Introduction

Over the last couple of years lithium producers and miners have enjoyed a parabolic jump in their stock prices and market caps. As I will later illustrate, much of the gains for lithium related companies have come as a result of the “hype” surrounding electric automobile development. Of course, Tesla has been the primary instigator of this “hype”type, followed by mainstream automotive manufacturer’s initiatives in all electric and/or hybrid automobiles.

Check out our H2 hedge fund letters here.

Personally, my assessment of the lithium industry is generally bullish long-term. Consequently, I believe that investing in carefully selected lithium companies at appropriate valuations could represent a compelling long-term investment opportunity. On the other hand, I never see value in positioning yourself as the “greater fool.” For those not familiar with this term, it suggests that you foolishly pay more for a company than it’s worth on the basis that a “greater fool” than you will soon come along and be willing to pay you more in the future.

Therefore, the seminal question I will attempt to answer with this offering is straightforward. Has the recent drop in lithium stocks brought these companies down to attractive valuation levels? As a general statement, most lithium stocks are significantly off their previous highs. Consequently, I have begun to see a rash of articles suggesting that this recent selloff in lithium stocks has produced a buying opportunity. Since the drops were pretty significant and over a short period of time, it appears logical that attractive valuations have recently manifested.

The Principle and Importance of Valuation

Before I go on, I want to be clear that this article is not intended to denigrate or criticize the works of other contributors. Instead, my primary motivation for producing this article is because this lithium scenario offers me the opportunity to point out and illustrate a quintessential example of both the dangers and risks that high valuations create. This is consistent with my plans for producing articles that elaborate on and demonstrate sound value investing principles as articulated in my January 18, 2018 blog post found here.

The primary sound investing principle that the following FAST Analysis video will clearly illustrate is that not all price drops are the same. Implicit in this analysis is what I consider the undeniable reality that there are major differences between an attractively valued company with strong fundamentals that experiences a significant price drop versus the price drop of a significantly overvalued company with strong fundamentals. My contention is that the former likely represents a strong buying opportunity, whereas the latter may or may not. Most importantly, I believe this distinction is critical towards controlling risk and generating adequate long-term returns commensurate with the risk you are taking.

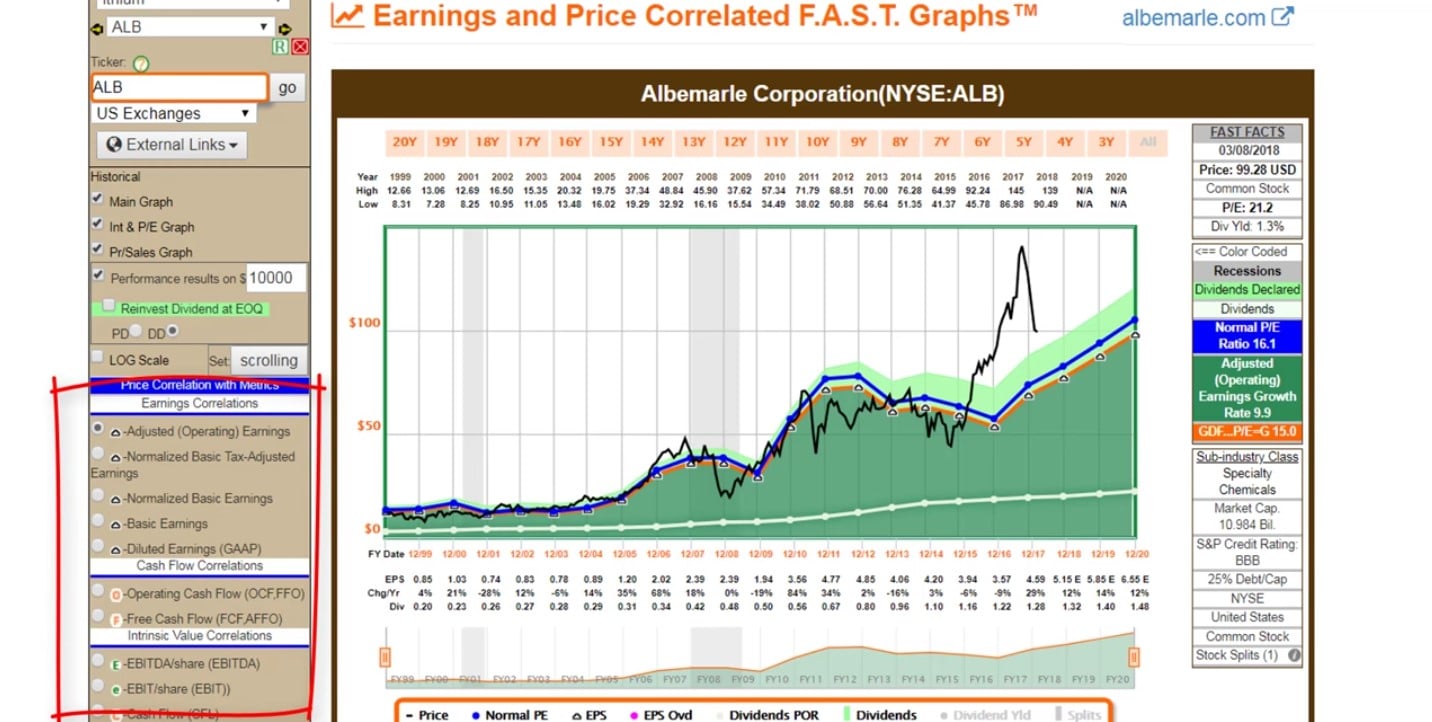

FAST Graphs Analyze Out Loud Video: Albemarle vs FMC

Both Albemarle (ALB) and FMC Corp (FMC) are leading developers of lithium used in lithium-ion batteries. And, most lithium related companies have seen parabolic increases in their stock prices over the last couple of years. However, as the following video will clearly reveal, the prices of both of these quality lithium producers have seen their prices rise ahead of even optimistic forecasts of future growth of earnings.

Consequently, when this happens (as I’ve written about many times before) when a company’s stock price rises significantly above its true worth value, that high price becomes vulnerable to even a hint of bad news. Since Tesla is the poster child for electric cars utilizing lithium-ion batteries, negative reports on and recent guidance from Tesla have shaken investor sentiment towards lithium companies. The result has been a recent and rather significant drop in prices and market cap for leading lithium producers.

With the following video I will illuminate whether or not these price drops have been enough. Additionally, I believe the video will further reveal that excessive valuation represents an apparent mistake that investors can – and should – avoid. It is hard enough to get investing in stocks right. Therefore, it’s imperative that investors do not make mistakes that are readily apparent. Significant overvaluation is an obvious mistake that is easy to avoid if you keep your emotions in check.

Summary and Conclusions

As I illustrated in the video, lithium stocks experienced a wide disconnect from intrinsic value based on fundamentals versus stock price action. Moreover, even though the recent swoon in price and value has created a better opportunity than we have seen recently, it’s still questionable whether it’s enough or not. Personally, I would say not quite yet, but we are certainly getting closer.

On the other hand, I believe that the recent surge in lithium consumption has created an enticing long-term investment opportunity. Consequently, the recent correction with these companies’ stock prices might be attractive enough to motivate more aggressive investors to invest. However, if you are conservative and/or have a low tolerance for risk, prudence and patience may be in order.

Finally, the most important message I was attempting to convey was to illustrate that excessive valuation is an obvious mistake that can be avoided if you are looking at fundamentals relative to current valuations. Additionally, excessive valuation adds what I consider an avoidable level of risk while promising less return than the businesses are capable of generating on your behalf. Buying low with the objective of selling high is more than a catchy old adage. Being only willing to invest when valuations make practical economic sense is a tried and true value investing strategy. You don’t have to catch the perfect bottom, but you should be rational and prudent with your investing decisions. Caveat emptor!

Disclosure: No position.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Article by F.A.S.T. Graphs