By Daniel Nevins, CFA, Nevins Research, author of Economics for Independent Thinkers

Summary

Auto sales slid further in August.

Some argue that weak auto sales signal an imminent recession.

A broader look at personal consumption yields a different conclusion.

August auto sales (released Friday and charted below) weakened further and should trigger a few recession forecasts. In fact, over the past few months, I’ve read about half a dozen commentaries linking the recent plunge in auto sales to an imminent recession. And I understand the reasoning, but I’ve yet to buy into it.

I agree that car sellers face a degree of demand saturation while potential buyers suffer from credit saturation, or at least that’s what the data seem to show. I also agree that the saturation twins tend to be late-cycle indicators. But I’d like to add another possible explanation for slowing auto sales, one that yields a different conclusion about recession risks.

My view is this: Maybe the sales slump isn’t so much an independent force that’s driving the business cycle but merely a substitution for other types of spending.

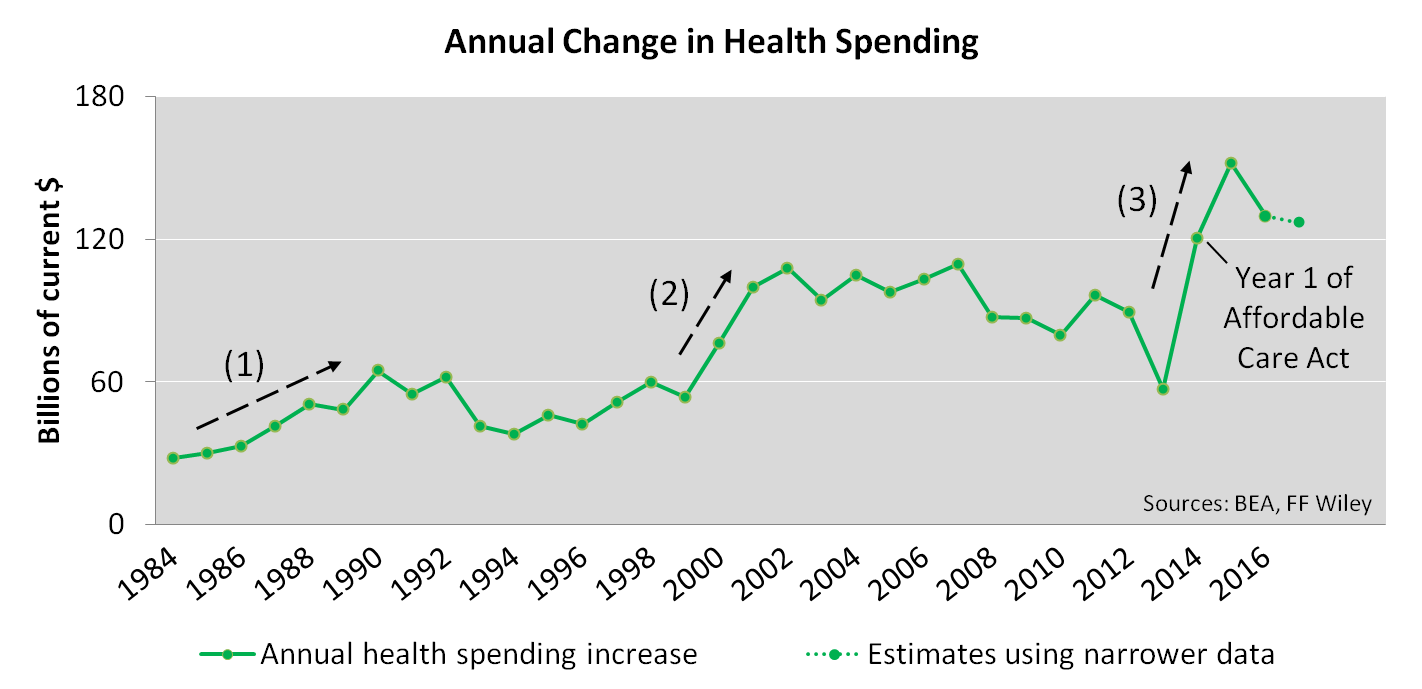

Think, for example, healthcare. Classifying healthcare as a “big ticket” item in the consumer’s basket (seems reasonable), it surely falls in the big three, alongside homes and autos. There’s only so much room in the average middle-class budget for those three items. Changes in outlays for one of the items can easily squeeze the other two. And I think I can demonstrate the sumo battle between healthcare and auto sales with two charts. The first chart shows three separate instances of soaring health spending:

The chart shows that the most recent jump in health spending growth, beginning in 2014, was even bigger than earlier episodes. Of course, 2014 was also the first year of Obamacare. In my view, it stands to reason that Obamacare’s cost effects should eventually prey on other types of spending. Also, the most vulnerable types are those that require large commitments that are difficult to shed, such as lease payments on new cars.

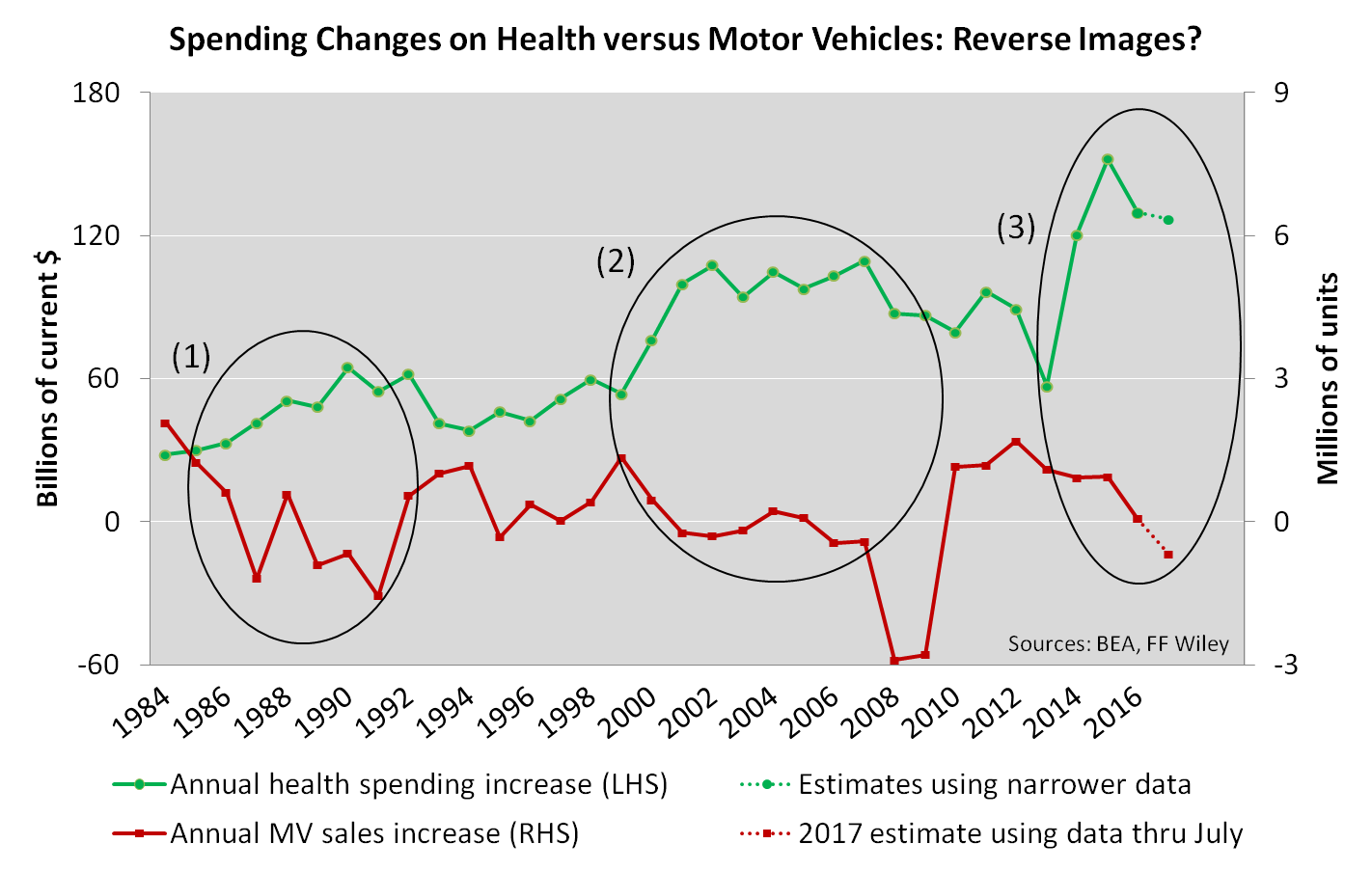

While that may sound speculative, history seems to support my theory. The second chart (below) shows that the recent decline in auto sales, if it continues, would be the third consecutive instance of health and autos occupying opposite ends of the same seesaw.

And how do the charts relate to recession risks?

Well, the math suggests that any hurt felt by those in the auto industry is mitigated - at least on a whole economy basis - by good times being had by those working in healthcare, pharmaceuticals, and insurance. In fact, if I'm right about that substitution, it may even be a net positive for GDP. Consider that each dollar of auto spending scatters among producers of autos and auto components all over the world, whereas a dollar of medical spending tends to be felt more strongly in the United States.

(To be clear, I'm offering only a short-term business-cycle view, not an endorsement of our current health system. I'm not applauding large increases in premiums, co-pays, and deductibles. Those increases belong in the “unintended consequences” column of your Obamacare scorecard).

So, if you haven’t yet traded your old RAV4 for a new 4Runner because you’re shell-shocked by medical premium increases, you may have recycled more of your income back into the domestic economy than you otherwise would have. And the additional income you’re applying to medical costs shows up in GDP, per the charts above. Unfortunately, it also eats into other types of spending. But that fact alone shouldn’t cause you to change your business cycle forecast from expansion to recession. When it comes to recessions, you might put more weight on indicators such as financial conditions, which, if they deteriorate, would tip the scales against many industries at once.

Disclosure:I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.