| Pennywise: | Tasty, tasty, beautiful fear. |

| … | |

| Eddie: | Okay, so let me get this straight. It comes out, from wherever, to eat kids for, like, a year, and then what? It just goes into hibernation? |

| ― It (2017) | |

Even at eleven, he had observed that things turned out right a ridiculous amount of the time.

― It, Stephen King (1986)

Same with markets. Things turn out right a ridiculous amount of the time. Pennywise only shows up once every 27 years. Should we be scared about his market equivalent?

Like many children with over-developed imaginations, I was always scared of things that go bump in the night. To this day I remember vividly the events (all fictional, of course) that frightened me so badly, like this scene from the 1979 made-for-TV movie of Stephen King’s Salem’s Lot, where little vampirized Danny tries to get his friend to open the upstairs window and let him in. You see, vampires have to be invited into your house. You have to give them permission to destroy you.

Hold that thought.

Anyway … as a child, I convinced myself that I could keep myself and my family safe from these malevolent forces and evil eyes if only I surrounded myself with the proper talismans (mostly stuffed animals, arranged just so around the bed) and said the proper words to God before going to sleep.

And it worked! This was classic magical thinking, just like that used by so many of our smartest and most powerful adults to protect us from the malevolent forces of economic recession and political decay.

I’d love to say that I’ve outgrown these fears that I know are irrational, but the truth is that I still surround myself with protective talismans and carry them with me wherever I go … a couple of lucky pennies, sure, but also a lucky dime (h/t Scrooge McDuck); one of the many chestnuts that I’ve rubbed between thumb and fingers till it’s oiled black and smooth, thinking this was my uniquely private charm until I recently found a well-worn chestnut hidden away in my grandfather’s rolltop desk; fortunes from cookies I ate 20+ years ago; my half of the turkey wishbone from this Thanksgiving, where my wife and I always not-so-secretly try to let the other win; an ancient post-it note wishing me luck, scribbled by one of my kids not for any particular reason, but just because. Powerful magics, all.

I’ll bet any amount of money that everyone reading this note has their own protective talismans. Maybe not as over-the-top as me, but you have them. This has always been my can’t-miss Turing test — the question you ask of an intelligence you can’t see to determine if it’s human or machine — what’s your talisman? What’s your charm of protection or luck? Every human being has a talisman. No machine would. It’s like asking a computer what mnemonic device it uses to remember something like the colors in the spectrum of visible light … the name Roy G. Biv has no meaning to a non-human intelligence other than as a curiosity of a less-capable species.

In investment and allocation circles, we have a name for these magical protections against spooky market forces that go bump in the night. We call them hedges. Now I’m not talking about hedge funds per se. I’m talking about the ad hoc hedges used by naturally long-only allocators like foundations and endowments and pension funds and big family offices. I’m talking about the ad hoc hedges used by naturally long-only investors like everyone with an IRA. I’m talking about how everyone reading this note has, at one time or another, gotten scared about markets and decided to hedge their professional portfolio or personal account with something that will make money if markets go down. Not as part of a considered review of risk tolerances and return projections and portfolio convexity (whatever THAT means). Not as part of an intentional portfolio that might include a long-volatility manager or a dedicated short fund. But just because we’re scared of something going bump in the night, and we need a talisman to ward off the bogeyman.

The most common of these casual hedges, the investment equivalent of a lucky penny, is the put option, and its most common expression is the put spread.

Quick review! A put is an option where you’re betting on whether the underlying thing, say the S&P 500, will go down below a certain price level before the expiration date of the option. So if I buy a put option that’s “struck” at a price level 5% below where the S&P 500 is today, and that option expires three months from today, then in three months my put option will only have value if the S&P 500 is at least 5% below its current price. The farther below that 5% strike price, the more money the option is worth.

A put spread is when I both buy AND sell a put option. Slightly different put options, of course, otherwise I’d just be buying and selling the same thing, but the difference between the two options — either in expiration time or (more commonly) the strike price — is the “spread” that I’m now betting on. So let’s say I bought a three-month put option struck at 5% down on the S&P 500 and sold a three-month put option struck at 15% down. When those options expire, I’ll make money on the put I bought if the S&P 500 is down at least 5%, and I’ll make a little money on the put I sold (limited to the price someone paid me for the option in the first place) if the S&P 500 avoids being down more than 15%.

Why would I do this complicated little dance? I do it in order to reduce the net cost of the put option I’m buying (the one struck at 5% down in this example). I want to buy some “insurance” on my portfolio that will pay off if the market is down more than 5%, and I can reduce the cost of buying that more-than-5%-decline insurance policy by selling someone else a more-than-15%-decline insurance policy. I mean … yeah, I’m scared of a 5% bogeyman attacking the market, but a 15% bogeyman? In the next three months? C’mon, that’s crazy talk. I’m not THAT scared.

As you can imagine, there are a zillion different variations on the put spread theme, depending on how scared I am and what I’m scared about. As you can also imagine, selling these put spreads to naturally long-only investors is a lucrative business for Wall Street, the bread and butter of equity derivative desks everywhere.

Again, I want to make clear that I’m not talking about the Street’s interaction with professional investors where options trading is part and parcel of their particular strategy. If you’re a BMW salesman, do you make your money by selling to a guy who owns a limo service and knows everything about the car business? No, of course not. You make your money by selling (or better yet, leasing) a new vehicle every three years to the doctors and lawyers and financial advisors who love their beemers. They’re not dumb guys and you’re not fleecing them (or else they’ll try a Mercedes for a change), but it’s not their business. This is where you make your margins. It’s exactly the same thing with the Street and selling portfolio hedges to naturally long-only investors.

Here’s the other similarity between luxury car sales and portfolio hedge sales. When you step back for any sort of a long-term view, is there really a meaningful difference in the transportation utility between a new BMW and a used Chevy? Of course not. There’s a personal utility I get in driving a BMW. My dad bought a BMW 1600 (the cheaper cousin of the 2002) in Birmingham freakin’ Alabama back in 1972 when BMWs were economy cars. I learned to drive a stick shift with that car. That car would flat-out FLY. It connects me with my father, gone 20 years now, and my own youth to own a BMW. So you’re damn straight I’m going to keep driving one. But I don’t own a BMW because it improves the Sharpe ratio of my transportation portfolio. I own it because it’s a powerful talisman for my personal life story. It makes me feel better about myself.

This is the reason why so many naturally long-only investors have paid for billions of dollars in ad hoc portfolio hedges, mostly in the form of put spreads, over the years. Not because these hedges have improved the risk-adjusted returns of their portfolio — decidedly on the contrary, in fact — but because they make long-only investors feel better and more secure about their portfolio. Ad hoc portfolio hedges are a crucial part of the STORY we tell our investment committees — either an external committee or, more importantly still, that internal investment committee we all carry around inside our heads — about how we are ever-vigilant against the monsters lurking just beyond the castle walls.

And it works! Not in an economic sense, of course, but in the powerful psychic benefit it provides, like me as a child arranging the stuffed animals around my bed just so, or me as an adult driving a BMW.

But here’s the thing about our adult talismans — they’re not cheap. Sure I might not care about the premium I pay to drive a BMW when times are good, but I can tell you from experience that I care a lot if my annual income takes a big hit. Talismans and charms are great for the psychic benefit they provide, and god knows I’m all about psychic benefits, but if it’s that or paying the mortgage …

I think that naturally long-only investors are now abandoning their portfolio hedges, because they can no longer easily afford the psychic benefits of these expensive adult talismans.

The investment returns of so many naturally long-only investors have been so disappointing for so many years (in relative terms if not in absolute terms) that it is harder and harder to justify the very real cost of putting on ad hoc portfolio hedges. If you don’t keep up with the Joneses in the investment returns you provide your client, external or internal, you will be fired. If you’re a good story-teller, that will buy you more time with your client than if you’re a poor story-teller, but it’s only a matter of time. You. Will. Be. Fired. In times like this, psychic benefits go by the wayside, and I think this is creating a big shift in the behavioral structure of markets.

I don’t have any proof-positive charts to show you that naturally long-only investors (who control the vast majority of financial assets in the world, btw) are now changing their long-held behaviors by abandoning ad hoc portfolio hedges. I have plenty of anecdotes and stories, and a couple of suggestive charts, but like all big shifts in investor behavior this is a slow burn that won’t be obvious until it’s already happened. If I’m right, though, this is a sea change in the way that the game of markets is played, with important implications for anyone who cares about playing the players and not just playing the cards.

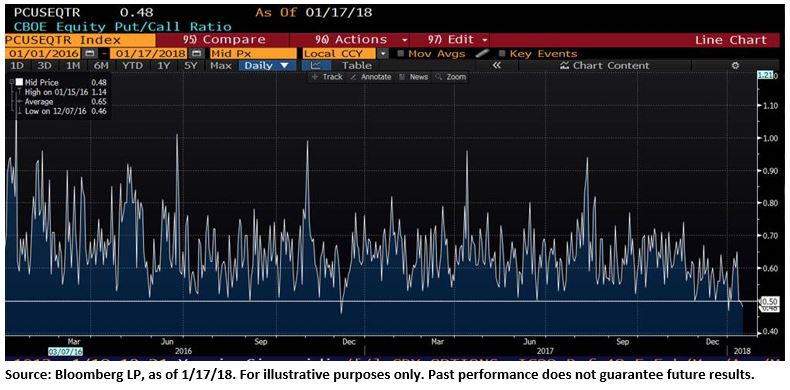

Here are two charts that suggest a behavioral shift.

First, this chart (h/t Joe Gulotta) shows the ratio of outstanding equity put options to call options on the Chicago Board Options Exchange (CBOE), the largest options exchange in the U.S. I like looking at the ratio of puts to calls because it’s not impacted by the overall level of options usage in and of itself. Whatever the overall option activity might be, this ratio is isolating how many investors are participating in negative markets bets (puts) versus positive market bets (calls). The put/call ratio is typically used by traders as a sentiment indicator (so in this case showing a bullish market sentiment), and that’s all well and good. I’m using it for a different purpose … not to judge sentiment levels per se, but to see if we can glean behavioral patterns from the path in which those sentiment levels change over time. I’m not particularly interested in measuring sentiment or even change in sentiment. I’m interested in understanding the behaviors associated with sentiment, and how those behaviors change over time.

There have been six trading days over the last eleven where there were only half as many put options held by investors as call options. Prior to this, there were six trading days with this 1:2 ratio over the past two years. Also, you can see on this chart that there have always been spikes of put buying activity every few months, when investors get scared about this or that and decide to buy some talismans for “protection”. We haven’t had that sort of spike since last summer, and it’s not like there haven’t been any well-publicized market bogeyman since last summer. It’s the put-buying behavior that’s changed.

Second, this chart (h/t Devin Anderson and the rest of the Deutsche Bank equity derivatives team) shows the changing value of outstanding put options on the S&P 500. In other words, I’m less interested in the ratio or total number of put options out there at any given time, than in the dollar amount of hedging that those put options represent. This is what it means to show “delta-adjusted” open interest on put options, measured here in billions of dollars. So per this chart, over the past five years the maximum amount of hedging on the S&P 500 index using put options occurred in the fall of 2015, with about $230 million worth of “insurance”. Today, however, there is only about $70 million in S&P 500 index protection outstanding, the lowest amount in five years, and it sure looks to me like it’s on a path to nothing. Which would be an amazing thing.

I’m not saying that it’s a bad thing.

In fact, as someone who has a strong professional interest in encouraging allocators and investors to focus on what truly matters for their portfolios (see, of course, Rusty Guinn’s 2017 serial opus for Epsilon Theory, summary of the chapters linked here), I think it’s a good thing to stop making these ad hoc portfolio hedges. And if it’s accompanied by a conscious review of risk, reward and REGRET in our investment strategies for a profoundly uncertain world … well, that’s a really good thing.

But it is an amazing thing, with some important implications. Here’s one:

For years now, whack-a-mole vol-selling strategies, where any slight pick-up in volatility was promptly whacked on the head with a mallet of put selling and volatility futures shorting, have been extremely successful. Why? Because when volatility spiked up it meant that there was a bogeyman narrative being projected by CNBC and the like, and the naturally long-only allocator or investor got all scared and decided to “buy protection” with a put spread or some similar ad hoc hedge. And then when the bogeyman didn’t materialize, this “insurance” expired worthless, and the premiums paid were pocketed by the volatility selling strategies. If you’ve ever bought a portfolio hedge (and god knows I have), then you’ve been the counterparty to these vol-selling strategies. Time after time after time, you’ve been on the losing side of the zero-sum game that is the options market.

Today though … if that talismanic put-buying behavior is going away — and I think it is — then systematic volatility selling strategies won’t work as well going forward as they have in the past. That’s not a bold market call. It’s just a mechanistic fact of markets: sellers don’t get as high of a price for what they’re selling if you have fewer buyers. Volumes go down and margins are squeezed for traders, too.

This isn’t just an issue for hedge funds and Big Bank equity derivative desks. Systematic vol-selling strategies are everywhere these days, including the most vanilla of accounts. Got a covered-call overlay (also called a buy-write strategy) on your RIA account? That’s a systematic vol-selling strategy. Now please, I’m not saying that these are bad strategies or anything like that. Really, I’m not. I’m saying that a change in the hedging behaviors of institutional investors isn’t just inside baseball stuff. It matters for every financial advisor, every individual investor trying to figure out what to do.

And it goes way beyond the impact on this investment strategy or that strategy. What I think we’re seeing is the next necessary step in the transformation of markets into political utilities, where political institutions like the Fed are tasked in a more and more explicit manner with supporting the interests of the Nudging State and the Nudging Oligarchy. Does anyone doubt that if a vampire were truly to appear and knock on the market’s window, say a vampire in the form of a North Korean artillery attack, that the central banks of the world wouldn’t do “whatever it takes” to keep markets from falling? Why should we pay good money to buy put options as a hedge on our portfolio when the Fed will give us a put option for free? I think this is the most far-reaching and transformative effect of the extraordinary central bank policies of the past eight years — we are no longer afraid of things that go bump in the night.

But should we be?

Let’s agree (I hope) that buying ad hoc hedges in response to our fear of things going bump in the night is a poor implementation of our worries, that it’s an expensive psychic benefit that rarely moves the portfolio performance needle even if it works. But if we could implement a hedging strategy in a systematic way (not necessarily mathematical, although maybe, but always rigorous and repeatable in its process … something I’ve written about a lot, notably here and here), should we?

Are there monsters that the Fed can’t protect us from?

YES.

I think that there are two ways to think about the monsters that are immune to the central bankers’ Protection from Evil spell (sorry, revealing my OG D&D roots there).

First, there are monsters that the central bankers CAN’T control. Now to be honest, there aren’t too many of these bogeymen out there after eight years of forward guidance chants and $20 trillion of asset purchases, but the most obvious ones all come out of some unexpected turn of events emerging from China — a military coup, a hot war, a yuan devaluation (or float), a cold war on trade … something of that ilk. All very low probability events, but not totally crazy, either. If China and the U.S. are ever seriously at odds in a geopolitical sense, then it doesn’t matter how much jawboning we get from central bankers … the market is going to decline in a serious way. But I don’t get too worried about these monsters that the Fed can’t control.

Much more important, I think, are the monsters that the Fed WON’T control.

There’s an old saying that I remember liking so much when I first heard it: “Ask for forgiveness, not permission.” It appealed to me (and I suspect to most readers) because it speaks to our personal sense of independence and autonomy. By golly, I’m going forward with this smart plan of action that might not get approved in advance by my boss or my board or my significant other, because I truly believe it’s best for the team. And if my boss or my board or my significant other has a problem with my actions after the fact … well, then I’ll swallow hard, take full responsibility and ask for forgiveness.

This is exactly the opposite of how vampires behave.

Vampires ALWAYS ask for permission.

Vampires NEVER ask for forgiveness.

You get one chance to say no to a vampire. After that … well, you asked for it.

I’m not talking about Stephen King vampires. I’m talking about real-world vampires, intensely self-interested professions that have been institutionalized into destroyers. Real-world vampires aren’t knocking on the window asking for permission to come in. We’ve already given them permission. They’re already inside.

Like politicians who are invited into our White House and Capitol with our votes. Politicians who then enact policies to enrich and empower themselves, their families and their posses. Politicians who pursue these policies with absolute entitlement and zero shame.

Like police and surveillance organizations who are invited into our homes and cellphones with our tacit and explicit expressions of support for civil security. Police and surveillance organizations who then seize our property and our communications. Police and surveillance organizations who pursue these seizures with absolute entitlement and zero shame.

Like technology companies who are invited into our friendships and purchasing behaviors with our voluntary social media and online commerce participation. Technology companies who then monetize our most private habits, opinions and preferences. Technology companies who pursue this monetization with absolute entitlement and zero shame.

Like unfathomably large banks who are invited into every aspect of our lives with our insatiable appetite for debt and consumption. Unfathomably large banks who then claim a permanent and unbreakable lien on our income and our labor. Unfathomably large banks who pursue this claim with absolute entitlement and zero shame.Each of these modern vampires has charisma. They don’t present themselves as ghouls floating outside the upstairs window. They present themselves as the Robert Pattinson equivalent for whatever group of citizens they need to open the front door wide. It is, per Anne Rice, the first lesson of the vampire: “to be powerful, beautiful and without regret.”

Each of these modern vampires of the Nudging State and the Nudging Oligarchy shares a certain DNA. Not to get all Marxist here, but these vampires share the DNA of Capital, in opposition to the DNA of Labor, and this is why you will never see the Fed or any other central bank lift a finger against them. Because the Fed is also a creature of Capital — not a vampiric destroyer as these modern manifestations of Capital have become — but a creature of Capital nonetheless.

Meaning what, Ben? Meaning that all of the Fed’s policies — and particularly the monetary policies that are most impactful on our investment portfolios — are in the service of Capital. Sometimes, as we’ve experienced over the past eight years, that means incredibly accommodative monetary policy to support asset collateral prices. Sometimes, as we’ve seen in the past and I think we’re about to see again, that means punitive monetary policy to crush labor and wage inflation.

I don’t know how this change in monetary policy regime plays out. I don’t know how quickly punitive monetary policy happens or how far it runs. I can’t predict it. But I know that the Fed won’t prevent it, because the Fed isn’t your protector, and that’s what you should hedge against in an intentional, systematic way.

In real life it’s never the monster that goes bump in the night that gets you.

It’s always the monster in plain sight.

epsilon-theory-things-that-go-bump-in-the-night.pdf (738 KB)

Article by Salient Partners