2018 is upon us and the world seems a bit crazed; many people that I talk to appear to be worried on all fronts. The coming tax change and how it effects people’s investments is creating additional consternation since folks live off of this money and they fear a repeat of 2008. There is a Wall Street investment saying: “When the U.S. sneezes, the world catches a cold.” But a reduced U.S. corporate tax rate and the possibility of cheaply repatriating the U.S. Dollar (USD) might be the perfect drug for causing continued rising global stock markets. This extra corporate money will cause higher corporate earnings and this money will, under today’s conditions and with today’s transnational corporations, be pushed toward stock buy-backs and dividend payments. Stocks up.

[REITs]The corporate rate is being lowered all of the way down to 21%. But very good research coming out of Yardeni Research shows that, because loopholes remain un-closed, the new average effective U.S. tax rate actually drops down to 13%, Even more extensive research coming out during the last week of December from U.Penn-Wharton shows the effective corporate tax rate falling all of the way down to 9%! Stocks up.

I already hear talk from Republicans that, starting in 2019 (after the 2018 elections) in order to pay for coming infrastructure spending [AKA: $-Trillions transferred from working people to corporations via tax-receipts and tolls] and for the generous tax reduction given directly to the richest Americans, and the rapidly growing national debt that results, there will be a big push to whittle down Social Security and Medicare (which U.S. taxpayers have spent their working life paying into) and also Medicaid and child services that help the poor. But stocks up.

Complex U.S. TAX CHANGES Simplified:

- Americans won’t be doing their taxes on “the back of a postcard.”

- Individual tax rates: New individual tax rates are set as: 10%, 12%, 22%, 24%, 32%, 35%… and 37% for the top 1% of Americans with income in excess of $500,000 per year for single tax filers and $600,000 for joint filers. Because of the loss of some deductions, anyone that was near the top of an old bracket may be kicked up into a higher tax-bracket under this plan.

- Corporate tax rate: drops from 35% to 21%.

- Repatriation: There is a one-time repatriation opportunity for foreign held (U.S.) corporate money to move back to the United States at a tax-rate of of 8% (15.5% for cash); much of this money will flow toward stock buy-backs.

- Pass-through tax rate: S-corps, LLCs, partnerships and sole-proprietorships, including those owned by trusts and even those that pay no wages whatsoever, would be allowed to deduct 20% of their income as long as their income is below $315,000. For income above that level, the deduction would be limited to half of the W-2 wages or the individual’s portion of the pass-through entity’s income. Someone in the 37% tax bracket could reduce their tax burden down to 29.6%. Anyone that can create multiple, small pass-through organizations (rather than one larger one) may benefit. The new law would make it more profitable for pass-throughs to own their property (in a separate entity) rather than rent and to own their equipment rather than lease and, unfortunately, to automate as many jobs as possible. Many pass-throughs will now file to become C-corporations to save even more. High income earners that do not act to protect their income will absolutely pay higher taxes and perhaps as much as 10% more, and this would be dumb.

- Allows businesses to fully expense new equipment right away.

- Investments: No changes to long-term capital gains and dividend tax (which is already low in the U.S.) and no changes to cost-basis accounting for stock sales (which is good). Short-term capital gains are taxed at the tax bracket level, so this may be reduced for many investors, which is good. Corporate money diverted into share buy-backs and dividends would benefit stock holders.

- The Obamacare tax of 3.8% on investment income will be left to implode on its own, which may also occur in 2018.

- Take-give-take: No longer allowed to write off moving expenses, alimony payments or tax preparation.

- Anyone that is age 65 or older still gets to take the $1300 Additional Standard Deduction and…

- Everyone gets their “standard deduction” doubled to $12,000 per person, but this then eliminates the charitable giving tax write-off for 90% of American filers. There are far reaching effects to this tax change!

- The $4050 per family member personal exemption is eliminated, so a young married couple with two kids loses $4050 even with the standard deduction doubled, but…

- The child tax credit is doubled to $2000 per child, making an actual loss of $2050 for a married couple with two kids (which is then offset by opportunity to be in a lower tax-bracket).

- Eliminates the Children’s Health Insurance Program for the poorest children in America.

- AMT: Much harder for individuals to be hit by the Alternative Minimum Tax… a big gift to the rich. Corporations now have no AMT to worry about.

- Mortgage deduction: allows up to a total of $750,000 in bank loans to be deducted and this also applies to second homes but not to home equity lines of credit.

- SALT: State and local and property tax deductions are capped at $10,000 total. This predominantly hits Democrat states in the North East region, Great Lakes region and the West Cost, but one day after passage of the bill, these states were already finding some brilliant ways to skirt around this part of the law.

- Estate tax: doubled to exempt $11-million (or $22-million for couples).

- Contrary to rumor, deductions for small business expenses are still allowed, although it does eliminate ‘unreimbursed’ employee paid business expenses.

- The individual mandate of Obamacare is repealed effective 2019, so if one does not have health insurance after that, they are not fined, although I currently expect Obamacare to collapse before the end of 2019.

- High level medical expenses are still deductible.

- Retirement accounts: There are no changes to any retirement accounts such as IRA, SEP, ROTH or 401k.

Because President Trump refused, against advice, to wait an additional 5 business days (until January 2, 2018) to sign the new tax bill into law, it now mandates $175-Billion in PAYGO (Pay As You Go) spending cuts to Medicare, Social Security, border security and farmer subsidies to start in 2018 rather than in 2019. On December 23rd, President Trump stood in the dining hall of his exclusive Mar-A-Lago and triumphantly stated: “You all just got a lot richer.”

Do U.S. corporations plan to create jobs with any new found cash? According to an extensive study by Bank of America, they plan to do these six things, in the following order of importance. The first five boost profits for investors and shareholders (including management). Job creation did not even land on the list. Instead, corporations will push money toward:

- Pay down debt

- Share buy-backs

- Merger & acquisition

- Capital expenditures (improvements)

- Dividends

- Fund pensions for owners and management

RISK UPDATE: Risk is still higher than normal in the near-term and MarketCycle’s client accounts still hold protection to hedge its current 65-70% stock exposure from downside risk. The market has now gone an historic 1.5 years without a normal and routine 5% correction, plus the stock market is currently overbought. I don’t know how much longer this increased risk level will remain valid since the stock market is now backstopped via tax cuts. We are watching our MarketCycle Indicators closely and we trust them enough to not jump-the-gun. When risk has reduced, we will be removing our hedge and adding to our stock positions.

RELATIVE STRENGTH: The following chart visually shows Relative Strength for the 3 major markets (how strong is one as compared to others) and it clearly shows that, despite popular opinion in the investing press, the United States stock market is ‘leading’ the world in strength, Emerging Markets (China, India, Brazil, Russia, etc.) are ‘weakening’ and Developed Markets (big countries minus the U.S.) are ‘lagging’ but recent strength in Japan is causing the direction to rise. The large dot shows where each stock market is now and the trailing line and smaller dots show the connected direction of each of the 8 prior weeks.

Summary of Wall Street predictions for 2018:

- Goldman Sachs: “The stock bull market will continue in 2018.”

- Charles Schwab: “We believe that the U.S. bull market still has room to run in 2018, but it could shape up to be a bumpier ride as expectations and sentiment are elevated. We appear to be in the late stage of the [market] cycle. Global markets’ outperformance is unlikely to be repeated but conditions are still supportive of further gains.”

- Federated: “Unlike most years, we think that the actual 2018 corporate earnings numbers are going to come in above analysts’ expectations.”

- First Trust: “The velocity of money is picking up. Get ready for a continued stock bull market in 2018.”

- Fidelity: “We remain favorably disposed toward global equities and inflation-resistant assets.”

- Natixis: “We’re very optimistic about the economy going into 2018.”

- Legg Mason: “We see few reasons to expect the positive environment to deteriorate.”

- Wells Fargo: “Looking forward, we expect that the global economic expansion will continue through 2018.”

- Strategas Research: “This stock bull market could run quite a bit more, but 2017 will be a difficult act to follow.”

- Brown Brothers Harriman: “The bull market is still intact for 2018 because the positive fundamental backdrop is still in place.”

- Nomura Group: “We’re going to see very strong economic growth next year.”

- HSBC: “U.S. corporations are sitting on a lot of cash that will be spent on capex and share buybacks.”

- T. Rowe Price: “We expect the global economy to carry much of its momentum into the new year. The global economy appears to have entered a synchronized expansion. Disruptive Innovation should continue to benefit mega-cap tech companies. In our view, Treasury-bonds offer beneficial attributes within a portfolio as a counter to potential periods of heightened equity market volatility.”

- BMO: “Earnings are forecast to be even stronger over the first three quarters of 2018.”

- BlackRock: “We see stable global growth with room to run. We believe that investors will still be compensated for taking risk in 2018, but they might receive lower rewards.”

- Deutch Bank: “Robust U.S. growth and a pickup in global growth. We expect more regular 5% pullbacks to resume in 2018.”

- Citi: “Tax cuts could be quite stimulative to S&P-500 earnings per share.”

- Oppenheimer: “We believe an expected reduction in tax liabilities and opportunities for repatriation of the USD plus corporate deregulation would ultimately support share buybacks.”

- UBS: “We think our upside case, based on tax cuts in the United States, is more likely than a downside scenario, and upside potential outweighs a downside case by 2X.”

- JPMorgan: “The upcoming reduction of U.S. corporate tax rates may be one of the biggest positive catalysts for U.S. equities this cycle. It will likely result in rotation from bonds to equities and from international equities to U.S. equities.”

- Bank of America: “We think 2018 could be the year of [late-stage] euphoria. Sentiment will be a more important driver of returns in 2018.”

- Jefferies: “With tax reform boosting earnings for U.S. companies, we think that U.S. stocks are a better position.”

- Canaccord Genuity: “Ultimately, the market correlates to the direction of earnings. That direction of earnings is driven by economic activity and that looks positive for 2018.”

- Invesco: “Our base case scenario remains that the stock market will continue to perform well in 2018, although that doesn’t mean we won’t experience a pullback during the year.”

- Leuthold Group: “We expect that a [10%] correction in early 2018 is likely, and then the bull market resumes.”

- Credit Suisse: “In 2018, the economy clearly will be better. Recessionary risks remain well contained.”

This year’s prediction list is 100% bullish. It makes me worry when everyone agrees because whenever they do all agree, then something else usually happens. I’m watching things closely.

SUMMARY: Near-term = IMO, there is still a risk of a potential 5-10% temporary stock pullback, we’ve gone too long without one, but the new tax changes in the United States do help to backstop the global markets. Inflation remains low, making extended-duration Treasury-bonds a relatively safe portfolio hedge that also pays one interest to hold it. Longer-term = continued cyclical bull market in stocks. It is the middle of the late-stage of the market cycle. Calculated recession chances are less than 1% two months out, which is crazy low. Bitcoin is extremely over-valued and in my opinion will soon visit the $10,000 or even the $6500 price level, which would mean a crash of some size.

*** IMPORTANT Client PORTFOLIO CHANGES: We will soon be using some select socially responsible ETFs in our client portfolios. This has been difficult because of the lack of products and the low volume in those ETFs that did exist, but some new “ESG” ETFs coming out of Nuveen and i-Shares look promising. As additional innovative ETFs become available, we will attempt to go further in this direction.

“ESG” stands for “Environmental” where the company’s impact on the environment is measured, “Social” where the company’s external values are measured and “Governance” which measures the company’s internal ethics and actions. These companies are not only not harming the planet, but are actually working toward a better world. How great is that!

*** Our CHARITY for 2017: MarketCycle Wealth Management always gives a good-sized chunk of its profits to charity each year. Since this income originates from our client’s fees, this charitable contribution actually comes from our clients. This year we are all giving to the Natural Resources Defense Council that “works to ensure the rights of all people to clean air, clean water and healthy communities.” We also give smaller donations to other charities throughout the year.

If you like what MarketCycle is doing, join as a client and spread the word! We purposely keep our fees affordable and our risk low… we accept clients from across the globe… the first three months are free!

NOTE: Client tax documents will be available in mid-February and you will be notified at that time.

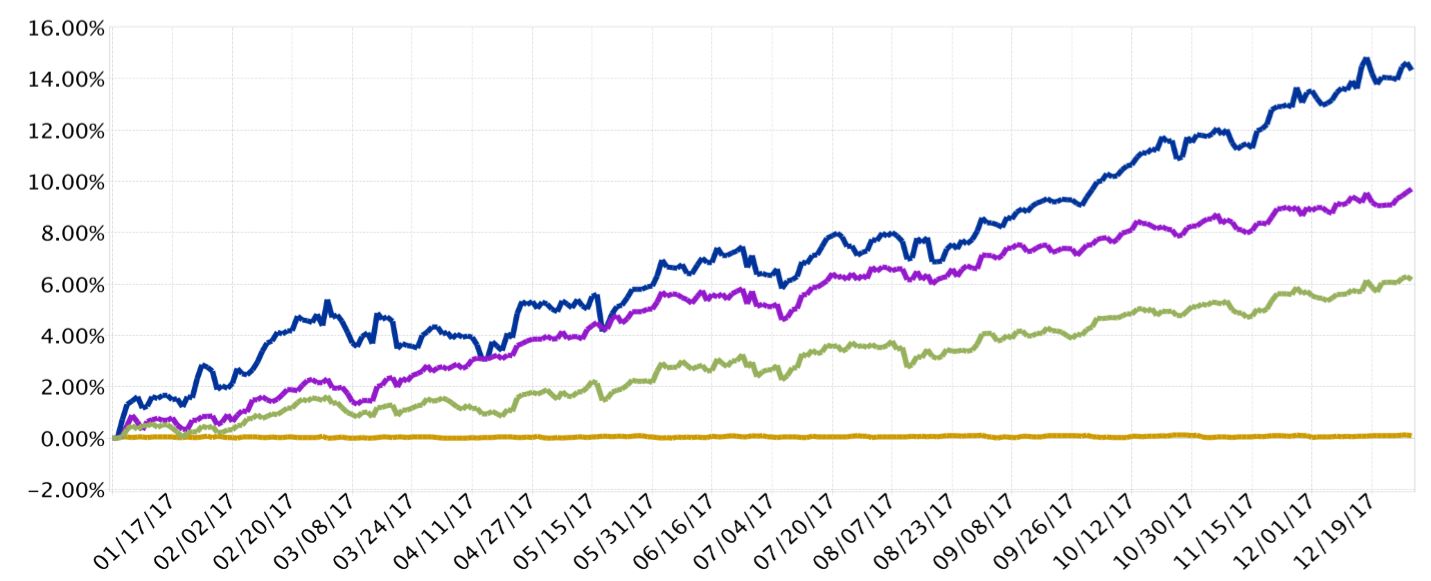

- PORTFOLIO PERFORMANCE for the total year 2017. MarketCycle’s client accounts have held relatively conservative stock positions plus we have been safely hedged during the last six months of 2017, reducing gains but giving us nearly 0% risk in the bargain. All four below are shown without a management fee. The order & color in the 4 bullets mimic the order & color in the chart:

- MarketCycle

- Buy & Hold Index (roughly 75% stocks and 25% bonds)

- Hedge Fund Performance Index

- Savings Account

This is me, over time, put into a chart:

Article by Stephen Aust, MarketCycle Wealth Management