Logos LP’s weekly commentary titled, “Market Cycles,” in which they discuss the relationship between price and value.

Bit behind on this July update but better late than never!

Stocks fell on Friday for the fourth straight day, capping off a volatile week for investors as rising trade fears and a tech sell-off led to broad weekly losses. The Nasdaq Composite fell 0.3 percent to 7,902.54, led by declines in Apple, Amazon and Alphabet. The tech-heavy index posted its fourth straight loss — its first since April — and is worst start to September since 2008.

The S&P 500 pulled back 0.2 percent to close at 2,871.68 as utilities and real estate both dropped more than 1 percent.

President Donald Trump, speaking from Air Force One, said Friday the U.S. is ready to slap tariffs on an additional $267 billion worth in Chinese goods. His remarks come after a deadline for comments regarding tariffs on another $200 billion in Chinese goods had passed last night.

Q2 hedge fund letters, conference, scoops etc

"The $200 billion we're talking about could take place very soon, depending on what happens with them," Trump said. "I hate to say this, but behind that, there's another $267 billion ready to go on short notice if I want." (targeting a sum of goods equal to virtually all imports from China)

The selloff pummeling emerging market currencies shifted to stocks as contagion concerns weighed on risk assets. MSCI Inc.’s EM equities gauge entered a bear market on Sept. 6 and had its worst week since mid-August.

The fear also comes after the Wall Street Journal reported, citing U.S. officials, that the possibility of the U.S. and China reaching a trade deal are fading as the Trump administration tries to revamp the North America Free Trade Agreement (NAFTA). Meanwhile, Bloomberg News reports that the U.S. and Canada will likely end the week with no trade deal in place.

Investors wrestled with a sharp decline in tech stocks this week, this year's best-performing sector. Tech fell nearly 3 percent as Wall Street fretted over potential regulation for companies in the sector, especially social media giants like Twitter and Facebook.

Wall Street was also under pressure after strong wage data stoked fears of tighter monetary policy in the U.S. Average hourly earnings rose 2.9 percent for the month on an annualized basis, marking the largest jump since 2009. The U.S. economy added 201,000 jobs in August, more than the expected increase of 191,000.

Treasury yields jumped to their highs of the session following the jobs report release, while the dollar also rose. The Fed has already raised rates twice this year and is largely expected to hike two more times before year-end.

Our Take

There is little doubt that the U.S. economy is in a boom. The Conference Board is reporting the highest levels of job satisfaction in more than a decade given a tight labor market — the ratio between the unemployment level and the number of job vacancies is at its lowest level in a half-century. A broader measure, the prime-age employment-to-population ratio, is back to 2006 levels. Meanwhile, real gross domestic product growth for the second quarter was just revised up to 4.2 percent. Corporate profits are rising strongly. And investment as a percentage of the economy is at about the level of the mid-2000s boom.

Wages are still lagging. But all other indicators show the U.S. economy performing as strongly as at any time since the mid-2000s — and possibly even since the late 1990s.

Why? A few reasons present themselves as outlined recently by Noah Smith:

- Demand Side Explanations:

- Low interest rates: lowered borrowing rates for corporations and mortgage borrowers, which tends to juice investment. Fiscal deficits provide an added boost to demand, and deficits have been rising as a result of President Donald Trump’s tax cuts. Typically pumping demand will eventually lead to rising inflation but this hasn’t happened yet.

- “Animal spirits” or “sentiment” as small business confidence is at record highs, and consumer/investor confidence also is very strong.

- Tail end of the long recovery from the Great Recession — consumers and businesses might finally be purchasing the houses and cars that they waited to buy when the recovery was still in doubt. Housing, traditionally the most important piece of business-cycle investment and consumption, is still looking weak, with housing starts below their 50-year average. But business investment might be experiencing the positive effects of stored-up demand.

- Supply Side Explanations:

- The Trump tax cuts removed distortions that held back business investment, and that fast growth — and the attendant low unemployment — is the result of the economy’s rapid shift to a higher level of efficiency.

- Technology: Information technology advances such as machine learning and cloud computing might be driving the investment boom — perhaps also spurring companies to invest in intangible assets such as brands and workers’ skills.

Which one is responsible? It is difficult to say but determining which are responsible matters as it can give insight into how the boom will end and how it can be prolonged. In our view all these factors have played a role, albeit certain ones have played a more crucial role during different stages in the bull market.

At the current stage of the bull market we see evidence that the demand-side “animal spirits” or “sentiment” factor is doing a lot of the heavy lifting.

It should be remembered that although of late there has been a minor repricing of high multiple/risk assets, the trend is still firmly in place: investors are not put off by unprofitable companies. In fact, the proportion of companies reporting losses before going public in the United States is at its highest since the dotcom boom in 2000.

Last year, 76 percent of the companies that listed were unprofitable in the year before their initial public offerings, according to data compiled by Jay Ritter, a professor at the University of Florida's Warrington College of Business.

That's lower than the 81 percent recorded in 2000, but still far higher than the four-decade average of 38 percent.

Investors are currently keen on “new business models” are are willing to overlook losses. In fact, many are questioning whether “value investing” and classic investing principles even makes sense anymore. The market's euphoria for so-called "growth companies" has even made billionaire hedge fund manager David Einhorn question if classic investing principles that worked for him still make sense today.

As Howard Marks reminds us, in investing as in life, there are very few sure things. Very few things move in a straight line. There’s prograss and then there’s deterioration. We must remain attentive to cycles.

The process/cycle is typically the same: 1) the economy moves into a period of prosperity 2) providers of capital thrive, increasing their capital base 3) because bad news is scarce, the risks entailed in lending and investing seem to have shrunk 4) risk aversion disappears 5) financial institutions and investors move to expand their businesses - that is, to provide more capital 6) they compete for market share by lowering demanded returns (e.g. cutting interest rates), lowering credit standards, lowering prudence, disregarding the linkage between price and value, paying less attention to profits or disregarding them all together and providing more capital for a given transaction.

At the extreme, providers of capital finance borrowers and businesses (investments) that aren’t worthy of being financed. This leads to capital destruction -that is, to investment of capital in projects where the cost of capital exceeds the return on capital, and eventually to cases where there is no return of capital.

Is this time any different?

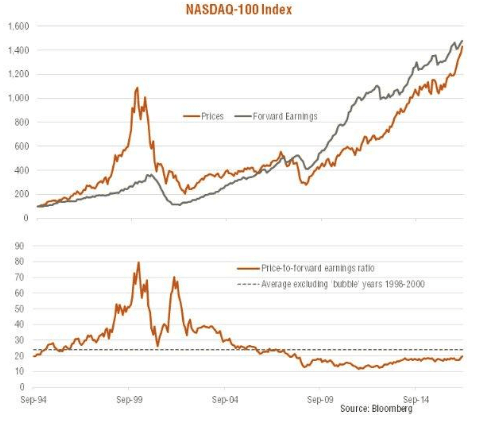

Chart(s) of the Month

Are overall tech valuations overstretched or only certain segments? Notice the absence of earnings in the dot com bubble years. Valuations do not appear stretched when put into perspective, prices appear to be in line with the underlying earnings picture. The NASDAQ-100’s price to forward earnings ratio is still a little below its longer run average of about 23x.

Musings

What of valuation? What of the relationship between price and value? For an investor (whether a “value” investor or not) price has to be the starting point regardless of where we are in the cycle and especially in the last innings. No asset is so good that it can’t become a bad investment if bought at too high a price.

As an example of the current “animal spirits” climate we should consider the following:

Cannabis : the thesis or “story” here is that cannabis, like alcohol, tobacco and other hedonistic instruments, has now achieved positive momentum with policymakers across the world. As such the fragmented industry will consolidate and a few early movers will reap the profits of this new multi-billion dollar industry. But just like investing in the nascent stages of many industries that in essence were revolutions from a status quo, speculation will initially replace prudent financial analysis of price relative to value.

As Easterly points out in a recent article Cronos' (CRON) current valuation is an outright manifestation of "extraordinary delusions" stemming from the madness of crowds.

Cronos trades at about 17.25 forward price to sales (TTM price to sales of 332.97 and TTM price to earnings of 874.69) compared to its peers. For some further clarity, highly valued SaaS stocks prized for their recurrent revenue stream and high gross margins seldom trade at 17.25 forward P/S ratio. The average P/S ratio for stocks in the software application industry is around 6.8, compared to 2.16 for the S&P 500.

Hence, why does an agricultural commodity producer trade at a higher valuation than Shopify and other?

In Deloitte's "A society in transition, an industry ready to bloom" 2018 cannabis report, they expect legal cannabis sales during 2019, the first full year post-legalization to be [CAD]$4.34 billion. This figure is likely inflated when compared against the results of other markets. Further, the study only surveyed a sample size of 1,500 adult Canadians, which is not significant enough to estimate the Cannabis purchase habit of millions of Canadians.

For some perspective, California, which is regarded as the most important Cannabis market on Earth realized sales of [USD]$339 million or [CAD]$444 million (at current spot USD/CAD) during the first two months post-legalization. Extrapolating this across a full year would infer total sales of [USD]$2.01 billion or [CAD]$2.7 billion. Sure there are other factors to consider like a larger Californian black market and a different set of regulations and taxes. However, the Californian market has also not been as stringent on marketing as Canada will be.

Assuming the Canadian market is at least on par with California, the author models the potential market using an optimistic CAGR of 23.54% from 2019 - 2023 which is more optimistic than some market reports. The author also models Cronos' revenue for the years from 2018 - 2022.

Cronos' current market valuation of [USD]$1.75 billion or [CAD]$2.29 billion is around 84.81% of the total Canadian legal cannabis market in FY2019. (And this does not take into account the fact that the total estimated legal cannabis sales [CAD] $4.34 billion number mentioned above represents a total retail sales projection and that will likely be shared between grower, distributor, retailer, and the government through taxes. Taxes will be large, perhaps even 30%. Retail will be handled by government in a few big provinces like BC -- yet the government will still take a retail margin cut. What will be left for growers could be as low as sub $4 CAD / gram.. half or less of that total [CAD] $4.34 billion number…

At a current market valuation of [CAD]$2.29 billion ($2.79 billion at time of writing) which is around 84.81% of the total estimated Canadian legal cannabis market in FY2019, has the fairness of Cronos’ price been considered? Or have people without disciplined consideration of valuation simply decided that they want to own something because the story is good, risk aversion is low and the future looks bright?

Overall, we see current valuation trends in certain growth stocks (cannabis, select tech.) (not to mention that the ratio of bearish option bets to bullish ones is waning as the S&P 500 keeps churning out records. That implies investors may be loading up on derivatives as way to make up for lost ground should 2018 deliver a year-end rally similar to last year’s, when stocks closed with a 6.1 percent fourth-quarter surge) to be evidence that the demand-side “animal spirits”/“sentiment” factor is doing a large portion of the heavy lifting to prolong the current bull market.

As such, we would advise caution before increasing exposure to these “loved” and therefore richly valued businesses. Investing is a popularity contest, and the most dangerous thing is to buy something at the peak of its popularity. For our portfolio, given where we are in the present cycle and overall market conditions we are abiding by the following maxim: “The safest and most potentially profitable thing is to buy something when no one likes it. Given time, its popularity, and thus its price can only go one way: up.” -Howard Marks

Logos LP July 2018 Performance

July 2018 Return: -0.34%

2018 YTD (July) Return: 0.00%

Trailing Twelve Month Return: +12.79%

CAGR since inception March 26, 2014: +18.29%

Thought of the Month

"The polar opposite of conscientious value investing is mindlessly chasing bubbles, in which the relationship between price and value is totally ignored. All bubbles start with some nugget of truth: 1) Tulips are beautiful and rare 2) The internet is going to change the world 3) Real estate can keep up with inflation, and you can always live in a house.” -Howard Marks

Articles and Ideas of Interest

- After Coltrane, there is nothing left to say. The saxophone virtuoso pushed jazz as far as it could go, and it’s been downhill ever since.

- These Fake Islands Could Spell Real Economic Trouble. Glitzy property projects and financial crises tend to go hand-in-hand.

- U.S. Household wealth is experiencing an unsustainable bubble. Jesse Colombo suggests that Since the dark days of the Great Recession in 2009, America has experienced one of the most powerful household wealth booms in its history. Household wealth has ballooned by approximately $46 trillion or 83% to an all-time high of $100.8 trillion. While most people welcome and applaud a wealth boom like this, research suggests that it is actually another dangerous bubble that is similar to the U.S. housing bubble of the mid-2000s. In this piece, he explains why America's wealth boom is artificial and heading for a devastating bust.

- Who needs democracy when you have data? Here’s how China rules using data, AI and internet surveillance.

- How tourists are destroying the places they love. Travel is no longer a luxury good. Airlines like Ryanair and EasyJet have contributed to a form of mass tourism that has made local residents feel like foreigners in cities like Barcelona and Rome. The infrastructure is buckling under the pressure. Great 2 part expose suggesting that travel has almost become a human right yet it has become predatory - devouring all the beautiful places which drive it. Has nature itself come to be viewed as merely one more good to be consumed? ; Have we developed a shallow, modern need to present a life free from the tyranny of a nine-to-five office job in the tight frame of Instagram? No wonder you are not original or creative on instagram. Everyone on Instagram is living the same life.

- Peak Valley. The Bay Area’s primacy as a technology hub is on the wane. Don’t celebrate. Although capital is becoming more widely available to bright sparks everywhere yet unfortunately the Valley’s peak looks more like a warning that innovation everywhere is becoming harder.

- Americans live in the ruins of the 2008 financial crisis. Prosperity is undercut by broken institutions, from health care to law enforcement. NYT presents some astonishing facts. Is the American dream dead?

Missed a Post? Here's the Last 5:

The Art of the Deal

Mistakes Happen

Do Bull Die of Old Age

Less Is More

Everything Has Been Done