Warren Buffett is famous for being one of the most successful active investors in the world.

Through his investment conglomerate Berkshire Hathaway, Buffett manages a stock portfolio that is valued at more than $100 billion. Interestingly, his portfolio is filled with high-quality dividend growth stocks. You can access Buffett’s portfolio below.

Fellow dividend growth researcher Dividend Growth Investor is revisiting Warren Buffett’s 10-year bet against active investing (specifically against hedge funds), and Sure Dividend was invited to participate.

This article will discuss Buffett’s original bet before outlining a group of investments that we believe is likely to beat the S&P 500 over the next 10 years.

You can skip to a particular section of this article using the table of contents below:

- Buffett’s Original Bet Against Active Investing

- Why Warren Buffett Won The Bet

- Our Contender For The Next Ten Years

- How To Invest In Our Contender

Buffett’s Original Bet Against Active Investing

Despite being one of the world’s most successful active investors, Buffett made a sizable bet against the segment of the investing world that is most active in nature: hedge funds.

Buffett recapped his decade-long bet with the following passage in Berkshire Hathaway’s 2016 Annual Report:

“In Berkshire’s 2005 annual report, I argued that active investment management by professionals – in aggregate – would over a period of years underperform the returns achieved by rank amateurs who simply sat still. I explained that the massive fees levied by a variety of “helpers” would leave their clients – again in aggregate – worse off than if the amateurs simply invested in an unmanaged low-cost index fund. (See pages 114 – 115 for a reprint of the argument as I originally stated it in the 2005 report.)

Subsequently, I publicly offered to wager $500,000 that no investment pro could select a set of at least five hedge funds – wildly-popular and high-fee investing vehicles – that would over an extended period match the performance of an unmanaged S&P-500 index fund charging only token fees. I suggested a ten-year bet and named a low-cost Vanguard S&P fund as my contender. I then sat back and waited expectantly for a parade of fund managers – who could include their own fund as one of the five – to come forth and defend their occupation. After all, these managers urged others to bet billions on their abilities. Why should they fear putting a little of their own money on the line?

What followed was the sound of silence. Though there are thousands of professional investment managers who have amassed staggering fortunes by touting their stock-selecting prowess, only one man – Ted Seides – stepped up to my challenge. Ted was a co-manager of Protégé Partners, an asset manager that had raised money from limited partners to form a fund-of-funds – in other words, a fund that invests in multiple hedge funds.

I hadn’t known Ted before our wager, but I like him and admire his willingness to put his money where his mouth was. He has been both straight-forward with me and meticulous in supplying all the data that both he and I have needed to monitor the bet.

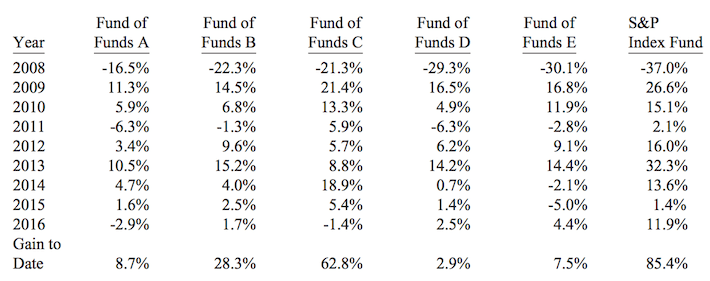

For Protégé Partners’ side of our ten-year bet, Ted picked five funds-of-funds whose results were to be averaged and compared against my Vanguard S&P index fund. The five he selected had invested their money in more than 100 hedge funds, which meant that the overall performance of the funds-of-funds would not be distorted by the good or poor results of a single manager.

Each fund-of-funds, of course, operated with a layer of fees that sat above the fees charged by the hedge funds in which it had invested. In this doubling-up arrangement, the larger fees were levied by the underlying hedge funds; each of the fund-of-funds imposed an additional fee for its presumed skills in selecting hedge-fund managers.

Here are the results for the first nine years of the bet – figures leaving no doubt that Girls Inc. of Omaha, the charitable beneficiary I designated to get any bet winnings I earned, will be the organization eagerly opening the mail next January.”

Footnote: Under my agreement with Protégé Partners, the names of these funds-of-funds have never been publicly disclosed. I, however, see their annual audits.

You now have a solid understanding of the administrative details embedded in Buffett’s bet against hedge funds. The reason why Buffett has won the bet is also worth discussing.

Why Warren Buffett Won The Bet

There are two main reasons why Buffett won the bet, in our view.

The first is because of the prolonged and aggressive bull market that took place since 2009 or so. Hedge funds are designed to deliver returns through all economic environments, which means that they will sometimes take substantial short positions – harming returns in a market that is delivering broad positive returns.

Buffett wrote about this in his summary in Berkshire’s annual report:

“The compounded annual increase to date for the index fund is 7.1%, which is a return that could easily prove typical for the stock market over time. That’s an important fact: A particularly weak nine years for the market over the lifetime of this bet would have probably helped the relative performance of the hedge funds, because many hold large “short” positions. Conversely, nine years of exceptionally high returns from stocks would have provided a tailwind for index funds.

Instead we operated in what I would call a “neutral” environment. In it, the five funds-of-funds delivered, through 2016, an average of only 2.2%, compounded annually. That means $1 million invested in those funds would have gained $220,000. The index fund would meanwhile have gained $854,000.”

The second – and far more important – factor that led to Buffett winning this wager is the significant fees charged by the hedge fund industry in general. Buffett also wrote about this in his annual report:

“Bear in mind that every one of the 100-plus managers of the underlying hedge funds had a huge financial incentive to do his or her best. Moreover, the five funds-of-funds managers that Ted selected were similarly incentivized to select the best hedge-fund managers possible because the five were entitled to performance fees based on the results of the underlying funds.

I’m certain that in almost all cases the managers at both levels were honest and intelligent people. But the results for their investors were dismal – really dismal. And, alas, the huge fixed fees charged by all of the funds and funds-of-funds involved – fees that were totally unwarranted by performance – were such that their managers were showered with compensation over the nine years that have passed. As Gordon Gekko might have put it: “Fees never sleep.”

The underlying hedge-fund managers in our bet received payments from their limited partners that likely averaged a bit under the prevailing hedge-fund standard of “2 and 20,” meaning a 2% annual fixed fee, payable even when losses are huge, and 20% of profits with no clawback (if good years were followed by bad ones). Under this lopsided arrangement, a hedge fund operator’s ability to simply pile up assets under management has made many of these managers extraordinarily rich, even as their investments have performed poorly.

Still, we’re not through with fees. Remember, there were the fund-of-funds managers to be fed as well. These managers received an additional fixed amount that was usually set at 1% of assets. Then, despite the terrible overall record of the five funds-of-funds, some experienced a few good years and collected “performance” fees. Consequently, I estimate that over the nine-year period roughly 60% – gulp! – of all gains achieved by the five funds-of-funds were diverted to the two levels of managers. That was their misbegotten reward for accomplishing something far short of what their many hundreds of limited partners could have effortlessly – and with virtually no cost – achieved on their own.”

In summary, the terrible performance of hedge funds can be chalked up to a strong overall equities market and substantial investing fees.

If you’re interested in learning more about the wager, the following article by Bloomberg provides some interesting perspective from Ted Seides himself. It’s worth reading if you want to understand the psychology behind his recommendation of hedge funds.

- Why I Lost My Bet With Warren Buffett by Ted Seides

Ted Seides failed to beat the S&P 500 over the 10-year time frame. We’d like to retake Buffett’s challenge (although he is unfortunately not participating this time). Our contender in a 10-year standoff versus the S&P 500 is introduced below.

Our Contender For The Next Ten Years

At Sure Dividend, we often write about the benefits of investing in the Dividend Aristocrats. The requirements to be a Dividend Aristocrat are:

- Membership in the broader S&P 500 Index

- 25+ years of consecutive dividend increases

- Certain minimum size and liquidity requirements

You can see the entire list of all 51 Dividend Aristocrats here.

Dividend history is the most notable requirement for inclusion in the Dividend Aristocrats. It is also the reason why we’ve chosen the Dividend Aristocrats for our hypothetical ten-year bet. Dividend history is an accurate barometer of business quality. With 25+ years of consecutive dividend increases, the Dividend Aristocrats are some of the most high-quality businesses around.

“Business quality” is an abstract concept and is not the only reason why we’ve chosen the Dividend Aristocrats in our hypothetical bet against Warren Buffett. There are five more actionable reasons why we believe that the Dividend Aristocrats are likely to outperform the S&P 500 during the next ten years. We outline each reason in the following passages.

You can skip to any of our reasons by clicking the links below.

- Reason #1: The Historical Performance of the Dividend Aristocrats

- Reason #2: The Dividend Aristocrats Excludes Risky Stocks

- Reason #3: Dividend Stocks Have Better Capital Allocation

- Reason #4: The Shareholder-Friendly Nature of Dividend Aristocrats

- Reason #5: Current Market Valuations

Reason #1: The Historical Performance Of The Dividend Aristocrats

The historical performance of the Dividend Aristocrats has been remarkable.

As the following image shows, the S&P 500 Dividend Aristocrats Index has outperformed the broader S&P 500 Index by a wide margin over the past ten years.

Source: S&P 500 Dividend Aristocrats Index Fact Sheet

Here’s what the numbers look like:

- The Dividend Aristocrats have delivered annualized returns of 11.57% over the past 10 years

- During the same time period, the broader S&P 500 Index has delivered annualized returns of 8.30% per year

- This means the Dividend Aristocrats have outperformed by more than 3% per year for ten years

What is special about the outperformance of the Dividend Aristocrats is that this group of high-quality businesses has delivered greater performance with less volatility.

While traditional academic finance theory tells us that an investor must incur greater volatility to achieve outsized returns, the historical performance of the Dividend Aristocrats shows that this isn’t always the case in practice.

Source: S&P 500 Dividend Aristocrats Index Fact Sheet

You are probably thinking “past performance is no guarantee of future results.” That is certainly true in many cases.

With respect to the Dividend Aristocrats, though, their remarkable past performance is grounded in other common-sense investment themes, which gives us confidence in their likelihood to beat the S&P 500 Index moving forward. We outline the other reasons why the Dividend Aristocrats are likely to outperform in the following passages.

Reason #2: The Dividend Aristocrats Excludes Risky Stocks

In our view, there are two groups of stocks that present the lion’s share of risk for investors: pre-earnings startups, and companies undergoing bankruptcy proceedings.

The Dividend Aristocrats is a group of dividend stocks with 25+ years of consecutive dividend increases. The dividend history requirement excludes pre-earnings startups because it is impossible for a pre-earnings startup to pay increasing dividends for 25 years. There simply isn’t enough cash flow to support more than two decades of rising cash distributions to investors.

Similarly, the Dividend Aristocrats will exclude companies going through bankruptcy as such companies will almost always cut their dividends – removing them from the Dividend Aristocrats – before filing a Chapter 11 or Chapter 7 bankruptcy claim.

Because the Dividend Aristocrats excludes these two categories of business, they also avoid their poor performance. This boosts the returns of the Dividend Aristocrats over time.

Reason #3: Dividend Stocks Have Better Capital Allocation

Since the main Dividend Aristocrats inclusion requirement is based on dividend history, each member of the Dividend Aristocrats must pay a dividend.

In other words, each member of the Dividend Aristocrats is delivering a proportion of every earned dollar to its shareholders via dividends.

This leaves less cash available for internal reinvestment. Accordingly, the C-suite executives of the Dividend Aristocrats must be ultra-selective with their capital allocation. They must pursue only their most attractive growth opportunities (leaving their so-so options behind) because there is less cash available for organic reinvestment.

Over time, this means that the Dividend Aristocrats’ capital allocation decision-making is enhanced by their decision to consistently grow their dividend payments. This is a powerful yet unintended benefit to dividend payments and one that contributes to our confidence in the future returns of the Dividend Aristocrats.

Reason #4: The Shareholder-Friendly Nature of Dividend Aristocrats

Outstanding companies operate with the best interests of their shareholders in mind. Conversely, poor investments often operate with other motives: maximizing executive compensation, growing a business’ size with no consideration for per-share intrinsic value, or generating fame or wealth or managers.

When the goals of a company’s management team diverge from the goals of its stockholders, shareholder value is almost always destroyed. Investing in shareholder-friendly stocks avoids this potential problem.

This is intuitive, but finding shareholder-friendly stocks is a bit harder. Fortunately, the steadily rising dividend payments of the Dividend Aristocrats is a very strong indicator that these companies operate with their shareholders’ best interests in mind. This mindset likely spills over to other decisions that are made at the corporate level, enhancing total returns over the long run.

Reason #5: Current Market Valuations

The stock market is currently trading at valuation levels that are well above normal levels. The following graph of the S&P 500’s price-to-earnings ratio provides a nice illustration of this phenomenon:

Source: multpl.com

Note: the graph above displays a cyclically-adjusted price-to-earnings ratio, sometimes called the Shiller PE ratio, that uses the index’s average earnings over the past 10 years.

The above-average valuations of the overall stock market mean that investor returns from this point onward are likely to be far lower than the long-term average. Moreover, the probability of a stock market recession or bear market is also elevated.

What does this mean in terms of the Dividend Aristocrats?

The Dividend Aristocrats are, on average, very defensive businesses. It takes a good degree of resiliency for a company to continuously raise its dividend each and every year for more than 2 decades. Historically, this has led the Dividend Aristocrats Index to widely outperform the S&P 500 Index during periods of economic turmoil.

Given today’s elevated market levels, the recession resiliency of the Dividend Aristocrats is the last reason why we’ve chosen this group of stocks as our wager against the S&P 500 for the next 10 years.

How To Invest In The Dividend AristocratsWhile we aren’t necessarily recommending that you take investment action based on our hypothetical bet with Warren Buffett, it’s important to understand that there are simple, passive ways to invest in the Dividend Aristocrats today.

There are currently 51 Dividend Aristocrats. Buying each and every Dividend Aristocrat is not a wise strategy. There are three reasons why:

- It’s difficult and time-consuming to really understand the operations and performance of 51 different companies.

- By buying 51 different stocks, you’ll incur far more commissions and fees than is truly necessary. Adequate diversification can be achieved by owning as little 18 to 20 stocks.

- Certain members of the Dividend Aristocrats are overvalued right now (and are likely to be at any given time). Accordingly, they do not have appeal as an investment by themselves.

The alternative to buying the Dividend Aristocrats one-by-one is purchasing a dividend ETF. Fortunately, there is an ETF dedicated to owning a passive basket of the Dividend Aristocrats. The ETF is the S&P 500 Dividend Aristocrats ETF and trades under the ticker NOBL. For investors looking for a passive way to invest in the Dividend Aristocrats with no further work, this passive ETF is a promising option.

Final Thoughts

I want to be completely clear – at Sure Dividend we prefer to invest in individual securities (just as Buffett does) instead of funds. The majority of the Dividend Aristocrats are trading above fair value currently, as is the S&P 500. In aggregate we believe the Dividend Aristocrats Index is superior to the S&P 500.

We also believe that investing in individual high quality dividend growth stocks in a systematic and intelligent way is superior to investing in a fund. We picked a fund for this challenge to better lay out the investing thesis that high quality stocks are likely to outperform over the long run. There is significant risk that any 1 stock will under-perform; less so for a group of 51 stocks.

You can view the hypothetical 10-year bets that other dividend growth writers are making against the S&P 500 on the Dividend Growth Investor site.

Our contender is the Dividend Aristocrats Index ETF (NOBL) – some of the best dividend growth stocks in our investment universe. With that said, they are not the only place where high-quality dividend growth stocks can be found.

If you’re interested in finding high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend articles will also prove useful:

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings: widely considered to be the “best-of-the-best” when it comes to dividend histories, the Dividend Kings are a super-exclusive group of dividend stocks with 50+ years of consecutive dividend increases.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

Article by Nick McCullum, Sure Dividend