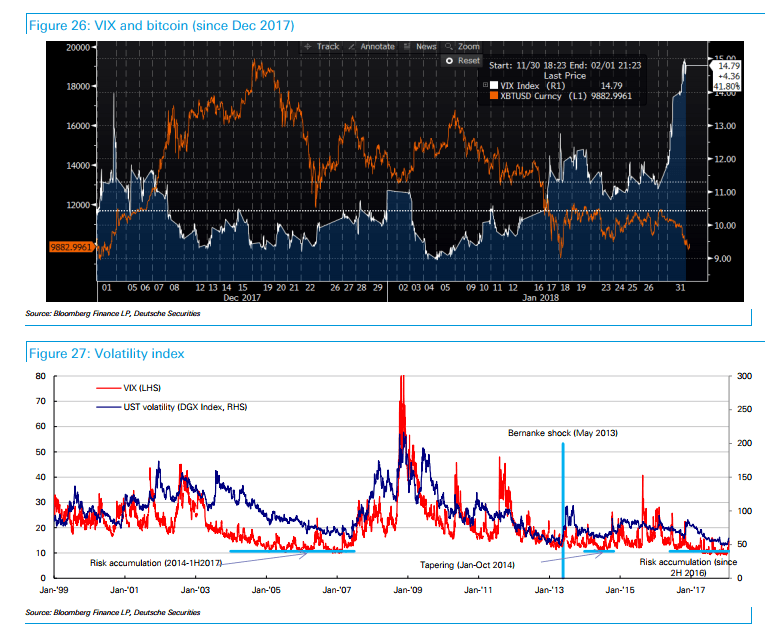

With the stock market gaining steam to the downside near the 2 PM EST, and Bitcoin, which has been touted as a safe haven also down by 6.74% on the day, Deutsche Bank Japanese research analysts Masao Muraki and Hiroshi Torii see a “divergence from Goldilocks.”

Bitcoin sell-off is the ultimate example of a value re-adjustment

Perhaps the end of a speculative bubble might first be seen in Bitcoin, which has been selling off strong today.

Japan is the nation that Muraki had credited with “holding up” the Bitcoin market. But since futures were added to the professional trader’s toolbox in December, the strength of those “holding up” the market might be getting tired.

On a day when Nouriel Roubini calls Bitcoin the “biggest bubble in human history,” the market for an asset without a fundamental value anchor is down yet again, near $8,525. It seems like a long time ago when the market had topped out at $19,458 on December 11.

While making a call on a Bitcon crash might seem a little redundant after a market is down by more than half, the bigger risks come from an asset price adjustment all around – particularly in the interest rate market and a time at which there is selling in Japanese stocks.

Muraki notes the performance drivers, with a particular focus on quantitative withdrawal:

The key drivers of US long-term rates appear to be (1) concerns about inflation due to the passage of the US tax reform, trade policies preferring weaker dollar, and rising oil prices; and (2) fears about the collapse of the UST bubble due to expectations for Japan, the US, and Europe to taper monetary easing at a faster pace, and media reports about UST sales by the People’s Bank of China. However, inflation indicators have yet to recover. Without a recovery, we think Japan and Europe and the US will find it difficult to taper monetary easing, making a prolonged increase in long-term rates unlikely.

Yields are causing the selloff as concern that Japanese central bankers are losing control weighs

To understand the sell-off in stocks is to recognize what is driving bond market yields higher, which is a sinking US dollar, a move that makes exports more competitive and is viewed as an economic accelerant.

UBS analyst Art Cashin told CNBC higher yields were playing a part in stocks moving lower with FANG stock price volatility, but also the release of the “Republican memo” might also be sowing seeds of concern. “The great rally suddenly might be under question,” he said, pointing to “landmines.”

“Is this an inflection point?” Cashin wonders?

Some of the market concern might be due to central bank hiccups around the world in tightening their balance sheet diet. “Just as they are worried about yields here,” the New York area-based Cashin said, “There are some problems with central banks elsewhere,” with bond yields in Japan have been moving up despite central bank efforts to tame them.

This is an issue that, likewise, Muraki sees all too clearly:

The absolute prices of Japanese financial stocks (aside from non-life insurers) have mostly been defined by Japanese and US interest rates, forex, and volatility. The recent correction in absolute share price for financial stocks appears to be due to yen appreciation and rising volatility. A ¥10 stronger yen weakens stock prices by 9.1% for banks, 7.8% for brokers, 6.0% for leasing firms and 5.8% for life insurers. Should the BoJ lower 10y rates 10bp to prevent yen appreciation, life insurer stocks would fall 11.8% (5.8% if 20y rate lowered by 10bp), brokers 8.8%, and banks 6.0% (Figure 22). A 10pt rise in Nikkei Stock Average Volatility would depress life insurer stocks by 13.9%, banks by 10.3%, and brokers by 5.1%

The world is globally and digitally linked as never before in history. When buyers catch a cold in one region, the sneeze occurs halfway around the world.