Whitney Tilson’s email to investors discussing Seth Klarman’s letter; I’m not as bearish; portfolio management; The Truth About Marijuana, Mental Illness, and Violence.

Note ValueWalk has Klarman’s full letter (please do not emailing us to ask for it) but we will have more coverage very soon here

1) Seth Klarman is a true investing legend (rightly called the “Oracle of Boston”), so his annual letters are always eagerly read by those who are lucky enough to get a copy (he’s always been kind enough to send me one, but I can’t share). I haven’t received his 2018 yet, but a couple members of the media have. Here’s Andrew Ross Sorkin in today’s NYT: Chilling Davos: A Bleak Warning on Global Division and Debt. Excerpt:

Q3 hedge fund letters, conference, scoops etc

As business and political leaders arrive in the Swiss Alps for the annual meeting of the World Economic Forum, a surprisingly alarming letter from an influential investor who studiously eschews attention has already emerged as a talking point.

The letter, written by Seth A. Klarman, a billionaire investor known for his sober and meticulous analysis of the investing world, is a huge red flag about global social tensions, rising debt levels and receding American leadership.

Mr. Klarman, a 61-year-old value investor, runs Baupost Group, which manages about $27 billion. He doesn’t make the annual pilgrimage to Davos, but his words are often invoked by policymakers and executives who do. His dire letter, which is considerably bleaker than his previous writings, is a warning shot that a growing sense of political and social divide around the globe may end in an economic calamity.

“It can’t be business as usual amid constant protests, riots, shutdowns and escalating social tensions,” he wrote.

He made the remarks in a 22-page annual letter to his investors, which include the endowments of Harvard and Yale and some of the wealthiest families in the world. It was being passed around ahead of the Davos gathering, which draws business leaders like Bill Gates and Sheryl Sandberg, social and cultural figures like Bono, and elected officials like Chancellor Angela Merkel of Germany.

Mr. Klarman expressed bafflement at how investors often shrugged off President Trump’s Twitter outbursts and the retreating American role in the world during the past year.

And here’s an article by Jason Zweig in the WSJ: Value Investor Klarman Watching for Stumbles Among ‘Unicorns’. Excerpt:

How can value investors, who seek to buy stocks at depressed prices, prevail in a financial world dominated by market-matching index funds?

That’s the main question posed by Seth Klarman, chief executive of the Baupost Group, the $32 billion hedge-fund group, in his 2017 year-end letter to shareholders.

“Could Baupost itself be disrupted?” asks Mr. Klarman in a copy of the letter reviewed by The Wall Street Journal.

He cites companies like Amazon posing an existential threat to existing businesses. “Today, taxi medallion owners, traditional newspapers, shopping malls and department-store chains are gravely threatened,” he writes. “Discussions in the Baupost conference rooms are increasingly likely to include an assessment of what Amazon executives are discussing in their conference rooms.”

2) I’m not as bearish as Klarman. While I share his concerns about “constant protests, riots, shutdowns and escalating social tensions” and there are certainly economic warning flags I’m monitoring closely, the U.S. economy remains remarkably healthy, the Fed may take a pause on increasing interest rates, and valuations, while high, aren’t extreme, so my best guess (and it’s only a guess) is that the market muddles along. Here’s Justin Lahart in the WSJ on how strong Q4 corporate earnings are shaping up to be: Earnings: First, the Good News. Excerpt:

…despite Apple, earnings warnings have been muted. By Refinitiv’s count, the ratio of companies with negative earnings pre-announcements to those with positive pre-announcements is 1.5—well below the long-term average of 2.8. In the third quarter, the negative-to-positive ratio was 1.4, and eventual earnings growth ended up at 28.4%, versus the 21.6% analysts expected at quarter end.

Another plus: Among the admittedly small number of companies that already have reported results, some 85.2% have topped estimates. That compares with 64.5% historically and 78% over the past four very strong quarters.

Nor, despite all the recent worries, did anything really adverse happen to the U.S. economy over the course of the fourth quarter, even as Wall Street’s favorite economic indicator—the stock market—stumbled. Indeed, the cuts to earnings estimates may have something to do with falling stock prices tempering analysts’ moods.

3) One of my students from the first seminar I taught 13 months ago, Peter Gylfe, wrote this thoughtful response to a question posed by one of my other students about whether it made sense to use a more rule-based system for portfolio management:

On the upside case where a stock is working, I sell some as it gives me more flexibility so I have room to add if it later goes against me. And I sell it all when I find something else more compelling – I’m a big fan of forced ranking all positions and new opportunities.

But how to trade the upside case is easier.

Far more important is the process during drawdowns – this is what separates average portfolio managers from the great ones.

I’m probably out of consensus here in that I favor some rules – at the end of the day, we’re in the decision-making business so you want to keep a clear head, which is hard during a drawdown so it helps if you have a plan going in (you don’t want to be making it up as you are in it) and the last thing you want to do is be on tilt and compounding errors.

I’m in the camp that’s it always best to live to fight another day and so nothing is worth dying over – there are always more opportunities so you don’t have to get it back the way you lost it.

We trade mostly pairs so I do it at the pair level but you could do the same at the portfolio level. (I think it’s better to break the portfolio down into as small a subgroup as you can. So, for example, maybe you have inside your portfolio a consumer book, tech book, energy book, etc. You want to be able to triage the specific area that’s causing the drawdown versus generalizing about the whole portfolio, which is very hard to do.) Go back and look at all of your drawdowns and see if there were any common (qualitative AND quantitative) characteristics and what did the paths and volatility look like.

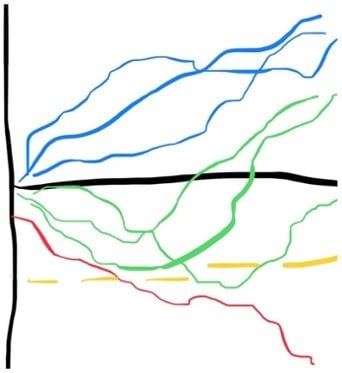

My bias is your investments look like this (P&L on the horizontal axes and time on the vertical):

When I look back at all of my investments (which look somewhat like the above but with a lot more lines), what I found was past a certain point (which will be different for everyone given the types of trades you make and the volatility you underwrite), the investments became negative expected value. When you run the statistics you’re going to have hundreds of observations on different investments so you should be able to get some statistical significance out of saying past a certain point on average the investments do not reverse. I think everyone wants to believe they come back, but some don’t and you’ve got to be able to identify those as quickly as possible and get them out of the portfolio.

When I look back at all of my investments, I basically draw two of those yellow lines. The first one calls out that they’re starting to be a problem but it’s not past the point of no return yet, so at that point I start from scratch and try to re-underwrite the thesis, etc. – all the normal stuff you’d do. But cutting the position is discretionary.

Then I have a second yellow line down further – where I sell the stock. In some ways I think about this similarly to the way our legal system is structured. I’m sure you all know the example, called Blackstone’s Ratio: “It is better that ten guilty persons escape than that one innocent suffer.” There are going to be some of those stocks that come back and you’ve got to be able to live with that but getting the few that don’t come back out of the portfolio vs. continuing to double down on them is career saving. I just think you have to get those red lines out of the book and it’s okay if you let a couple of the green ones go in the process.

Past the second line I’m out and I don’t let myself come back to it for 30 days, which gives me time to think with a clear head. I’m a big fan of knowing that you can always buy it back.

In response to this follow-up question, “Do you have rules for managing the upside - when a trade goes in your favor?”, Peter added:

I just force rank the longs and all new opportunities (which for me is a weekly process) to ensure the portfolio is expressing the views I intend it too (otherwise you get drift vs your underlying views). I think forced ranking gets you a lot of the way there (and just the normal inputs you’d think of: conviction, catalyst path, how variant is the view, valuation, how hedgeable, volatility, etc.).

Then sizing or trimming is naturally going to flow out of that.

Unrelated to all of that, I’m always a fan of locking in a little. I use to work for a great PM who called it “donating to the profit gods.” You lock in a little on a good trade and then have more flexibility going forward to add later if it goes against you.

Unrelated but related while you’re looking at data: The outside view is that most people are terrible at sizing and would thus be better off running something more equal weight than “conviction ranked.” (If you haven’t looked at your data you should: you can easily go back and make all your trades equal weight and look at that vs. your performance.) You might find that sizing isn’t adding that much value and you’d be better off just having 20 5% longs, for example, and spend your time focusing on finding the right 20 vs sizing/trading.

4) I just finished reading (listening to) Alex Berenson’s new book on marijuana, Tell Your Children: The Truth About Marijuana, Mental Illness, and Violence – and it’s pretty damn scary.

(If you don’t have time to read it, here’s Berenson’s NYT op ed: What Advocates of Legalizing Pot Don’t Want You to Know)

After reading two rebuttals (What Alex Berenson’s new book gets wrong about marijuana, psychosis, and violence and Is Alex Berenson Trolling Us With His Anti-Weed Book?), I’m less scared – but still gravely concerned that the champions of cannabis, who I can only describe as a cult, are leading us down what could be a VERY dangerous road, extolling it as a miracle cure (even when evidence is thin or even contradictory) and downplaying its many potential harms.