GreenWood Investors letter for the third quarter ended September 30, 2018, titled, “Time to Simplify.”

Q3 hedge fund letters, conference, scoops etc

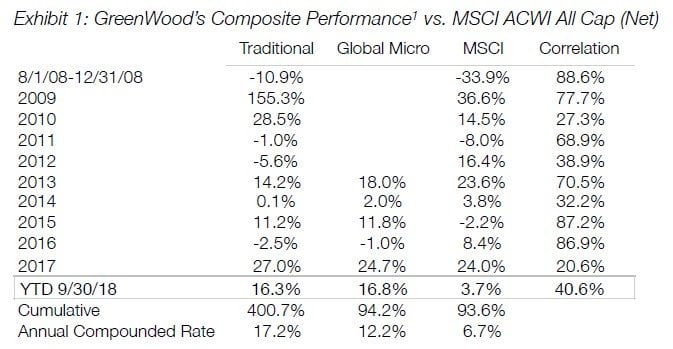

When typical market behavior becomes more difficult to predict, either as a result of robots, unprecedented monetary policy or some unknown unknown, do we run and hide or do we take advantage of the opportunity? The answer is obvious for us, as all of our best-performing investments were implemented during very emotionally volatile conditions for the particular security, country or economy. Just because the next tick in the price of a stock is less predictable doesn’t make the opportunity any less attractive. In fact, it’s what gets us quite excited. As we outlined in last quarter’s letter, large gaps between perceptions and reality drive a very large portion of our alpha. Accordingly, although we had a quarter that was not satisfactory (-4.2% for the Traditional Composite, -4.3% for the Global Micro Composite and -0.8% for the Global Micro Fund), in an otherwise decent year, I’m very convicted in our opportunity set today. Our portfolio’s risk-adjusted return today has hit an unprecedented high. While this is an art and not a science, this has been the most reliable indicator of forward-looking performance.

Historical performance is important over longer periods, but I’m always trying to improve our process in order to maximize our future returns. We’ve re-allocated capital towards the most timely and most attractive opportunities and today, our Traditional portfolio’s risk-reward (the one for which we have the longest history) has hit a record high of over 50x. The Global Micro accounts, which have individual short exposure, have a more favorable profile in the 60’s and our Global Micro Fund’s risk-reward has surpassed 70x. This is because our largest position in the fund is an investment in our coinvestment fund, which is our highest conviction name and perhaps the most attractive position we’ve found since Fiat in 2011. Success here, like many other of our positions, will be measured with X’s, not %’s.

When I first set up GreenWood, in our first year, “we” managed $2 million. With many thanks to our investors and to our performance, we now manage over $60 million. While our scrappy structure is still manageable at what is still a very small size, with both separate accounts and multiple funds, we’re taking the opportunity to simplify our structure over the next quarter. Clearly, a structure that cannot add exposure to our highest conviction name for all clients is suboptimal. We’re making sure this doesn’t happen again, while at the same time, simplifying our lives quite a bit. Starting January 1, 2019, we will only offer our current domestic fund and a new international fund with the same terms as domestic, but with more favorable tax considerations for international investors. We will ensure our European investors will have no issues with the domicile or regulatory structure. Of course, our current European investors can enjoy the same account and terms they’ve received thus far. Each fund will have separate classes, and we are closing the current Founders’ Class to new investors at the end of this year.

Given subscriptions to our coinvestment fund are closed, we are taking this step to close the class in order to limit dilution to our best idea. We still have capacity in the fund today, and will be closing it before the weight of our coinvestment drops below an acceptable level. Our coinvestment has a waiting list building for entry, and our Founders’ class will also be the first in line for increasing its exposure to this opportunistic idea.

Because we cannot build a proper infrastructure with a 0% management fee, subsequent classes will carry a 1% management fee, but in order to offset this, we’re adding a 5% hurdle to the current 15% performance fee. The current separate accounts with a 1.5% management fee will no longer be available in 2019. Our ranking framework of constant portfolio optimization adds transactional alpha that has typically more than offset this relatively modest fee structure. Of course, I will continue to take zero salary, and will only get paid when my capital performs alongside investors’. In order to eliminate any future temptation to gather assets, we’re also committing to reducing our management fee as our assets continue to scale. Given the current fund has no management fee, we will introduce a hurdle to the performance fee for our Founders’ Class. This will have the effect of making the Founders’ class carry a slightly more favorable fee structure, but our founding investors deserve the benefit for helping us build this firm. Existing clients can continue to add under original terms, or roll into the new structure.

This new simplified structure will ensure all investors have access to our best ideas. Just like the last coinvestment fund, we will prioritize our investors for access to any future coinvestment ideas. Using a multiple-class structure, we will also take steps to limit dilution in future coinvestments through closing subsequent classes. We have no other coinvestment on the horizon today, as we are quite busy ensure this first one delights our investors. Yet, we are already convinced our early engagement with the company’s management, board, shareholders, competitors and partners will add considerable gamma (outperformance driven by our efforts) to our performance. And just like our other investments, we are hunting in markets and industries that are on few other investors’ radar screens.

Lastly, our transparency of the fund’s holdings will not change. We update our exposures monthly for investors, along with the most refreshed risk-reward of each opportunity. While much of the research and engagement efforts have been focused on the coinvestment throughout the year, we recently published comprehensive updates to Rolls-Royce and Ferrari, with EXOR, Bolloré, Telecom Italia and TripAdvisor on their way in the next couple of weeks. We believe this transparency combined with education keeps all of our expectations and interests aligned. It also provides incredible insights for our diligence process, as our investor base is comprised largely of very successful business builders, many from the same industries in which we are investing, and professional investors.

As we explained in our last letter, we’ve had to limit the audience for this research as we are loathe to affect market expectations. We’d prefer the market to be pleasantly surprised by the positive fundamental and often transformational changes that are on the horizon for most of our portfolio. The wider the gap between expectations and reality, the better will be our near and medium-term performance. However, we are not managing our portfolio for short-term performance. In fact, the very edge we believe we’ve had is taking near-term risk for long-term significant rewards. Few investors, particularly asset managers that are growing today, are willing to endure volatility. Looking at the opposite of our approach, GE is a terrific example of what happens to companies that, along with nearly 80% of other companies, maximize short-term profits with little care for the long-term trajectory. Decades of “beating the quarterly guidance,” have resulted in a very large destruction of value not just for shareholders, but customers, employees and communities that are paying the price today.

Family-controlled companies in Europe and founder-led companies in Silicon Valley have helped provide a refuge from this myopic market. Yet, as interest rates rise, discount factors for all investors around the world will continue to rise. This will have the effect of causing investors to shorten their time horizons even further. With higher discount rates, cash-flows that will materialize far in the future will suddenly have a much lower value today than in a zero-interest-rate world. Many of the companies, particularly out of Silicon Valley, that invest for the medium and long-term have very high valuations today (or low FCF yields), and they are significantly more susceptible to yields rising in all asset classes. Because fund raising in venture capital has typically been highly cyclical, corporate America will soon face an alarming dearth of investors willing to look out beyond the next quarter or two. We’re going to expand on this topic in a presentation for the upcoming International Value Investing Conference in Luxembourg later this month. Investors, of course, will be receiving the presentation before it’s presented. As always, critical feedback will be most welcome.

Rising rates will favor our value-focused portfolio, as when yields rise by 1%, it has a very magnified effect on an asset trading at a 2% free-cash-flow (FCF) yield, but limited valuation impact for companies, like ours, that trade at doubledigit normalized FCF yields. Yet, despite the deep undervaluation, these are not forgotten companies wandering through the desert. They are mostly well-run businesses with competitive advantages. The management teams will not sit still, they will continue to create value. Thus while a security like Telecom Italia has hit record lows, the fundamental value of the company keeps modestly increasing, creating a double-boost to the margin of safety.

Because we seek to optimize our investments for risk-reward (value), quality (conscious capitalist principles), and the expectations gap, we typically own an eclectic portfolio full of names that most people either haven’t heard of, or look like they don’t quite fit together. Since we’ve optimized across these very different investment lenses, we won’t have to necessarily tread water in a sideways or negative market. We expect most of our portfolio will deliver news that will pleasantly surprise its skeptical audience over the next year. For example, we believe asset sales are on track within EXOR’s portfolio companies, Bolloré’s portfolio companies, and Telecom Italia. These sales or separations will be key to both a re-rating of these companies but also will allow all companies to take advantage of the very low valuations and wide discounts to fair value where they trade today, which remain near record levels. Telecom Italia is trading at a valuation lower than a Russian telecom, and the country is being treated by investors today as a banana republic. We’re not going to get into a macroeconomic discussion here, but let’s just say we’re finding ourselves increasingly in disagreement with the “establishment” in Brussels which looks determined to prohibit independent government policy despite growing revolutions in nearly every country. Leading economic indicators in Italy are still positive and outperforming much of the rest of Europe, just as investors have decided they are not interested at any price. We have been taking advantage of this wide gap between sentiment and reality and price-agnostic selling.

Despite the positive performance this year, we still believe the market is materially underestimating the near-term earnings power of Rolls-Royce and TripAdvisor, with longer-term estimates further off the mark. These five investments form the core of our high-quality, low-valuation portfolio where we’ve concentrated over half the fund. The smaller positions in our portfolio are more asymmetric, but slightly lower-quality investments. A few years ago, some suggested that we focus only on the quality-value names and ditch the special situations. Yet, these opportunities have generated significant alpha for us, and returns are completely independent of what is happening in the economy or markets with high cross-asset correlations.

In rare occasions, like Fiat-Ferrari, these continuums converge and we get an event-driven investment opportunity that also has high quality assets and a deeply discounted valuation. This convergence is why we went big on our coinvestment name, as there are very high quality aspects of its businesses, the valuation could barely get more depressed, and we are working on significant value-unlocking events for the company. While the coinvestment’s returns have been mildly positive thus far, much of the alpha will be generated on key developments. This will produce non-correlated and very inconsistent returns.

One of your author’s dear friends was recently looking back on his career and quite tellingly postulated that had his outperformance been half of what it was, yet been more consistent, he would have attracted significantly more assets under management. This observation was completely on point, as very few investors today are willing to wait for the second marshmallow, and routinely raid the cookie jar and shoot themselves in the foot. The only investment managers we know that deliver consistent monthly performance either use significant amounts of leverage, increasing the chance of losing it all, or are behind bars today. Yet, many continue to chase this elusive siren.

We are not. We are unapologetic about our concentration in our best ideas, where we have high conviction that our assessment of reality, which is very divergent from the market’s, will reward our risk-taking. As your author’s hero Sergio Marchionne would say, “mediocrity is not worth the effort.”

Annuit coeptis,

Steven Wood, CFA