As 2018 gets rolling, markets don’t have great expectations for Fed interest-rate hikes. Based on futures pricing, roughly two small increases are anticipated this year. We think there will be more.

[REITs]In our view, several economic and policy factors are converging that could pave the way for four 25-basis-point hikes in 2018, pushing official short-term rates up by a total of 1% for the year. Here are five things that tell us the market is coming in on the low side:

- The economy is rolling along. US gross domestic product grew by more than 3% in annualized terms over the final nine months of 2017 and the momentum has carried over into 2018. A strong economy makes rate hikes more likely, in order to prevent overheating. Run the economy too hot for too long, and there’s a good chance inflation will exceed acceptable levels. A vibrant economy should also make the Fed more confident that raising rates won’t derail the expansion—just slow it to a more sustainable pace.

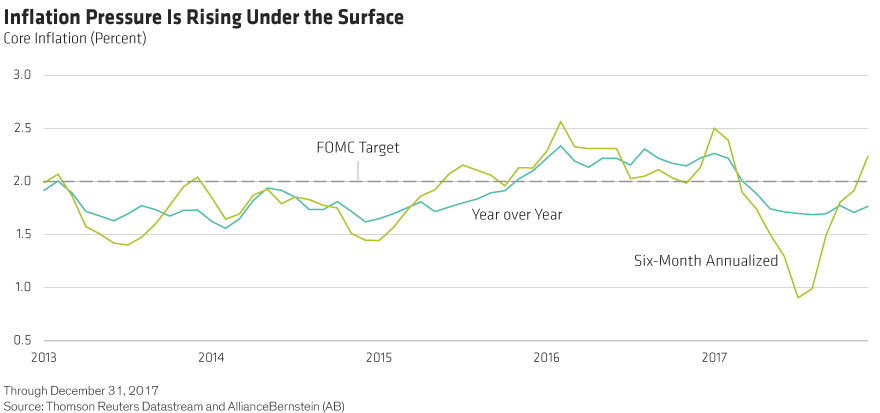

- Inflation pressure is rising. Year-over-year core inflation, which excludes food and energy, is still well below the Fed’s 2% target. However, pressure is rising below the surface. Six-month annualized core inflation has already topped the 2% mark and is rising (Display). Many factors that continue to hold down the year-over-year reading are likely to dissipate over the next few months. And rising oil prices offer more evidence to support our expectations for higher prices.

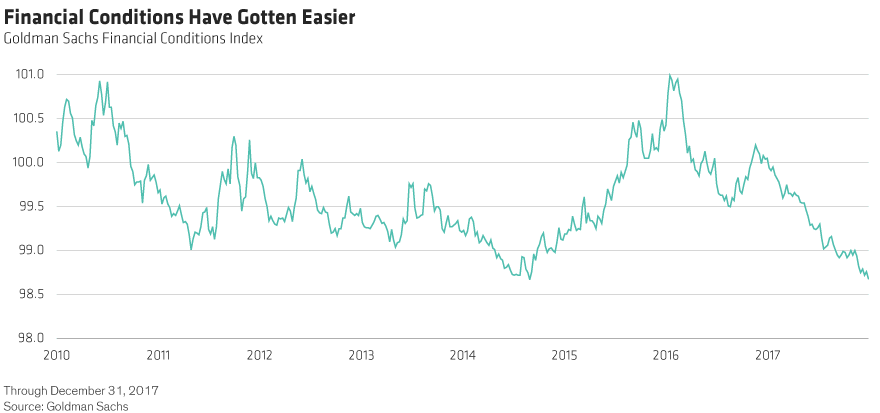

- Financial conditions have gotten easier—not tighter. When financial conditions are easy, households and businesses have ready access to cheaper funds to fuel consumption or investment. When a central bank raises rates, it’s an effort to tighten conditions—to slow the economy and keep inflation contained. The Fed has hiked rates four times since December 2016, but financial conditions have actually eased (Display). That’s great for growth, but the Fed is probably starting to worry about too much of a good thing.

- Policy was tightened four times last year. The Fed raised rates three times in 2017 (as well as once in December 2016). It also started to shrink its balance sheet. That’s four cases of policy tightening. The economy is in better shape now and inflation will likely be higher, so it’s hard to see why the Fed would be even slower to tighten in 2018 than it was last year. The Federal Open Market Committee (FOMC) still describes its tightening cycle as “gradual,” but slowing the pace to two hikes in 2018 would be even more gradual—despite a stronger economy and markets.

- The Fed doesn’t want markets to overheat. Several FOMC members have expressed concern that a too-accommodative monetary policy could contribute to financial-market excesses and asset-price bubbles. We’re not worried yet that bubbles are emerging (neither is the Fed), but rate hikes that tighten conditions would reduce that risk. And with the economy strong enough to handle higher interest rates, pulling the reins in a bit on financial markets makes sense.

And One Reason We Might Be Off the Mark

We think there’s a strong case for tighter monetary policy in 2018, but there are always risks that could upend both the economy and our expectations. Political turmoil in Washington is the biggest wild card—as highlighted by the recent (and thankfully brief) government shutdown.

Whether it’s a longer shutdown down the road, a debt-ceiling cliffhanger or turmoil surrounding November midterm elections, we still see politics as the single biggest risk to the expansion. If political risks play out in a disruptive way, it would make the Fed much less likely to raise interest rates as much as we think they will.

But as things stand now, we’re confident in our assessment. The economy is striding along and has shrugged off political developments to this point; our base-case forecast is for it to stay that way. That should set the stage for the Fed to hike four times this year—more than the market expects.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Article by Eric Winograd, Alliance Bernstein