The concept of risk parity was a novel conception based upon the premise of an allocation of risk, usually defined by volatility, rather than an allocation of capital. In a traditional 60/40 equity/bond portfolio allocation, the risk allocation is far from 60/40, more likely approaching 90/10. That is, 90% of your portfolio’s risk, again using the trusty volatility metric, would be a consequence of the equity allocation, with fixed income being a minor contributor.

Q1 hedge fund letters, conference, scoops etc

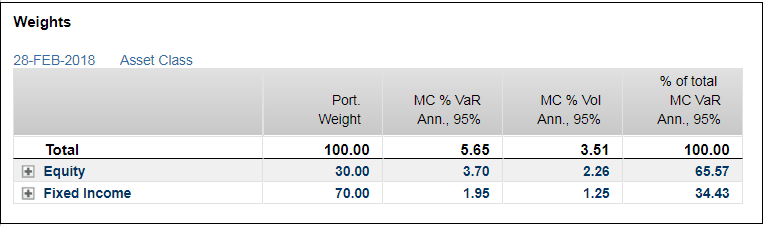

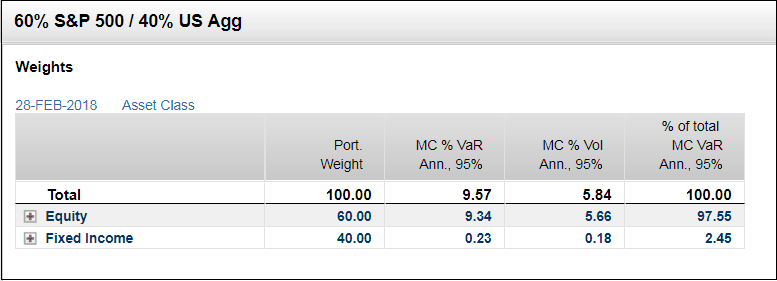

Using a multi-asset class risk model, we can see that a simple 60/40 split of S&P 500/US Aggregate actually gives a 98/2 risk profile.

We need a split more in the region of 30/70 equity/fixed income to give a risk split nearer to the desired 60/40.

In risk parity, rebalance of the composite, and therefore reallocation of capital, is based not around restoring the 60/40 balance by way of market value, but by retaining a 60/40 balance by way of risk, with 60% of your portfolio’s risk contributed by your equity allocation, and 40% from the fixed income component. The weights and capital allocation would be backed into from there, and a mere consequence of hitting the risk target.

A darling of the world’s largest hedge fund, Bridgewater Associates, the risk parity concept of portfolio management has proved hugely popular, with up to $400 billion in such strategies.

This all seems great, and appears to offer a neat solution. After all, the premise of a classic 60/40 split was to balance risk/return, and to offer a 60% exposure to the equity markets, with a 40% fixed income risk to hedge against equity downside. However, this assumes a consistent risk profile of each asset class, and the long held view of inverse correlation continues (and will indeed further continue to hold true).

But How Well Does Risk Parity Work in the Real World?

Risk parity and volatility targeting improves the classic allocation profile, since in an equity bull market increasing exposure would be a great decision with respect to returns, and would equally be permissible from a risk perspective. What comes with an equity bull market? Decreased volatility, decreased risk.

So from a risk perspective, if risk is decreasing and returns are increasing, we have found the holy grail of portfolio management. As the stock market moves higher and higher, volatility (and therefore apparently risk, too…) moves lower and lower, and so we can afford to allocate more and more to the stock market without affecting the risk profile. In fact, it’s compulsory if we’re risk targeting. We would have to increase our equity exposure. Right when equities are soaring. It’s no wonder the strategies have proved so popular.

Not so fast though. This strategy can, and does, lead to large dislocations in the markets. As the stock market plods higher, volatility moves lower, which means these strategies have to hit the bid and buy more and more stocks. This suppresses volatility, which means the allocation to stocks must increase, so they hit the bid, thus suppressing volatility… You get it. This leads to a perpetual trend following, and mixed with huge asset purchases from the central banks, gets us nicely to the record breaking low volatility we’ve seen for what seems like an eternity now.

However, there’s an elephant in the room. What happens when the stock markets turn? What happens when the trillion dollar buyers in the central banks decide enough is enough, and the bids disappear? The second the markets turn and volatility increases, the exact opposite will occur. The strategies will be forced to sellers, spiking the VIX in a heartbeat, leading to an even bigger dump of equities as the strategies seek to rebalance their risk and reduce their volatile equity exposure, which in turn drops the markets, which in turn increases volatility, which forces sellers. Again…you get it.

VIX

The VIX started out as a measure of stock market volatility, but has become one of the most significant benchmarks in finance, not simply because of its measurement of stock market health and volatility, but because of the sheer amount of money bet directly on it. Since the invention of the VIX future, VIX options, and subsequent VIX ETFs, billions upon billions have been bet directly on its level.

As volatility was suppressed by central bank purchases and risk parity strategies, short-volatility bets snowballed, and the build-up of a short position became yet another suppressor of volatility. To offer the short volatility positions that investors were demanding, dealers had to hedge their side, and how do you readily hedge your long volatility position? Long stocks. As volatility lagged, and investors piled in to such profitable and trendy short volatility positions, their bets were further suppressing volatility.

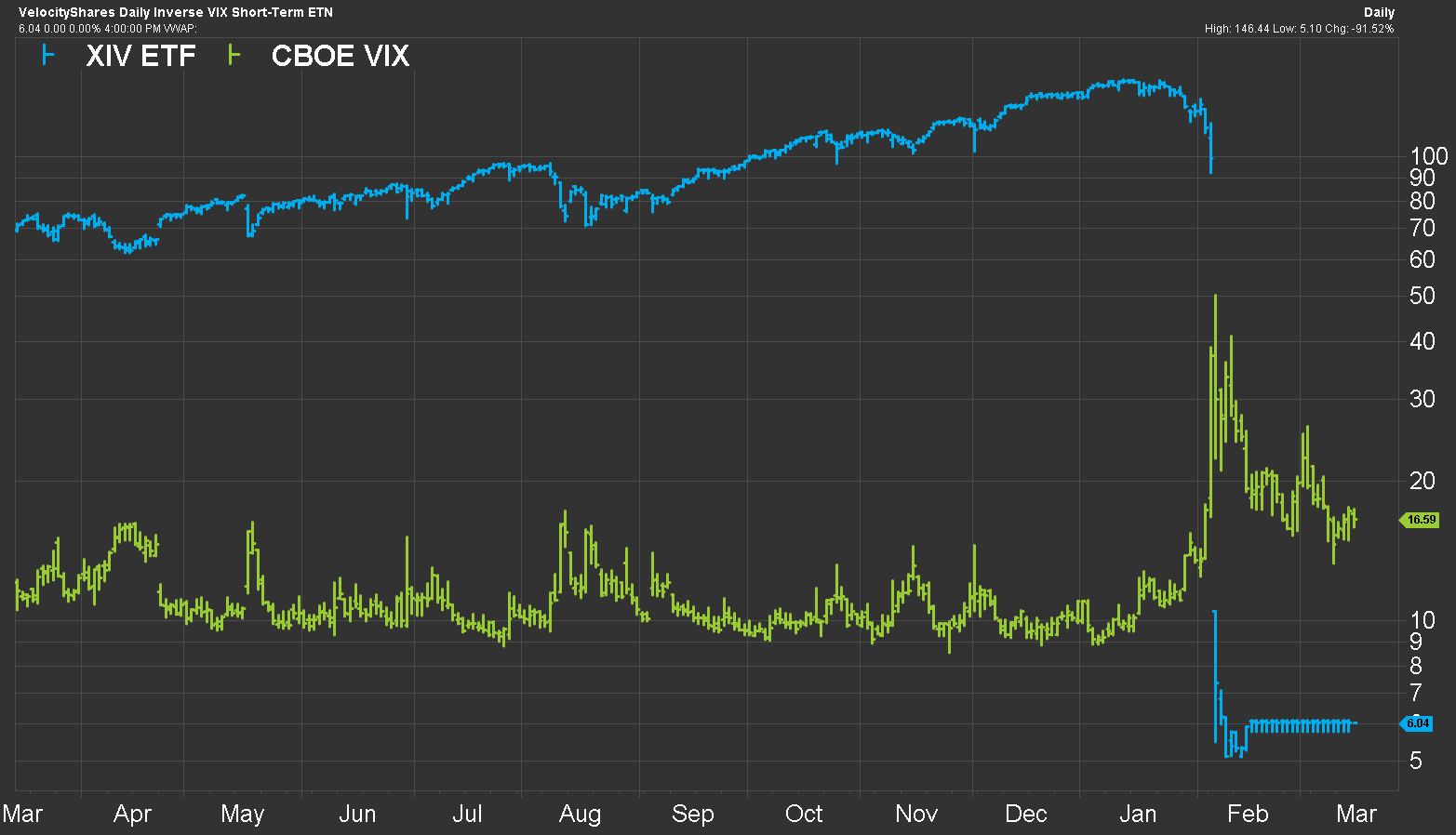

(AUM of the largest short volatility ETF, XIV)

This notion has subsequently drawn the concerns of ‘the tail wagging the dog’, or perhaps a more sinister comparison to Ouroboros.

http://mythologian.net/ouroboros-symbol-of-infinity/

Volatility used to be a measure of the stock market, or a derivative of stock market behavior, an effect, whereas now bets on volatility have become a driver of the stock market, a cause.

The positions paid off handsomely, though, and the inverse VIX ETFs, helped by the VIX future contango, were some of the best performing assets last year.

However, just like the risk parity strategies, such bets are a double-edged sword. As volatility increases, dealers rush to buy back volatility future positions to rebalance hedges. In an illiquid market, a sudden buyer of huge quantities of VIX futures drives prices higher, increasing the VIX, creating further need to rebalance and buy back volatility, begetting higher volatility.

Now the correlation between VIX spot and futures isn’t quite perfect due to a lack of facile arbitrage between the two, but the causality is there.

We can now see clearly the effect of this volatility Ouroboros in the events of last month, where the VIX exploded from 10 to 40 in minutes, futures exploded even higher as the sudden rush of volatility buyers disconnected the VIX spot and futures, and short volatility products disintegrated and dissolved, taking with them the billions of dollars bet on them.

(As the VIX spikes, the price of the largest inverse VIX ETF capitulates)

What Do We See for the FI Side, and What of This Assumes Inverse Correlation?

Now, we see the effects of these strategies on the stock market, but how did these risk parity strategies, and volatility blow-up, affect the bond markets?

You could argue that the bond markets have been distorted beyond all recognition by central banks, and considering their unlimited coffers, a mere $400 billion in risk parity strategies would be a drop in the ocean. The sheer size of the bond market renders it far more robust and sheltered from such flow effects. The bond market is simply too big for the risk parity guys to be major players.

With central banks printing new money and injecting it into the bond markets, flows become meaningless, as money doesn’t need to be extracted from the stock market to flow to the FI market (or vice versa); it can just come from the printing press.

This has mostly been true, although the danger here lay not in spiraling flows and trend following, but the presumed inverse correlation between bonds and equities. Historically, bonds and equities have indeed been inversely correlated, and bonds have provided a useful safety net in times of stock market turbulence.

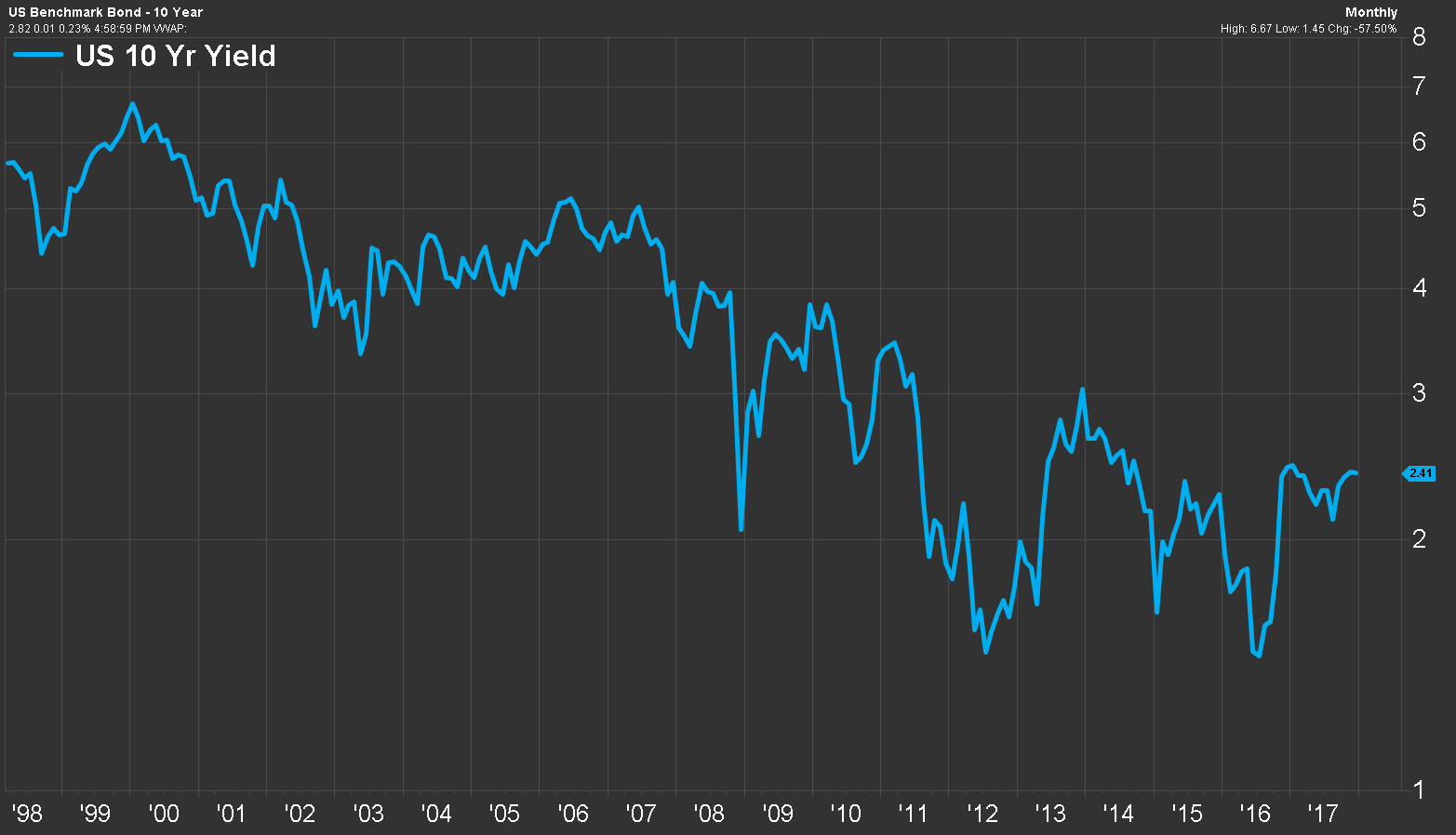

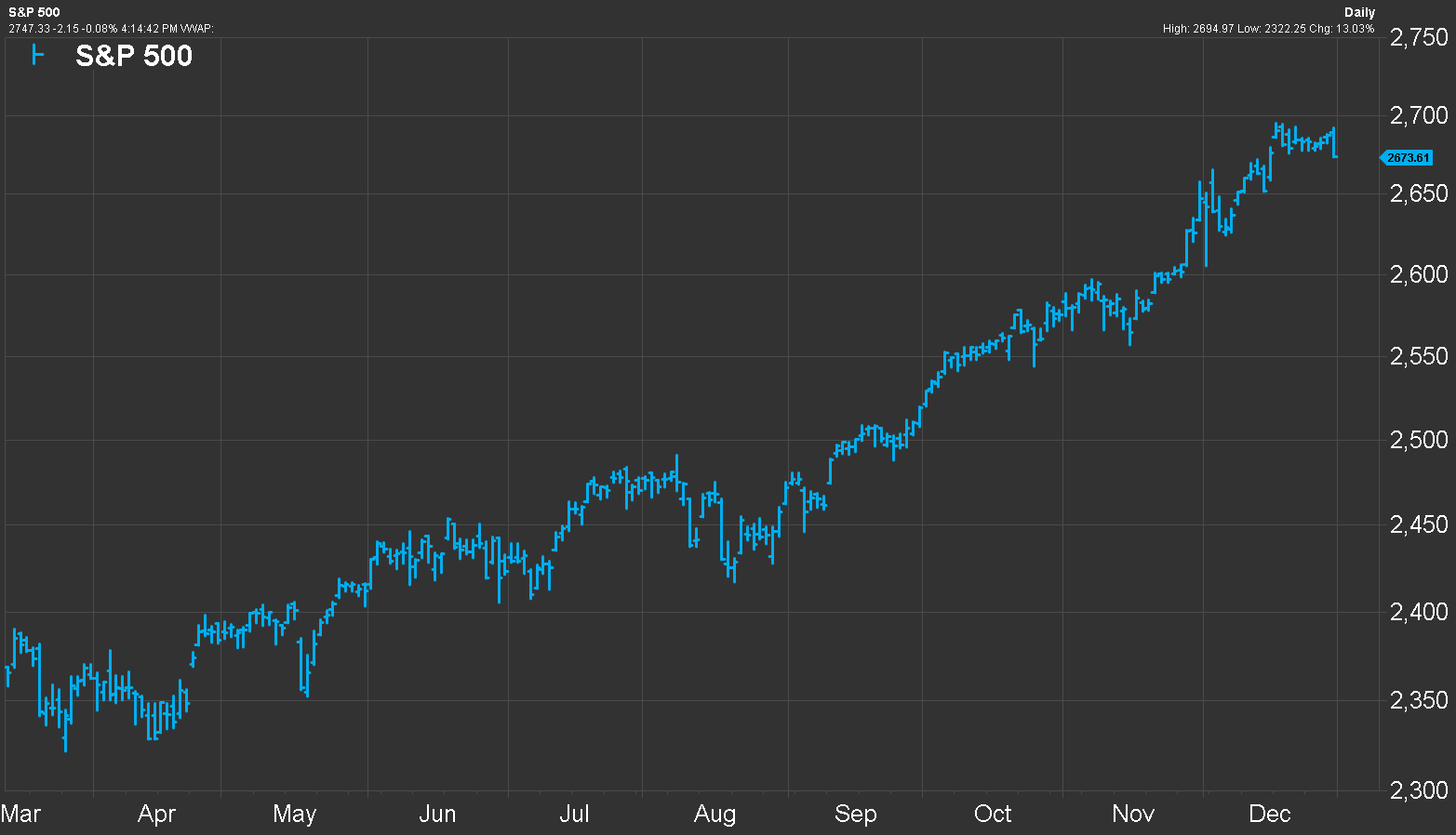

However, recently we’ve seen both equity and bond markets hitting all-time highs, which seems counter to our notion of inverse correlation. Despite the recent retracement, the U.S. 10-year yield is hovering near all-time lows and well below historical averages, whilst the S&P has been unstoppable.

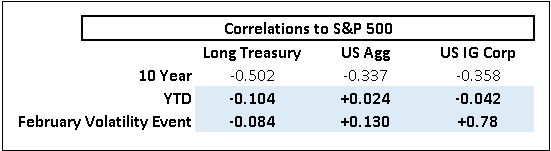

Using correlation coefficients to determine correlation between the equity market returns and some common fixed income hedges, we see that the 10-year correlation is exactly in line with what we know for sure, that equity and fixed income movements are indeed complimentary.

10-year correlations between the S&P 500 and TLT (a long dated U.S. Treasury Bond ETF), the U.S. Aggregate (a generic U.S. bond market index), and U.S. Investment Grade corporate debt are all comfortably negative.

However, things get interesting when we start to look at how they have behaved more recently. Year-to-date correlations drop notably, with only TLT offering a significantly negative correlation. The two indices show a drastic decrease in inverse correlation, with the U.S. Aggregate actually flipping positive.

If we look at correlations throughout the latest market event, things are even uglier. During the recent volatility blow-up throughout February, our fixed income hedges have all moved even further into positive territory; only TLT remains negatively correlated, and over five times lower than the historical average at that.

Using the latest volatility-based market blow up, shows that the traditional "equity falls and bonds rise” notion is perhaps no longer an appropriate way of allocating risk and capital. Most risk parity funds will be more complex than a simple equity/fixed income blend. However, this shows that the markets can, and will, change, and strategies based on historical correlations may be left exposed. Correlations work… until they don’t.

As Mark Twain so famously put it, “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

Article by Jack Hayes, FactSet Insight

{kind=link}