Ten years ago, Warren Buffett made a decade-long wager on an S&P 500 index fund — and emerged triumphant. But would we make a similar bet in today’s market?

Check out our H2 hedge fund letters here.

In late 2007, Warren Buffett made an interesting wager with Ted Seides, who was president and Co-CIO at Protégé Partners at the time. The wager pitted an S&P 500 index fund against a hand-picked assortment of pooled hedge fund investments (commonly known as fund of funds). It measured the total return (after fees) over the subsequent decade. Of course, Buffett backed the index fund. The measurement period of the wager officially began January 1, 2008 and came to an end on December 31, 2017. The widely reported result was a triumph for the index fund, and the wager amount went to the charity of Buffett's choice.

I’ve been musing about this wager since the new year began. Many hail the result as a victory of passive investing over active investing — but I believe they’re mistaken. I can’t help but wonder if a similar 10-year wager were offered today, whether it would be better to take the opposite (or at least a modified) position as Mr. Buffett.

The Buffett wager was not a test of active versus passive.

While we don’t have a list of the precise fund of funds that competed against the S&P 500, I feel safe making two assumptions. First, the collection of fund of funds was probably not cheap to own, with fee arrangements like “two and twenty” (2% management fee and an additional 20% of any profits earned), which was very common in early 2008. Second, by the very nature of a hedge fund (emphasis on the word “hedge”), I’m guessing the fund of funds collection did not behave with perfect sensitivity to the equity market. For many investors, the goals of a hedge-fund-style investment include downside risk control and returns that do not correlate meaningfully to traditional market returns. In technical terms, a beta to the S&P 500 of roughly 0.3 would be typical for such an investment.1 If we look at it this way, Buffett’s wager was not so much a contest between active and passive investing, but rather a competition between equity market returns on one hand and high fees combined with low equity market sensitivity on the other. A fund of funds would struggle to keep up with the stock market return if the stock market rose meaningfully, which it almost always does on a 10-year horizon. Also important to note: the wager only considered absolute return, not risk-adjusted return.

The same bet against the S&P 500 remains unattractive. Even today.

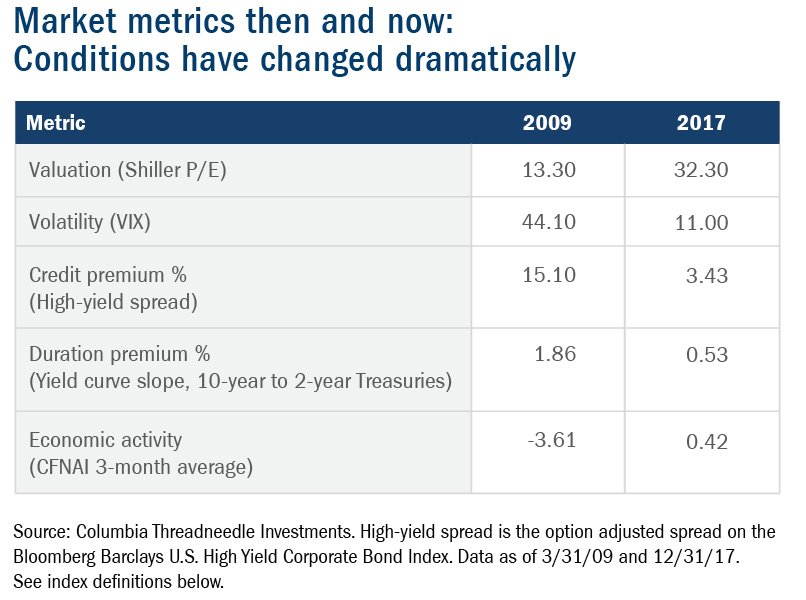

Given current market conditions and valuations, you might be easily tempted to take the other side against Buffett’s original wager for the next 10 years. But let’s compare today’s market environment to the S&P 500 lows in 2009. If you believe that buying and holding the S&P 500 in March 2009 was well timed (and let’s agree, it was), we might gain perspective by comparing relevant metrics with their levels back then:

The comparison is striking. In 2009, the U.S. economy was very weak, equities were cheap and unloved, credit markets were distressed and investor anxiety was high. The reversal of these conditions facilitated a long bull market. Obviously today’s conditions bear little resemblance to those in place at the beginning of the bull market. But while we feel secure in positing that we are now closer to the end of the bull run than the beginning of it, it doesn’t make automatic sense to bet against the S&P 500 for the next 10 years. An important detail from Buffett’s bet illustrates the importance of a decade-long investment horizon. The wager commenced at the end of 2007, not the beginning of 2009, and by some measures the prospects for equities seemed bleak then. In fact, the S&P 500 lost nearly half of its value in the first 15 months of the wager. Despite the significant early setback, that ground was more than recovered by the end of a decade. The lesson? Temper the bearish instincts stoked by the recent data in our exhibit above, especially in light of a holding period of that duration. Even today, we consider it improbable that a low beta hedged investment would deliver a higher return than the S&P 500 over a 10-year holding period.

A different approach to betting against the S&P 500 makes more sense.

During the past decade, the magnitude of U.S. equity outperformance over other asset classes defies intuition. A diversified portfolio did not stand a chance against the venerable index.

The U.S. dominance raises the question of whether the United States offers a unique business-friendly environment that allows persistent advantages for corporations. If so, then perhaps the performance spread is justified and may even be repeated. On the other hand, U.S. equities may have become relatively overvalued during the past decade. Existing forces could level the corporate playing field over the next decade. I believe the truth lies between these two extremes; if this is true, then I would bet on diversification for the next 10 years.

What kind of wager would work today?

While I wouldn’t wager against the S&P 500 on Buffett’s original terms, I would accept a 10-year wager against the benchmark today, but with different parameters. Here’s how I believe a portfolio competing with the S&P 500 (let’s call it a “rival portfolio”) could win that bet:

- First of all, to level the playing field for this wager, the rival portfolio must be constructed to have a beta of 1.0 to the S&P 500.

- The rival portfolio could use numerous asset classes beyond the S&P 500, including some that are more aggressive, like small-cap and emerging market stocks, and some that are less aggressive, like investment-grade bonds and value stocks.

- We’d calibrate our beta by permitting this portfolio to use leverage, so that its more diversified starting point doesn’t encumber returns.

- It would allocate to both active and passive strategies, with the active allocation targeting either less efficient asset classes (such as high-yield bonds or international equities) or time-tested active managers who offer a compelling, fee-adjusted value proposition.

- We would establish a strategic asset allocation and rebalance to those target weights at the end of each year.

In effect, regardless of whether the S&P 500 delivers high or low returns over the next decade, we would expect the performance of the rival portfolio to differ from the S&P 500 because of the relative performance of the other asset classes we’ve included and through the security selection of our chosen active strategies. When we consider the extraordinary margins of the S&P 500’s outperformance over other asset classes like international stocks, emerging market stocks and commodities over the last decade, we don’t mind being exposed in those directions for the next 10 years.

Any takers?

Article by Jeffrey L. Knight, Columbia Threadneedle Investments

{kind=link}