We are shifting from an era of geopolitics based on conventional military might to geo-economics – where national interests are fought with markets, currencies and commerce, rather than with missiles, submarines and drones, according to a new report by Bank of America, U.S. Trust.

Q2 hedge fund letters, conference, scoops etc

Combat through economic means has the potential to be very destructive. Yet, the upside is just as significant, says Joe Quinlan, Head of Market Strategy, and could ultimately help level the playing field for U.S. companies.

In addition to solid U.S. economic growth, strong earnings and corporate tax reform, the markets sense that in the new unfolding era of geo-economics, the U.S. will emerge a clear winner.

Investing in the Era of Geo-economics

‘Geo-economics—the systematic use of economic instruments to accomplish geopolitical objectives’i

The global economic order is being upended. We are shifting from an era of geopolitics based on conventional military might to geo-economics—whereby foreign security goals and national interests are fought with markets, currencies and commerce, rather than with missiles, submarines and drones.

This is not to say that conventional military hardware is unessential to the practice of statecraft. Hardly. Military might still matters in a multipolar world fraught with fault lines in the Middle East, the Indian subcontinent, Africa and Asia. The world’s a messy place, and that is one key factor behind our high-conviction sector call on defense and cybersecurity.

That said, however, rarely has Washington so openly and blatantly used its economic might and resources in pursuit of national and global interests. The use of U.S. import tariffs on a variety of products—solar panels, dishwashers, aluminum, steel, potentially automobiles and much more—is war by other means. The long-time refrain among policymakers—that the United States “too often reaches for the gun instead of the purse in its international conduct”—has been turned on its head by a White House bent on harnessing America’s economic might to its strategic interest and advantage.

The levers of geo-economics

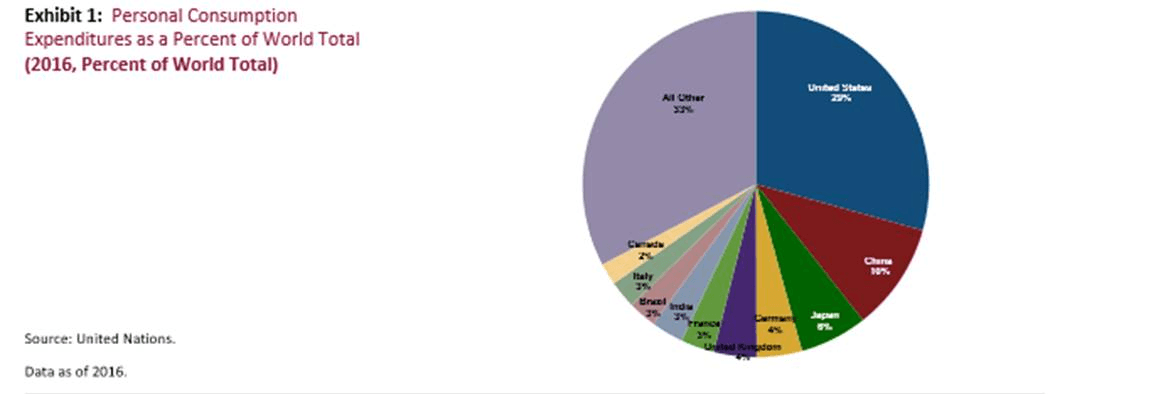

It’s America’s large and wealthy consumer market, along with the U.S. dollar’s global reign, that gives the United States so much economic throw-weight relative to the rest of the world. Per the former, no market in the world—including China—offers foreign countries and companies as much commercial opportunity as the United States, home to only 4.5% of the world’s population yet 29% of total global personal consumption (Exhibit 1). While America’s share of global consumption has trended lower over the past few decades, falling from 34% in 2000 to 29% last year, the U.S. consumer remains one of the most potent economic forces on earth.

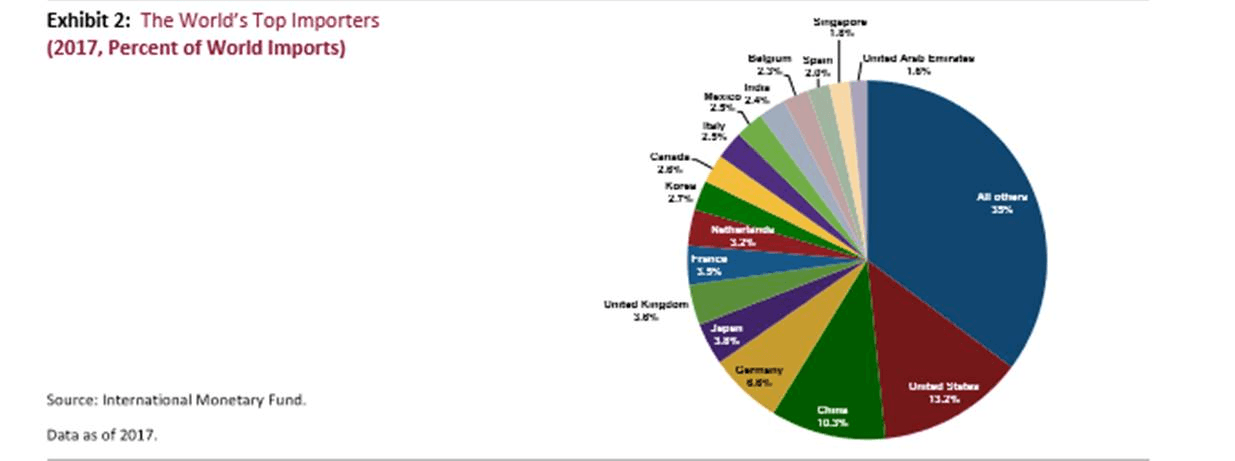

Similarly, for decades, no market in the world has been as open to foreign competition as the United States, home to some of the lowest general tariffs on trade on the planet. The latter was purposeful or by design since liberal cross-border trade and investment regulations have long suited America’s consumption-led economy. The lower the tariffs on imports, the lower the cost of foreign goods and services to U.S. consumers and the more choices of goods from which to choose. In addition, giving nations like Germany, Japan, South Korea and others liberal access to the U.S. market helped underpin economic growth in a number of U.S. allies over the post-war era, promoting the global strategic interests of the United States. As depicted in Exhibit 2, the U.S. remains the world’s largest importer, reflecting, in part, the ease of access to U.S. consumers.

Today, however, access to the U.S. market isn’t a given; in addition, the cost of doing business is set to rise for a number of countries/companies if the U.S. continues down the path of protectionism.

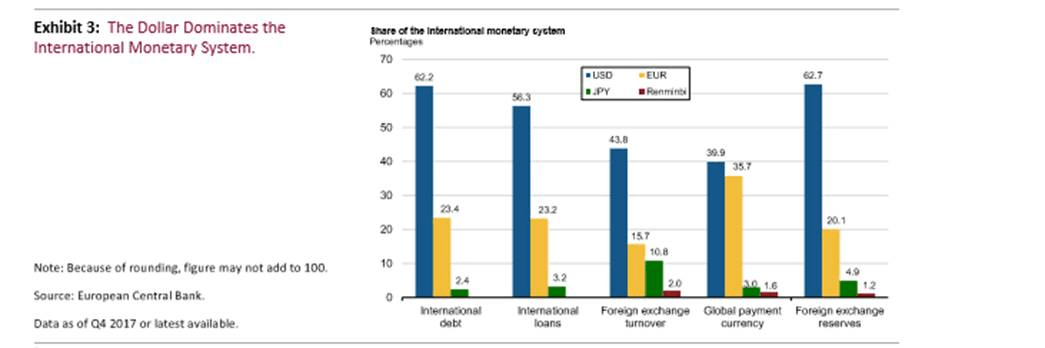

Beyond America’s sizable and wealthy consumer market, the nation’s pre-eminent geo-economic lever is the U.S. dollar and the fact that the global financial architect pivots on the greenback. While the world can do without many currencies, it cannot survive, at least for now, without the greenback. The U.S. dollar is the primary grease of global commerce, lubricating virtually every foreign transaction, every day of the year. As The Economist recently noted:

“On average, countries’ dollar imports are worth five times what they buy from America. More than half of all global cross-border debt is dollar-denominated. Dollars make up nearly two thirds of central bank reserves. That gives the Treasury a veto over much of global commerce.”ii Now, consider the following—that developing nations’ collectively owe $2 trillion in dollar-denominated debt, that roughly 88% of global foreign exchange turnover involves the dollar, and that the dollar’s share of crossborder borrowing now stands at 62% (2017) versus 45% in 2008—and the global potency of the U.S. dollar becomes even clearer (Exhibit 3).

Through the U.S. Federal Reserve, the Department of Treasury and Wall Street, America controls the financial plumbing of the global economy. The global payments system runs on dollars and is routed through the canyons of Wall Street, giving Washington tremendous leverage to deny virtually any foreign country or company access to U.S. dollars. And being without dollars is like being without oxygen—you cannot function or survive for long.

Case in point: After the U.S. Treasury slapped sanctions against Russia in April 2018, Rusal, an aluminum producer, was frozen out of financial markets, causing its publicly traded shares to decline by more than half. U.S. sanctions against Chinese smartphone maker ZTE—albeit recently repealed—had a similar devastating financial impact on the company.

Meanwhile, the principal pain point for Iran in confronting U.S. economic sanctions is the U.S. dollar, or the lack of dollar-based financing as Washington attempts to ban Iranian access to SWIFT—the secure messaging system that supports cross-border flows of global capital. In addition, as a clear example of geo-economics, Washington has put the world on notice that any firms doing business with Iran will be denied access to U.S. dollars and the U.S. market, triggering many European firms to close shop in Iran out of fear of losing access to U.S. capital and markets.

Going where others have gone before

To borrow from Billy Joel, America “didn’t start the fire.” In the new and unfolding era of geo-economics, the United States is playing catch-up to more seasoned practitioners like Russia, China and many other states. With its massive domestic market as leverage, China has denied or curtailed goods and services from Japan, South Korea, the Philippines and Taiwan, to name a few nations that have pursued policies contrary to the interests of China.

Leveraging its massive surplus savings, Beijing now provides more loans to Latin American than either the World Bank or the International Monetary Fund, both traditional western-backed institutions. The Chinese-led Asian Infrastructure Bank now rivals any western financial institution and, along with China’s “One Belt, One Road” initiative, is one of the starkest examples of geo-economics in action. Ditto for China’s globally competitive state-owned enterprises, also instruments of geo-economics.

As for Russia, the energy power is not shy about shutting off energy supplies in the winter to either Ukraine or other parts of Europe when annoyed or threatened by external forces. After Poland protested against Russia’s intervention in Crimea, Moscow suspended cheese imports in retaliation. In the Middle East, meanwhile, economic and financial instruments (petro dollars) have long been deployed as instruments of statecraft by Saudi Arabia, the United Arab Emirates and others. Massive sovereign wealth funds—with the ability to invest (or not) billions of dollars in any particular market or economy—serve the same purposes.

Game on: Key risks to the United States

With the largest and wealthiest consumer market in the world, and with the U.S. dollar the linchpin of global finance, among other attributes, the United States wields tremendous geo-economic power. This power, however, needs to be used judiciously. While there is no real substitute for the dollar at the moment, leaving the world dependent on the greenback and dollar payment systems, the dollar’s global reign is not preordained. The more the dollar is used as an instrument of statecraft to the detriment of other nations, the greater the momentum to find an alternative currency (bitcoin, for instance) and the greater the incentive to move toward a multipolar currency, hastening the dollar’s decline. To wit, China and many of its trading partners are already trading in local currency, a trend that could accelerate with the unpredictable tone and policies of Washington.

That said, it’s worth recalling that the dollar’s global dominance bestows a number of unique advantages on the U.S. ‘King Dollar’ allows the U.S. to borrow cheaply, run chronic trade deficits, issue debt in its own currency and generally live beyond its means—which the nation has been doing for decades. However, all of these advantages would wane if the buck became a weapon of Washington, galvanizing the world to create an alternative. Another key risk: U.S. firms in the coming months are denied market access in China, Europe and other foreign markets in response to U.S. protectionist measures. Or just as damaging, they become targets of government/consumer boycotts, depressing foreign earnings—although these signs have yet to emerge.

Investment summary

The rise of geo-economics—or the use of economic instruments to promote and defend national objectives— has caught investors by surprise. In particular, the markets have underestimated the Trump administration’s willingness to use trade and finance as means of statecraft and diplomacy. While there’s nothing new about the United States slapping tariffs and sanctions on rogue regimes, the blunt application of various economic weapons against America’s main trading partners and allies has unnerved investors, and for good reason.

Combat through economic means has the potential to be very destructive. There are plenty of risks. Hence, the whipsawed nature of the capital markets this year.

Yet, seeing the glass half full, the upside is just as significant. The unfolding era of geo-economics could significantly reconfigure the global playing field, resulting in a more liberal and open market in China (already underway), the updating of various trade agreements (think NAFTA), and new bilateral deals that spur sector growth (think soaring U.S. energy exports). These, among other things, will ultimately help level the playing field for U.S. companies.

There is a reason the S&P 500—notwithstanding all the daily headline risks—is up nearly 5% for the year, trading just 2.5% off its all-time high, and outperforming the rest of the world. In addition to solid U.S. economic growth, strong earnings and corporate tax reform, the markets sense that in the new unfolding era of geo-economics, the U.S. will emerge a clear winner. Stay tuned.

i From the book, War by Other Means: Geoeconomics and Statecraft, by Robert Blackwill and Jennifer Harris, 2016.

ii See “About that Big Stick,” The Economist, May 19, 2018.

Article by Joe Quinlan, Head of Market Strategy, at Bank of America, U.S. Trust.

{kind=link}