period of volatility include Churchill Downs, CGI Group Inc., Cerner, Huntington Ingalls Industries, Kinaxis and Acuity Brands. We continue to monitor the portfolio and still have quite a bit of available cash to deploy (we are always on the hunt for high-ROIC companies that are reasonably priced), but we are now in a ‘wait-and-see’ mode with the current portfolio. 75% of the portfolio is in 10 names which include the following:

- Church & Dwight

- CGI

- Cerner Corp

- Lassonde Industries

- Visa Inc

- Huntington Ingalls Industries

- Tyler Technologies

- Ross Stores Inc

- Kinaxis Inc.

- Home Bancorp Inc

Outlook for 2019

Although we don’t not see any immediate threat of a global recession, we do see a slowdown in global growth and corporate earnings in 2019, with the U.S. economy likely entering a late-cycle phase. We expect the Federal Reserve’s policy to become more data-dependent as it nears a neutral stance, making the possibility of a pause in rate hikes a key source of uncertainty which will lead to continued volatility.

Markets will likely continue to be vulnerable to fears that a downturn is near especially if the White House’s actions remain erratic and at times non-sensical. One event risk for next year is that Washington gridlock may wreak further havoc on the market when the debt ceiling needs to be raised in March – brinkmanship is a risk as it was in 2011.

When it comes to specific stocks, we see quality as a favorite choice for investors: cash flow, margin expansion, sustainable growth, secular growth trends and fortress balance sheets. The U.S. will likely be a favored region, but we expect emerging-market equities as well as select Canadian equities offering improved compensation for risk.

We also believe that there is a chance (that many are not pricing in) that markets will break out massively to the upside if several uncertainties which have clouded the minds of investors are resolved. To name a few, think Brexit, China-USA tensions, grid-lock in Washington and fears of China slowing down. The buying would be exacerbated by the fact that investors have already reduced portfolio risk in 2018 and seem poised to continue to do so in 2019. The FOMO buying by excessively bearish managers caught flat footed could be intense.

As for our fund, we look to stay the course and will likely be far less active in 2019 than we were in 2018.

Activities for the Quarter

As mentioned earlier, we made some significant changes to the portfolio given the opportunities presented during the bear market of 2018. We were net buyers of the following stocks: Cerner, Acuity Brands, CGI, Visa, Tyler Technologies, Kinaxis, Ross Stores, Churchill Downs, Marathon Petroleum, LeMaitre Vascular and Huntington Ingalls Industries. We were net sellers of Lassonde Industries, Mettler-Toledo and Altria. We sold out our position in IAG, JNJ, Couche-Tard, J.M. Smuckers, and Ollie’s Bargain Basement. We continue to monitor specific names we mentioned in our previous letter (such as MTY Food Group) in addition to new names we have purchased (particularly Cerner, Huntington and Tyler). Given our cash position in addition to additional capital contributed by new and existing LPs, we have also compiled a larger watchlist of stocks as many names in the market are trading at attractive multiples given expected earnings growth. The current rise in the overall market since December 24th has deterred us from making any large purchases in the new year and we believe that remaining patient is the best course of action at present. As Charlie Munger reminds us regarding discipline:

“We have this investment discipline of waiting for a fat pitch. If I was offered the chance to go into business where people would measure me against benchmarks, force me to be fully invested, crawl around looking over my shoulder, etc. I would hate it. I would regard it as putting me in shackels.”

Although we believe that the immense volatility we experienced in December is behind us, we continue to remain cautious and will act when the right opportunity presents itself.

All the best for a 2019 filled with contentment,

Peter Mantas

General Partner, Logos LP

Matthew Castel,

General Partner, Logos LP

This article first appeared on ValueWalk Premium

{kind=link}