Bronte 2017 letter to investors

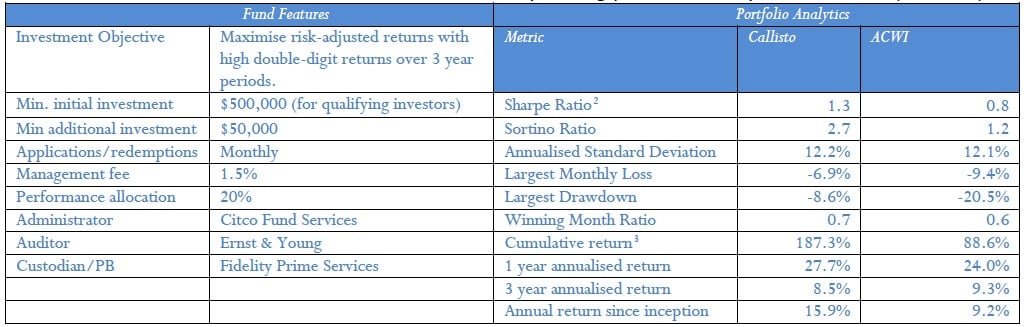

The Bronte Capital Callisto Fund L.P. is a global long/short fund targeting double digit returns over the long term, advised by a performance orientated firm with a process and portfolio that is genuinely different. Objectives include lowering the risk of permanent loss of capital and providing global diversification without the market/drawdown risks typical of long-only funds. A highly diversified short book substantially reduces risk and enables profits to be made in tough markets.

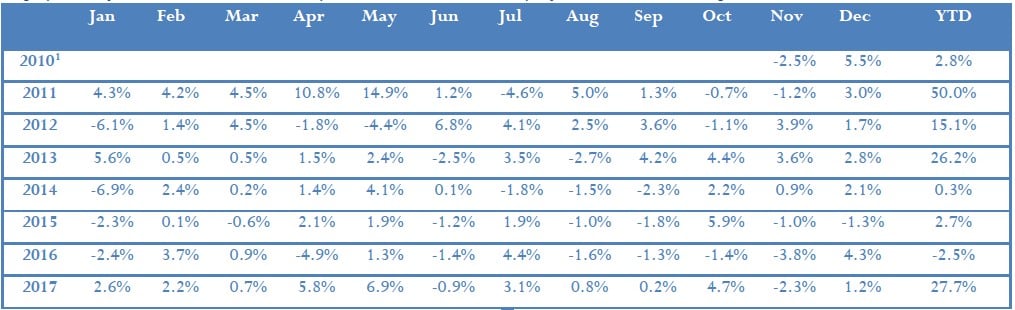

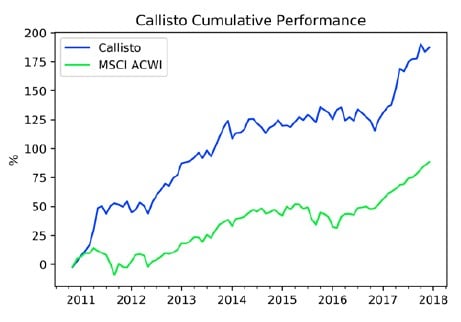

The fund gained just over a percent in December, falling slightly behind what was yet another positive month for global stocks. For the quarter it rose by 3.3% and by 27.7% for the calendar year. Indeed, this year’s results are astonishing given our positioning. There is a raging bull market, we run a large short book and we have roughly broken even on the shorts. We run more than 100 percent long, did not lose money on our shorts and our longs have performed okay so we have outperformed long only global indices. Winners for the quarter included Interactive Brokers and MTU on the long side, but pleasingly one of the top 3 winners for the quarter was a short (the South African retailer Steinhoff which has imploded with disclosures of “accounting irregularities”).

The fund gained just over a percent in December, falling slightly behind what was yet another positive month for global stocks. For the quarter it rose by 3.3% and by 27.7% for the calendar year. Indeed, this year’s results are astonishing given our positioning. There is a raging bull market, we run a large short book and we have roughly broken even on the shorts. We run more than 100 percent long, did not lose money on our shorts and our longs have performed okay so we have outperformed long only global indices. Winners for the quarter included Interactive Brokers and MTU on the long side, but pleasingly one of the top 3 winners for the quarter was a short (the South African retailer Steinhoff which has imploded with disclosures of “accounting irregularities”).

Bronte recently ventured through the mid-west of the USA and then to Northern Europe visiting investment candidates. We saw extremely high-quality companies in both locations – but the European ones are cheaper than the American ones. Our bias towards European longs and American shorts is right for now.

As a business, Bronte also had a good year. We hired Andrew Reeves – a former Hong Kong based investment banker. He has helped improve processes, included moving to a multi- prime broker arrangement, and his experience in Asia adds further depth to our investment team.

Importantly, we continue to plan to close to new funds when we reach about half what we think our capacity limits are. At the rate at which we are growing we will probably close to new monies sometime in 2018.

Because of this we ask you to indulge us in a long letter explaining Bronte from the top-down. We want to explain how we think about portfolios – how we think about risk management decisions – and why Bronte is structured for multi-cycle – even multi-generational sustainability. We want you to understand what you own at Bronte and why you own it.

It’s also an easier time to explain what we are doing because we have outperformed. We will underperform sometimes too – and it will give you more confidence in what we do and why we do it if we explain the portfolio positioning before any period of underperformance.

Strengths and weaknesses at Bronte

We believe that Bronte has a sustainable and meaningful advantage in shorting stocks. We have made (some) money shorting throughout the bull market. We roughly broke even shorting during 2017 during a rip-roaring bull market. This is enormous outperformance – albeit aggregate returns from shorting over our full history have not been large – and this is the sort of “outperformance” that is hard to eat.

Alas the advantage we have in shorting stocks is not scalable beyond a certain AUM. Bronte constantly reviews our capacity and will close our funds well before our size starts to cannibalize returns. Most of the intellectual effort that Bronte has expended over the past nine years has been in systems to improve our edge short-selling. As our systems get better our edge gets better – and just as importantly – our ability to scale our edge becomes better.

Our approach to longs is very different – value investing is a proven model, but it is a less differentiated and novel approach than our shorting. We have spent a lot of time trying to work out what makes for a “good business” and we try to buy those at reasonable prices.

Our record is good – our longs have done better than market over the period we have been running Bronte. Our edge in longs scales pretty well - we could be managing 5x as much money and it would not meaningfully impair performance.

Alas this is the wrong-way around. We wish our differentiatied substantive edge was in going long. The really big money in the world is made by people who own things, build things and invest in things. Short selling is just not as good a way to make money over the long run. Bluntly – you would rather be Warren Buffett than any of the, very few, famous short sellers though both approaches have generated a lot of “alpha”.

What a mathematical finance type would do

One of the best books we have read in the past year was Edward Thorp’s autobiography “A Man for all Markets”. Thorp (literally) wrote the book on how to beat casinos by counting cards at Black Jack – and he later traded (very) successfully on global markets.

Thorp’s formula is to find an edge. Any edge – but the bigger and more sustainable the better. Then adding trades to systematically reduce any risk. Thorp would have his edge (usually some statistical anomaly he found) and then he would work how to hedge it – systematically working out with factor analysis all of the optimal hedges. This would be dynamically managed with computers. If the risks could be reduced, then the edge could be levered. You could get more and more of the good stuff. Thorps’ results were astonishing.

We would love to be able to do this – but for it to work well you need an edge that can be levered. For the most part though our edge in short selling is – as we have stated – constrained – and so leveraging the edge up a few times is simply impossible.

That said – we irregularly find specific offsetting trades we can add that allow us to scale our positions further and reduce risk simultaneously. This is what a true “hedge” fund would do. And we do it when the opportunity arises. At the moment such trades amount to about a 5 percent gross position.

Most of the time we manage a far more conventional portfolio – a portfolio whose idea goes back to the most famous of all portfolios – the so-called 60-40 portfolio.

The 60-40 portfolio

The 60-40 portfolio is the benchmark of the risk averse passive investor – especially the risk averse passive American investor.

The idea is simple. Put 60 percent in a broad equity index (usually an S&P 500 ETF) and 40 percent in a broad bond index (in the past the choice was the Lehman bond index but these days people substitute a Treasury index).

Then every month you rebalance so that the weighting remains 60-40.

If the equity market goes up relative to bonds you are forced to sell equities and buy bonds to keep the 60-40 ratio. If the equity market goes down relative to bonds you are forced to sell some bonds and buy some equity. The net effect is you tend to buy equities when the market falls and sell equities when the market rises. Over fairly long periods of time this simple passive portfolio outperformed both the equity and the bond market.

The portfolio worked well for another reason too – which was that the bonds were inversely correlated to equities. The bonds appreciated just as the equity market was giving you a tough time. This meant (by selling some bonds) you could buy even more equities when the equity market was low.

The current “everything bubble” however has challenged the 60-40 portfolio. Bond yields have fallen to the point where real yields are approximately zero (or even negative). Moreover, equities have become more correlated to bonds which removes many of the rebalancing advantages of the 60-40 portfolio. Notwithstanding this we still believe the 60-40 portfolio has much to recommend it.

Indeed, we think (as do several of our clients) that the 60-40 portfolio is the benchmark for a multi-generational endowment. It may not be flashy – but it is low risk – and it should be stable enough for the next century.

It will also – just by its nature – underperform every bull market, outperform bear markets but still be positively market correlated. The 60-40 portfolio still loses money when the market goes down – just not as much as more aggressive portfolios.

We (usually) do not own bonds though. We can obtain far more negative correlation to equities via our short book. Our default positioning is to reconstruct a 60-40 portfolio but throw out the (very low return) bonds and add in our (genuinely alpha generating) shorts.

How would the Bronte 60-40 portfolio actually look?

If stocks were uncorrelated to bonds, then a 60-40 portfolio would have a beta of 0.6. That would mean it moves about 0.6 times the move in the stock market on any given day.

Given that bonds used to be negatively correlated to stock markets the beta is closer to 0.5. The portfolio managed to a 0.5 constant beta (which of course involves buying as stocks go down and selling as stocks go up) has a pretty good record versus the stock market or bond market.

The beta of our shorts is somewhere between 1.5 and 3 but we consider it to be about 2 on average. [We promise you this range has been one of the most continual talking points at Bronte – but for the sake of argument let’s consider it is about 2 for this analysis. It is not 2 – but we will consider the variance on that number later.]

If we were to manage to a portfolio beta of 0.5 we could set our portfolio as 150 percent long and 50 percent short. The long book would be beta of one and the short book a beta of two. The net beta of the portfolio would 0.5.

Whatever – a 150 long 50 short portfolio would be wonderful if our shorts were to behave like this year. Our shorts broke even in a rip-roaring bull market. If our longs just returned market we would earn 1.5 times the market return with 0.5 times the market risk.

And if the market were to fluctuate – rather than being the monotonic up market of the past year - we would do even better as there would be some rebalancing effect. That would just be the same rebalancing effect of the 60-40 portfolio which is small, but is real.

In this stylized portfolio the advantage of the short book is not that it makes you money when the market goes down. Rather it allows you to make more money when the market goes up without losing as much when the market goes down. You don’t short to make money per-se, rather you short because it allows you to go more long.

Our modifications to the portfolio above

There are modifications we make to the portfolio above. By far the most important – is that we are not wedded to any particular percentage long or short. A 60-40 portfolio works pretty well – but so does a 50-50 or even a 40-60 portfolio.

It would be better (but requires some judgement) to be slightly dynamic, having a 60-40 portfolio whenever the market is cheap, a 50-50 portfolio when it is middling and ac40-60 portfolio when it is expensive. You would need a measure of “expensive” and the one we might choose would be market cap to GDP. This is also a measure that Warren Buffett cites.

We have another measure, which achieves a similar result: if our system for finding shorts is identifying limited opportunities we get longer. We could wind up being very long – maybe as high as 140 long 40 short.

If by contrast – we can find shorts at will – but finding rational longs is difficult we will run with that too. And our portfolio will look more like it does now – something like 110 long, 60 short.

One little nuance: the beta of our short book

We have attempted to measure the beta of our shorts several times. The answers typically come out around 1.7 – and if you measure the beta of the portfolio it turns out to be positive most times and most ways we measure it.

However, since we started Bronte the market has had three (small) hiccups. The first was in 2011, the second was the “taper tantrum” of 2013. The final was the debt-hiccup of the first six weeks of 2016.

If the beta of our portfolio is positive we should go down (albeit slightly) during all these events.

Instead we went up – only a little – but we performed better than our positioning. And the reason we went up is that our shorts performed really well.

It seems that our shorts (which are highly idiosyncratic – mostly chosen by following bad people) are less correlated when the market is rising than when the market is falling. The beta appears to go well over two in a falling market.

We hope this is generally true – but to be honest we do not have enough data points. If it is true then the fund should be positive when the market eventually retreats – at least for the first part of the retreat.

That said – we are as short as we have ever been – and even then, we think our effective beta is between 0.1 and 0.4.

The long book

As noted above we would prefer to be good at longs than at shorts. You would rather be Warren Buffett than even the best of the shortsellers.

As John puts it – he with the best long book wins.

Here Bronte aspires to be as close to Warren Buffett/Charlie Munger as possible. The motto: buy businesses that spin off cash, will be bigger and better in ten years, and get them at a reasonable price.

‘’Short-term Catalyst’’ is the most common style we see from our competitors. We are emphatically not “event driven”. We tend to be uninterested in quarterly earnings except in as much as they signal a break in a business model. We are far more interested in how a business keeps its edge over a decade. We want to understand what makes businesses tick.

We are very interested in businesses that have hard to displace products. As a typical example there is a global duopoly for engines for wide bodied planes. Every wide-bodied plane you will fly on for at least the next fifteen years will have an engine made by Rolls Royce or General Electric. If you think that Rolls Royce can expand and exploit that position over the next decade you probably should own the stock. We do think that, but we could be wrong. If our view is falsified, we will sell the stock.

--

We would prefer to buy good businesses very cheaply but that option is not available very often. Normally we buy very good businesses at reasonable prices.

If the market is really weak the shorts will give us (hopefully) a lot of cash – and that cash will be used to buy more of these good businesses at better prices.

On longs we are very selective. During 2017 we bought three new positions but only one large position. And the two small positions were closely related (one of their main assets is a joint venture). We would rather keep the names quiet as we may buy more. But these were not distressed assets and the PE ratio was about market on average. They were not “cheap” but we believe prospects over the next decade are very good.

We will reject a position entirely when our thesis about the long-term prospects of the business is falsified. Our goal here it to continuously improve the quality of our investments – using dips in the market and profits from the short book when they come as a way of funding more longs.

We mentioned earlier our recent trip through the mid-west of America. Elementis – a stock we thought we would own for decades – was sold in its entirety this year because we lost faith in its ten-year prospects after this trip. We constantly seek to better understand the broader industries our companies operate in. In this instance, substantive product developments by a competitor/customer, Sherwin Williams, caused us to question Elementis’ prospects

Thank you for your ongoing support and we wish you a prosperous 2018.

The Bronte Team