Shares of Wesco Aircraft Holdings Inc (NYSE: WAIR) are receiving a lot of investor interest as of late due to the stock’s 16.4% increase over the last month. Shareholders are now asking themselves whether the company’s current stock price is reflective of its true value or if shares have even further upside from here.

Let's take a look at Wesco Aircraft's value and outlook based on its most recent financial data to see if there are any catalysts for a price change.

Is Wesco Aircraft Still Cheap?

Good news, value investors! Wesco Aircraft is still a bargain right now. According to the valuation below, the intrinsic value for the stock is $12.66, which is above what the market is valuing the company at the moment. This indicates a potential opportunity to buy low.

| Wesco Aircraft Holdings Inc Valuation Detail | ||

| Analysis | Model Fair Value | Upside (Downside) |

| 10-yr DCF Revenue Exit | $13.98 | 36.4% |

| 5-yr DCF Revenue Exit | $13.56 | 32.3% |

| 10-yr DCF EBITDA Exit | $14.76 | 44.0% |

| 5-yr DCF EBITDA Exit | $14.67 | 43.1% |

| Peer EBITDA Multiples | $9.86 | -3.8% |

| 10-yr DCF Growth Exit | $12.38 | 20.8% |

| 5-yr DCF Growth Exit | $10.93 | 6.7% |

| Earnings Power Value | $11.11 | 8.4% |

| Average | $12.66 | 23.5% |

Click on any of the analyses above to view the latest model with real-time data.

Wesco Aircraft's share price also seems relatively stable compared to the rest of the market, as indicated by its low beta. If you believe the share price should eventually reach its true value, a low beta could suggest it is unlikely to rapidly do so anytime soon, and once it’s there, it may be hard to fall back down into an attractive buying range.

What Does The Future Of Wesco Aircraft Look Like?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Buying a great company with a robust outlook at a cheap price is always a good investment, so let’s also take a look at the company’s future expectations.

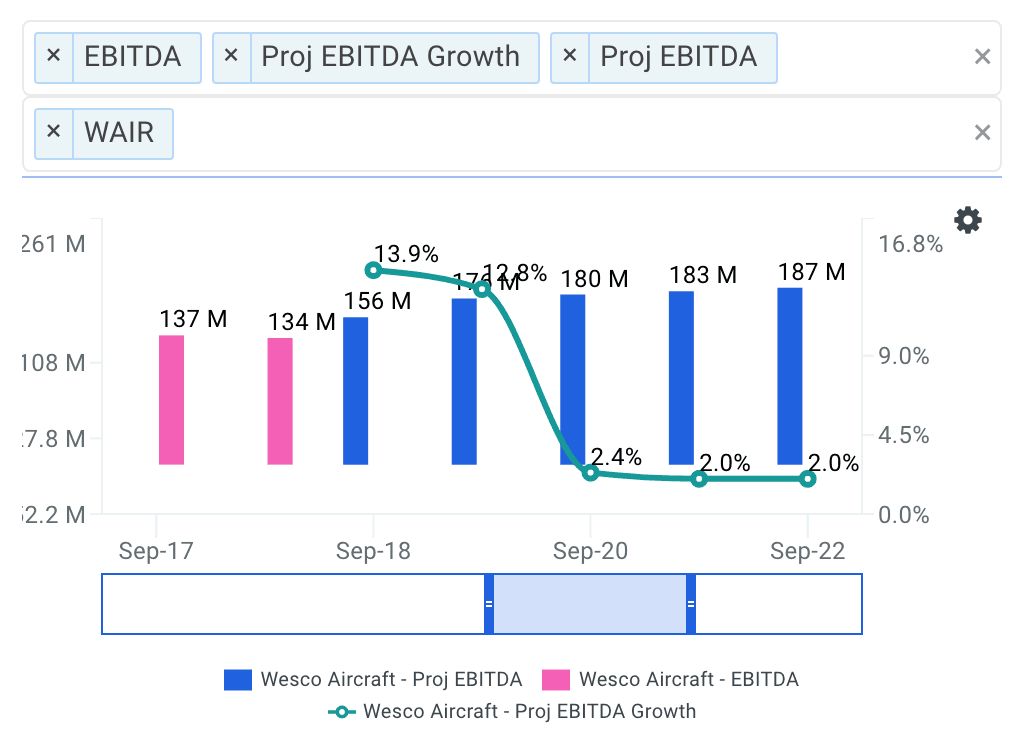

source: finbox.io data explorer

With Wesco Aircraft's relatively muted EBITDA growth of 6.5% expected over the next five years on average, growth doesn’t seem like a key catalyst for a buying decision, at least in the short to medium-term.

How This Impacts You

Many investors separate stocks into value and growth categories based on quantitative metrics. However, one of the most famous investors in the world views this as foolish. In Warren Buffett's 1992 letter to Berkshire Hathaway shareholders, Buffett touches upon a subject at odds with much of the investment industry:

"Most analysts feel they must choose between two approaches customarily thought to be in opposition: 'value' and 'growth.' Indeed, many investment professionals see any mixing of the two terms as a form of intellectual cross-dressing. We view that as fuzzy thinking… In our opinion, the two approaches are joined at the hip: Growth is always a component in the calculation of value."

While investors tend to categorize stocks into value and growth, some of the most successful investors view growth as simply one component of a company's value.

Although Wesco Aircraft's future growth is relatively low, the company's stock still appears to be trading at a discount to its intrinsic value. Therefore, it may be a great time to purchase shares or add more to your existing holdings.

But before making an investment decision, I recommend you continue to research Wesco Aircraft to get a more comprehensive view of the company by looking at:

Valuation Metrics: how much upside do shares of Wesco Aircraft have based on Wall Street's consensus price target? Take a look at our analyst upside data explorer that compares the company's upside relative to its peers.

Risk Metrics: what is Wesco Aircraft's asset efficiency? This ratio measures the amount of cash flow that a company generates from its assets. View the company's asset efficiency here.

Forecast Metrics: what is Wesco Aircraft's projected EBITDA margin? Is the company expected to improve its profitability going forward? Analyze the company's projected EBITDA margin here.

Article by Andy Pai, Finbox.io