I recently wrote an article for Sure Dividend entitled “Consider Equity REITs for Your Next Investment“. In that article, I listed nine equity REITs (eREITs) for dividend investors to consider in light of the drubbing that eREIT valuations have recently taken due to fear of rising interest rates and to capitalize on the pass-through provision for REIT income included in the new tax legislation.

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

Both of these topics are covered in some detail in the previous article. This article provides a more complete investment thesis for Welltower, Inc. (HCN) one of the nine eREITs highlighted in the previous article.

Welltower, Inc.

Welltower is one of the larger healthcare eREITs in the US with an enterprise value of roughly $33B and more than 1330 healthcare properties/assets consisting primarily of Senior Housing Developments located in the US, the United Kingdom, and Canada as well as Post Acute Care Facilities located in the US. HCN has very little exposure to Medicaid and/or Medicare payment structures with roughly 93% of its revenues generated through operators relying on private pay or private insurance reimbursement for senior housing and healthcare services.

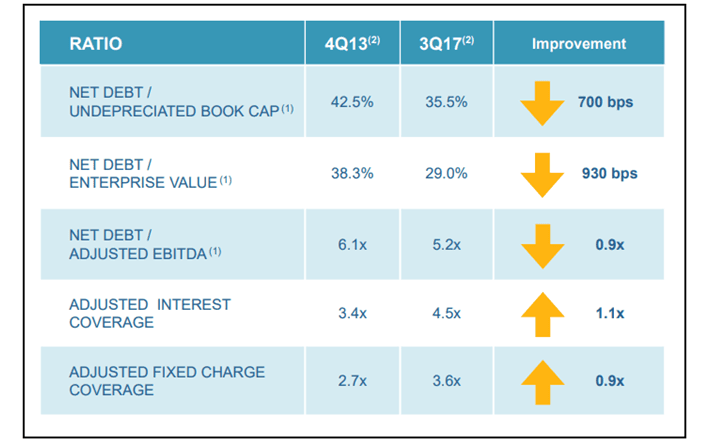

Welltower maintains a strong balance sheet with conservative use of debt and carries a BBB+ credit rating. The chart below shows four critical metrics for HCN’s balance sheet.

Source: Welltower Investor Site

The bottom three metrics are particularly important as they show that HCN’s net debt including preferred stock issues is manageable with respect to EBITDA and the interest on debt and preferred dividend payments (fixed charges) is well covered by EBITDA. These are the metrics that are important to maintaining an investment grade credit rating and allows HCN to issue more debt for growth acquisitions at favorable (i.e. low) rates.

Welltower’s continuing growth strategy is focused on projected demand growth in senior housing and post acute medical care (short and long term). Senior housing (independent and assisted living) demand is projected to grow at roughly 8% per year over the next 20 years.

Source: Welltower Investor Site

Many seniors will need to move from independent living to assisted living to skilled nursing or memory care as they age. Welltower’s investment strategy encompasses the demand for that level of continuous managed care. Welltower’s existing developments and future investments are focused on high per capita income areas of the US, the UK, and Canada.

Outpatient and post acute care demand is also expected to grow significantly over the next 30 years as the baby boom generation ages. The chart below shows the projected growth in outpatient services in just the next 9 years.

Source: Welltower Investor Site

As we boomers age, the demand for medical services and outpatient procedures will grow significantly and HCN’s growth strategy includes the post acute care facilities that will be needed to support the expected transition from inpatient to outpatient procedures. This transition from inpatient to outpatient procedures followed by post acute care has shown to be significantly more cost effective than the traditional inpatient hospital stays and it is the direction that both private insurers and the government (Medicare and Medicaid) is moving.

Welltower’s Recent Financial Performance

Had you made a $10,000 investment in HCN ten years ago and reinvested all dividends, today you would have roughly $23,500. The chart below shows that growth in value compared to the growth of all US REITs.

Source: Morningstar

Welltower’s early performance was interrupted by the 2008/2009 recession where the value dropped to roughly $7,500 after the first year. The nine year performance of an initial $10,000 investment in February 2009 would have the investor holding a bit more than $33,500 today.

Welltower, like all REITs, shares its financial performance with investors primarily through its dividend distributions. REITs must distribute 90% of their of their taxable income to shareholders to maintain their REIT status. Today, HCN’s annual dividend is $3.48 per share for a yield of 6.27% as of February 9, 2018. Readers should note that the recently passed tax reform legislation contained a new pass-through provision exempting 20% of income of REITs and partnerships from Federal income tax. That means that investors will only pay tax on $2.78 (80% of $3.48) of HCN’s dividend distribution.

The dividend is well covered by HCN’s cash flow. Funds from operations (FFO) for 2017 is expect to be $4.22 (range midpoint) providing a dividend to FFO payout ratio of 0.82. Anything less than 90% payout for a REIT is considered acceptable.

HCN Investment Thesis

With the general market currently experiencing a mini-correction and eREIT valuations suffering further from fear of rising interest rates, why would I be considering an investment in HCN at this time? Today, HCN is on sale having fallen nearly 19% while at the same reporting stellar 3Q17 financials. While the market has pushed eREIT valuations down over the last quarter, and particularly the past two weeks, due to fears of rising rates, history tells us that eREITs generally do well during periods of slowly rising rates and some eREITs will even beat the big market indexes under these conditions. For a more complete discussion of the impact of rising rates on REIT financial performance as well as a more detail on the new pass-through provision, readers should see my earlier article “Consider Equity REITs for Your Next Investment“.

The other significant driver for healthcare eREITs in general and HCN in particular is the shift in our age demographics here in the US. Today, we have roughly 8M citizens over the age of 85. Due to the benefit of medical advances and increases in longevity, by 2050 we will have more than 20M citizens over the age of 85. That is a 2.5 fold increase over 30 years. Another metric to consider is that we have currently 10,000 baby boomers retiring every day. Readers can find a more detailed discussion of our aging demographics here. The chart below shows the estimated growth of various segments of our aging population between 2000 and 2050.

This will be very significant for companies providing services and housing specifically to accommodate the needs of our senior citizens. Welltower will have a long term growing client base for the services of their senior housing and post acute care facilities.

Final Thoughts

Welltower is a large well established and well run healthcare eREIT with a solid balance sheet and a long history of growth through economic contractions as well as expansions. Recent investor jitters over rising interest rates has pushed HCN’s stock price into bargain territory and its dividend yield up to just under 6.27%.

The partnership and REIT pass-through provision in the recently passed tax legislation will shield 20% of HCN’s dividend from Federal income taxes. Our aging demographics essentially ensures a growing client base for HCNs buildings and facilities over the next 30 years. Welltower should provide many years of healthy dividends and capital appreciation to today’s investors.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.