As written by Chain Reaction Research, following the financial crisis of 2007-2008, there has been a growing investor interest in farmland around the world. In Brazil, this interest has been most pronounced in the Cerrado, a large tropical savanna biome that covers more than 20 percent of the country. Here, institutional investors such as pension funds and private equity, real estate firms and agribusinesses have adopted business models that aim to produce value from land appreciation by acquiring land, clearing it from its native vegetation and transforming it into farmland. While land prices in the Cerrado have increased nearly fivefold between 2003 and 2016, there are signs that the farmland real estate market is currently overheated.

These large-scale farmland acquisitions have resulted in significant environmental and social impacts. Between 2013 and 2015, 1.9 million hectares (ha) of the Cerrado was cleared of its native vegetation. Cerrado deforestation contributed to 29 percent of Brazil’s carbon emissions. Moreover, land acquisition in Brazil is linked to a process of grilagem, whereby land deeds are falsified and later sold. Traditional communities have been impacted through forced removals, loss of hunting grounds and other livelihood impacts.

| The Cerrado The Brazilian Cerrado is the biologically richest savanna in the world, home to hundreds of endangered species. It covers more than 20 percent of Brazil’s territory. The savanna’s native habitat and rich biodiversity are being destroyed faster than the neighboring Amazon. As the source of rivers and waterways, the Cerrado functions as a vital source of water for the region as well as many of Brazil’s largest cities. It is also home to many traditional communities that have inhabited the area prior to the agricultural expansion. |

Key Findings

- Financial risks: Brazil’s Cerrado region may be subject to a potentially overvalued farmland real estate market. Indications include 1) a disconnect between farmland and global commodity prices; 2) the financialization of farmland and inflationary effect of the entry of institutional investors; 3) investments moving into areas less suitable for agriculture; and 4) reduced market appetite for deforestation-related soy and other commodities.

- Environmental risks: The Cerrado is one of the most environmentally sensitive areas in the world. Farmland investment models inherently drive the transformation of native Cerrado vegetation into agricultural land. This conversion contributes to increased carbon emissions, threats to biodiversity, reduced drinking water supply for Brazil’s large cities and erratic rainfall.

- Social risks: Illegal land grabs can precede the acquisition of farmland by investors. Through a process known as ‘grilagem’, land is made inaccessible to traditional communities, after which property titles are forged. In several cases, such land is subsequently sold to farmland investors. Traditional communities consequently face negative livelihood impacts. This heightens the risks for violence, social unrest and litigation.

- Risk might remain hidden to investors. Investors in farmland companies may be directly exposed to the risk of stranded land. Given the increased stakeholder attention to deforestation, it may become financially less attractive to transform forested land to farmland. Farmland investment firms generally do not specify whether their portfolio contains forested land.

Growing Global Interest in Farmland

Following the financial crisis of 2008, global interest in farmland has been on the rise. Land Matrix identified 26.7 million ha of farmland transferred to foreign investors between 2000 and 2016 globally (approximately two percent of all arable land worldwide). Cropland expansion can be explained by growing global food demand through population growth and rising incomes in emerging markets, biofuel mandates as well as increased global trade. Investors seeking stable financial returns have turned to the agricultural sector in response to geopolitical instability, low interest rates, and slow economic growth. In 2009, five agricultural strategy funds collectively raised USD 500 million. 2017 data suggests there are currently 51 unlisted agriculture/farmland funds, with total investments of USD 13 billion.

While direct equity or debt financing of agribusinesses is the most common type of investment in the agricultural sector, investors have increasingly turned to a strategy of direct farmland purchases. As explained by the agricultural analyst group Gro Intelligence, “an investment in agriculture and forestry is a claim on two streams of returns: the financial return from crop and harvest income and the capital appreciation of land or timber.” In 2015, TIAA-CREF, a leading US-based retirement and investment services provider, closed its USD 3 billion Global Agriculture II LLC fund, the largest farmland investment fund to date. This fund invests in farmland assets across North America, South America and Australia.

Brazil is one of the five countries with the most international acquisition of agricultural land. International investment and pension funds, as well as domestic agribusinesses and real estate firms have been buying large tracts of land. Consequently, Brazilian farmland prices have increased exponentially in recent years.

The Cerrado, one of the most environmentally sensitive biomes in the world, is at the heart of this farmland investment growth. According to 2017 data by Informa Economics FNP, a consultancy company specialized in the land market in Brazil, land prices in Brazil’s Cerrado increased nearly fivefold between 2003 and 2016 (corrected for inflation). Land holdings are highly concentrated in Matopiba; ten agribusiness and real estate firms control a total area of 1 million ha of farmland. These firms include SLC Agrícola, Agrifirma, BrasilAgro, YBY Agro, Radar, AgriInvest and Terra Santa Agro.

Farmland Investments Include Financial Risks

Institutional investors that are active in the Brazilian land market point to macroeconomic fundamentals as the basis for their investment strategy. The expected growth in global population, paired with a growing demand for protein from meat, dairy and nuts drives interest in farmland in countries such as Brazil. However, several recent trends point to the possibility that the Brazilian farmland real estate market might be ‘overheated’ and prices might be inflated. These indicators suggest potential financial risks for investors with exposure to the Brazilian farmland market, especially in the Matopiba region. The Matopiba region is shown in Figure 1 (below).

Figure 1: Matopiba, comprising of parts of Maranhão, Tocantins, Piauí and Bahia. Source: Florestal Brasil.

Figure 1: Matopiba, comprising of parts of Maranhão, Tocantins, Piauí and Bahia. Source: Florestal Brasil.

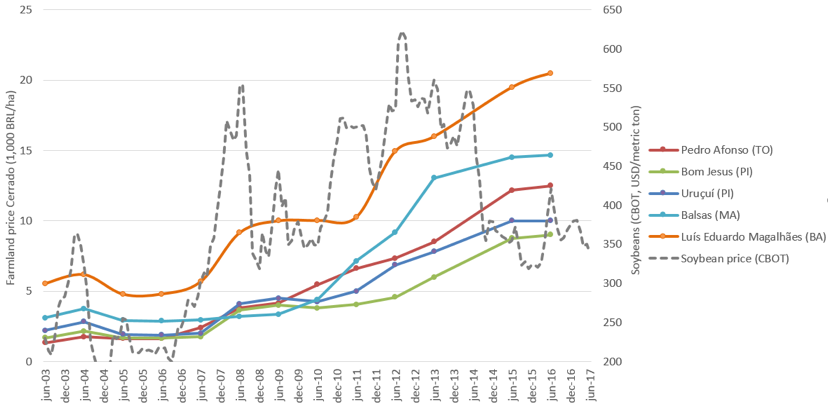

Figure 2: Prices of high productivity Cerrado farmlands (BRL/ha) 2003-2016, vs. global soybean prices 2003-2017 (USD/metric ton). Source: Informa Economics FNP, Index Mundi.

Figure 2: Prices of high productivity Cerrado farmlands (BRL/ha) 2003-2016, vs. global soybean prices 2003-2017 (USD/metric ton). Source: Informa Economics FNP, Index Mundi.

Farmland Prices Disconnected From Commodity Prices

A first indication is the existing imbalance between worldwide commodity prices and land prices in Brazil’s Cerrado. Between 2000-2013, there was a positive connection between land and commodity prices. As shown in Figure 2 (above), since 2011, the drop of global commodity prices from 2011 onward has not been reflected in farmland prices in the Cerrado.

Farmland Financialized; Value Appreciation of Land instead of Revenue from Production

A possible explanation for the disconnect between soy prices and farmland prices is that the drop in global soy prices has been accompanied by financialization of farmland and the entry of institutional investors in the Brazilian land market. Financialization is defined by Krippner as “a pattern of accumulation in which profit-making occurs increasingly through financial channels rather than through trade and commodity production.” In recent years, several rural real estate companies and investment vehicles were created. Their business models focus on value appreciation of farmland rather than – or in addition to – revenues from commodity production.

For example:

- Radar Agriculture Properties (Radar) is a partnership between US-based TIAA-CREF and Brazilian sugar and biofuel producer Cosan. The Joint Venture was established in 2008 to identify and acquire rural properties and convert them into sugarcane and other commodity farms. In 2016, TIAA-CREF increased its equity stake in Radar with USD 326 million. Radar is the main vehicle through which the TIAA-CREF Global Agriculture II LLC Fund invests in Brazilian rural real estate. This USD 3 billion closed end fund holds a total of 64,733 ha in Brazil, of which 16,891 ha in the states of Maranhão and Bahia.

- SLC Agrícola is Brazil’s largest publicly traded farming company, founded in 1977. Some of the 15 farms operated by SLC Agrícola cultivate soy, cotton and corn are in Matopiba. In 2012, SLC Agricola started a subsidiary called SLC LandCo, through a long-term partnership with Valiance Asset Management Limited, a British private equity fund. SLC LandCo acquires, develops and sells agricultural land. Of the 323,000 ha SLC Agricola owns, 87,000 ha is held through SLC LandCo.

- BrasilAgro is a listed rural Brazilian real estate firm, that is active in the soy and sugar value chains. As of June 2017, it holds 225,832 ha of farmland. BrasilAgro’s main business strategy is to acquire rural properties and transforming and developing “underutilized and non-productive” land. It produces soy, corn, sugarcane and livestock on some of its farms, and leases and sells other properties in its portfolio. Most of its properties are in the Cerrado region. The company combines the returns generated from land value appreciation and agricultural production. In 2015, BrasilAgro sold its 27,754 ha Cremaq farm, located in Piauí, for USD 85 million, equivalent to more than USD 3,000 per ha. This equals seven times more than what was paid for it nine years earlier.

Researchers and analysts have pointed to the financialization and entry of institutional investors as having an inflationary effect on farmland prices. They conclude that land as an asset has become the main target of financial investors, with a business model that is not necessarily geared towards agricultural production, but rather towards land speculation.

Investments Move Into Less Fertile Farmland

Farmland investors have increasingly acquired land in Matopiba. Between 2000-2014, soy production in this region grew by 253 percent. Reportedly, the plateaus in this area are preferred as they are more conducive to the development of mechanized agriculture. 2017 data from Informa Economics FNP illustrate that prices of farmland on the plateaus of southern Piauí, such as Uruçuí and Bom Jesus, displayed great appreciation between 2003 and 2016.

However, a 2016 study by the Input Project showed that most of the Cerrado’s already converted land with optimal agronomic conditions for soy can be found outside of Matopiba. Whereas the Input Project identified 25.4 million ha of suitable converted land in total, only 2.8 million ha is located in Matopiba. A total of 6.4 million ha in Matopiba has lower agricultural suitability, have restrictions or are unsuitable for agriculture. The region is known for year-round high temperatures and variability of rainfall.

In recent years, soy producers in Matopiba have suffered from unfavorable climatic conditions, such as droughts and erratic rainfall. In eastern Bahia, soy producers have been faced with four consecutive years of harvest losses caused by periods of droughts from the 2011/2012 to the 2015/2016 season.

The 2016/2017 season has seen a record harvest, with good weather conditions in Matopiba as a contributing factor. However, soy producers are reducing their exposure to the region because of the high climatic volatility. Companies such as Agrifirma Brasil Agropecuaria, SLC Agricola and Terra Santa Agro all took steps to reduce soy production in Matopiba in 2016. In August 2017, SLC Agrícola, which holds several large farms in Piauí and Bahia, cut its exposure to these states to 23 percent down from 34 percent four years ago. This signals that the region that was once touted as the new agricultural frontier, and the area of interest for many farmland investors, has failed to live up to its productivity promise.

Reduced Market Appetite for Deforestation-Related Commodities

A growing number of companies active in agricultural commodity value chains have made public zero-deforestation commitments and stated time-bound ambitions to exclude deforestation from their supply chains. These include large soy traders such as Cargill and Bunge, who are taking active steps to increase traceability, monitor their suppliers and identify deforestation risks. The most recent report by Supply Change shows that 447 companies have made 760 commitments to curb forest destruction in agricultural commodity supply chains. Progress on these commitments is most noticeable in the palm oil and timber supply chains, but the soy supply chain also saw an increase in corporate commitments.

Market actors as well as various other stakeholders also turn to deforestation driven by soy in the Cerrado:

- In a September 2017 Manifesto, a broad coalition of civil society organisations ask markets to stop the deforestation of the Cerrado. The manifesto requests that companies that purchase soy and meat from the Cerrado and investors working in these sectors act immediately to protect the biome.

- In November 2016, Ceres and the UN PRI launched an initiative to tackle global deforestation, with a particular focus on soy from Latin America. Through a new investor working group, the organizations aim to support institutional investors to press food and timber companies to eliminate deforestation.

- In September 2017, Bunge, The Nature Conservancy and other groups launched AgroIdeal, an online database to help purchasers of soy make decisions that discourage farmers from cutting down trees for arable land. It currently contains data on the Cerrado, and aims to include the Amazon region later.

- Also in September 2017, the Good Growth Partnership was launched by the Global Environmental Facility and the United Nations Development Program in an effort to enable sustainable agriculture and reduce deforestation. Matopiba is one of the landscapes where the program will be implemented.

As witnessed in the palm oil sector, the scope, definitions used and implementation of zero-deforestation commitments can rapidly evolve to the point where any deforestation poses a risk of being excluded from certain supply chains. As such, any deforestation event should be regarded as inherently containing the business risk of losing customers.

A consequence of the reduced appetite and growing business risk of deforestation is that undeveloped farms and concessions can become stranded. Such land cannot be developed without violating the sourcing policies of the traders and refiners of agricultural commodities. The farmland investments made in Matopiba and other regions of the Cerrado often contain native forest and savanna vegetation. The deforestation required for soy production on these farms could affect a firm’s market access. As such, the risk of overvaluation of farmland is particularly pronounced for those assets that contain native Cerrado vegetation. For some firms, the financial impacts of the stranded land risk could amount to a 20 percent loss in equity value. Nonetheless, none of the major investors in farmland in Matopiba appears to have a zero-deforestation commitment, nor do they communicate detailed information about the native vegetation of the land in their portfolios.

Farmland Investments Drive Environmental Degradation

Through the process of transforming native vegetation to cropland, the farmland investment model inherently places environmental pressure on the Cerrado biome.

Environmentally Sensitive Cerrado at Risk

The Cerrado is the second largest Brazilian biome following the Amazon. It covers more than 20 percent of Brazil’s national territory, and is the biologically richest savanna in the world. It has over 4,800 endemic plant and vertebrate species. In recent years, deforestation rates in the Cerrado have been higher than in the Amazon. Deforestation rates are rising, leaving the Cerrado highly susceptible to loss of forests and biodiversity. To date, the Cerrado has already lost 46 percent of its natural vegetation. Annual deforestation rates in the Cerrado have accelerated, increasing from 299,000 ha in 2009 to 765,200 ha in 2012 (156 percent). Between 2013 and 2015, another 1.90 million ha of the Cerrado was destroyed.

Soy cultivation is one of the major drivers of increased deforestation in the Cerrado. While global soybean prices have dropped significantly since 2013, the area planted with soybean in Brazil has steadily grown. The Cerrado is known as the last agricultural frontier in Brazil. Between 2000 and 2014, agricultural land in the Cerrado expanded by 87 percent, dominated by soybean production. In the 2013/2014 harvest, more than half (52 percent) of the soybeans produced in Brazil came from the Cerrado. The areas of land that are under production for monoculture, tend to be very large. In the Cerrado the median farm size is 1,000 ha and many companies operate more than 100,000 ha of cropland.

Farmland investment strategies in the region often include the transformation of Cerrado savanna into agricultural land. For example, SLC LandCo’s stated strategy is to ‘monetize the value of its land portfolio and add new productive farmland through land transformation’. Similarly, BrasilAgro’s business model includes a land transformation process, whereby acquired land is cleared and prepared for cultivation. By its very nature, such transformation often requires deforestation of Cerrado lands.

There are multiple environmental impacts of deforestation in the Cerrado.

- Forest-to-cropland conversions in the Cerrado account for 29 percent of Brazil’s carbon emissions between 2003 and 2013. The large-scale cropland conversion in the Matopiba part of the Cerrado between 2010-2013 contributed 45 percent of the total Cerrado forest carbon emissions.

- The Cerrado holds 5 percent of the world’s biodiversity, including over 800 bird species, giant anteaters and armadillos. There are 12 critically endangered species in the Cerrado. According to WWF, biodiversity and ecosystem services are suffering from the expansion of soy.

- With the destruction of the Cerrado savanna, drinking water supply in the cities of Brasília and São Paulo might suffer. This is because the intricate root system of the various grass types function as a sponge that recharges underground aquifers that bring drinking water to some of the most densely populated regions in Brazil. With the conversion to soy and other crops, these underground aquifers are at threat of drying up. Scientist have warned that the conversion in Matopiba might have the most devastating impacts.

- Finally, there is recent evidence that the large-scale deforestations in the Cerrado alters the region’s water cycle system, leading to a vicious cycle of volatile rainfall and higher crop failure.

Investments Drive Land Grabs and Social Impacts

Land is Purchased Through the ‘grilagem’ System

The purchase of farmland in Matopiba has involved illegal land grabs. Through a process known as “grilagem”, lands are acquired and farms established by local businessmen. According to the NGO GRAIN, “grilagem” involves using political connections and false documents to claim title over public lands and forests. Reports describe how land grabbers fence off public lands, evict local people, hire security firms and subsequently acquire property titles through the connivance of local notaries and government officials.

Properties are subsequently sold to large agribusinesses and financial investors. Although the interpretation of the Brazilian Law 5,709 in 2010 imposed strict limits on how much land foreign investors can control, it did not stop them from buying land.

In 2016, in the area of Santa Filomena, the Agrarian Court of the state of Piauí filed a court case against Colonizadora De Carli (CODECA) for alleged illegal land grabbing. CODECA, reportedly connected to grilagem practices, had sold land to large agriculture and real estate firms, including SLC Agrícola and Radar. In this case, the Agrarian Prosecutor for the Court ordered the cancellation of land claims of 124,400 ha by CODECA, on the allegations of illegal land acquisition.

Traditional Communities are Impacted

The process of illegal land titling by ‘grileiros’ and the subsequent acquisition by farmland investors takes place on land that is in use by traditional communities. The Cerrado is home to a large variety of communities, including 80 different indigenous groups. These communities historically use the plateaus of the Cerrado for hunting, gathering and pastoralist activities. This has led to expropriation of land from communities living on these plateaus, and migration to (peri-) urban regions (REDE 2017, unpublished).

Adverse social issues with soy expansion in Matopiba is receiving increasing attention, as illustrated by a recent fact finding mission to the region by over 30 civil society organisations and researchers.

Conclusions

The social and environmental impacts linked to farmland investments could in themselves be enough for investors with ESG criteria to refrain from further investments in farmland in Matopiba. The financial risks that come with these impacts might also be considered by mainstream investors.

| Disclaimer:

This report and the information therein is derived from selected public sources. Chain Reaction Research is an unincorporated project of Aidenvironment, Climate Advisers and Profundo (individually and together, the "Sponsors"). The Sponsors believe the information in this report comes from reliable sources, but they do not guarantee the accuracy or completeness of this information, which is subject to change without notice, and nothing in this document shall be construed as such a guarantee. The statements reflect the current judgment of the authors of the relevant articles or features, and do not necessarily reflect the opinion of the Sponsors. The Sponsors disclaim any liability, joint or severable, arising from use of this document and its contents. Nothing herein shall constitute or be construed as an offering of financial instruments or as investment advice or recommendations by the Sponsors of an investment or other strategy (e.g., whether or not to “buy”, “sell”, or “hold” an investment). Employees of the Sponsors may hold positions in the companies, projects or investments covered by this report. No aspect of this report is based on the consideration of an investor or potential investor's individual circumstances. You should determine on your own whether you agree with the content of this document and any information or data provided by the Sponsors. |