Get ready… if history is any guide, 2018 could be a weak year for U.S. and Asian stock markets.

For starters, we’ve been saying for a while that the “Trump rally” is getting old. Maybe more to the point, the MSCI All Country World Index (which reflects the performance of global stock markets) posted an unprecedented streak of monthly gains in 2017 – a streak that can’t go on forever. And U.S. stock market valuations are higher than any other time in history, except for the late ‘90s dotcom bubble.

Today, we’re showing you another indicator that shows we could be in for a below-average year: the U.S. election cycle.

Politics and performance

The economic cycle and market valuations generally play a bigger role than presidential politics in the movements of U.S. markets. But in the past, American presidential elections still have a significant impact on the U.S. stock market. The cycle of anticipated policy changes, economic stimulus, the fantasy that real positive change might happen, and, of course, disgust and despair at politics as usual, all figure into markets.

As we’ve shown you before, U.S. markets have historically done well in a post-U.S. election year, which was 2017. This has little to do with the identity of the person who happens to be sitting in the American White House.

Since 1928, the S&P 500 has risen, on average, by 5.1 percent in a post-election year. In 2017, the S&P 500 rose around 20 percent.

In pre-election years (which we define as the calendar year that’s before the year in which a presidential election takes place), the S&P 500 has risen on average by 12.8 percent.

But, on average, the S&P 500 has seen the worst performance in the second year of a U.S. president’s four-year term (which is 2018 for this cycle).

This cycle holds true in Asia, too.

The U.S. election cycle and Asia’s stock markets

Surprisingly, Asia’s stock markets have been more affected by the American presidential election cycle – especially when a Republican is in power – than the U.S.’s own stock markets. (An important caveat, as I’ll explain below: There isn’t that much history for this, as Asia’s stock markets are a lot younger than those of the U.S.)

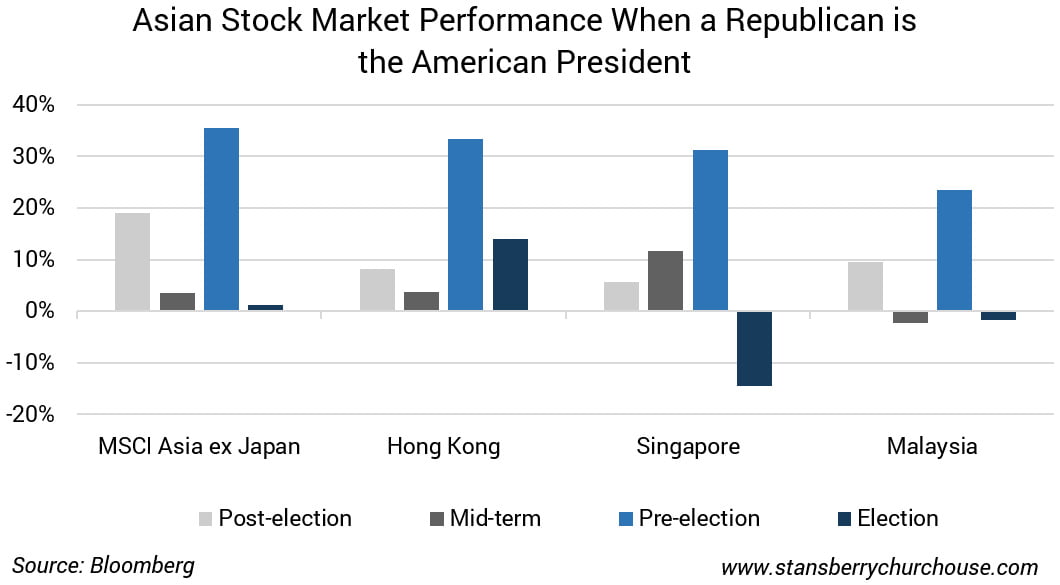

In the past, when a candidate from the Republican party of the U.S. has become the country’s president, Asia’s markets (measured by the MSCI ex Japan Index) overall have performed well during the first year of the new president’s term, rising just over 19 percent on average. In 2017 (the first year of a new Republican party president) the MSCI ex Japan rose nearly twice that, 34 percent.

And like in the U.S., things take off in the third year (which will be 2019) of a Republican president’s four-year term. During this year, the MSCI Asia ex Japan Index has seen average returns of nearly 36 percent. Hong Kong’s stock market has risen nearly 33 percent, Singapore and Malaysia have seen average returns of 31 percent and 24 percent, respectively.

But during the president’s second year (which will be 2018), there’s a slump. The MSCI Asia ex Japan Index has seen average returns of 3.4 percent. Hong Kong’s stock market has risen only 3.6 percent and Malaysia has seen average returns of -2.3 percent. Only Singapore wins in the second year, rising 11.7 percent.

For our purposes in the graph above, we break the election cycle down into four periods:

1. Post-election year: The first calendar year after the U.S. presidential election. That was last year – 2017.

2. Midterm: The second year. This is 2018 in the current cycle.

3. Pre-election: The third year of the president’s term, which is also the year before the next election. This will be 2019 in the current cycle.

4. Election year: The fourth year of the president’s term, and the year in which elections are held. 2016 marked the election year in the previous cycle, and 2020 will be the current cycle’s election year.

However, the sample size for the Asian market results is small. The indexes that we’re using – and Asia’s stock markets – haven’t been around for many four-year American presidential cycles. And broken down by the two major U.S. political parties, the sample size is even smaller.

For instance, the MSCI Asia ex Japan Index has only seen seven U.S. presidential election cycles, covering three Republican presidents and four Democratic presidents. The small number of data points means that historically unusual periods (like big stock market losses during the global economic crisis in 2008, or particularly strong years for the stock market) have a very big impact on average returns.

Why would American politics affect Asia’s stock markets?

Only rarely does American foreign policy towards Asia have a direct impact on stock market performance in Asia. Far more important is the role of American politics on U.S. market movements, and on global stock market sentiment – and therefore also on Asian markets. This may play out in a more important way in smaller, less liquid markets in Asia (where a smaller absolute sum of funds invested or withdrawn can have a far greater impact than in bigger markets). So positive or negative sentiment in the U.S. with respect to American policy, and presidents, might impact smaller Asian markets more than others.

Twitter-happy U.S. President Donal Trump could also impact Asian markets more than usual – and markets could deviate from the election cycle norm. In light of Trump’s unorthodox policies and positions, stock market performance patterns may be completely different over the next three years from the past. And recent changes to the tax code in the U.S. may have a positive impact on markets.

But if the U.S. election market performance cycle remains intact – as it has so far – it’s looking like 2018 could be weak for most Asian markets.