Every investor wants to know, “How high will markets go and when will they get there?”

The simple answer is, “The market’s future is dependent on events which are unpredictable.” This makes predicting market levels and even individual stock prices day-to-day a fool’s errand. Longer term is even more uncertain. Uncertain as market forecasting is, there are long-term trends which have proved generally reliable as guidelines. The Trade Weighted US$ Index Major Currency and the T-Bill/10yr Treasury Rate Spread are two of the most important guidelines today.

First, the US$. One of the significant unpredictable events which is impacting markets today is the strengthening of the Trade Weighted US$ Index Major Currency to a 37% premium of its historic trend. The long-term chart includes the price of West Texas crude oil which has had an inverse correlation with the US$. The Trade Weighted US$ Index Major Currency is in a long-term decline relative to our major trading currencies of ~-0.86%, annually. This is shown as the DASHED BLACK LINE. Contrary to much that is in the media, a declining US$ reflects the intellectual creativity which occurs in a Free Market Democracy. Financially, in order to meet the demands of its own citizenry, inventive societies build inherent wealth and costs which require sourcing low value manufacturing in lower cost countries. The process of establishing overseas manufacturing and importation of goods results in raising the currencies of those countries relative to one’s own. This results in the most continuously vibrant society as having the weakest currency over the long-term. The long-term Trade Weighted US$ Index Major Currency shows that peaks in the US$ have diminished in magnitude since 1973. A diminishing series of US$ peaks as shown by the large gray arrow(above) indicates that there are an increasing number of investment opportunities globally over time. The US is less and less the only option. US export of its standard of living has raised the importance of many currencies over time.

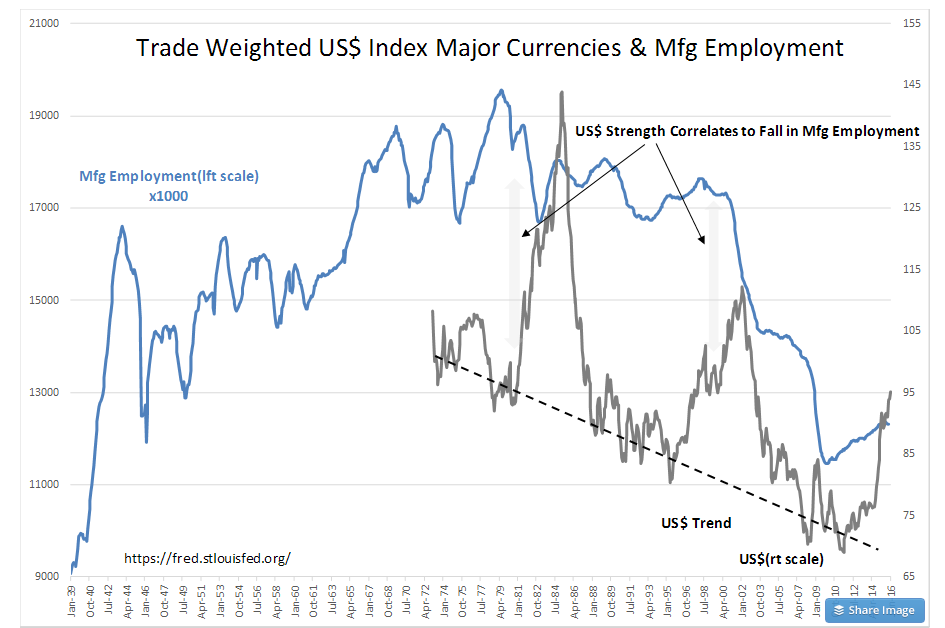

But, that is long-term! Short-term there have been periods of US$ strength which have disrupted global trade patterns. During periods when the Trade Weighted US$ Index Major Currency rises above trend, the high value exports are disrupted. History shows that during these periods, some of our manufacturing jobs in effect are transferred overseas. Trade Weighted US$ Index Major Currencies & Mfg Employment shows these periods. Mfg Employment stabilizes once the US$ returns towards its long-term trend. The prolonged period of US$ strength 1995-2005 coupled with a recession in 2008 was a prolonged period of Mfg Employment reduction saw a reversal in 2009.

The reason for periods of US$ strength rest with global investors seeking higher/safer returns than they see elsewhere. The early 1980s rise to 56% above trend came after Chairman Volcker successfully ended the 1970s high inflation era. Global investors favored the US markets for better returns net inflation. Roughly 15years later, the Internet Bubble attracted a similar surge of global capital. More recently the rise of terrorism and global autocracies, i.e. Russia, Iran, China, Turkey and etc., caused capital to flee to Western countries especially to the US. The US$ has been the strongest global currency 2013-2016 after Russia’s invasion of Crimea/Ukraine and was a significant unexpected event. Globally, the US$ remains the ‘elephant in the room’.

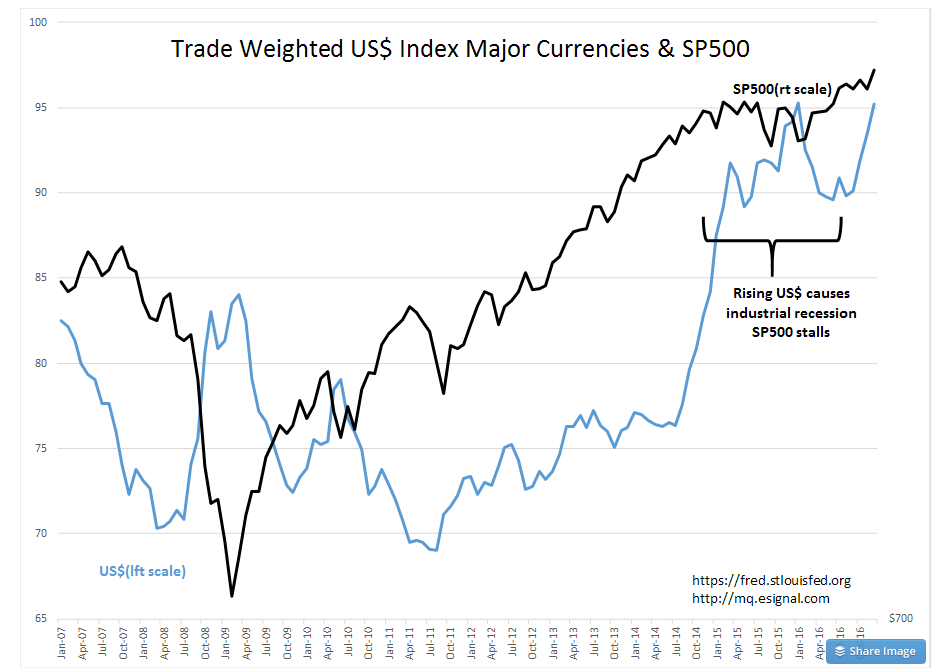

That recent US$ strength is coupled to industrial manufacturing weakness can be seen in detail in two charts from Jan 2007-Dec 2016, the Trade Weighted US$ Index Major Currencies & SP500 and the Chemical Activity Barometer & SP500. The Chemical Activity Barometer(CAB) stalls mid-2014 with industrial manufacturing in response to weak exports of high-value goods and falling commodity prices. Many investors have been unaware that the SP500 stalled with the invasion of Crimea and only began to shift higher after the Presidential Election. The main reason for not being aware of the non-performance of the SP500 for this period sits with the media which has focused on the performance of F.A.N.G(Facebook, Amazon, Netflix and Google) while manufacturing companies fell into recession. Normalization of the US$ to trend should be very positive for industrial US.

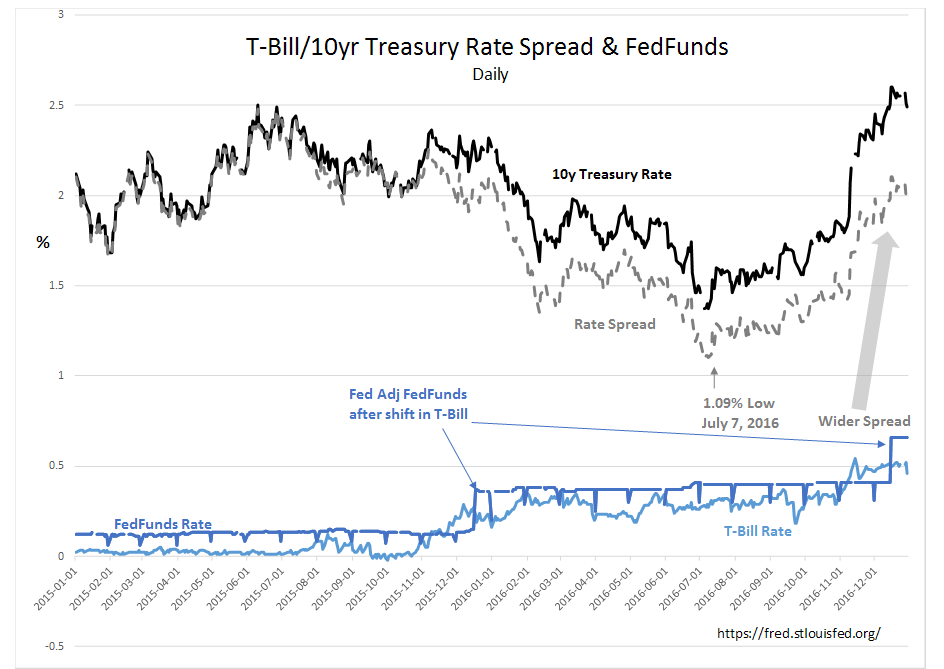

The second important trend for 2017 is shown in the T-Bill/10yr Treasury Rate Spread & FedFunds chart. The discussion of rates in the media and in analyst reports is one of the most difficult topics for investors to comprehend. Many believe that not only does the Fed control rates, but that higher rates slow economic activity. These are long held beliefs by Wall Street even though they have never been supported by the data. Why does this occur? The short answer is “Group Think”.

Recent data tells the long-term story which anyone can go to the link: https://fred.stlouisfed.org/ and satisfy the need for proof. The Fed only controls the Fed Funds rate. (This is the rate at which banks in trouble borrow from the Fed Reserve Window. No bank wants to do this.) On this everyone can agree. However, the history, as shown in T-Bill/10yr Treasury Rate Spread & FedFunds, shows us that it is the T-Bill which shifts first, then the Fed follows with a shift in Fed Funds rate. The only time the Fed has acted first was under Chairman Volcker who raised rates sharply in the early 1980s to control inflation. Even then, all he did was to raise rates to Wicksell’s “Natural Rate” level as the prior Fed Govenor had forced rates well below free market rates. I encourage anyone who is interested to download the data and examine it in chart form as presented here.

Higher rates by themselves do not impede economic activity, even though many believe this to be so. It is the spread in rates between the cost of funds for lending institutions and the rate at which they can lend funds where their profitability is determined. The wider the rate spread, the greater the propensity to lend and the faster the economy grows. When investors sell the 10yr Treasury and force the spread wider, it is because they perceive returns will be higher elsewhere. It is only when the T-Bill/10yr Treasury Rate Spread narrows to 0.0% that overall economic activity loses its momentum and we fall into recession. Today’s condition is a widening spread. 2017 should see decent economic expansion by this measure alone.

The wider the rate spread, the greater the propensity to lend and the faster the economy grows.

Summary: Two Important Trends for 2017 and Beyond. Our Industrial Recession has ended-Onward and Upwards

As discussed, economic activity has many inputs. Even with historically severe levels of bank regulation (even regulations which changed without being announced) and fines, the economy has recovered. This cycle bank regulatory environment resulted in the Single-Family Housing sector, normally a major contributor, operating at half-pace. Just the same, we have achieved record Employment, record Real Personal Income, record vehicle sales (not even adjusting for price increases) and record Real Retail and Food Service Sales. We have continued to experience this pace of economic expansion even with our industrial sector being in recession for 2 ½ years due to the strong US$. The recent series of record levels in the CAB shows that we have exited the industrial recession with the US$ remaining elevated. Free markets have always adjusted to headwinds and moved forward.

In my estimation, US$ and rate spreads are the two important trends for 2017. Rate spreads are widening and should continue to widen further. The spread of 2% today could very easily widen to 3.25% in the next couple of years as the new administration reduces some of the regulation currently perceived as slowing economic growth. Even if the US$ remains at elevated levels, history shows that a widening rate spread trumps all else. But, I expect the US$ to weaken, a sign that capital was shifting back to developing and emerging markets. Should that occur, we should experience acceleration in our industrial economy. It is my guess that this is the most likely outcome.

A widening T-Bill/10yr Treasury Rate Spread and a weaker Trade Weighted US$ Index Major Currency should be quite positive for equity prices.

Keeping in mind that future events may color the level of the US$ and could impact rate spreads in a direction not anticipated, 2017 looks likely to be a positive year. If we see the US$ weaken towards its long-term trend, it is a process which is likely to take more than 5yrs. Every year this normalization occurs will boost the US economy further and continue to support rising equity markets. I will revisit the US$ and the T-Bill/10yr Treasury Rate Spread multiple times in 2017.

Best for the New Year.

Why The Trade Weighted USD Index Major Currency and 10yr Spread are the most important guidelines today

By valueplays

Updated on