“No act of kindness is too small. The gift of kindness may start as a small ripple

that over time can turn into a tidal wave affecting the lives of many.”

Kevin Heath

The car is loaded with clean clothes and dog food. I’m heading out mid-morning to help load a support truck headed for Houston. Thankfully, my kid’s school has organized the donation drive. It has been heartwarming to watch the countless random acts of kindness in the wake of the current challenges. Much more will be needed in the days ahead. Hang in there, Houston. Across the country and from many parts of the world, a tidal wave of kindness is coming your way. Our collective thoughts and prayers are with you.

Houston’s economy is the fourth largest in the U.S. From an economic perspective, the damage will create a short-term drag on U.S. GDP. Longer term, as the insurance funds kick in, the rebuild will provide an economic boost. Overall, like storms past, it will be a temporary economic bump. Following are a few charts I found interesting and hope you do as well:

Source: WSJ Daily Shot, 9/1/17

Looked at through a global lens, Houston produces more than Sweden, Poland, Norway and South Africa.

Source: WSJ Daily Shot, 9/1/17

The damage and impact is immense. Here is a look at the amount of rain received in just seven hours.

Source: WSJ Daily Shot, 9/1/17

In the wake of Hurricane Harvey, Credit Suisse lowered its Q3 and Q4 GDP forecasts. Here is what CS thinks in terms of economic boost. Note pickup in Q12018 estimate.

Source: WSJ Daily Shot, 9/1/17

Nonetheless, I believe the U.S. economy will remain stuck around 1.50% to 2% annual GDP growth for some time to come. If GDP growth comes from the number of workers and their collective productivity, then this next chart showing U.S. population growth should prove to be a headwind.

Source: WSJ Daily Shot, 9/1/17

Bottom line: Expect the overall trend in U.S. GDP growth to remain low for some time to come. Fewer workers, producing fewer things is not good for growth. Current high global debt and aging demographics will keep growth lower for longer. Economic growth has a high correlation with corporate earnings growth. The equity market remains richly priced and earnings growth is unlikely to change that picture any time soon.

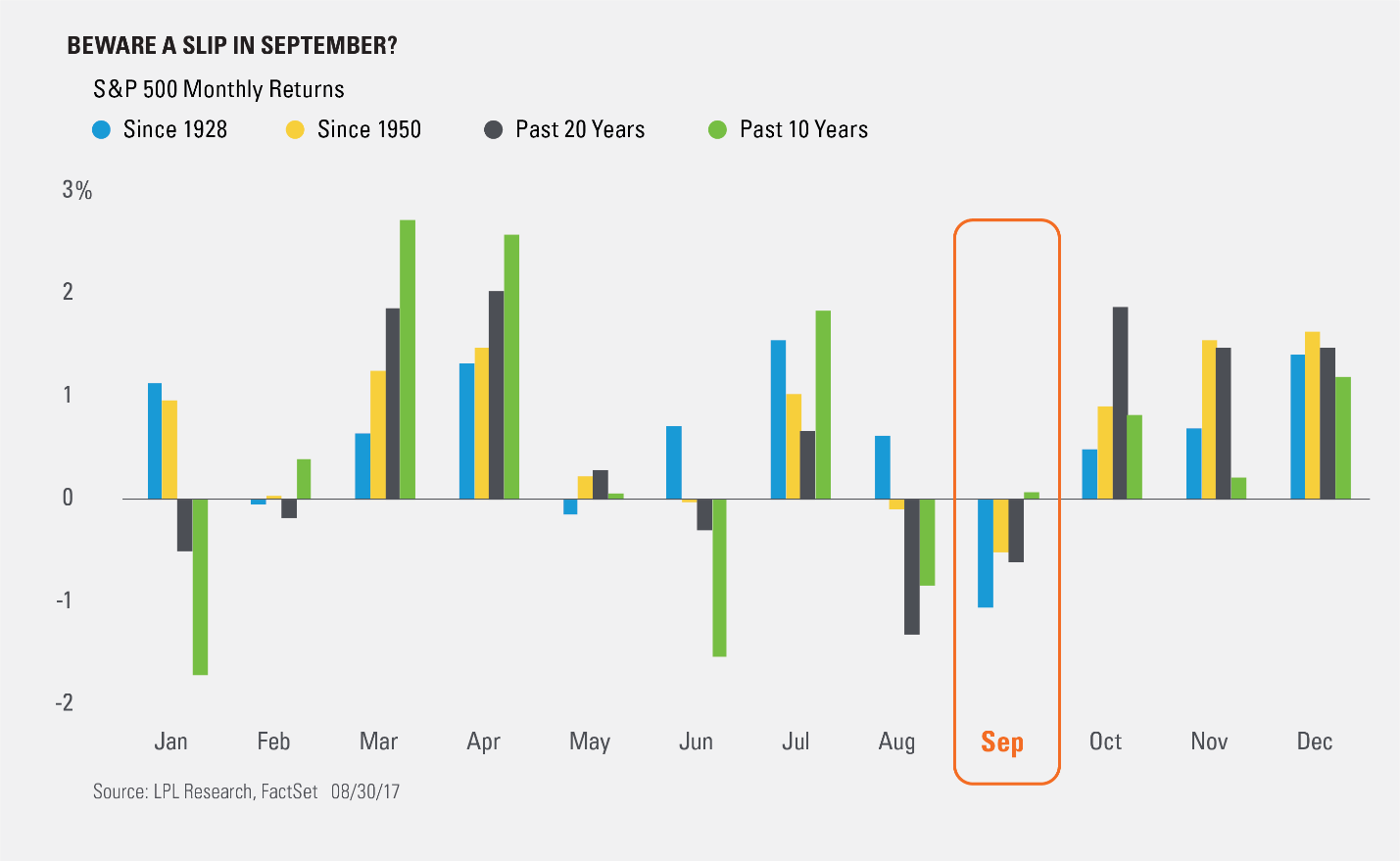

Switching gears, this next chart advises to beware of a slip in September:

Buy a September dip? As you’ll see in the Trade Signals section below, the weight of collective evidence continues to support the continuation of the equity bull market trend. You’ll find a number of my favorite indicators, such as the Ned Davis Research CMG Long/Flat Index, Don’t Fight the Fed and a chart that measures Volume Supply vs. Volume Demand. Bottom line: Should September prove as challenging as periods past, despite the second highest valuation level in history, I remain modestly constructive on equities.

Also, I share with you a short but thoughtful piece from my friends at 720Global. They compare the current Fed stimulus QE period of current policy to the prior three and ask “How Much is Too Much?” Wait until you see their chart. Forward we look and consider, “… the ramifications of a Fed that continues to increase the Fed Funds rate and moves forward with plans to slowly remove QE.”

I believe the trend data can help you both participate in growth and protect against material downside loss. In the Trade Signals section, I share a dashboard that color codes (green is good, red is bad) various market, sentiment and economic indicators. It helps me stay centered on evidence and remove emotion. I hope it helps you as well. See important disclosures below. Not a recommendation to buy or sell any security.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Follow me on Twitter @SBlumenthalCMG.

Included in this week’s On My Radar:

- “How Much is too Much?”

- Trade Signals — August/September Seasonal Challenges Yet Trend Signals Bullish

- Personal Note

“How Much is too Much?”

Data Courtesy: Federal Reserve

Like periods past, we have to wonder what investment behaviors such periods create.

The amount of monetary stimulus increasingly imposed on the financial system creates false signals about the economy’s true growth rate, causing a vast misallocation of capital, impaired productivity and weakened economic activity.

Federal Reserve (Fed) stimulus comes in two forms as shown above. First in the form of targeting the Fed Funds interest rate at a rate below the nominal rate of economic growth (blue). Second, it stems from the large scale asset purchases (Quantitative Easing -QE) by the Fed (orange). When these two metrics are quantified, it yields an estimate of the average amount of stimulus (red) applied during each post-recession period since 1980. It has been almost ten years since the 2008 financial crisis and the Fed is applying the equivalent of 5.25% of interest rate stimulus to the economy, dwarfing that of prior periods.

The graph highlights that the Fed has been increasingly aggressive in both the amount of stimulus employed as well as the amount of time that such stimulus remains outstanding. Amazingly few investors seem to comprehend that despite the massive level of monetary stimulus, economic growth is trending well below recoveries of years past. Additionally, as witnessed by historically high valuations, the rise in the prices of many financial assets is not based on improving economic fundamentals but simply the simulative effect that QE and low interest rates have on investor confidence and financial leverage.

Now consider the ramifications of a Fed that continues to increase the Fed Funds rate and moves forward with plans to slowly remove QE.

Click here for the full piece.

Trade Signals — Gold Looks Good

S&P 500 Index — 2,446 (8-30-2017)

Notable this week:

J.P. Morgan said, “Gold is money. Everything else is credit.” Currently, gold looks good. Both our intermediate and short-term signals remain buys. Investor sentiment has improved. The overall trend evidence for equities remains bullish as does the trend for high quality bonds (the Zweig Bond Model continues to signal lower interest rates and higher bond prices). Our CMG Managed High Yield Bond market trend indicator is in a sell, signaling caution on high yield bond exposure.

We continue to see a “risk on” positioning in the CMG Opportunistic All Asset Strategy with overweight exposures to international developed and emerging market ETFs. For clients, more on that in the Update on CMG Investment Strategies section below.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Click here for the latest Trade Signals.

Personal Note

Years ago I used to send a small book that shared stories of Random Acts of Kindness. When I was talking to my sister Amy this week she told me how she quietly tries to do at least one kind act per day.

“No act of kindness is too small. The give of kindness may start with a ripple that over time can turn into a tidal wave affecting the lives of many.”

My mom taught me, “The more you give, the more you get.” I think that is a universal law. I thought about her when I was talking to Amy. No act of kindness is too small. I’m going to try to be more like Amy.

I’ll heading to Chicago next Tuesday to attend the Morningstar ETF Conference on September 6-8. If you are attending, please send me a quick note. I’d love to connect.

Dallas follows on September 20-21. John Mauldin along with his team of four ETF strategists are presenting to a select group of independent advisors. John will share his outlook, one he calls the “Great Reset” and his approach to navigating the period ahead. You can also learn more . The October advisor event is scheduled for October 25-26. Email [email protected] if you’d like to attend.

Wishing you a wonderful holiday weekend with spirits held high. Fire up that grill and grab an ice cold beer (for me an IPA). Send some love to Houston and celebrate with those you love most. September 1… hard to believe. Time is moving by much too fast.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.