On February 13, 2018, the DoubleLine Emerging Markets team held a webcast discussing the Emerging Markets Fixed Income Fund (DBLEX/DLENX), the Low Duration Emerging Markets Fixed Income Fund (DBLLX/DELNX) and the Global Bond Fund (DBLGX/DLGBX) titled “To Euphoria and Beyond.”

Check out our H2 hedge fund letters here.

This recap is not intended to represent a complete transcript of the webcast. It is not intended as solicitation to buy or sell securities. If you are interested in hearing more of the Emerging Markets team’s views, please listen to the full version of this webcast on www.doublelinefunds.com under “Latest Webcasts” under the “Webcasts” tab. You can use the “Jump To” feature to navigate to each slide. You can also learn more about future webcasts by viewing the 2018 webcast schedule at www.doublelinefunds.com under “Webcasts”.

To Euphoria and Beyond

- Long term, we believe that Emerging Markets (EM) presents a secular improving credit story

- Current economic and market fundamentals look strong for both Developed Market (DM) and EM countries

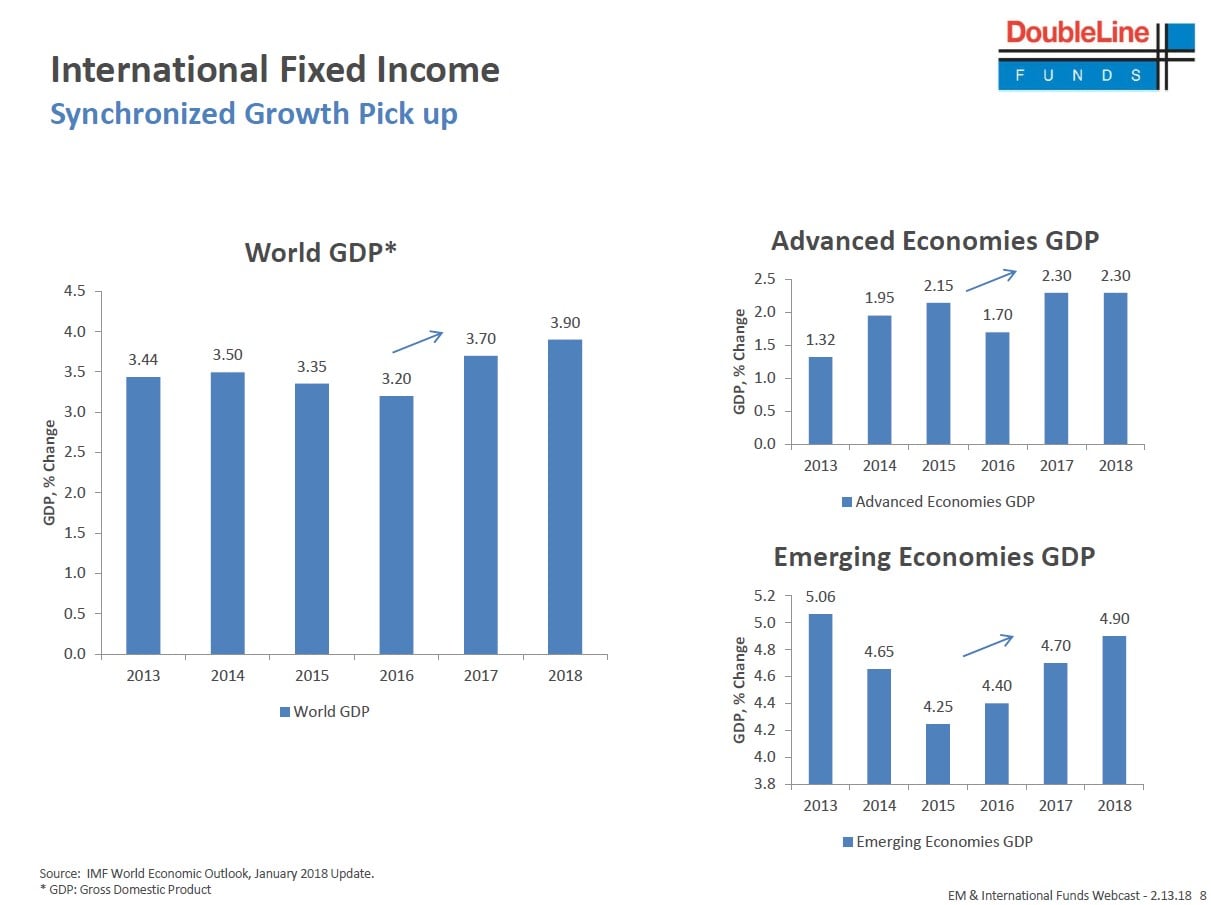

- Gross Domestic Product (GDP) has steadily risen since 2016 for DM economies and is expected to continue to increase, particularly in the U.S. off the back of tax reform and infrastructure spending

- GDP has been rising since 2015 in EM economies and is expected to continue to be strong to the tune of 4+%

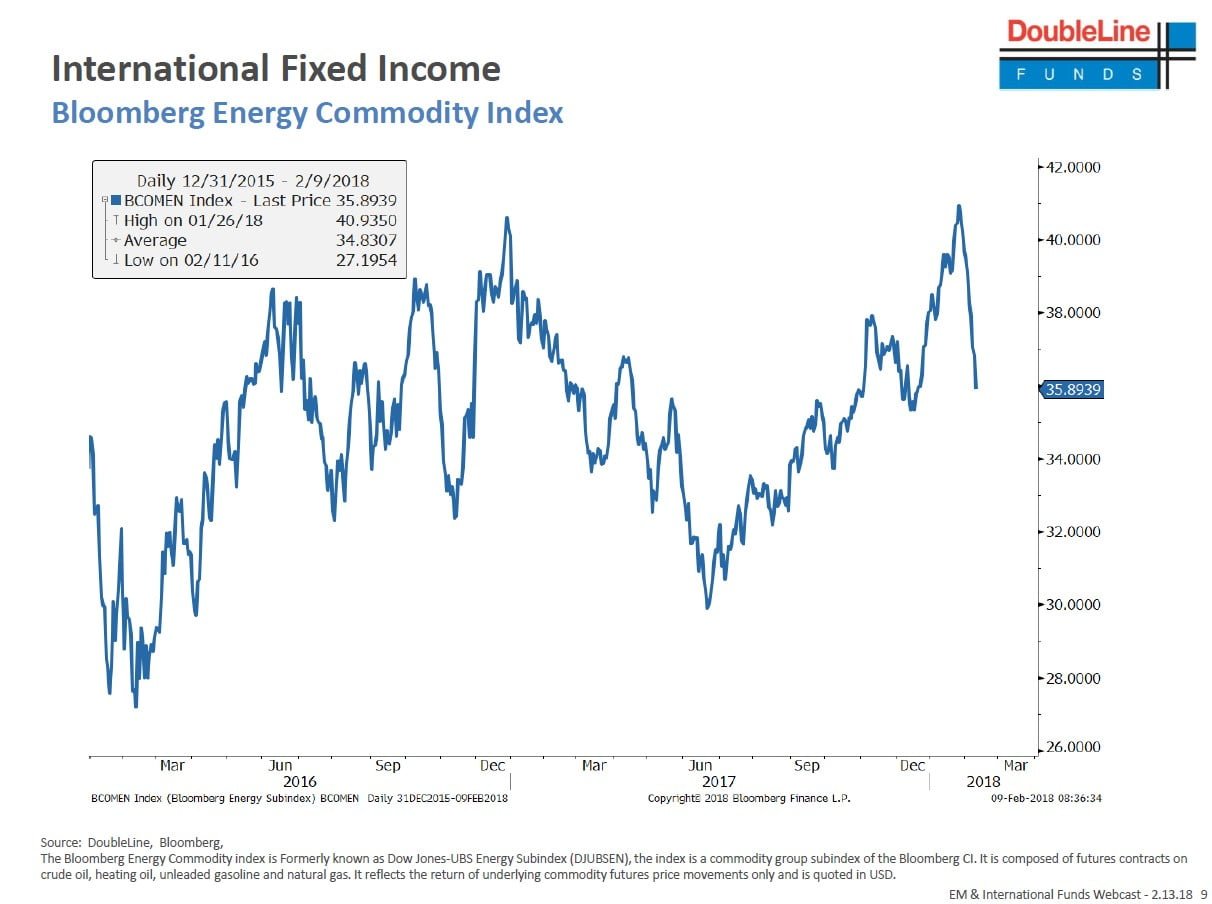

- Starting in 2016 Commodity prices have turned to the upside

- This is expected to continue as higher energy prices should lead to more capital expenditure (CapEx) from energy producers

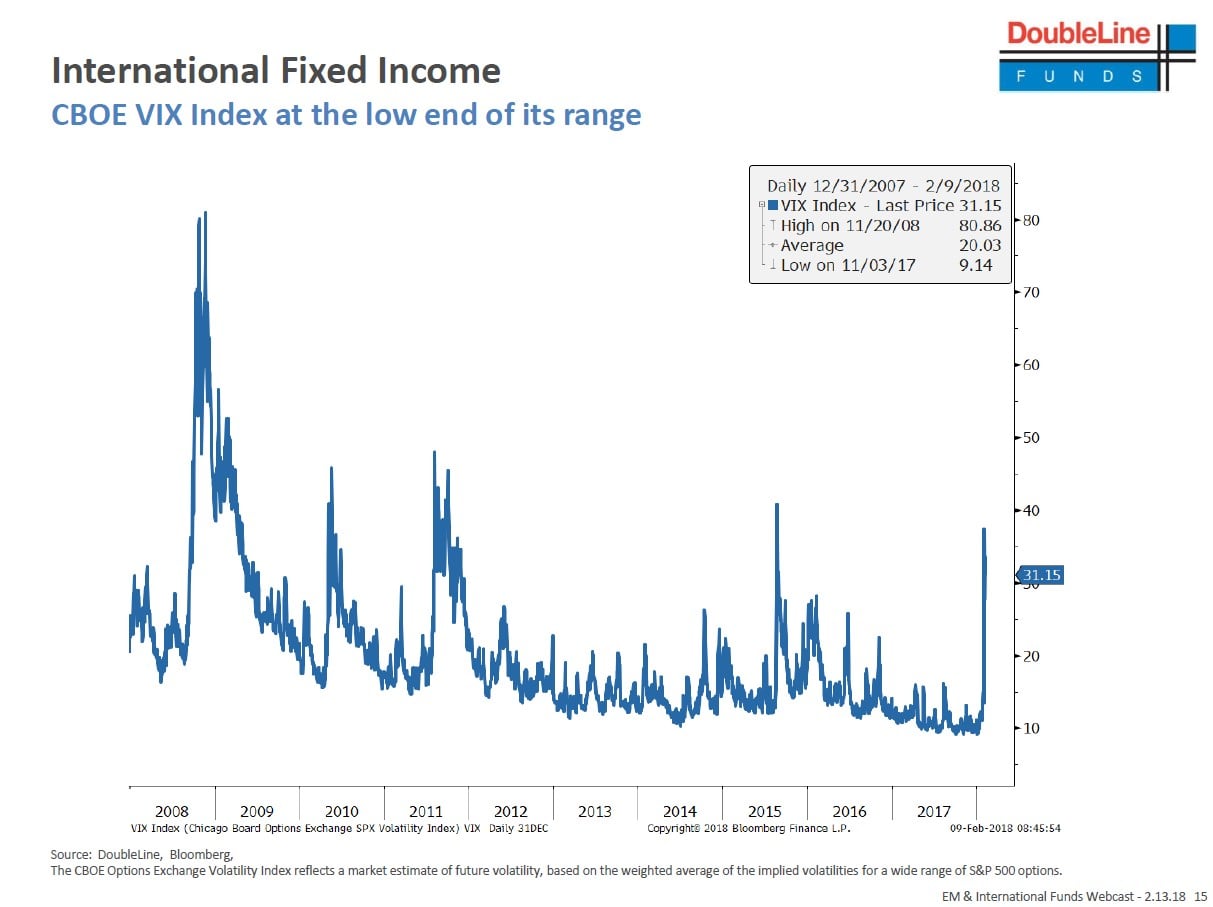

- Volatility has been very low, as measured by the Volatility Index (VIX)

- Inflation pressures were contained

- European political risk and geopolitical flare ups did not materializ

- China posted another very stable growth number in 2017

- Trade disputes did not spill over to the markets

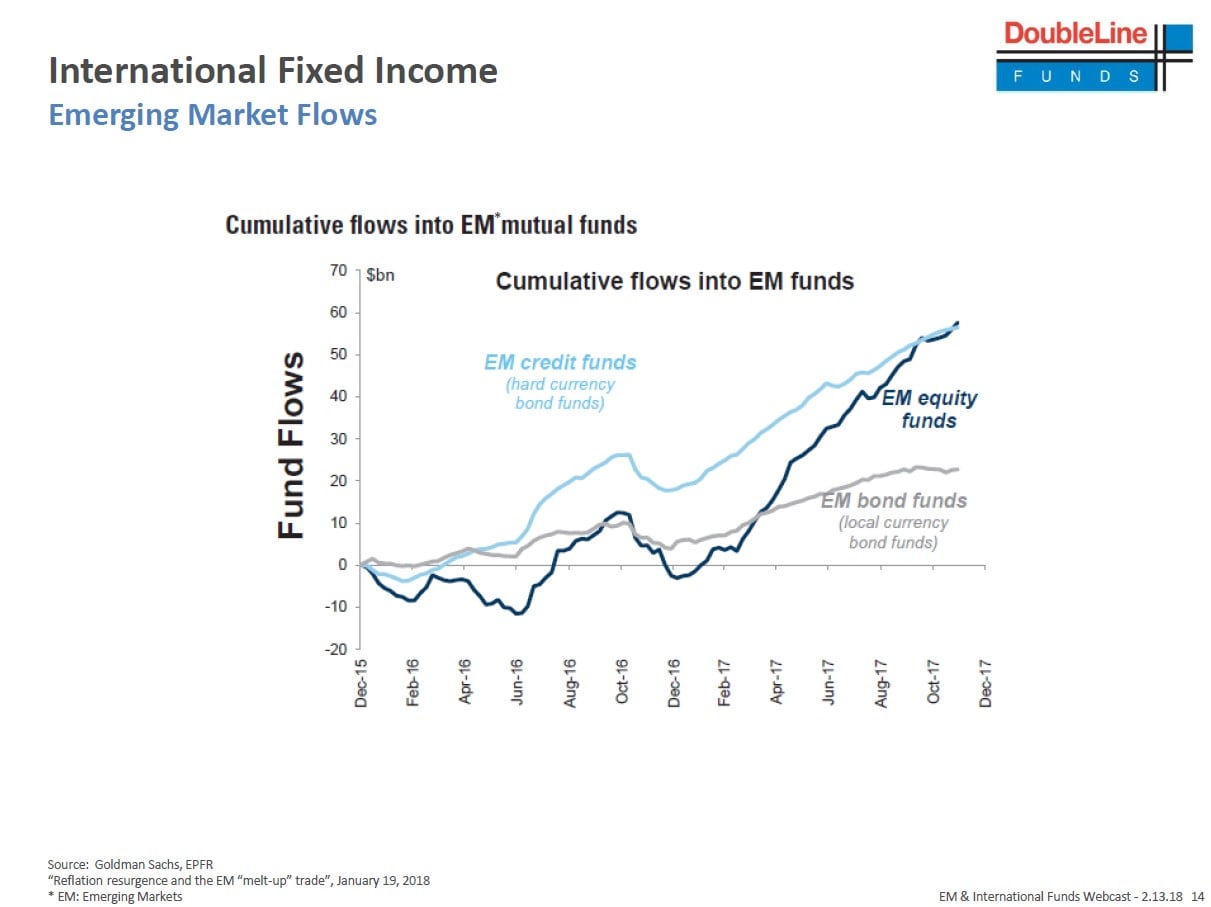

- As a result, performance of EM equities and fixed income sectors have been positive in both 2016 & 2017 leading to strong inflows across EM asset classes

- Short-term we believe there is a chance for increased volatility in EM for the following reasons:

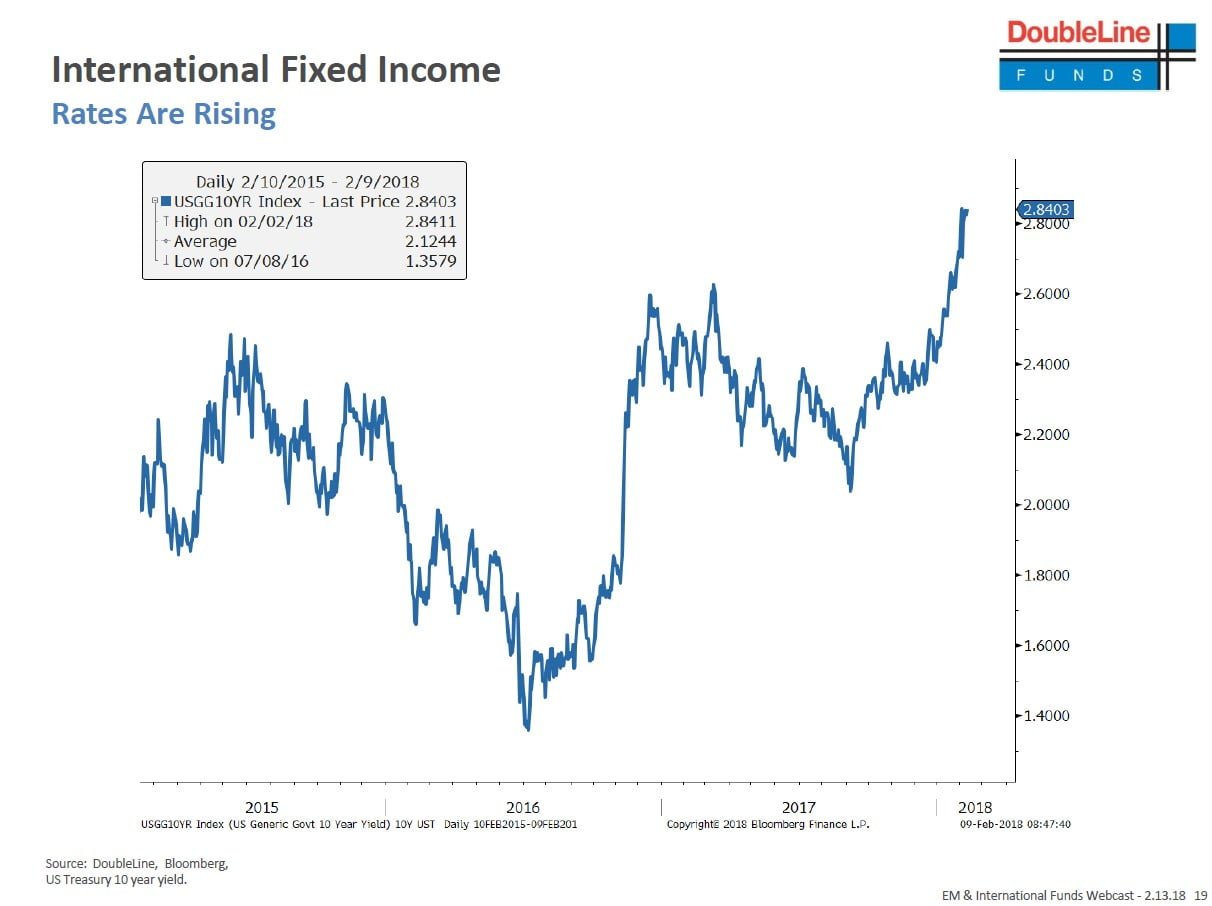

- Rise in U.S. rates due to upward GDP pressure, fiscal stimulus, a new government budget deal, infrastructure spending, an increase in inflation, an unwinding in the Federal Reserve’s (Fed) balance sheet and an increased government deficit

- Potential geopolitical flare ups

- Potential trade wars

- Heavy election cycle

- These potential risks have led us to position our EM portfolios more defensively, and we have increased our credit quality and shortened duration

Global Outlook

- Major Risks to International Fixed Income

- Rising Rates

- Increasing inflation stemming from higher global GDP growth

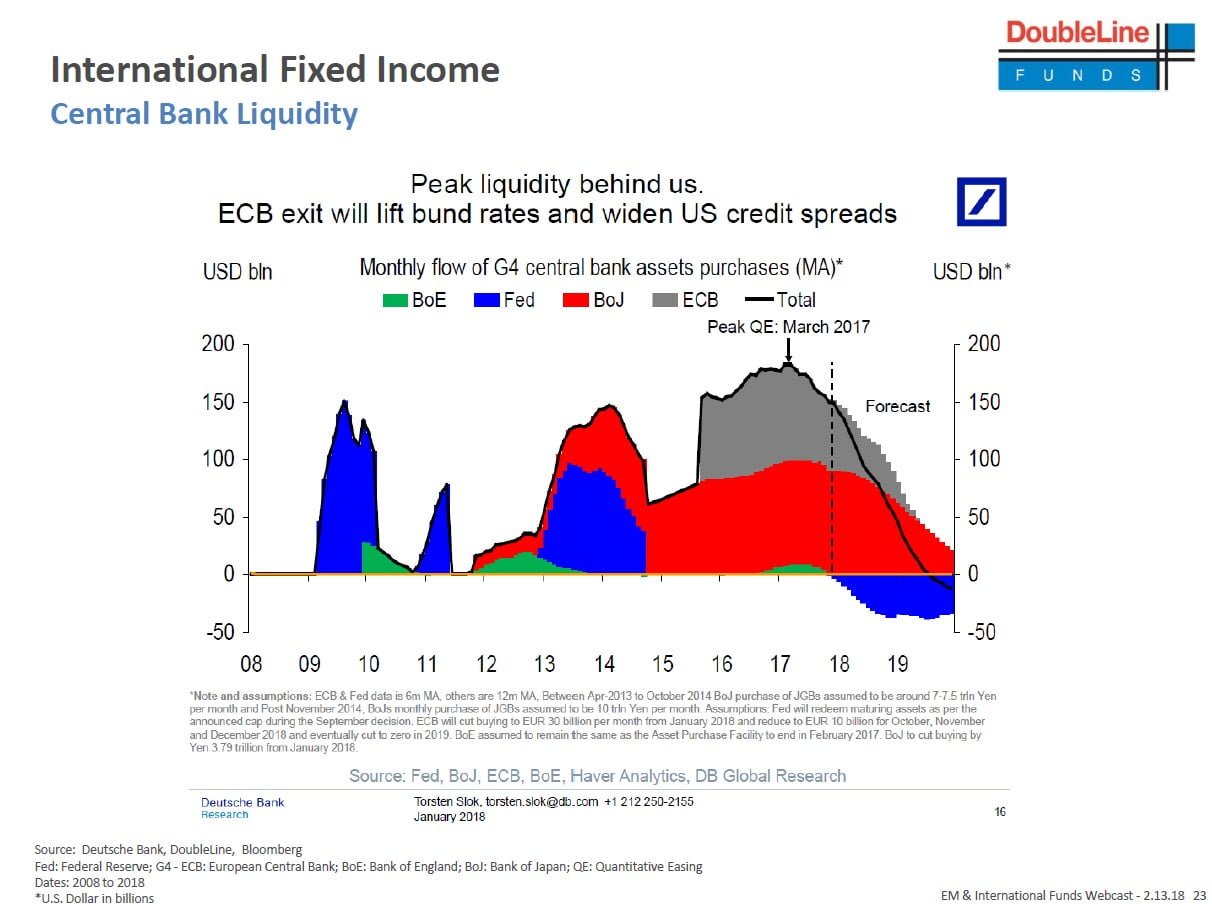

- Removal of accommodative policies and liquidity from the four main central banks (The Fed, Bank of England (BoE), European Central Bank and Bank of Japan (BoJ))

- Political risk stemming from influential elections around the world

- European Union-United Kingdom Brexit transition negotiations

- Protests relating to Russian elections

- Leftists leading polls in Columbia and Mexico

- Brazil faces crucial elections in October that could promote an economic turn-around

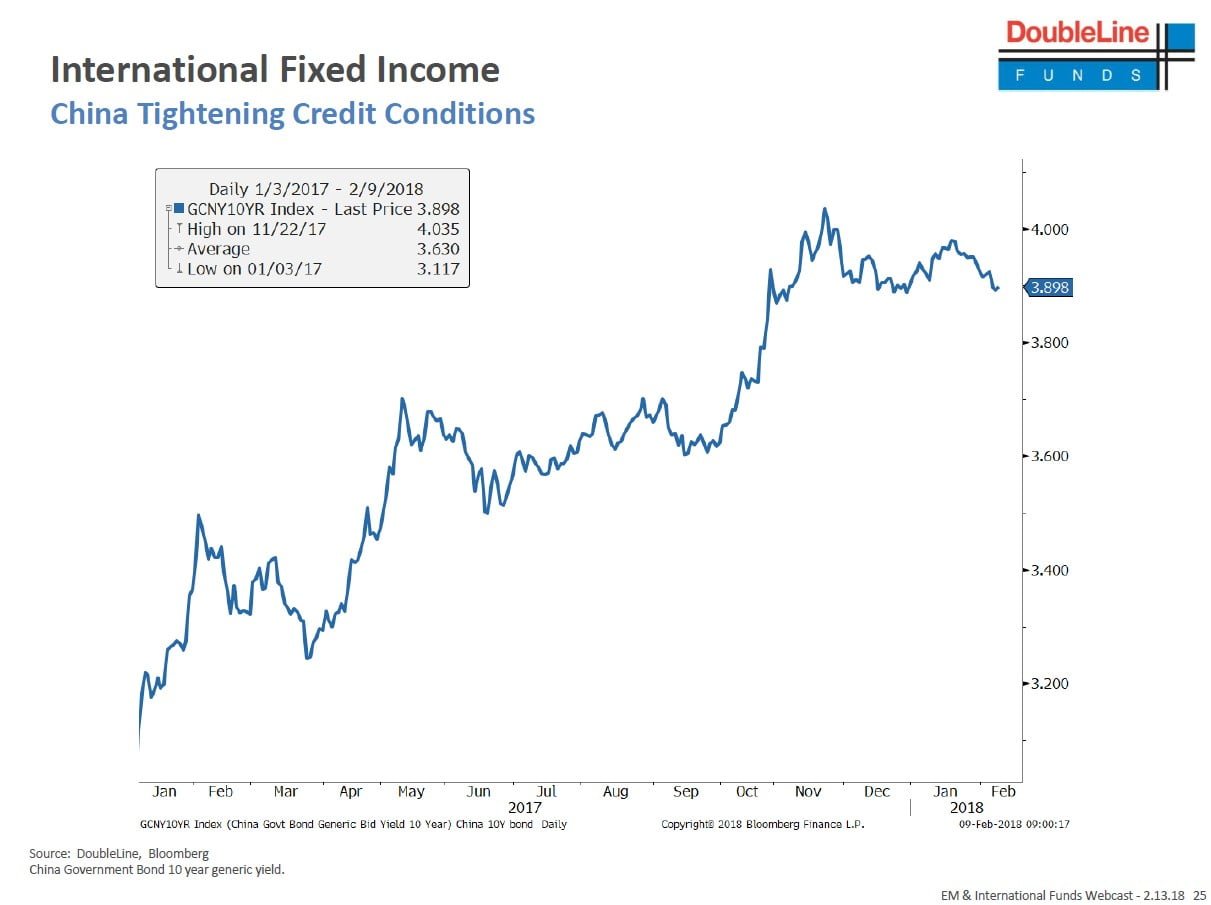

- China has been tightening credit conditions for the past year which could slow growth

- Chinese debt stands at about 270% of GDP

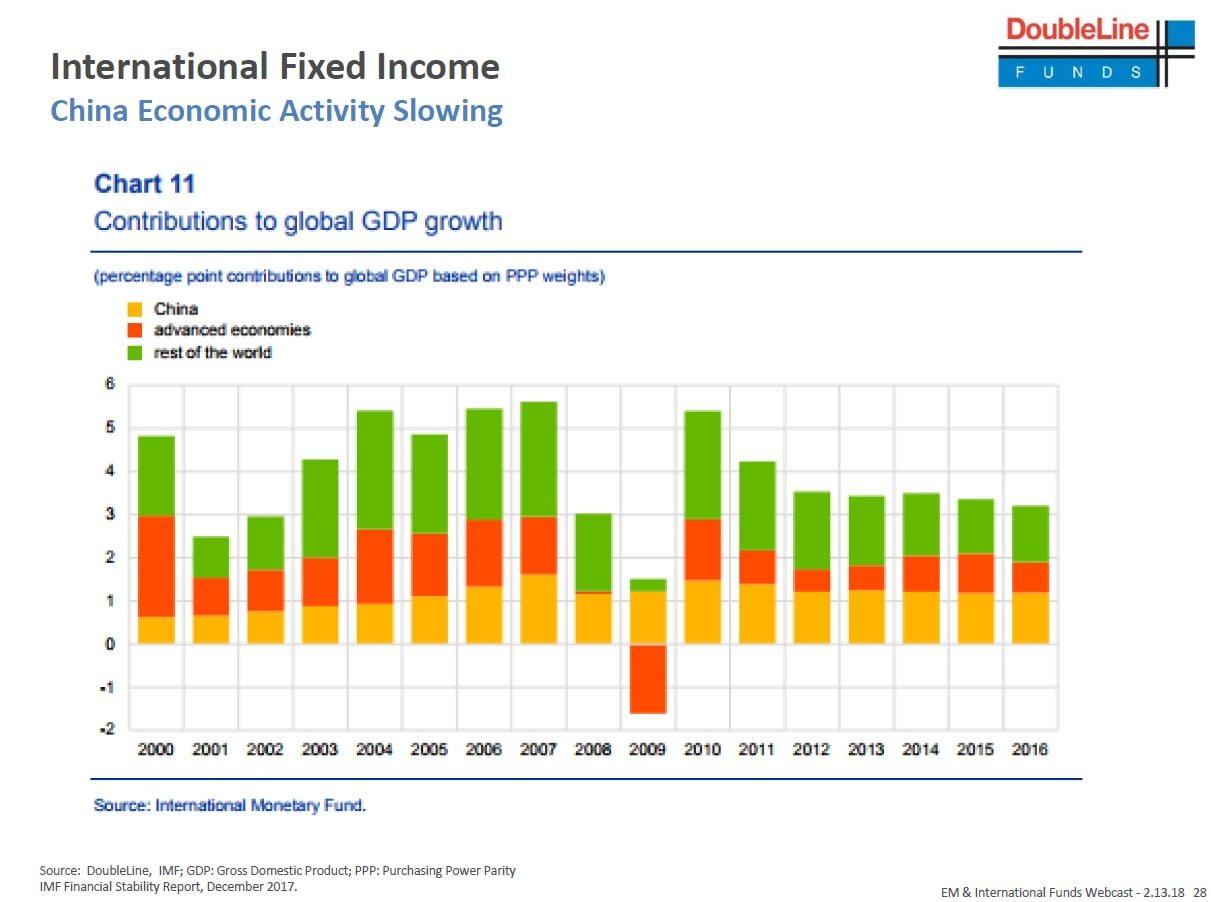

- Decelerating growth in China is globally impactful as China makes up about 1/3 of global GDP

- U.S. risks

- Geopolitical (Iran, North Korea, China, Russia)

- Trade Wars

- Domestic Political Backdrop – gridlock

2017 EM Overview

- Strong year in all areas of the asset class

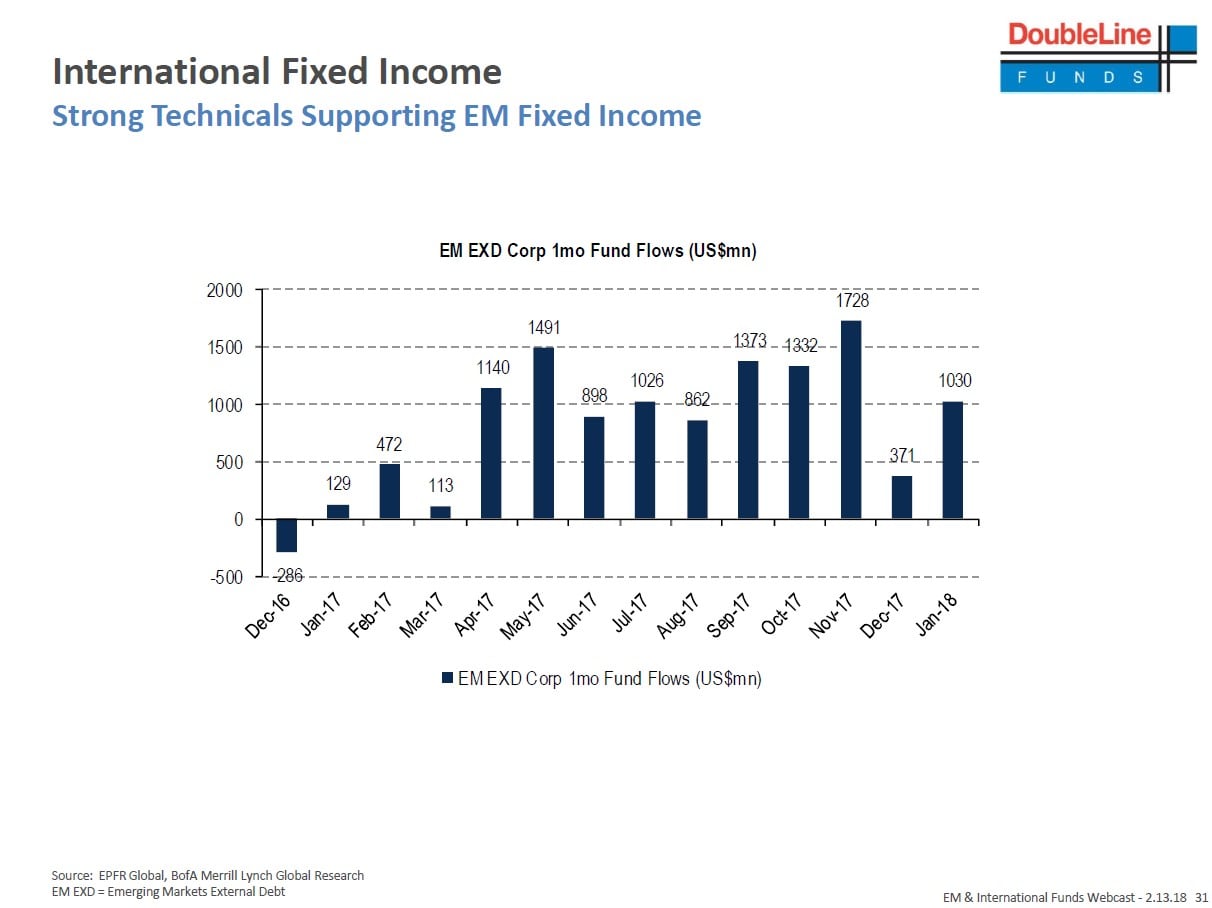

- Record inflows into EM space

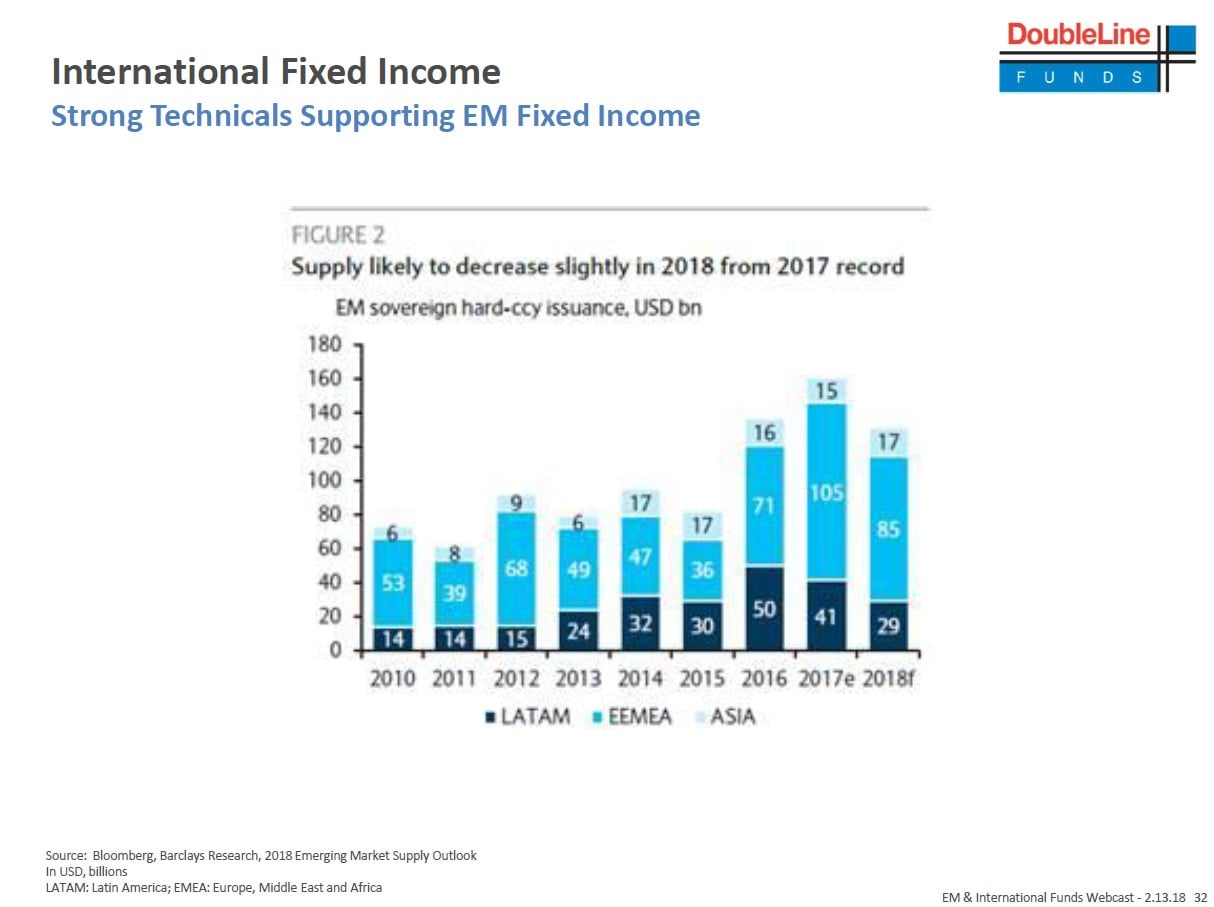

- 2017 saw record years for new issuance of new EM U.S. Dollar (USD)-denominated sovereign debt and on the corporate side

EM Expectations

- Many sell-side reports expect more of the same regarding strong flows, solid new issuance, good GDP growth, slowly rising rates, steady inflation and continued EM spread tightening

- At DoubleLine we realize market conditions do not last forever and markets change. As a result, we feel it’s important to prepare for potential downside events

- 2017 had many similarities to the 2012 environment

- Solid global growth o Impressive EM flows o Record bond issuance

- Good performance

- What followed 2012 in 2013 is well documented., At DoubleLine we believe looking back to 2013 can help us determine possible scenarios for 2018?

- In late 2012, many strategists were predicting the market landscape of 2013 to be a continuation of 2012, and in a similar fashion, many strategists are predicting the market landscape of 2018 to be the same as that of 2017?

- 2013 ended much differently than expected

- Less issuance

- Spreads widened, rather than the expectation they would tighten

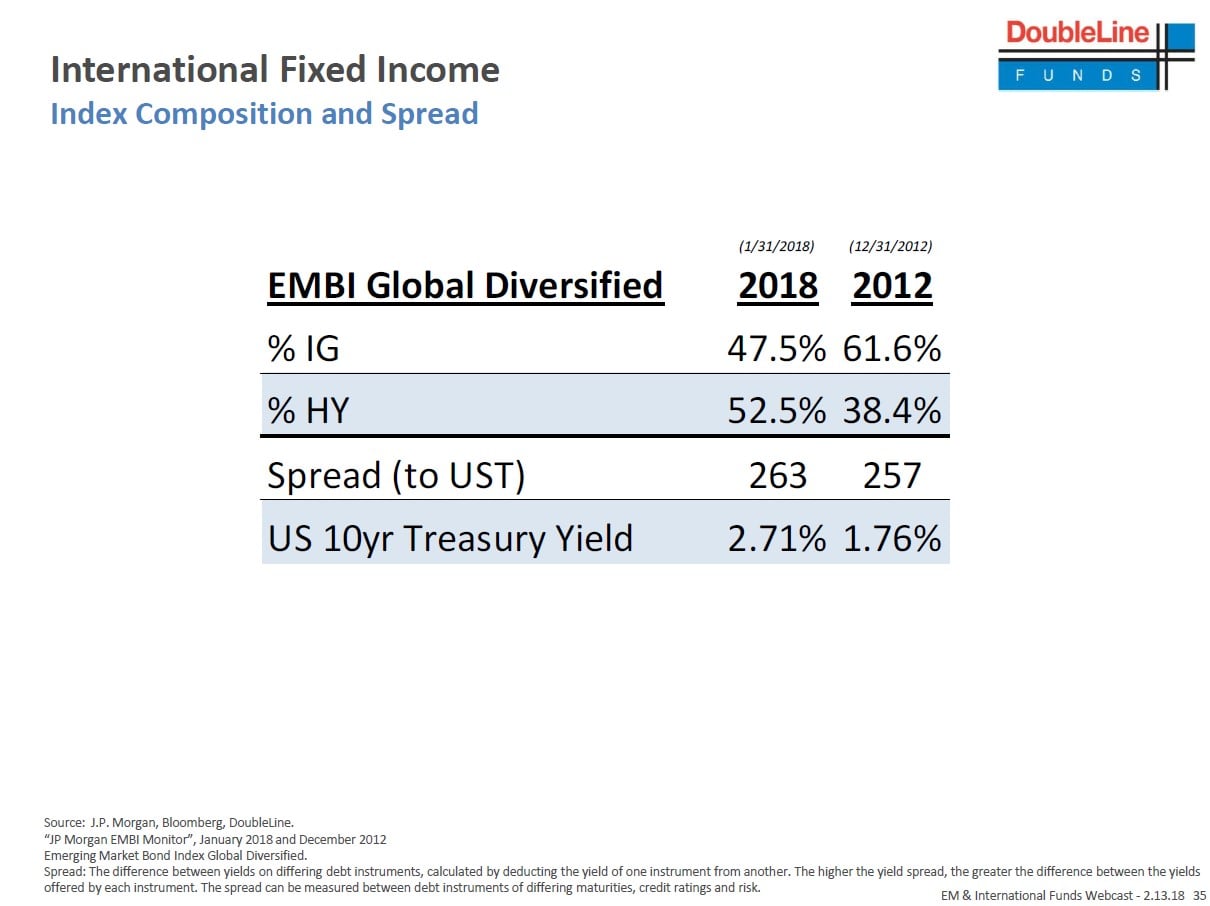

- Rates rose significantly Within Emerging Markets in 2013 the JP Morgan EM Global Diversified Index (the Index) saw spreads widen 50 bps relative to the U.S. Treasury (UST) from 256 bps to 308 bps.The Index returned -5.25% annually during 2013

- 2013 ended much differently than expected

- In late 2012, many strategists were predicting the market landscape of 2013 to be a continuation of 2012, and in a similar fashion, many strategists are predicting the market landscape of 2018 to be the same as that of 2017?

- DoubleLine EM Expectations

- We remain constructive on the asset class

- Fundamentals remain solid, but we are cautious about the market potential due to market euphoria and tight spreads

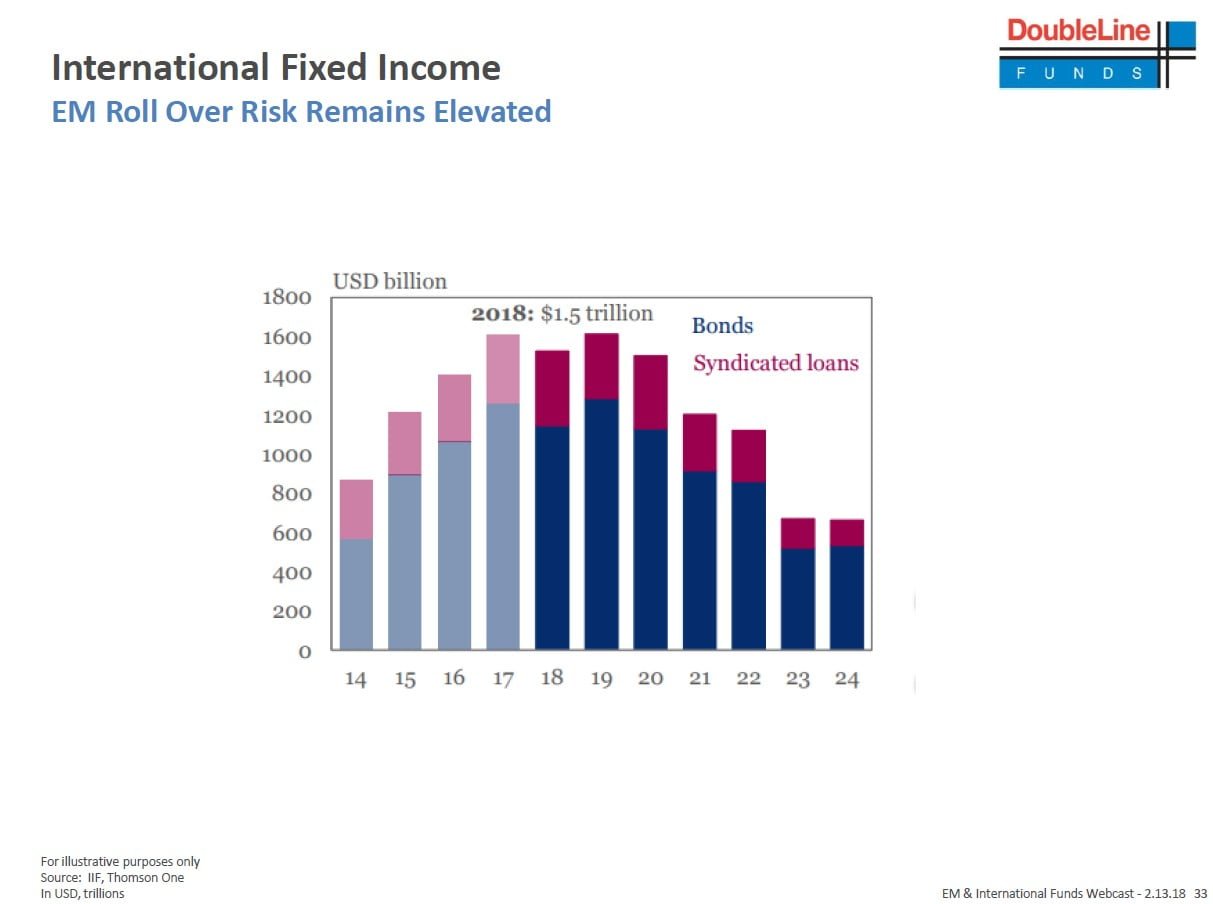

- We continue to evaluate the potential downside risks against the upside potential o High EM debt rollover expected through 2020

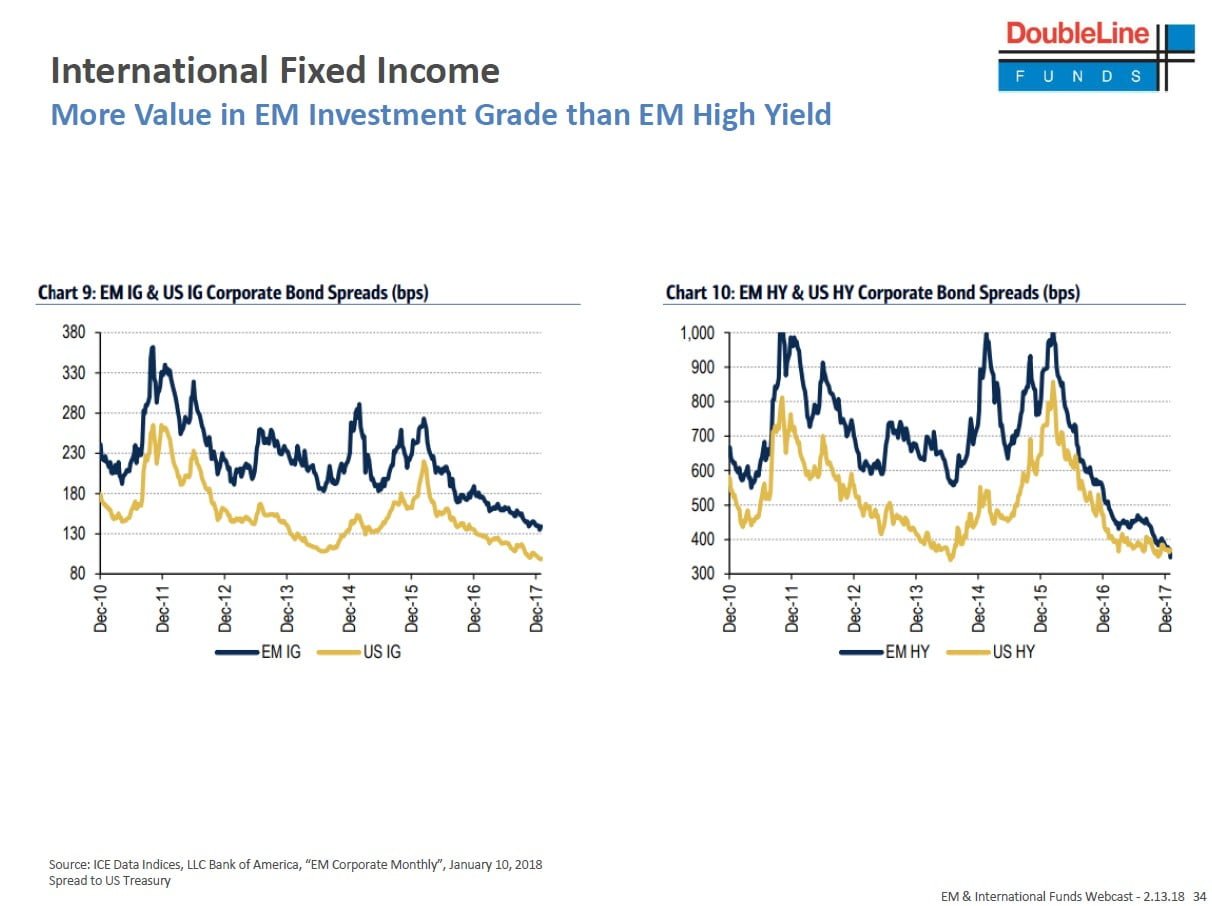

- EM High Yield (HY) spreads are tighter than U.S. HY spreads

- EM Investment Grade (IG) spreads are still showing relative value to U.S. IG spreads

- The combination of a likely supply decrease in 2018, rollover risk and tighter EM HY spreads relative to U.S. HY spreads lead us to believe 2018 does not show a lot of upside in EM debt, especially in the HY space

- The quality of the Index has declined since 2012. What is more concerning is investors are not being compensated for the lower quality via a higher spread (only 6 bps)

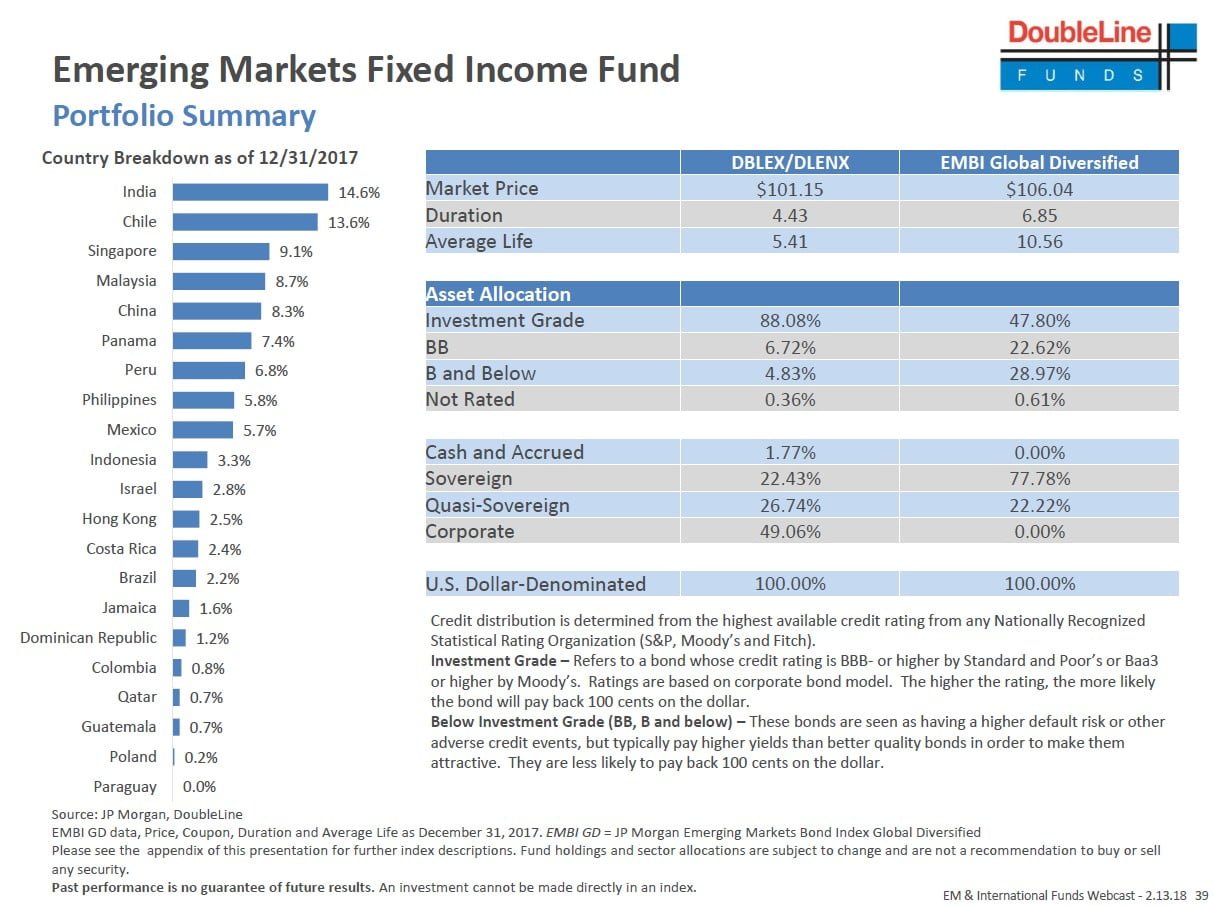

DoubleLine Emerging Market Fixed Income (DBLEX/DLENX) as of December 31, 2017

- Combining all of the previously mentioned factors and risks within the EM space along with the risks on the global macro landscape, the portfolio has been more prudently positioned through late 2017 and into 2018

- We have been migrating the portfolio up the credit curve toward higher IG names and shortening duration

- We would likely be buyers of riskier assets if there is a credit event or opportunities present themselves going positioned in higher quality names

- As a result, the portfolio has been overweight Asia versus Latin America (LatAm) and Africa

- 100% USD-denominated debt

- Fund positioning

- Top 5 countries: India, Chile, Singapore, Malaysia, China

- The Fund’s position in Asia grew from 33% as of June 30, 2017 to 52% as of December 31, 2017 and the Fund’s position in LatAm declined from 60% to 41% over the same time period - IG: 88% verses 48% IG in the JPM EM Global Diversified Index

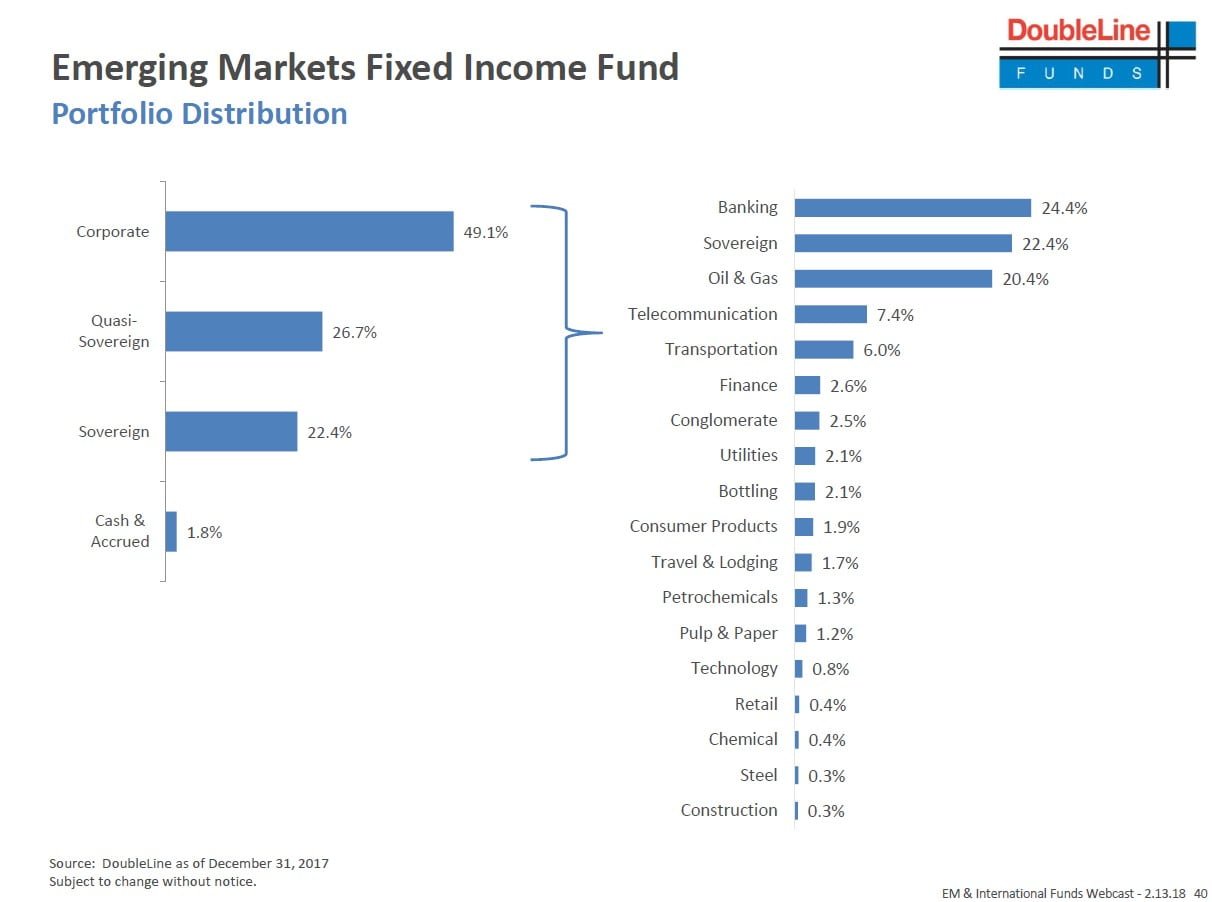

- Sector Breakdown:

- We have reduced Sovereign exposure, partly in order to reduce duration

- We have increased Corporate exposure, and exposure to the Banking sector

- Top 5 countries: India, Chile, Singapore, Malaysia, China

- Duration peaked in mid-2017 at 6.7 years, but ended January closer to 4.4 years

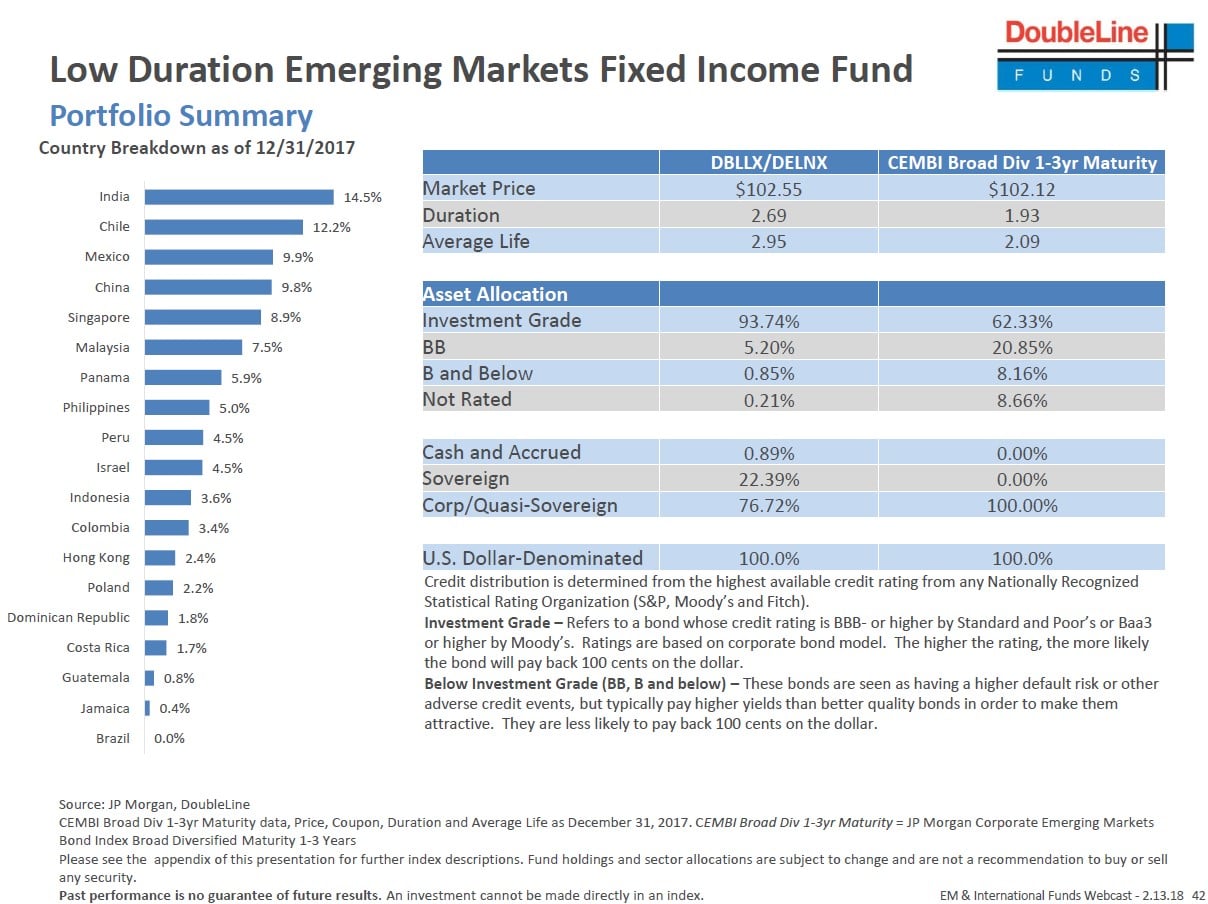

DoubleLine Low Duration Emerging Markets Fixed Income Fund (DBLLX/DELNX) as of December 31, 2017

- Fund Positioning

- Top 5 Countries: India, Chile, Mexico, China, Singapore

- Fund was overweight LatAm for first half of 2017 - 100% USD-denominated debt

- Top 5 Countries: India, Chile, Mexico, China, Singapore

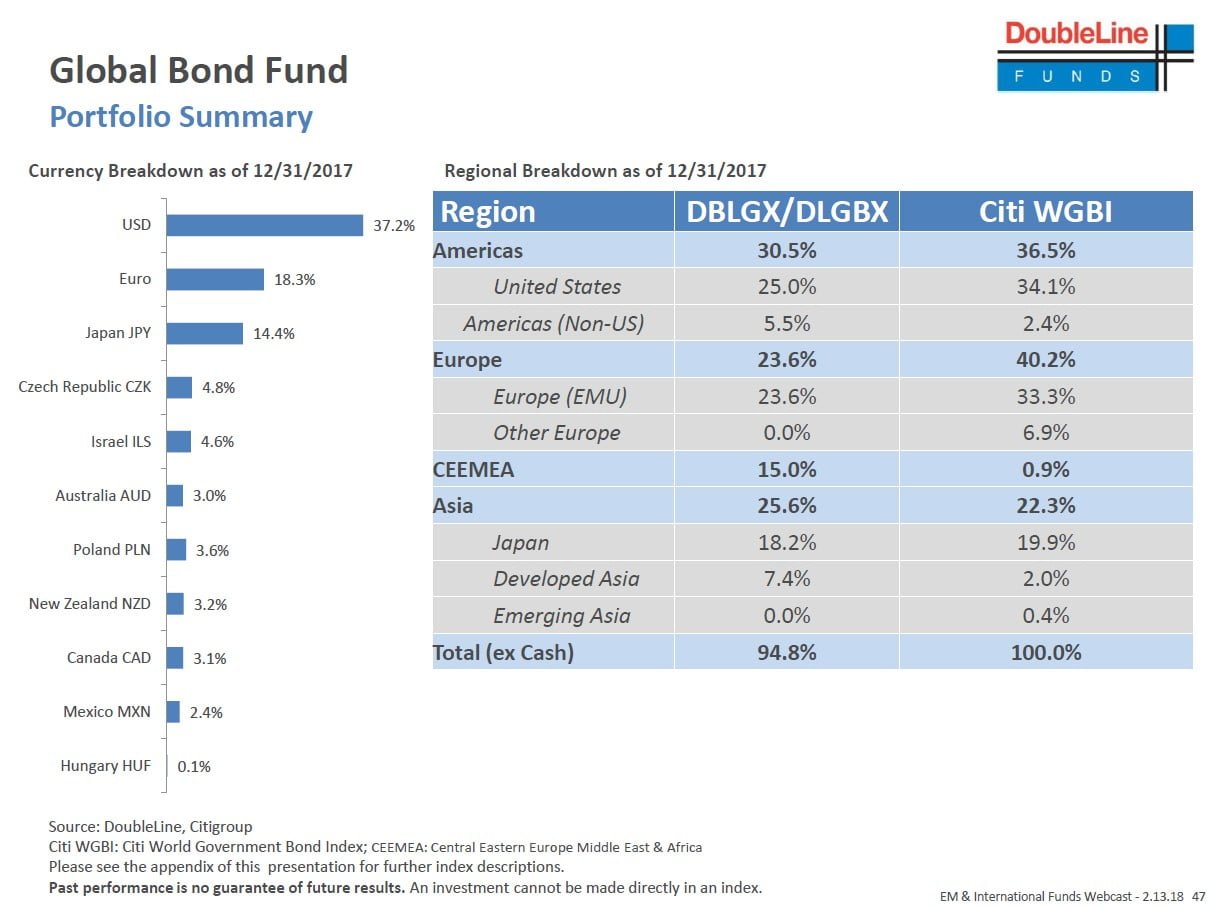

DoubleLine Global Bond Fund (DBLGX/DLGBX) as of December 31, 2017

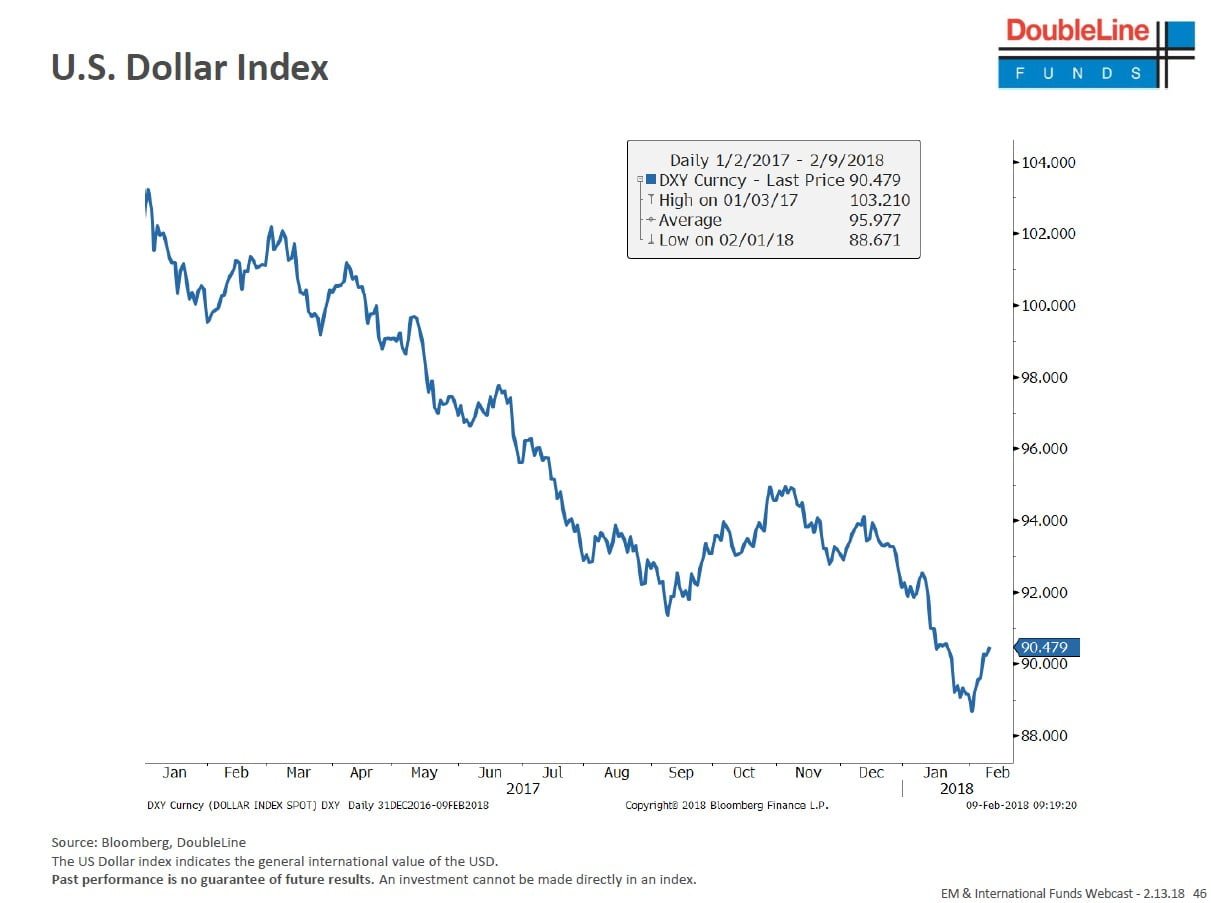

- The USD

- The Fund started 2017 short the USD and overweight non-USD bonds

- We started to hedge out the non-USD positions in September as we felt the USD move had become overextended and we thought that rates were going to back up. At the same time, we went long the USD and have remained long USD since

- We feel the USD tends to rally as U.S. rates go up, when U.S. growth tends to outperform the rest of the world, and during risk-averse time periods or when risk assets sell off

- We believe the current environment has shown those three circumstances, so we do not plan to enter into non-USD positions until we feel we are at a better level

- Europe Outlook

- The European Central Bank (ECB) has started to taper Quantitative Easing (QE) and is likely to discontinue it by the end of 2018 and potentially hike rates into 2019

- This should be supportive of Euro currency but could hurt rates. Thus, we are reducing our allocation to core Europe (i.e. Germany) and moving those allocations into periphery Europe (i.e. Portugal or Spain) and Central Europe, Middle East and Africa (CEMEA) credits

- We believe these curves will hold in better during ECB tapering and they have higher all-in yields than core Europe yields while maintaining Euro foreign exchange (FX) positioning

- The European Central Bank (ECB) has started to taper Quantitative Easing (QE) and is likely to discontinue it by the end of 2018 and potentially hike rates into 2019

- Japan Outlook

- We want to match the Citi World Government Bond Index (WGBI) weighting to Japan

- We believe the yield curve will remain pegged by the BoJ, at least for the near term, but the Japanese Yen provides a risk-off hedge to the portfolio should something go wrong.

- Japan has the second largest net international investment position

- When risk assets start selling, Japan will bring those flows back home which tends to appreciate the Yen

- Commodities Outlook

- A major theme for DoubleLine has been Commodities should have a good year in 2018

- The Fund has oversized positions in countries that are Commodity exporters like Canada, Australia and New Zealand, and we feel those currencies should perform as long as Commodities continue to perform

- A major theme for DoubleLine has been Commodities should have a good year in 2018

- Overall Global Macro risks

- Rising DM rates

- Slowdown in global growth

- Heavy political calendar

- Commodity shock

- Country-specific stories, i.e. Venezuela

- Risk of geopolitical events

- Global Macro Expectations

- Global growth to remain fairly stable

- Moderately higher DM rates

- Political risk to be generally digested and to continue to be reduced

- China expected to slow down, but remain stable

- Stability, and perhaps strength in Commodity prices

See the full slides below.