SUMMARY

- Investors can directly access factor returns via ETFs in the US & futures in Europe

- However, neither of these come without some investor concerns

- Realised returns differ substantially from theoretical returns

INTRODUCTION

Despite factor investing having gained immense popularity in recent years, it has been relatively difficult for most investors to directly access long-short factor returns as portrayed in academic and quantitative research. Smart beta ETFs have flourished, but these are long-only products with excess returns that differ from those of the long-short factors (please see our report Smart Beta vs Factor Returns). However, in recent years a few product providers have launched products that allow most investors to gain more direct access to factor exposure. In this short research note we will analyse factor ETFs in the US and factor futures in Europe.

METHODOLOGY

We focus on factor ETFs in the US from AGF Management Limited and factor futures in Europe from the Eurex Exchange. The factor data used in benchmarking the investible products is created by constructing long-short beta-neutral portfolios of the top and bottom 10% stocks ranked by the factors. Portfolios rebalance monthly and include 10bps of transaction costs. Only companies with a market capitalisation of larger than $1 billion are included.

FACTOR ETFS IN THE US

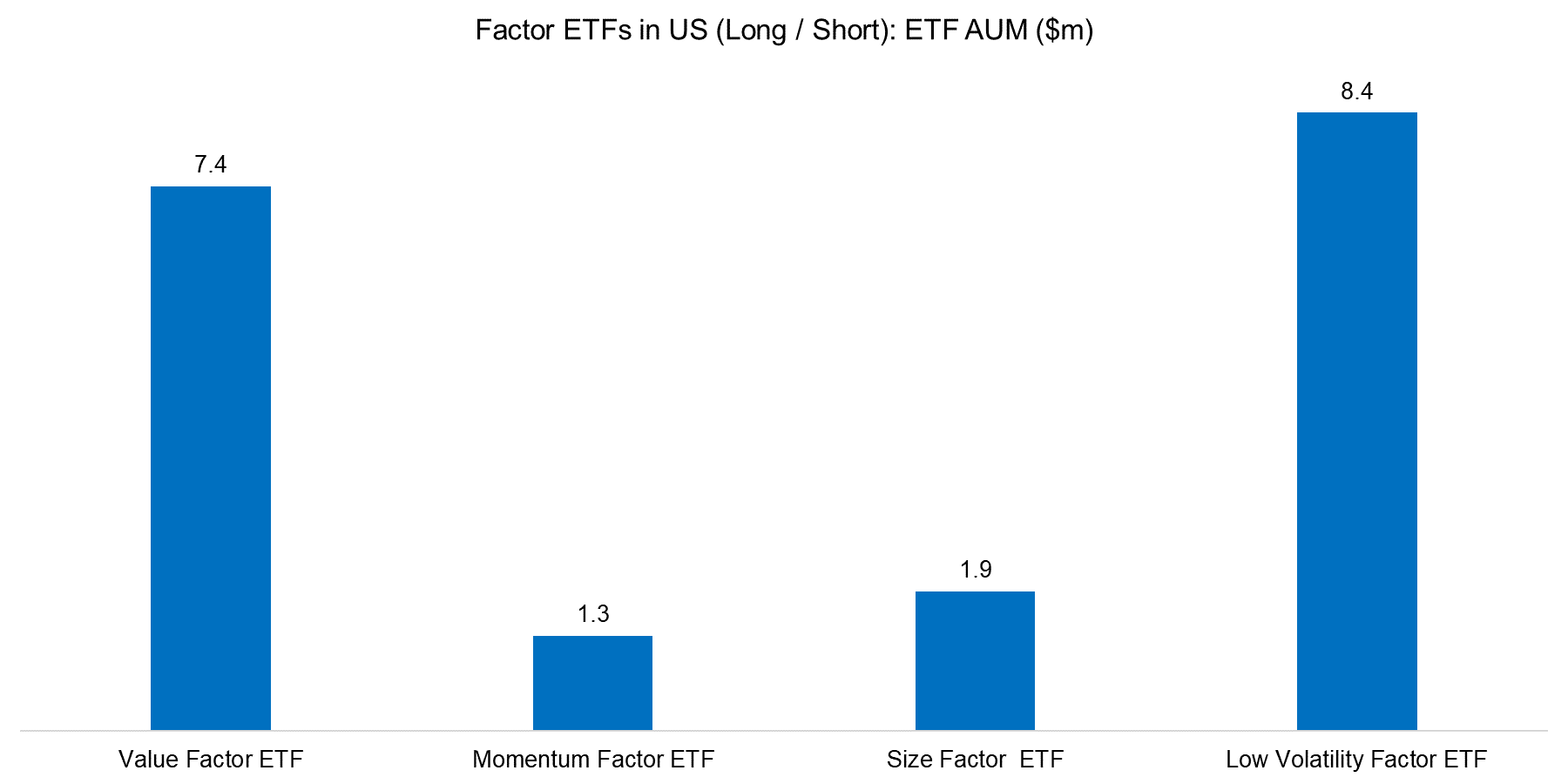

The factor ETFs in the US are available for the Value, Momentum, Size and Low Volatility factors (we ignore the Dividend factor ETF as it has less trading history). They are constructed as dollar-neutral long-short portfolios and rebalance monthly. The ETFs have been launched in 2011 and offer investors the opportunity to directly harvest factor returns via easily-traded securities. Unfortunately the assets under management are below $10 million for each of the ETFs, which can be seen in the chart below. At that fund size the expense ratios are exceptionally high, which deters investors. However, the ETF provider has agreed to reimburse fees and keep the ratio from exceeding 0.75% per annum, which is competitive for a long-short product.

Source: AGF, FactorResearch

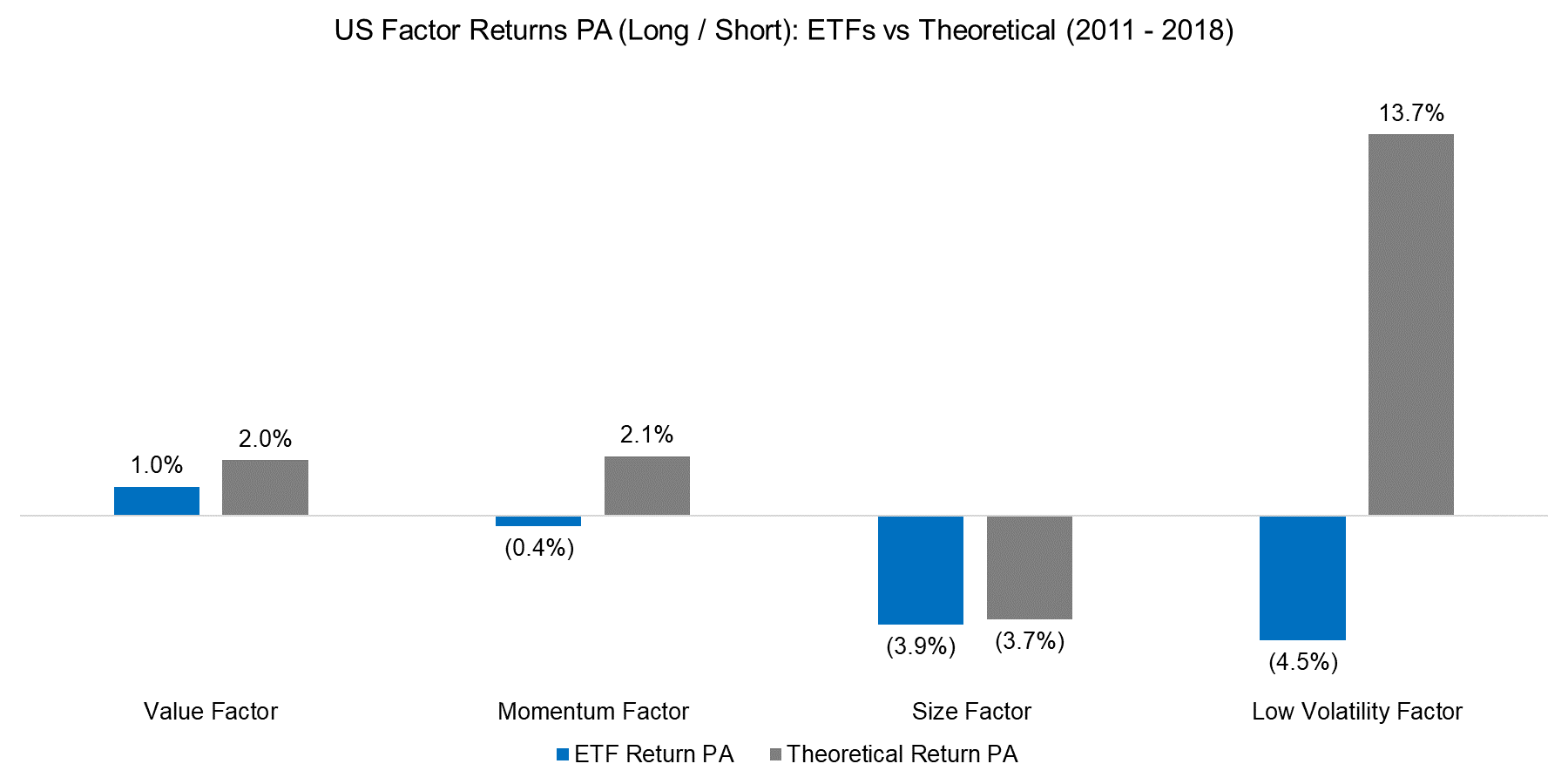

Given that the ETFs have been trading since 2011, we can benchmark these against the theoretical returns, although different factor definitions have to be considered. In the chart below we can see that the performance of the ETFs and the theoretical returns are somewhat comparable for the Value and Size factors, but quite different for Momentum and especially for the Low Volatility factor. The significant difference for Low Volatility can be explained by a divergent portfolio construction as the ETF portfolios are created dollar-neutral compared to beta-neutral portfolios for our factors. The theory behind the Low Volatility factor assumes that stocks with low volatility or beta have higher-risk adjusted returns than stocks with high volatility or beta. If the long and short portfolios are not adjusted for the different betas, then the factor will have structural negative beta, which tends to be punishing in rising markets.

Source: AGF, FactorResearch

FACTOR FUTURES IN EUROPE

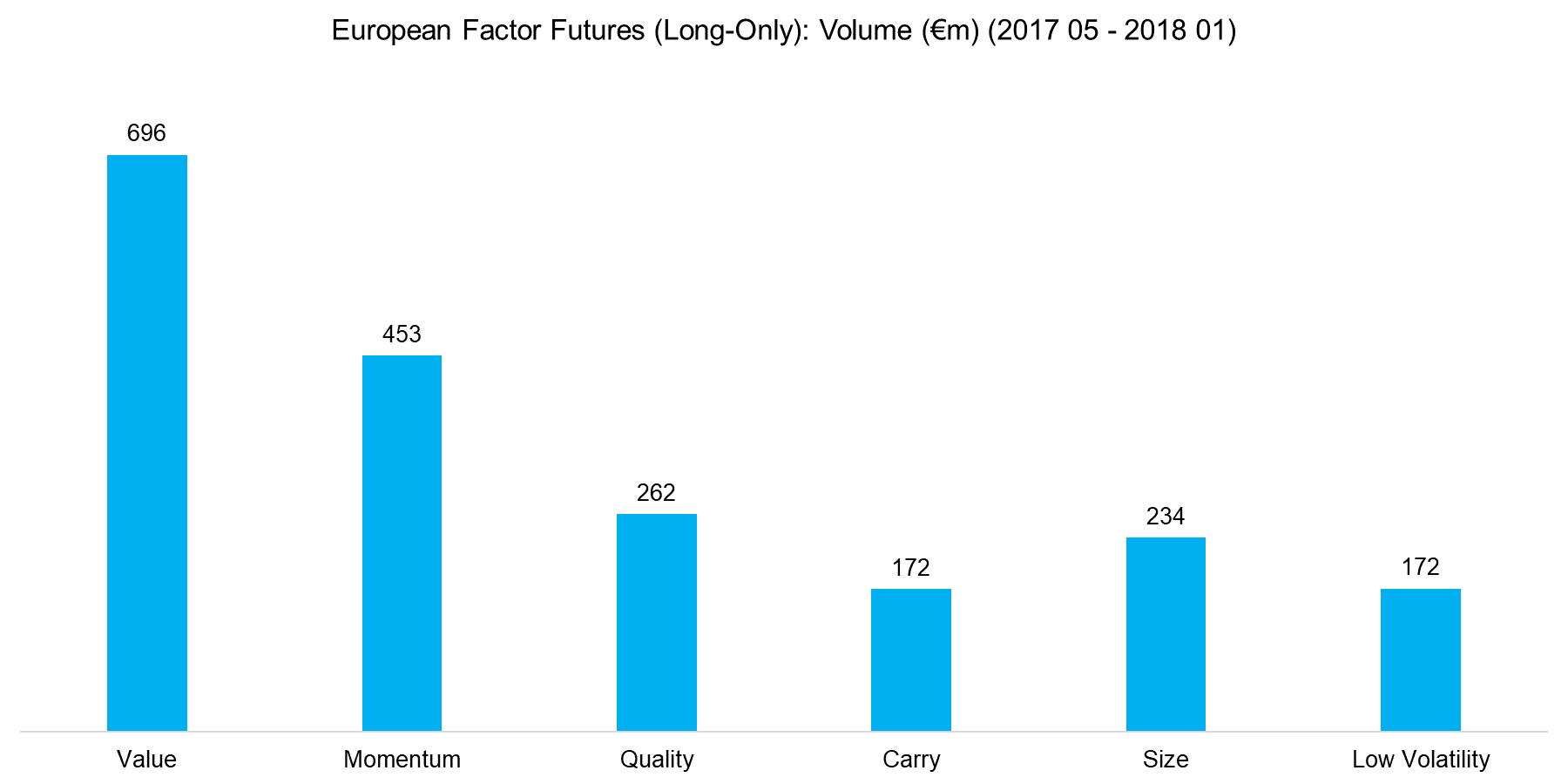

The Eurex Exchange launched factor futures for the STOXX Europe 600 index in 2017, which are long-only products and can be seen as an alternative to smart beta ETFs. The chart below exhibits the volume traded in the contracts in slightly less than a year, which shows a healthy volume. It also highlights that investors had a clear preference for the Value and Momentum factors in 2017 while the Carry and Low Volatility factors were of lesser interest.

Source: STOXX, FactorResearch

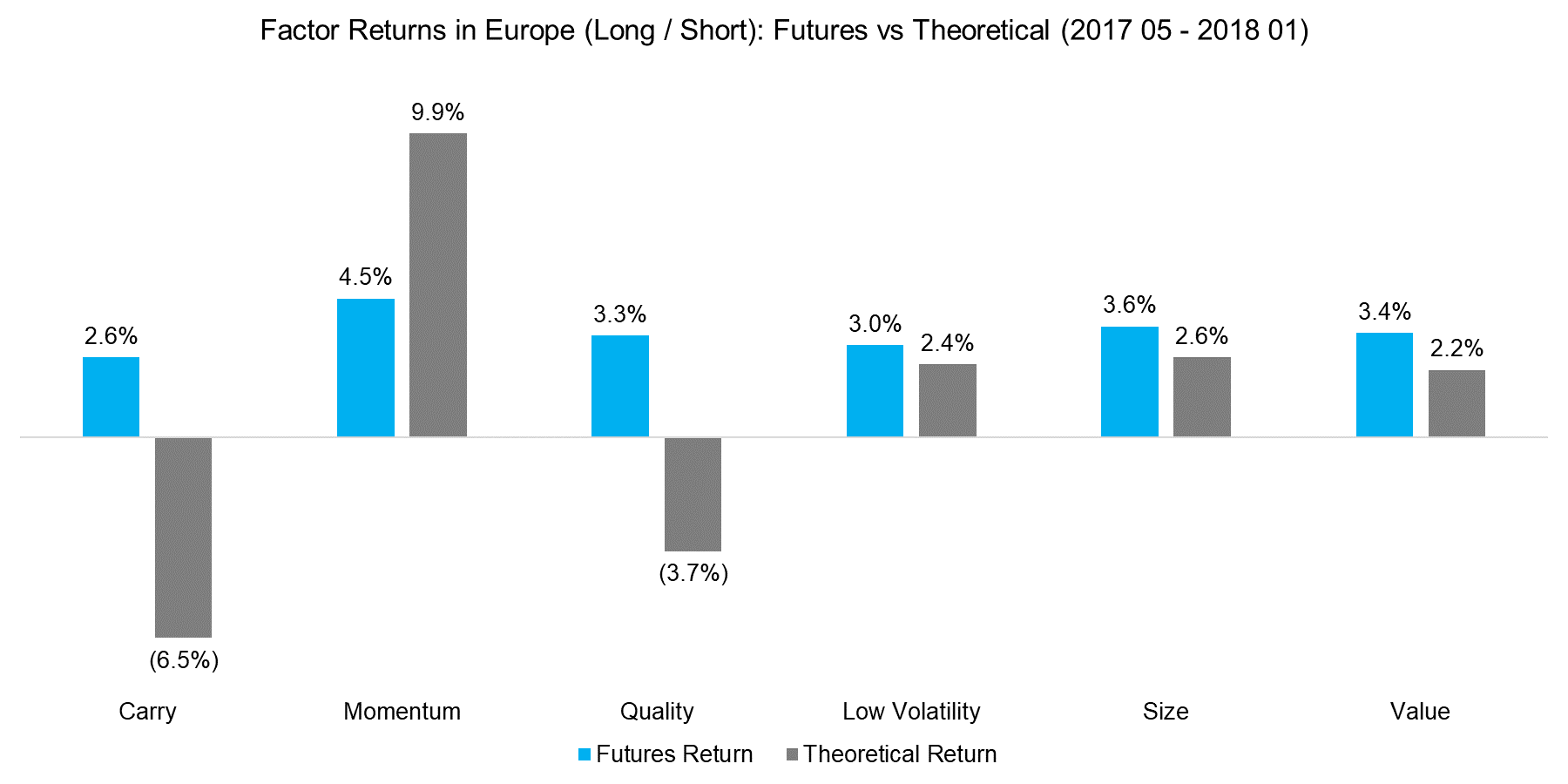

Investors can relatively easily create a long-short factor from the long-only factor future by shorting the STOXX Europe 600 index future. The chart below shows the resulting excess returns from the long-short futures portfolios compared to theoretical returns. We can observe significant differences, which are likely explained by different factor definitions. It is worth highlighting that the excess returns from the factor futures have been all positive over the time period, which is slightly unusual given that some of the factors, e.g. Value and Quality, tend to be negatively correlated.

Source: STOXX, FactorResearch

FURTHER THOUGHTS

This short research note highlights how investors can directly access long-short factor returns via exchange-traded products, albeit with some concerns. Investors can partially access factor returns via smart beta ETFs, but it is not particular easy to distinguish the beta from the factor returns. If the smart beta ETF performance was positive yesterday, was that due to the market or the factor? Investing should not be so complicated and investors should have the opportunity to buy long-short factor exposure from various providers as efficiently as long-only exposure.

Article by Factor Research