PT Indofood Sukses Makmur Tbk. (Indofood SM – OTC:PIFMY), listed on the Indonesia Stock Exchange, is the country’s largest food company and the market leader in instant noodles, flour, cooking oils, margarine and fats. Its largest shareholder is First Pacific Co. Ltd., a Hong Kong-listed conglomerate with interests in food, telecom, construction, and natural resources. The Indonesian Salim family controls First Pacific. Both Indofood SM and First Pacific face financial risks from their upstream investments. These material risks include contested land and labor risks associated with their supply chains and reputation risks from their investments in their Singapore-listed oil palm plantation subsidiary Indofood Agri Resources.

Published by Chain Reaction Research, and written Fenneke Brascamp, Aidenvironment; Gabriel Thoumi, CFA, FRM, Climate Advisers; and BrunaTomaidis Lima, Profundo.

Key Findings

- Indofood Sukses Makmur: Indofood Agri’s ESG risks couldnegatively impact the share price of its parentcompany. A stock price decline of 16 percent could materializeif banks and equity investors with ESG policies avoid IndofoodSukses Makmur because of concerns about deforestation andlabor issues at its 74.5 percent controlled subsidiary IndofoodAgri.

- First Pacific: Indofood Agri’s ESG risks could alsonegatively impact First Pacific’s share price. The HongKong-listed conglomerate First Pacific has a controlling 50.1percent stake in Indofood Sukses Makmur and derives 38percent of its revenues from this investment. Because of thesestrong links, banks and equity investors could avoid thisultimate parent company as well.

- A RSPO complaint was recently filed accusing IndofoodAgri of employing child labor and exhibiting poor laborpractices. The company has allegedly undermined job securityfor workers and the freedom of association in trade unions. It isallegedly paying employees below the minimum wage andsetting individual quotas for workers unrealistically high. Also, the company allegedly employs children to assist withharvesting.

- 36 percent of the CPO processed in Indofood Agri’srefineries comes from undisclosed sources, creating bothsupply chain and reputation risks for buyers andinvestors. Simultaneously, various private oil palm plantationcompanies indirectly controlled by Anthoni Salim are developingsupply chain and reputation risks by their deforestation activitiesfor their current and future CPO buyers.

- 42 percent of Indofood Agri Resources’ 549,287 ha totallandbank is contested. Indofood Agri Resources (IndofoodAgri) controls 63 concessions. Six plantations (7 percent of itstotal landbank) allegedly have community conflicts and laborcontroversies. Four plantations (9 percent of its undevelopedlandbank) are located on peat and/or forest areas, potentiallyprohibited from development given Indonesian governmentregulations. Approximately 5,900 ha of peatland burned in 2015on Indofood concessions. 16 plantation companies (29 percentof its total landbank) do not publish concession maps.

| PT Indofood Sukses Makmur Tbk | ||

| Bloomberg ticker | INDF:JK | |

| No. of shares outstanding | 11,662 billion | |

| IDR | USD | |

| Present share price | 8,000 | 0.6 |

| 52Week Low | 9,200 | 0.69 |

| 52Week High | 5525 | 0.41 |

| Market Cap | 70,243 b | 5.27 b |

| Main shareholders | Country | % |

| CAB Holdings | Seychelles | 50.07% |

| Dimensional Fund Advisors | United States | 1.63% |

| Vanguard Group | United States | 1.46% |

| BlackRock Institutional | United States | 1.26% |

| IDR billion | 2015 | F 2016 | F 2017 | F 2018 |

| Revenue | 64,062 | 68,309 | 74,076 | 79,768 |

| EBITDA | 9,230 | 10,517 | 11,635 | 12,923 |

| EBIT | 7,363 | 8,048 | 9,078 | 9,924 |

| Net Income | 2,572 | 4,035 | 4,463 | 5,011 |

| EPS | 293.00 | 469.74 | 507.26 | 567.54 |

| Net Debt | 13,439 | 11,892 | 12,279 | 10,231 |

| Net Debt/ EBITDA | 1.46 | 1.13 | 1.06 | 0.79 |

| Returns | INDF | JKSE |

| 3M Return | 7.25% | -1.53% |

| 1Y Return | 37% | 15% |

| 2Y Return | 6.39% | 0.77% |

Indofood Sukses Makmur: Products and Segments

PT Indofood Sukses Makmur Tbk. (Indofood SM) is the largest foodcompany in Indonesia with a market cap of USD 4.8 billion (IDR 65.4trillion). The company dominates the Indonesian instant noodles andflour markets. It is also a significant producer of baby foods, snackfoods, sauces, seasonings and biscuits. Moreover, Indofood SM is theIndonesian market leader for branded cooking oils, margarine andfats – products mostly made from palm oil. The company operates anational distribution network to supply these products to shopsacross Indonesia.

In fiscal year 2015, Indofood SM total revenue was USD 4,789million (IDR 64,062 billion), resulting in operating income of USD531 million (IDR 7,108 billion). Their net profit amounted to USD222 million (IDR 4,524 billion), equaling a 4 percent net profitmargin. Indofood SM generates 92 percent of its revenues from theIndonesian market. It generated smaller export revenues from otherAsian markets.

Indofood SM has grouped its business activities in five segments:

- Consumer Branded Products: This segment produces adiverse range of consumer branded products including noodles, dairy, snack foods, food seasonings, nutrition and special foodsand beverages. Brand names include Pepsi, Maggi, Indomie, Indomilk and Chitato. The holding company for this segment, PTIndofood CBP Sukses Makmur Tbk., is listed separately on theIndonesia Stock Exchange.

- Bogasari: This segment produces wheat flour and pasta.

- Agribusiness: The holding company for this segment isSingapore-listed Indofood Agri Resources Ltd., which operatesoil palm plantations in Indonesia with a total planted area of246,359 ha and 24 palm oil mills producing one million tons ofCPO per year. Its five Indonesian palm oil refineries have a totalannual CPO processing capacity of 1.4 million tons. IndofoodAgri has a leading position in the Indonesian branded cookingoil, shortening and margarine markets. Its brands includeBimoli, Delima, Happy, Palmia and Amanda. It also operatesrubber and sugar plantations.

- Distribution: This segment operates an extensive distributionnetwork in Indonesia, distributing the majority of its ownconsumer products, as well as third-party products. It includesmore than 1,100 distribution points to retail outlets acrossIndonesia.

- Cultivation and Processed Vegetables: Singapore-listedChina Minzhong Food Corporation (CMFC) operates thissegment. It produces and processes vegetables in China. Indofood SM has announced that it is selling its majority positionin CMFC. Marvellous Glory Holdings, controlled by AnthoniSalim, purchased 99.57 percent of CMFC for a total sum of SGD783 million in November and December 2016.

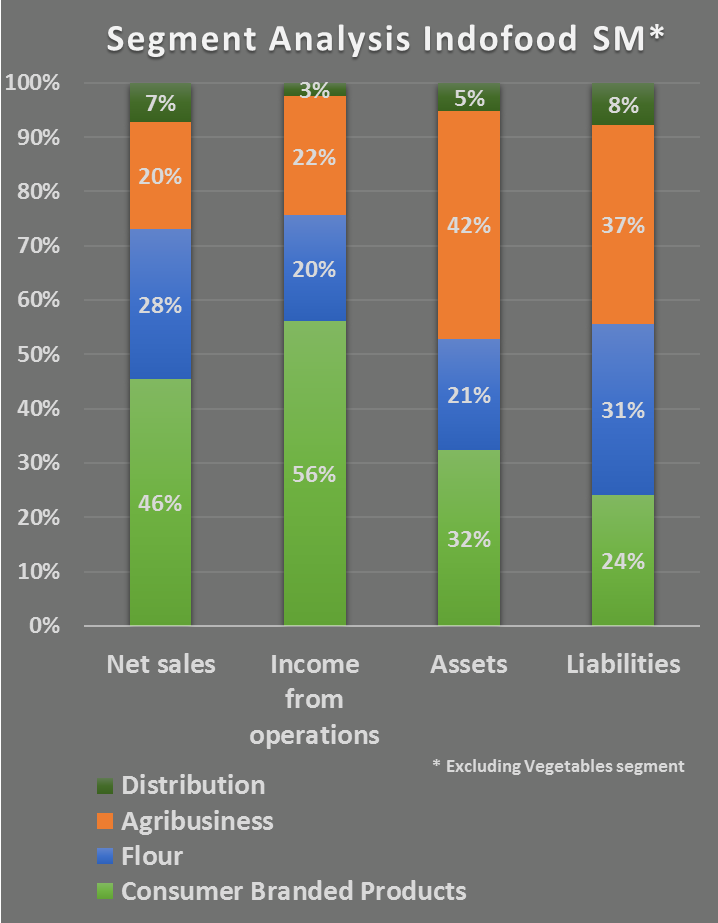

The Consumer Branded Products (CBP) segment accounted for 46percent of Indofood SM’s net sales (IDR 63,594 billion) in 2015, excluding its Cultivation and Processed Vegetables segment. TheCBP segment is more profitable than the other segments. Itcontributed 56 percent to income from operations. Return on assets (ROA) for this segment are high given that it accounts for only 32percent of total assets and its leverage is low at 24 percent of totalliabilities. The oil palm plantations and palm oil refineries in theAgribusiness segment account for 20 percent of net sales and 22percent of operational income, while using 42 percent of total assetsand 37 percent of total liabilities. This segment is less profitable andmore leveraged than the CBP segment.

Salim Family Businesses: History

Anthoni Salim inherited the family business from his father SudonoSalim. Sudono Salim was a close friend and business partner of ex-President Suharto. In the 1990s, the Salim family businessesaccounted for 5 percent of Indonesia’s economic output withinterests in food processing and marketing, automotive, chemicals, construction and building materials, real estate, telecommunications, financial services and trading. In the 1990s, via a web of offshorecompanies, the group acquired concessions to develop 1.1 million haof land into oil palm plantations.

When the Asian financial crisis occurred in 1998, non-performingdebts almost bankrupted Bank Central Asia. The Salim familycontrolled Bank Central Asia. At the time, it was the largest privatebank in Indonesia. The Indonesian Bank Restructuring Agency (IBRA) saved the bank from collapse because of its non-performingdebts. The Salim family was forced to transfer its 25 oil palmplantations, with a total planted area of 260,000 ha, together withits oleochemical businesses to IBRA as compensatory payment. IBRAsold these 25 plantations to the Malaysian company KumpulanGuthrie. Kumpulan Guthrie later merged with Sime Darby.

During this period, the Salim family succeeded in maintaining controlover its profitable flagship company PT Indofood Sukses Makmur. Asa producer of instant noodles, cooking oil, margarine and other foodproducts, this company was the largest Indonesian domestic buyerof palm oil. Indofood SM started to rebuild its oil palm plantationactivities to secure upstream supply. It acquired a majority stake inthe Indonesia Stock Exchange-listed plantation company PP LondonSumatra Indonesia. To attract foreign investors, these plantationswhere then grouped together with the Indofood palm oil refineriesunder Indofood Agri Resources. Indofood Agri Resources was listedon the Singapore Exchange in 2006 through a reverse take-over.

Salim Family Businesses: Structure and Governance

Market capitalization and enterprise value of Salimcompanies (million USD, January 2017)

| Company | Market cap | EV |

| First Pacific | 3,197 | 12,940 |

| Indofood Sukses Makmur | 5,204 | 8,110 |

| Indofood CBP | 7, 483 | 7,152 |

| Indofood Agri Resources | 548 | 1,874 |

| Salim Ivomas Pratama | 595 | 1,441 |

| PP London Sumatra | 860 | 810 |

To maintain control over its diversified companies while seekingforeign investors, the Salim family created a complicated structureincluding many listed and unlisted onshore and offshore companies. On the left is shown a simplified overview of the group structure, focusing on Indofood SM and some of the subsidiaries related to thepalm oil business, and leaving out many other businesses andintermediate vehicles.

Indofood SM and two Salim offshore companies own 74.49 percentof Singapore-listed Indofood Agri Resources Ltd, which is the holdingcompany for the oil palm plantations and palm oil refineries. Indofood Agri itself controls two plantation holding companies, whichare both listed on the Indonesia Stock Exchange. PT Salim Ivomas Pratama Tbk, which is 79.99 percent owned by Indofood Agri and itsparent company, manages almost all activities of Indofood Agri. Thecompany has a market value of USD 595 million (IDR 8.07 trillion).

In turn, Salim Ivomas Pratama owns 59.5 percent of PT PP LondonSumatra Indonesia Tbk. This is one of the oldest plantationcompanies in Indonesia. Its market value is USD 873 million (IDR11.8 trillion). Aidenvironment calculations estimate the totallandbank of Indofood Agri at 549,287 ha, of which 34 percent areowned by PT PP London Sumatra and 52 percent by PT Salim IvomasPratama. The ownership of the remaining 14 percent is unknown.

Indofood SM also owns 80.53 percent of Indonesia Stock Exchange-listed Indofood CBP Sukses Makmur. Indofood CBP Sukses Makmurcontrols the Consumer Branded Products segment of the group. Ithas joint ventures with major foreign food companies. PT NestléIndofood Citarasa Indonesia is a joint venture between Indofood CBPand Nestlé SA, producing culinary products. With the snacks andbeverages giant PepsiCo, Indofood CBP has the snack foods jointventure PT Indofood Frito-Lay.

First Pacific Subsidiaries

| Company | Country | Industry |

| Indofood SM | Indonesia | Food |

| Goodman Fielder | Hong Kong/ Singapore | Food |

| Philex Mining | Philippines | Mining |

| Roxas Holdings | Philippines | Mining |

| Metro Pacific | Philippines | Infrastructure |

| PLTD | Philippines | Telecom |

| Global Business Power | Philippines | Infrastructure |

| Meralco | Philippines | Infrastructure |

Main Salim family offshore holding companies

| Company | Country |

| Asian Capital Finance | British Virgin Islands |

| CAB Holding | Seychelles |

| First Pacific | Bermuda |

| First Pacific Investments | Liberia |

| First Pacific Investments (B.V.I.) | British Virgin Islands |

| Indofood Singapore Holdings | Singapore |

| Salerni International | British Virgin Islands |

First Pacific owns 50.07 percent of Indofood SM. First Pacific is aBermuda-registered conglomerate listed on the Stock Exchange ofHong Kong. First Pacific market value is USD 2.9 billion. Its businessinterests range from telecommunications to food, infrastructure andmining across the Asia-Pacific region. Indofood Sukses Makmuraccounts for 38 percent of First Pacific’s turnover. Anthoni Salimowns 45.03 percent of First Pacific through various offshore vehicles.

The ownership structure of the Salim family businesses, with itsmany listed subsidiaries, aims to optimize the family’s interests. Thestructure focuses on attracting outside financing without losingcontrol. A small group of managers controls these companies, whichderive their sales and market values to a large extent from the sameassets. This creates an imbalance of information between thedominant shareholder – the Salim family – and other investors aswell as potential conflicts of interests, exacerbated by frequent “related party” transactions.

Indofood Agri Resources: Palm Oil Supply Chain Risks

CPO sales Indofood Agri Resources

| Market | Tons | Revenue (IDR bln) | Price (IDR mln/ton) |

| External | 441,900 | 5,419 | 12.3 |

| Internal | 540,100 | 3,730 | 6.9 |

| Total sales | 982,000 | 9,149 | 9.3 |

Indofood SM describes its subsidiary Indofood Agri Resources as “one of the largest diversified and integrated agribusiness groups inIndonesia”. Indofood Agri Resources operates oil palm plantations, CPO mills and refineries. But in reality the vertical integration is lessstrong than suggested. According to Indofood Agri, the Plantationssegment sells 55 percent of its CPO to the Edible Oils and Fatssegment and 45 percent to external customers. As a result, therefineries source a 36 percent of their CPO supply from undisclosedthird party suppliers.

The segment revenues reported by the company seem to suggestthat the company’s refineries actually rely even more on externalsuppliers. This is because the reported 55 percent of the CPO volumesold to the refineries yields only 41 percent of the turnover of thePlantations segment. This means that this CPO would be soldinternally for IDR 7 million/ton, while the CPO sold to externalcustomers would yield IDR 12 million/ton. This is not realistic as theaverage CPO market price in 2015 was IDR 7.5 million/ton. Onepossible explanation for this discrepancy is that Indofood Agri inreality sold less than 55 percent of its CPO to its own refineries, increasing its refineries’ reliance on external suppliers.

The extent to which Indofood Agri enforces its own sourcing policyremains unknown. Currently, the company does not follow industrybest practices of publishing lists of its suppliers. While innovativecompanies that are market leaders prohibit development on peatregardless of depth and High Carbon Stock (HCS) forest, IndofoodAgri still allows conversion of secondary forest and peat up to threemeters.

This creates material supply chain risks for Indofood Agri Resources, which can spread to other businesses controlled by Anthoni Salim. In2015, IDR 3,854 billion (28 percent) of Indofood Agri total saleswere to related parties. Of this percentage, 11 percent was sold asedible oils and fats products to Indofood CBP, to be furtherprocessed into products like noodles and baby food. Another 2percent was sold to other subsidiaries of Indofood SM – most likelythe Distribution segment – while another 15 percent was delivered toother Salim-controlled businesses.

| First Pacific Co. Ltd. | ||

| Bloomberg ticker | 142:HK | |

| No. of shares outstanding | 4,281 million | |

| HKD | USD | |

| Present share price | 5.80 | 0.75 |

| 52Week Low | 6.35 | 0.82 |

| 52Week High | 4.7 | 0.61 |

| Market Cap | 24,854 M | 3,203 M |

| Main shareholders | Country | % |

| First Pacific Investments | Liberia | 18.46% |

| First Pacific Investments (BVI) | BVI | 14.79% |

| Anthoni Salim | Indonesia | 11.73% |

| Brandes Investment | USA | 7.94% |

| IDR billion | 2015 | F 2016 | F 2017 | F 2018 |

| Revenue | 6,437 | 6,557 | 7,044 | 7,604 |

| EBITDA | 1,009 | 1,209 | 1,320 | 1,574 |

| EBIT | 672.90 | 828.15 | 928.65 | 1,006 |

| Net Income | 293.90 | 276.93 | 291.16 | 389.94 |

| EPS | 0.07 | 0.07 | 0.06 | 0.09 |

| Net Debt | 4,750 | 3,983 | 3,691 | 3,090 |

| Net Debt/ EBITDA | 4.71 | 3.29 | 2.80 | 1.96 |

| Returns | 142 | HIS |

| 3M Return | -2.19% | 1.05% |

| 1Y Return | -18% | 21.77% |

| 2Y Return | -26% | -5.78% |

Anthoni Salim Private Plantations: Palm Oil Supply ChainRisks

Anthoni Salim controls indirectly various private oil palm plantationsnot owned by Indofood Agri Resources. Some are producing CPO, while others are under development. Salim’s ownership ties meanthese plantations might sell palm oil to Indofood Agri’s refineries. Several of these privately owned plantations are involved indeforestation and peat development. This could amplify supplychain, reputation and regulatory risks for Indofood Agri and IndofoodSM. Some examples are described below.

West Kalimantan: Clearing Peatland Contrary to IndonesianPolicy

PT Duta Rendra Mulya (PT DRM) and PT Sawit Khatulistiwa Lestari (PT SKL) operate in the Sintang district in West Kalimantan with acombined concession area of 19,595 ha. Anthoni Salim’s controllingstakes in these companies are concealed through complex layers ofownership.

From 2011 to 2015, 4,857 ha were cleared by PT SKL and PT DRM. Of this area, 4,300 ha (89 percent) were still forested in early 2013. The deforestation maps are available in Chain Reaction Research’spublished report on Indofood Agri Resources.

The Ministry of Environment and Forestry banned the developmentof peatland for oil palm development in November 2015 stating, “land opening or new land clearing within peatland for plantationpurposes is not allowed anymore”. But satellite imagery shows thatfrom September 2015 to September 2016, in violation of thepeatland moratorium, PT SKL and PT DRM cleared 6,277 ha.

Both plantation companies have commenced planting. They will mostlikely sell their fresh fruit bunches to the closest mills owned by theWings, Lyman, and Incasi Raya Groups, all of which rely on refinerswith NDPE policies such as Wilmar, Musim Mas, Golden Agri-Resources and others. The latter will now likely instruct these thirdparty suppliers to exclude Salim’s subsidiaries from their supplybase. PT SKL and PT DRM will have to invest in their own CPO millsto access markets. Other than Wilmar’s CEKA refinery in Pontianak, the only refinery facility in the province and proactivelyimplementing Wilmar’s NDPE policy.

East Kalimantan: Clearing Orangutan Habitat

In 2012, the Centre for Orangutan Protection (COP) filed a formalcomplaint against PT Gunta Samba Jaya (PT GSJ) in East Kalimantanfor the clearing of orangutan habitat inside the concession. COPbelieved that this was a Salim Ivomas Pratama/Indofood Agrisubsidiary given on-the-ground reports. Indofood Agri’s CEO flatlydenied in public that the company was an Indofood Agri or SalimIvomas Pratama subsidiary. A Salim family member successfullyresolved the case.

West Papua: Near-Term Deforestation Risk

In 2016, the Indonesian NGO MIFEE traced the ownership of four oil palm plantation companies in West Papua to an offshore trust with aSalim address – Jalan Ahmad Yani kavling 23 No. 15, Jakarta. This isthe same address of the Salim owned plywood business PT KayuLapis Asli Murni (Kalamur). Some of the West Papua companies’ executives were previously part of the management of Salimbusinesses. The four plantation companies have acquired plantationconcessions covering a total area of 135,620 ha. 86 percent of the135,620 ha total concession’s landbank remains undeveloped. It iscovered by forest and peatland. Any further development isexpected to escalate deforestation and deforestation related supplychain risks.

Indofood Agri: Contested Land

While Anthoni Salim’s privately owned plantations exhibitsustainability risks, similar issues occur in Indofood Agri’s 63 palmoil concessions estimated at 549,287 ha, of which 246,359 ha (45percent) is already planted with palm oil. According to Indofood Agri, as of December 2015 the company had approximately 25,000 ha ofland available for future palm oil developments. The remaining277,928 ha includes community agriculture, mining, timber andother undevelopable land.

Chain Reaction Research partner Aidenvironment’s data shows that42.4 percent of Indofood Agri’s landbank is contested. This includesconcessions with remaining peat and forest, reported environmentaland social issues, and the absence of maps. This also comprisesseveral RSPO certified concessions – estimated at 42,000 ha. Formore information see Chain Reaction Research’s published report onIndofood Agri Resources.

Indofood Agri Resources: Labor Concerns and Child Labor

In October 2016, Rainforest Action Network and its local partnerslodged a formal complaint against Indofood’s subsidiaries PP LondonSumatra Indonesia and Salim Ivomas Pratama. The complaintfocused on labor violations on multiple PP London Sumatra Indonesiaplantations. These alleged labor violations are in contravention of theRSPO Principles & Criteria and violations of the RSPO Code ofConduct.

According to the complaint, Indofood Agri violated more than 20Indonesian labor laws on two plantations in North Sumatra. Theseviolations may be systemic in nature. Among the exploitativepractices documented are:

- Child labor

- Exposure to highly hazardous pesticides

- Payment below the minimum wage

- Long-term reliance on temporary workers to fill core jobs

- Use of company-backed unions to deter independent labor unionactivity

The complainants requested that the RSPO membership status of thetwo Indofood Agri subsidiaries be suspended until transparentactions are taken to resolve the violations. A RPSO ruling is expectedin 2017. In the meantime, Accreditation Services International (ASI) retracted the accreditation of Indofood’s certification body, SAIGlobal, in December 2016.

Based on NGO community experience with the company, IndofoodAgri’s management is expected to pursue a highly defensivestrategy, which may increase the probability of a group suspension, or a voluntary retreat from RSPO. If the company were suspendedfrom the RSPO, it would be excluded from certified sustainable palmoil supply chains. Indofood Agri might lose a price premium for 38percent of its total CPO production. But as was shown by the 2016 RSPO IOI Corporation case, an initial suspension may magnify intoan unexpected and uncontrollable flow of interventions by investors, buyers, joint venture partners and consumers.

Indofood Sukses Makmur: Equity and Debt Structure

At the end of fiscal year 2015, Indofood SM’s enterprise valueamounted to USD 5,393 million (IDR 74,730 billion). Shareholderfunds accounted for 61 percent, minority interests contributed 21percent and the net debt 18 percent. The company‘s total debtconsists of 16 percent bonds and 80 percent bank loans.

Indofood Sukses Makmur: Equity Investors Face ReputationRisks

Indofood SM is 50.07 percent owned by First Pacific, via CABHoldings. The remaining Indofood SM free float shares, 49.03percent, are owned by a number of foreign and domestic investors. Figure 1 below lists the most important outside equity investors inIndofood SM.

| Investor | Country | Holding |

| Vanguard Group | United States | 1.63% |

| BlackRock | United States | 1.26% |

| Dimensional Fund Advisors | United States | 1.63% |

| Macquarie Funds Management | Hong Kong | 0.43% |

| Pictet Asset Management | Switzerland | 0.31% |

| Causeway Capital Management | United States | 0.28% |

| PGGM Vermogensbeheer | Netherlands | 0.28% |

| Total | 4.19% |

Figure 1: Indofood SM’s Equity Investors

Indofood SM’s direct and indirect ownership of concessions and CPOsuppliers with contested land and labor practices may violate theseinvestors’ No Deforestation, No Peat, No Exploitation (NDPE) policies. This possible violation may drive up Indofood SM’s cost ofequity.

For example, the American fund manager Dimensional FundsAdvisors, who recently divested palm oil positions with similarfinancial risks from two of its portfolios, has a 1.63 percentownership stake in Indofood SM.

Indofood Sukses Makmur: Financial Risks for Banks

| Bank | Country | Value (USD million) |

| Bank Central Asia | Indonesia | $454.9 |

| Bank Mandiri | Indonesia | $117.7 |

| Bank of Tokyo-Mitsubishi | Japan | $70.0 |

| Citibank | United States | $88.3 |

| DBS | Singapore | $163.3 |

| Mizuho Bank | Japan | $311.8 |

| Rabobank | Netherlands | $17.9 |

| Standard Chartered | United Kingdom | $4.8 |

| Sumitomo Mitsui Bank | Japan | $48.6 |

| UOB | Singapore | $141.1 |

| Total | $1,418 |

Figure 2: Indofood SM’s Outstanding Bank Loans, end of FY 2015

Indofood SM (INDF) and Indonesian market index return (JKSE)

| Indicator | INDF | JKSE |

| 1M return | -4.2% | -1.88% |

| 3M return | -14.99% | -5.08% |

| 1Y return | 49.04% | 13.13% |

As net debt accounts for 18 percent of the company’s enterprisevalue and bank loans account for 80 percent of its total debt, banksare important stakeholders in Indofood SM. Indofood SM’s bankloans outstanding at the end of 2015 are listed above in Figure 2.

Indofood Sukses Makmur: Underperforms its Peer Group

Stronger IDR pushed up Indofood SM’s net profit by 29 percentyear-over-year for the six months ending June 30, 2016, as thecompany stemmed losses on foreign-currency denominated debt. The company reported a USD 169 million (IDR 2.23 trillion) profit. Finance expenses declined to IDR 803 billion from IDR 1.48 trillion. Figure 3 below compares the key ratios of Indofood SM to its peergroup.

| Company | P/E2016 | P/E2017 | EV / EBITDA2016 | EV / EBITDA2017 |

| Indofood SM | 16.35 | 15.49 | 9.55 | 8.75 |

| Unilever Indonesia | 45.06 | 41.11 | 31.59 | 28.39 |

| Mitra Adiperkasa | 45.37 | 24.99 | 8.94 | 7.75 |

| Nippon IndosariCorpindo | 29.17 | 24.49 | 15.44 | 13.00 |

| Mayora Indah | 29.06 | 24.74 | 16.29 | 14.28 |

| Peer Mean | 37.17 | 28.84 | 18.06 | 15.85 |

| Peer Median | 37.12 | 24.87 | 15.86 | 13.64 |

| Food Products | 20.47 | 17.09 | 11.94 | 10.43 |

Figure 3: Comparison of Indofood SM with its Peer Group – Source: Thomson Reuters

As shown above in Figure 3, Indofood SM underperforms versus itspeers and consensus estimates. Indofood SM has P/E andEV/EBITDA ratios below its peer group for fiscal year 2016 and fiscalyear 2017. This shows that expectations for Indofood’s performanceare already lower than for its peers. Additional negative informationmay also severely affect its equity returns.

Indofood Sukses Makmur: Equity Valuation

Indofood Agri’s contested landbank and labor issues may negativelyimpact Indofood SM’s financial returns and its equity valuation. Indofood Agri is 74.49 percent owned by Indofood SM and accountsfor 22 percent of Indofood SM’s operational income. Also, 13 percentof Indofood Agri’s palm oil sales are to other subsidiaries of IndofoodSM.

Because of this close integration, Indofood SM’s lenders andinvestors could conclude that the company is contradicting their ESGlending and investing policies through these financially materialupstream relationships. These reputational risks could result inactivities similar to Dimensional Funds Advisors recent divestmentactivity. The threat of losing banks and investors could consequentlyraise the average costs of capital of Indofood SM.

Assuming a small increase of 5 percent in the cost of capital, due tothe ESG risks surrounding one of Indofood SM’s subsidiaries, adecrease of 16 percent of the market capitalization of Indofood SMwould be possible.

First Pacific: Equity and Debt Structure

In FY2015, Indofood SM’s parent company First Pacific had anenterprise value of USD 11,935 million (HKD 92,504 million). Shareholder funds accounted for 24 percent, minority interests for37 percent and the net debt contributed 39 percent. The largepercentage of minority interest that finances First Pacific representsthe equity investors in First Pacific’s listed subsidiaries, includingIndofood SM. The 39 percent net debt to total capital ratio, and anet debt to EBITDA multiple of 4.24x, makes its bondholders andlenders extremely important financiers of First Pacific.

First Pacific: Equity Investors Face Reputational Risks

First Pacific is 45.03 percent owned by Anthoni Salim and hisbusiness partners, the other 54.97 percent of the shares are ownedby other investors. First Pacific’s indirect and direct investment inIndofood Agri’s contested land and labor risks may violate the ESGpolicies of these investors, leading to divestments. This developmentmay drive up First Pacific’s cost of equity. Figure 4 below lists themost important institutional investors in First Pacific.

| Investor | Country | Shareholding |

| Brandes Investment Partners | United States | 7.94% |

| Lazard Asset Management | United States | 6.96% |

| Vanguard Group | United States | 0.98% |

| Nordea Funds | Sweden | 0.83% |

| Blackrock | United States | 0.72% |

| Total | 17.43% |

Figure 4: First Pacific’s Equity Investors

First Pacific: Financial Risks for Banks

As net debt accounts for 39 percent of the First Pacific’s enterprisevalue and banks account for 50 percent of its total debt, banks areimportant stakeholders of First Pacific. Figure 5 below lists banksproviding loans to First Pacific in the past four years.

| Bank | Country | Year | Value (USD million) |

| Bank of America | United States | 2014 | $40 |

| Bank of Philippine Islands | Philippines | 2012 | $40 |

| China BankingCorporation | Philippines | 2012 | $30 |

| HSBC | UnitedKingdom | 2014 | $40 |

| Malayan Banking | Malaysia | 2014 | $40 |

| Metropolitan Bank & Trust | Philippines | 2012 | $50 |

| Mizuho Financial | Japan | 2014 | $40 |

| Sumitomo Mitsui Financial | Japan | 2014 | $40 |

| Total | $314 |

Figure 5: First Pacific’s Bank Loans 2012-2016

Bank of America, HSBC and others have policies against financingdeforestation and child labor. First Pacific and its subsidiaries’ practices are likely violating these. If these banks decide to avoidfurther lending to First Pacific, this might lead to an increase in thecost of debt. Even a small increase of 5 percent in the cost of capital, due to the ESG risks surrounding one of First Pacific’s subsidiaries, can lead to a decrease 35 percent in the market capitalization ofFirst Pacific. Its high leverage contributes to the significant decline inits stock price, as a result of higher costs of capital.

Disclaimer: This report and the information therein is derived fromselected public sources. Chain Reaction Research is anunincorporated project of Aidenvironment, Climate Advisers andProfundo (individually and together, the “Sponsors”). The Sponsorsbelieve the information in this report comes from reliable sources, but they do not guarantee the accuracy or completeness of thisinformation, which is subject to change without notice, and nothingin this document shall be construed as such a guarantee. Thestatements reflect the current judgment of the authors of therelevant articles or features, and do not necessarily reflect theopinion of the Sponsors. The Sponsors disclaim any liability, joint orseverable, arising from use of this document and its contents. Nothing herein shall constitute or be construed as an offering offinancial instruments or as investment advice or recommendationsby the Sponsors of an investment or other strategy (e.g., whether ornot to “buy”, “sell”, or “hold” an investment). Employees of theSponsors may hold positions in the companies, projects orinvestments covered by this report. No aspect of this report is basedon the consideration of an investor or potential investor’s individualcircumstances. You should determine on your own whether youagree with the content of this document and any information or dataprovided by the Sponsors.