By Master Class Invest

No doubt you will have noticed that in the last week or so we've experienced a significant spike in market volatility. There's a common saying that markets go 'up the escalator, and down the elevator,' and that has certainly been evident of late. During the period of volatility we've witnessed stock markets being sold and bond prices falling, and through it all we've also watched investors all over the world react.

Historic correlations have also become unhinged, as the market's participants start to question the implications of global central banks normalizing interest rates. Whether this volatility will continue and the markets will decline further, no-one actually knows. But what is evident is that the market moves were largely unexpected.

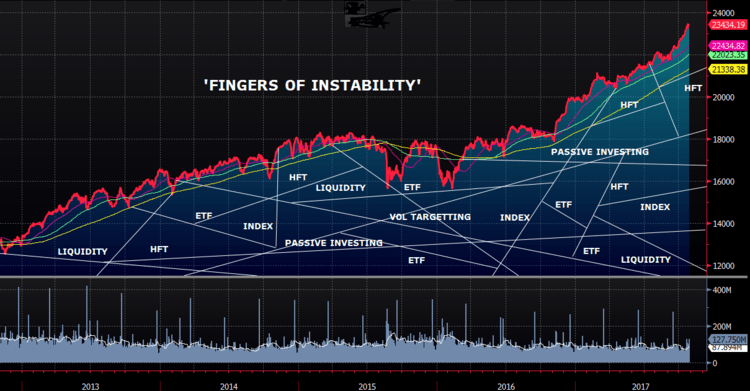

The recent blog post titled 'Fingers of Instability' highlighted the more recent changes in market structure that has created fragility in the system. As more assets are held by people with zero comprehension of what they actually own, it's no surprise volatility spiked when the unexpected happens. These investors have no idea of the underlying worth of their investments and therefore no price to anchor to. No price is too high or low for an index fund to sell or buy. And when there is fear they all try to run out the gate at the same time. Throw in HFT and momentum strategies and in the end you've got a recipe for absolute disaster. But while its a disaster for uninformed investors, its also a potential opportunity for unemotional investors who have done the hard work and can take advantage of indiscriminate selling.

So, given what has occurred in the markets of late, I thought it would be a good idea to revisit a few of the important lessons that emanate from all of this.

Common Sense - good investing requires common sense. Buying something that's expensive in the hope someone will pay more for it, is speculating, it's not investing. I can't see any rational reason why someone would think buying bonds as an investment makes any sense given ultra-low or negative yields . Historically bonds have provided a real return, but since the Financial Crisis bonds have moved from NOT providing a real return to in some cases giving a negative return. If you're holding to maturity you're going to be losing money after inflation in the first instance, and losing money full-stop in the second. That's an asymmetric bet the wrong way around.

Rear-View Mirror - Investors have a tendency to chase performance. One example of this is the bitcoin frenzy we've been witnessing lately. From time to time, I put a few things up on my Linkedin account, but if you follow it you'll note that I haven't written a lot about bitcoin as I don't see it as a legitimate investment. Its speculation, not an investment. I certainly have a view on the topic, but I'll also take note of the likes of Buffett, Munger, and Druckenmiller; they've been around the block a few times and their collective opinions are valuable to me. Despite my reticence to write about bitcoin, what's interesting is the number of my acquaintances who've asked me whether they should invest in it. And why do they care? Because it's gone up a lot, and they're wanting to chase performance. My Linkedin post on Bitcoin included a chart with a Warren Buffett quote on bubbles. It got 10,000+ hits.. that's an attention bubble right there!

Understand - if you don't understand something don't invest. Some investors learnt some tough lessons last week when the Inverse Volatility [XIV] ETF blew up. I'd say most investors in the fund were chasing performance. Selling volatility is a dangerous strategy if you don't know what you're doing and even more so when you don't know how the fund you're investing in works.

Expect the Unexpected - Don't set your portfolio up for that perfect outcome. Winning in the investment game is not losing. In a bull market all you need is an index fund. The difficult part is timing your exit. And no one knows when a market turns; they can and will turn on a dime. Don't be disappointed in lagging a bull market, it's often the price to pay for admission to long-term market-beating results. It's the outperformance in down markets which drive long term gains. You can't run a portfolio optimized for a bull market that will perform well in a down market. It's important to stress test your portfolio. How will the different assets perform under alternative investment scenarios?

I can't tell you with 100% conviction where the markets are going and neither can you. But you can give yourself the best chance of attractive long term returns by using common sense, understanding what you own and not chasing performance, and then building a portfolio of quality companies that are likely to continue growing over the next five or ten years. If you remain unemotional, focus on the intrinsic worth of your companies rather than market gyrations, the renewed increase in volatility is an opportunity, not a threat.