The turbulence throughout the markets last week – thanks to Italy – has given investors their first taste of a frothy summer.

Especially the ‘smart money’– they’re bolting for the exits. . .

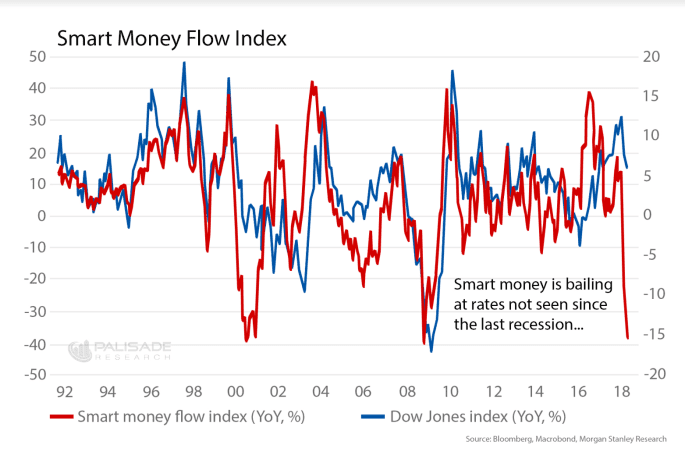

The Smart Money Flow Index (SMFI) is a leading-indicator in markets. That means when the SMFI drops sharply, usually the equity markets are right behind it.

And we haven’t seen the SMFI drop this much since the Great Recession of 2008 and the 2001 Recession. . .

What’s going on?

Last week I wrote about the forgotten economist – Hyman Minsky – and his excellent work about the Financial Instability Hypothesis (FHI), which details how an economy shifts through three stages.

From lowest risk to highest risk the stages are: hedged, speculative, and ponzi.

But probably the most important takeaway from the FIH is this simple sentence. . .

The periods of low volatility and market calm are the seeds for high volatility and market chaos in the future; then back the other way around.

Let me show you this using the last 10 years of the CBOE Volatility Index – the VIX – which gauges market volatility.

Like Minsky stated, the periods of market calm are breeding grounds for high market volatility.

Out of the last 10 years, roughly 85-90% of the time was peace and quiet. But the 10-15% were wild spurts of sharp chaos and turbulence.

What we can make out of this is “don’t confuse the current calm markets as signals everything is going to be OK.”

Unfortunately, that’s what the crowd is doing. . .

Things have gotten so peaceful that according to Goldman Sachs, Wall Street isn’t too far from record ‘quiet’ levels.

Looking at the single-stock ‘implied volatility’ throughout the S&P 500, it’s down 21% on a 3-month basis.

What’s implied volatility – informally known as iVol? This is the mathematical and artificial way to try and estimate how volatile something is – and will be – on the stock market. It’s most commonly used in option trading via the Black-Scholes Option Pricing Model.

Putting it simply, iVol is the estimated volatility of a security’s price and how traders price in the future price fluctuations.

For example, If the crowd’s bearish and expecting turbulent times, then the iVol will be higher – thus requiring more risk premium. But if they are instead optimistic and expecting calm markets, the iVol will be lower – settling for less risk premium.

So, with implied volatility down 21%, the equity markets are expecting calmer markets ahead. . .

This sort of ‘market complacency’ is where having optionality is key.

Borrowing ideas from the philosopher-esque former trader – Nassim Taleb – one needs to set themselves up with only ‘positive optionality’.

Positive Optionality is a situation where you have an asymmetric risk-reward setup; meaning unlimited upside with limited and fixed downside.

For example, buying car insurance offers this type of positive optionality. You pay small fixed premiums every month for complete protection during an unlikely chance of an accident.

Worst case scenario? You lose the small monthly premiums – no more, no less.

The upside scenario? There’s a freak-vehicle accident and your insurance company covers all your significant medical bills and replaces your totaled car with a brand new one – mountains more than what your small premiums cost you.

Negative optionality is the one writing the insurance – the one responsible for the huge payouts.

Remember that scene in The Big Short movie when Christian Bale’s character Mike Burry went to Goldman Sach’s and bought customized mortgage default insurance from the bank – and they laughed at him?

Unlike the bank that only wanted fixed monthly premiums and couldn’t see the bigger picture of risk – Mike actually understood positive optionality.

Later – during the crash of 2008 – Goldman Sach’s was on the hook to pay Mike a huge sum when the housing market bellied-up. Netting him a massive profit.

So, what’s this all add up to?

With the ‘Smart Money’ leaving in droves, and markets becoming too complacent – this gives us a subtle opportunity – and warning.

Take advantage of the low-implied volatility the market is pricing in while ignoring the smart money rotating out of equities. The Smart Money knows that all this ‘peace’ will be followed by spurts of high turbulence – eventually.

During this period of mis-priced risk, complacent markets, and false confidence – be long anything with positive optionality.

Now, go re-watch The Big Short. . .

By Palisade Research