Vilas Fund, LP letter to partners for the first quarter ended March 31, 2018.

Dear Vilas Fund Partner,

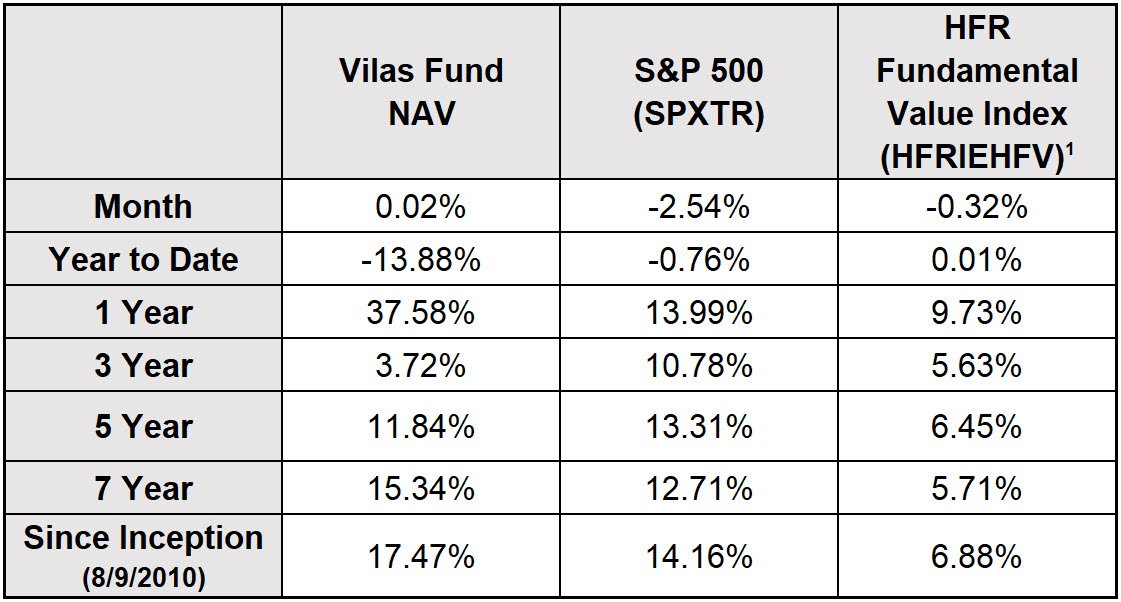

The performance of the Vilas Fund, LP, the S&P 500 and applicable HFR Index, as of March 31, 2018, follows:

Performance Discussion

Value shares continued to underperform growth shares in the first quarter of 2018, witnessed by the S&P 500 Value Index declining 4.3% while the S&P 500 Growth Index rose 1.5%. We believe that this dichotomy is one of the larger quarterly differentials since the late 1990’s. Due to this difference, the Fund lagged the market in the first quarter of 2018. We continue to believe that this will eventually reverse, and with a vengeance, but, again, we are unsure of the timing.

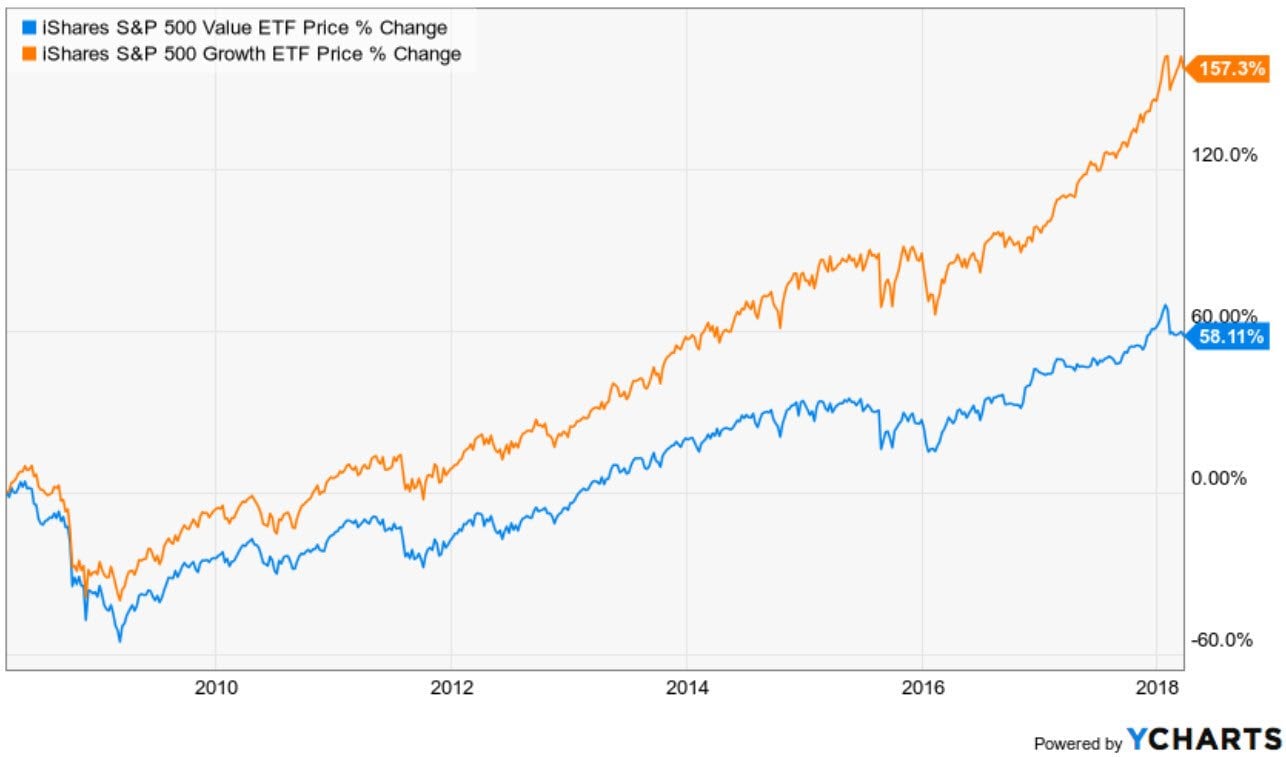

The following graph shows the hill we have been climbing better than any words:

As you can see, the Growth Index has outperformed the Value index by nearly 100% over the last 10 years (Orange is Growth, Blue is Value). As a value manager, this feels like a marathon race that simply won’t end. While we do not know when it will reverse, we do know that it will, eventually, as reams of academic data show that value shares have outperformed growth shares over the long run and the fact that corporate capital returns (dividends plus share repurchases) have accounted for the majority of equity returns. Value shares have far higher dividends and share repurchases than growth shares, which partially explains their long-term outperformance.

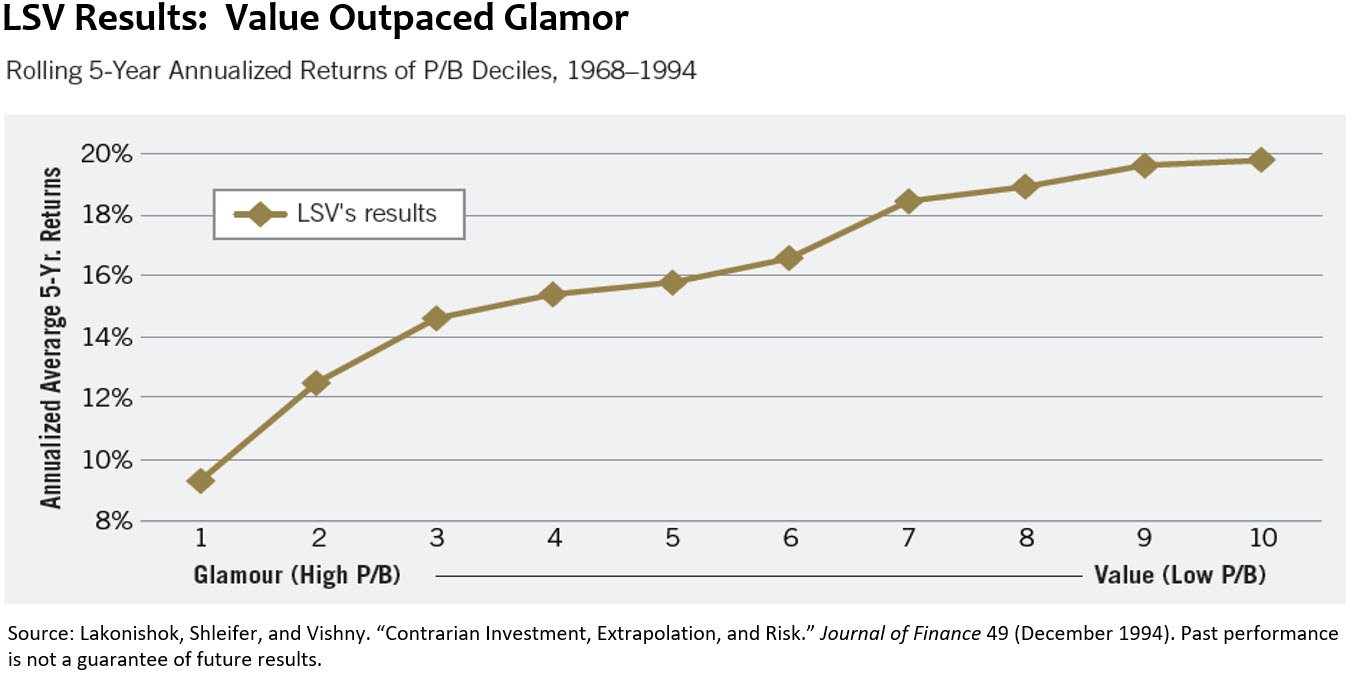

The following chart of the data from the paper “Contrarian Investment, Extrapolation and Risk”, Lakonishok, Shleifer and Vishny, 1994 shows the extent of the expected value premium and, therefore, why we are so optimistic:

This data shows that the cheapest stocks outperform the most expensive stocks by a significant margin, approaching 10% annually. The Brandes Institute updated this data through 2014, globally, and similar results were shown: the cheapest value stocks outperform the most expensive growth stocks by material amounts over long periods of time, regardless of market capitalization or geographical location.

Long Term Compounding

Despite value shares lagging badly, the Fund has compounded investor capital more rapidly than the S&P 500 and the competition since the Fund began operations on August 9, 2010. A $1 million investment into the Fund at inception increased to $3.4 million vs. $2.8 million in the S&P 500 Index and $1.7 million in the HFR Fundamental Value Index.

What makes the Vilas Fund unique, at least as of late, is that we prefer a somewhat lumpy 17% over a smoother 7%, as our competition has delivered, over long periods of time. Over the next 25 years, or roughly the amount of time remaining in my career, if we were fortunate enough to maintain our “since inception” performance rate of 17.5%, the Fund would compound $1 million today into $56 million. If the average fund in the HFR Fundamental Value index continued to compound at 6.9% per year for the next 25 years, it would compound $1 million into $5.3 million.

Clearly, continuing our “since inception” performance of 17.5% for twenty-five years is a very tall order and is highly unlikely. However, our point is that compounding at more rapid rates leads to massive differences in wealth creation over very long-time frames.

Investors with long horizons, such as those managing trusts, endowments, retirement accounts, insurance contracts or pensions, may find this thought process interesting.

Tax Efficiency

The Fund has been very tax efficient over time. Through 2016, the Fund has paid out a net negative amount of capital gains since its inception. This means that the returns we have generated have not been partially taxed away. We will continue to manage the Fund in an attempt to maximize after tax returns, though we will realize capital gains from time to time.

BarclayHedge Ranking

The Fund was recently ranked by BarclayHedge, a database service. The Vilas Fund, LP was in the top 30 Funds (#28) out of all 2464 funds in their database for the period of September 1, 2010 (first day of the month following our inception) to December 31, 20172. Importantly, there were roughly 4800 Funds in the BarclayHedge database at the time of our inception so roughly half of the competition has shut their doors, usually due to poor performance. Our goal is to continue to outperform most of the competition and the markets over long periods of time, as occurred with both the equity and fixed income funds that I managed previously.

Holdings

We have made a number of changes to the portfolio over the last few months. First, our healthcare exposure has risen significantly due to a large purchase of Walgreens Boots Alliance, currently our largest position, and additional purchases of CVS. The Fund also owns a smattering of other healthcare stocks, including Medtronic, Zimmer, Express Scripts, Valeant and Mallinckrodt. On average, these holdings are growing at attractive rates and are trading at low prices in relation to earnings, especially in comparison to historical averages.

We believe that the movement of pharmaceuticals from manufacturers to consumers will continue to be handled by retail pharmacies and Pharmacy Benefit Managers. The threat of new, online competition has depressed the pharmacy sector to a price to earnings level that is at or somewhat below the levels hit in the financial crisis. While it is relatively easy to distribute some products online and undercut other types of goods, such as clothing, electronics or household items, due to the need for immediate access to prescriptions when ill or out of supply (they offer 24/7 service for a reason), regulatory issues with safety, pharmacist supervision to check for possible drug interactions, and chain of control issues, we believe pharmaceuticals will be a very, very difficult nut to crack. If some investors would assume that the public will get immediately needed items from Walgreens or CVS and some from Amazon, this ignores the fact that it is important, if not vital, to have all of your prescriptions filled at the same institution. Why? The pharmacy is a second set of eyes to help prevent drug interactions that can cause major issues, if not fatalities. Thus, the average consumer would be ill advised to mix and match service providers to potentially save a small amount of money given the massive potential downside of drug interactions for themselves or their loved ones. Further, due to co-pay arrangements that are largely fixed, it will likely be hard to create a financial incentive to get consumers to move online in mass.

Walgreens is a compelling buy. The company is trading at roughly 10 times next twelve-month net income estimates, grew its earnings per share by 27% last quarter, continues to gain market share both organically and through store acquisitions, and should continue to grow markedly faster than nominal GDP with rising prescription volume derived from new therapies and the aging population worldwide. Because the company has compounded its earnings per share at roughly double the pace of the S&P 500 for a very long time, the shares have averaged roughly 22 times trailing earnings over the last 30 years, ignoring the late 1990’s bubble period. Below please see the chart of Walgreens next 12 months P/E ratio, which is currently near the financial crisis lows:

If we assume that Walgreens continues to grow its earnings to $8 per share in three years, in line with current analyst estimates, and sells at 16 times those earnings per share, far below its long-term average, the stock would reach $128, a double from today’s price of $64. However, with this better than average growth, the multiple could rise back to its long-term average of 22 times earnings. This would equate to $176 per share, up 175% from here. Because of this, we think that Walgreens will be the largest creator of profits in the Fund over the next few years.

Second, we sold many of our positions in US investment banks prior to their corrections, including Morgan Stanley, Goldman Sachs, JP Morgan and Bank of America. The Fund made very large profits in these positions, some tranches of which were over 4-fold. While these are wonderful companies and we are grateful for their recent very strong performance, we believe that the prices we obtained upon sale were rich in comparison to their underlying opportunities, especially given the fact that the economy appears to be in the latter stages of this expansion. We retained, and recently added, to our position in Citigroup as we believe that the company remains at an unjustified large discount to the industry and its outlook. For the first time in 40 years or so, Citi is being managed by a banker, and a good one at that. We believe that Michael Corbat is doing a great job and will cause the valuation disparity between Citi and the rest of the industry to narrow and, quite possibly, disappear.

We have largely maintained our positions in European banks and Barclays continues to be our second largest position. Barclays is currently underperforming and is relying on its investment bank to improve its operations and return on shareholders’ equity. We find it difficult to imagine Barclays being overly successful with this endeavor. For this reason, it has attracted a formidable activist investor named Sherborne, managed by Edward Bramson. This firm has an enviable track record and only focuses on one target company at a time. We believe that Mr. Bramson sees the core retail bank and credit card operation as very attractive and is pushing to reduce the capital and risk in the investment bank, thereby increasing the return on equity and the valuation of the stock in relation to that equity. We welcome Mr. Bramson’s input. Other European financial investments include Royal Bank of Scotland, Deutsche Bank, and Credit Suisse.

Third, we have added to the Fund’s insurance exposure. We have increased our positions in AIG, Brighthouse Financial (the life insurance spin-off of MetLife), and added to the US mortgage insurance sector following their recent, and quite violent, selloff. We believe that insurers, in general, will benefit greatly from higher interest rates and, in the MI space, continued growth in housing. There appears to be a shortage of homes in the US, which should lead to more construction (and F-150’s) and needs for financing.

We have maintained our investments in the global auto sector. These include Honda, Daimler (Mercedes), Ford and GM, in declining order of size. These companies are quite profitable, have experienced decent unit volume growth in recent years and, on average, are trading at roughly 7 times net income and near their book values. The market appears to have discounted the next recession in the share prices of the global auto industry, making them attractive holdings over the next few years. We believe that, while extremely cyclical, these companies should be trading at levels 50% higher than where they are today.

And finally, we have pared our short positions, after the recent selloffs, to basically only include Tesla, which comprises roughly 98% of our short book. We added meaningfully to our Tesla position in the first quarter at prices in the $340 range. We continue to believe that Tesla is extremely overvalued and that it will experience significant financial difficulties over time.

All companies in a capitalistic system need to earn profits and those profits need to be attractive relative to the amount of shareholder capital employed. Tesla has never earned an annual profit. Along with digital currencies and Unicorns, Tesla appears to be caught up in a gold-rush-fever type of emotional response, both from a “they will take over the world” and a “they will save the world” combination of hopes, instead of their owners looking at the numbers.

Tesla bulls will argue that their production will rise to 5000 Model 3’s per week soon and, therefore, the stock will trade meaningfully higher. Given that the company lost $20,000 per Model S and X sold for roughly $100,000 each last year, due to the fact that it cost more to build, sell, service, charge and maintain these cars than they collected in revenue, as it is important to include all costs when evaluating a business, we predict it will impossible for Tesla to make a profit on a $35,000 to $50,000 car. As anyone with automotive experience knows, profit margins are far higher on bigger, more expensive cars. Therefore, the faster Tesla makes Model 3’s, the more money they will lose.

Roughly five institutions make up nearly 50% of Tesla’s freely floating shares. All it will take is for one of them to realize the likely fact that the company won’t ever earn an annual profit, has been overly optimistic, at best, or quite dishonest, at worst, with their projections of cash flow and profit and Tesla’s shares should fall precipitously. We believe that the CEO’s recent tweet that the company will be profitable and will generate positive cash flow in the second half of the year are likely attempts to artificially inflate the stock and keep creditors at bay.

Given that our calculations show that Tesla needs to raise at least $5 billion of equity, if not closer to $8 billion, to stay solvent in the next 14 months, the company needs to find at least another dozen Ron Baron sized investors. We do not believe that this will be possible given their expected future losses, working capital and capital expenditure needs, lousy execution with the Model 3, falling demand for their somewhat stale Model S and Model X, tax rebates of $7,500 per car that will start going away shortly, impending competition from Jaguar, Mercedes, Porsche, BMW, Audi, etc., the credit rating downgrade by Moody’s to Caa+ while leaving the credit on watch for further downgrades (Caa+ is basically defined as impending default), the NTSB investigation into the accident caused by the “Full Self Driving” option that they collected $3000 for (which may create a class action lawsuit, fines and the disabling of the feature), the fact that they have had 85 letters and investigations back and forth with the SEC (a very unusual pattern), the fact that their three top finance executives (CFO, Chief Accounting Officer, and Director of Finance) have left the company over the last 18 months leaving huge amounts of awarded by unvested shares on the table, a highly suspicious pattern, and the fact that the company owes suppliers roughly $3 billion of unsecured payments, which could be “called” at any time, similar to a run on a bank.

If Tesla's suppliers simply asked for their past invoices to be paid and to be paid in cash at the time of their next parts delivery, a likely outcome the worse Tesla’s balance sheet gets, it is clear that Tesla would need to file for protection from creditors. Further, the banks lending Tesla money cannot ignore the balance sheet. They have strict rules that regulators enforce about lending to companies with increasingly negative working capital. The company’s story about further drawing down lines of credit to finance operating losses and capital expenditure needs may seem plausible to novice investors but, in our opinion, not to suppliers and regulated lenders. In a game of financial musical chairs, it is important to sit down quickly.

Who in their right mind would continue to finance this money losing operation? Up to this point, it has been from growth investors who have likely never owned an auto stock before. Once they figure out the industry and the truth about Tesla’s future, we doubt it will continue.

Outlook

We are very excited about the Vilas Fund’s portfolio. Our top holdings of Walgreens, Barclays, Honda, Citigroup, and NMI Holdings, should provide very attractive returns for our partners from this point forward. These companies are growing nicely and are trading at depressed valuations. We have added to a number of other holdings at compelling prices as well. Our long portfolio, on a weighted average basis, is currently trading at a bit under 10 times 2018 earnings estimates and roughly 9 times 2019. We believe that these holdings, in aggregate, should experience 6% to 8% annual earnings growth, pay a growing dividend stream of roughly 3%, buy back ~2% of their outstanding shares annually, and experience a couple of points of valuation expansion over the next five years. Nothing heroic.

While some may fret about the overall level of the stock market and whether another big decline is right around the corner, it is important to remember the words of Peter Lynch: "Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves."

When value stocks outperform growth once again, our portfolio should generate returns above the market averages, as occurred in the 2000-2002 period when the equity fund I managed rose 19% while the stock market fell 38%. This was the last time value outperformed growth by a meaningful margin. Due to the power of reversion to the mean, another run for value is both inevitable and quite overdue. For this reason, we are very, very optimistic. Further, we are short a company that will likely never make a consistent profit and who, in all likelihood, will enter the protection of bankruptcy if they cannot raise outside capital. As those with experience know, Wall Street is not always open for business and capital availability is very fickle. A cyclical, debt ridden, capital intensive business is highly likely to fail when the money spigot gets turned off.

As Ben Graham wrote: “the intelligent investor is a realist who sells to optimists and buys from pessimists.” Seems like a good strategy to us.

Sincerely,

John C. Thompson, CFA

CEO and Chief Investment Officer

Vilas Capital Management, LLC.

The Aon Center, Suite 5100

200 East Randolph Street

Chicago, IL 60601

{kind=link}