Klarman: “Value Investing Is Simple To understand But difficult to implement” And The Reach For Yield

“Value investing is simple to understand but difficult to implement.”

Also see

Seth Klarman On Value Investing In A Turbulent Market

Klarman "Catching Knives" Experiences Rare Yearly Loss, Looks ...

Seth Klarman: Now's Not The Time To Give Up On Value

Today, let’s take a look at the most recent market valuations. Hint and not a surprise: both stocks and bonds remain expensively priced. Value? Not today. Especially in the bond market.

[drizzle]What’s important for you, me and our clients to understand is that current valuations can tell us a great deal about what coming 10-year returns are likely to be. When should we play more defense than offense or more offense than defense? We’ll look at the numbers today.

Former head of the endowment at the University of North Carolina, Mark Yusko, wrote an outstanding client letter called The Value of Value. It is a great piece about value and a reminder about the investment discipline required to be successful. Mark shares some great quotes from value investor Seth Klarman. Here are just a few:

- There’s no such thing as a value company. Price is all that matters. At some price, an asset is a buy, at another it’s a hold and at another it’s a sell.

- There are only a few things investors can do to counteract risk: diversify adequately, hedge when appropriate and invest with a margin of safety.

- It is precisely because we do not, and cannot, know all the risks of an investment that we strive to invest at a discount. The bargain element helps to provide a cushion for when things go wrong.

- A margin of safety is achieved when securities are purchased at prices sufficiently below underlying value to allow for human error, bad luck or extreme volatility in a complex, unpredictable and rapidly changing world. (SB here – you will find most recent equity market valuations below in this week’s OMR.)

- While some might mistakenly consider value investing a mechanical tool for identifying bargains, it is actually a comprehensive investment philosophy that emphasizes the need to perform in-depth fundamental analysis, pursue long-term investment results, limit risk, and resist crowd psychology. (Emphasis mine.)

- Roy Neuberger said it first that there were three rules to managing money and Klarman reminds us that Warren Buffet paraphrased Roy saying,

- “The first rule of investing is ‘Don’t lose money,’ and the second rule is, ‘Never forget the first rule.’”

- An important clarification, however, is that “this does not mean that investors should never incur the risk of any loss at all.”

- Rather ‘Don’t lose money’ means that over several years, an investment portfolio should not be exposed to appreciable loss of principal. (Emphasis mine.)

What you’ll find this week, both for the equity and the fixed income markets, is that valuations remain significantly overvalued. In my view, the bond market resembles the tech bubble of 1999. There is little “value” today. 60/40 is in trouble – big trouble and unlike any period in time in my 32 years in the business. Just saying.

However, you’ll also see, in the Trade Signals section below, that the weight of trend evidence continues to point bullish for both stocks and bonds. To that end, I believe trend following can help us minimize loss and preserve principal. The preserving principal part will play the most important role in our ability to buy the bargains when the getting gets good again.

I favor trend following processes, especially given where valuations sit today. OK, grab a coffee and jump in. You’ll find a number of charts below (click on the orange link below) and today’s OMR should be a quick read.

Included in this week’s On My Radar:

- October 1, 2016 Equity Market Valuations & Probable Forward Returns

- Bond Market Valuations (High Grade and High Yield)

- Trade Signals – The Weight of Trend Evidence is Bullish for Equities and Bonds; Extreme Bearish Sentiment is S/T Bullish for Stocks (10-5-2016)

October 1, 2016 Equity Market Valuations & Probable Forward Returns

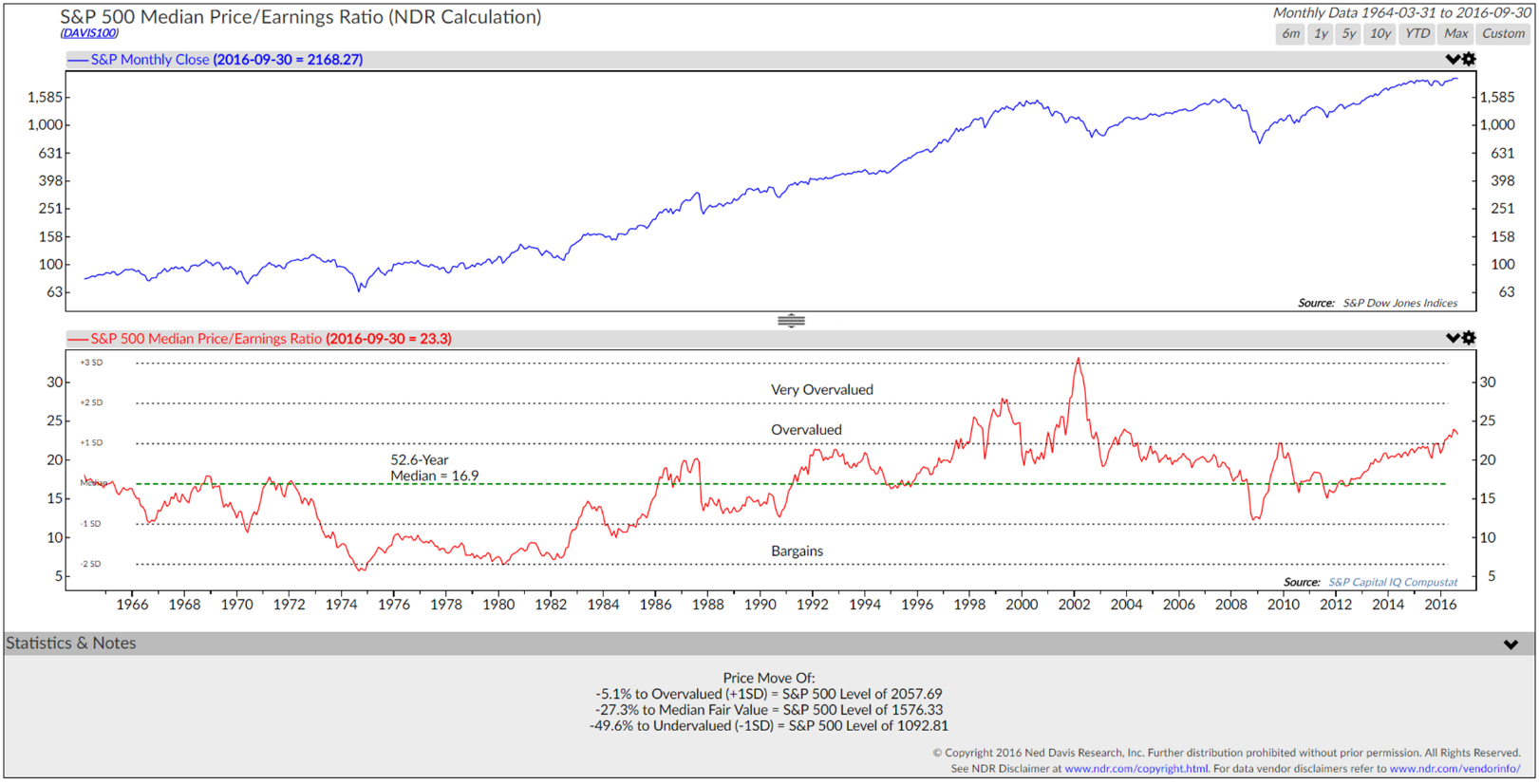

S&P 500 Median Price-to-Earnings Ratio = 23.3 (current level = 2,168.27 on 9-30-2016)

- 1,576.33 = Current Fair Value (this number is based on a 52.6-year median P/E of 16.9)

- 2,057.69 = Overvalued (the S&P 500 was at 2,168.27 on 9-30-2016, so it is at a level of more than 5% above what is considered overvalued)

- 1,092.81 = Undervalued is at 1,092.81 (a crisis event might get us there)

Source: Ned Davis Research (NDR)

Source: NDR

Shiller P/E = 26.8 as of 9-30-2016. The above chart uses 6-30-2016 quarter-end Shiller P/E of 25.9.

Source: dshort.com

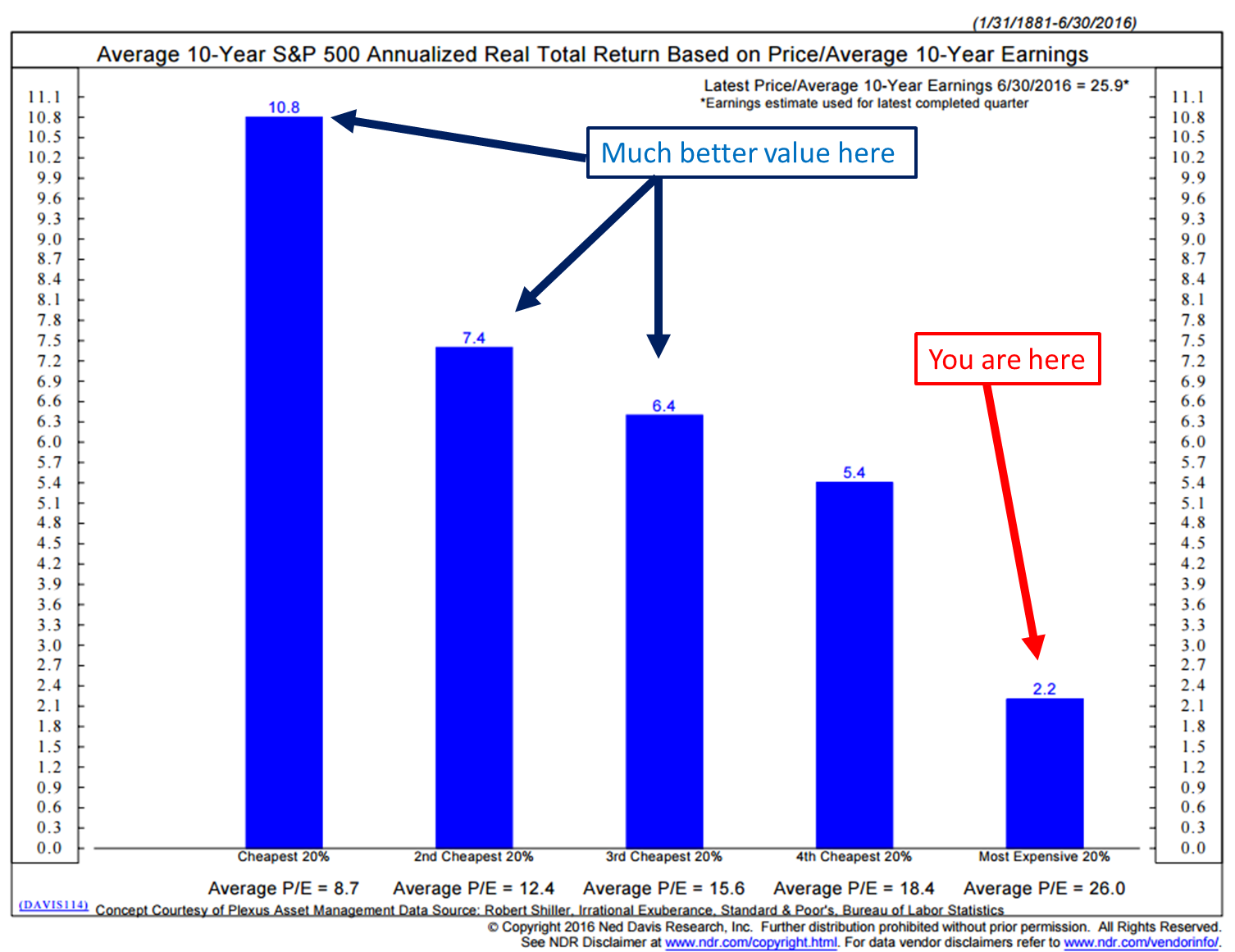

What does this tell us about returns over the coming 10 years?

The next chart shows the “Average 10-year S&P 500 Annualized Real Total Return Based on Price/Average 10-Year Earnings”

- Probable returns of just 2.2% per year over coming 10 years

Source: NDR

Crestmont Research – Ed Easterling

The 2011 article “P/E: Future On The Horizon” by Advisor Perspectives contributor Ed Easterling provided an overview of Ed’s method for determining where the market is headed. His analysis was quite compelling. Accordingly, we include the Crestmont Research data to our monthly market valuation updates.

The first chart is the Crestmont equivalent of the Cyclical P/E10 ratio chart we’ve been sharing on a monthly basis for the past few years.

Source: dshort.com; Crestmont Research (crestmontresearch.com)

The Crestmont P/E of 27.1 is 93% above its average (arithmetic mean) and at the 98th percentile of this 14-plus-decade series.

Source: dshort.com; Crestmont Research (crestmontresearch.com)

From Doug Short:

- The inflation “sweet spot,” the range that has supported the highest valuations, is approximately between 1.4% and 3%. See, for example, the highlighted extreme valuations associated with the Tech Bubble arbitrarily as a P/E10 of 30 and higher.

- The chronology of the orange “bubble” on the chart is a clockwise loop of 56 months starting at the 6 o’clock position.

- The P/E10 was 31.3 and the annual inflation rate for that month (June 1997) was 2.30%.

- The average inflation rate for the loop was 2.41%. The P/E10 peak of 44.2 in December 1999 was accompanied by a 2.68% annual inflation rate. Two months later the inflation rate topped 3% at 3.22%. The right side of the loop shows what happened thereafter.

- The ratio slipped below 30 for two months (the tail at the bottom of the loop) before its final three-month swan song in the 30+ range.

- The latest P/E10 valuation is 26.8 at a 1.31% year-over-year inflation rate, which is below the sweet spot mentioned above.

- And speaking of that 30 threshold for the P/E10, prior to the Tech Bubble, only two months in history had a ratio above 30: They were 31.5 and 32.6 in August and September of 1929, respectively, just before the Crash of 1929.

- Research estimates put the annual inflation rate during those two months at 1.17% and 0.00%. (Source)

Here is a reminder of secular bull and bear market cycles:

Source: dshort.com

In the useless fact category, I found it interesting that the bull market gain of 666% (the greatest bull market of all time) was followed by a low in the S&P 500 Index in March 2009 at 666. Aren’t those two interesting numbers?

How long have these cycles lasted?

Since that first trough in 1877 to the March 2009 low:

- Secular bull gains totaled 2075% for an average of 415%.

- Secular bear losses totaled -329% for an average of -65%.

- Secular bull years total 80 versus 52 for the bears, a 60:40 ratio.

This last bullet probably comes as a surprise to many people. The finance industry and media have conditioned us to view every dip as a buying opportunity. If we realize that bear markets have accounted for about 40% of the highlighted time frame, we can better understand the two massive selloffs of the 21st century.

Based on the real (inflation-adjusted) S&P Composite monthly averages of daily closes, the S&P is 151% above the 2009 low. (Source: Doug Short, Advisor Perspectives)

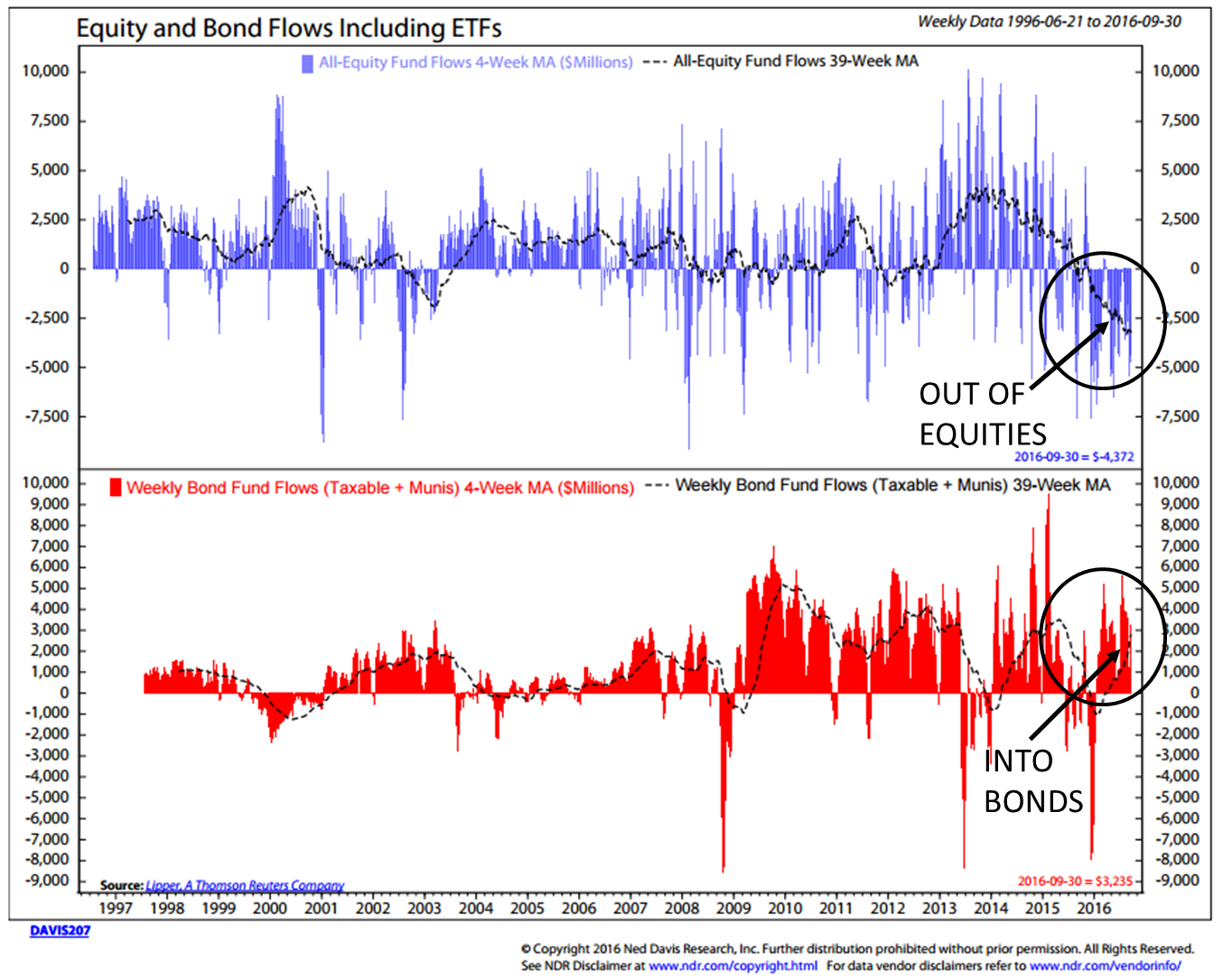

I was curious on where the majority of investor money is flowing and came across this next NDR chart. Every day we hear from investors that they have no other alternative but to find some yield. “I need income,” the retiree says. I imagine you are receiving a number of client calls in this regard.

So what is happening? The money is herding into bond funds and high dividend paying stocks. That is not where the value is today… it is where the bubble is today. Next is the data:

Source: NDR

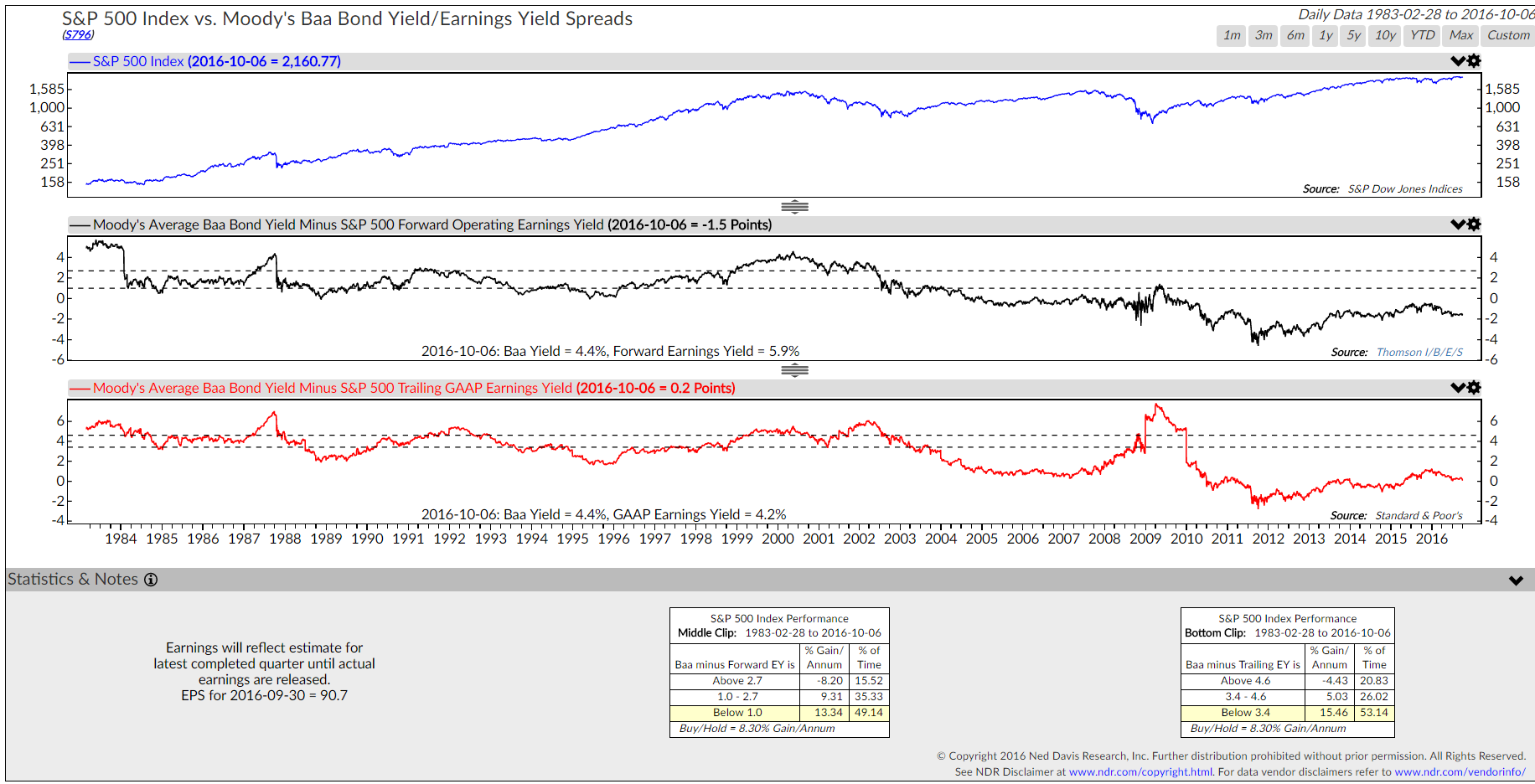

I’m often asked about the value of equities over fixed income and, yes, I agree on a relative basis it is there. You can see just what that looks like historically in regards to performance.

So let’s put this next chart in the plus column for now: Supporting the stock market is the higher earnings yields on equities in comparison to what bonds are paying investors as measured by the Moody’s Baa Bond Yield (yellow highlights in boxes below).

Source: NDR

This doesn’t take away from the fact that stocks are richly priced. I’m not buying into the argument that stocks are better than bonds so we should buy stocks. I see little upside over the next 7 to 10 years in equities at current valuations though I suspect equities grind higher but that doesn’t mean they are a good value.

Valuations are high and those earnings per share (with the added benefit of being goosed up with all of the stock buyback activity) haven’t been looking too good as you’ll see next.

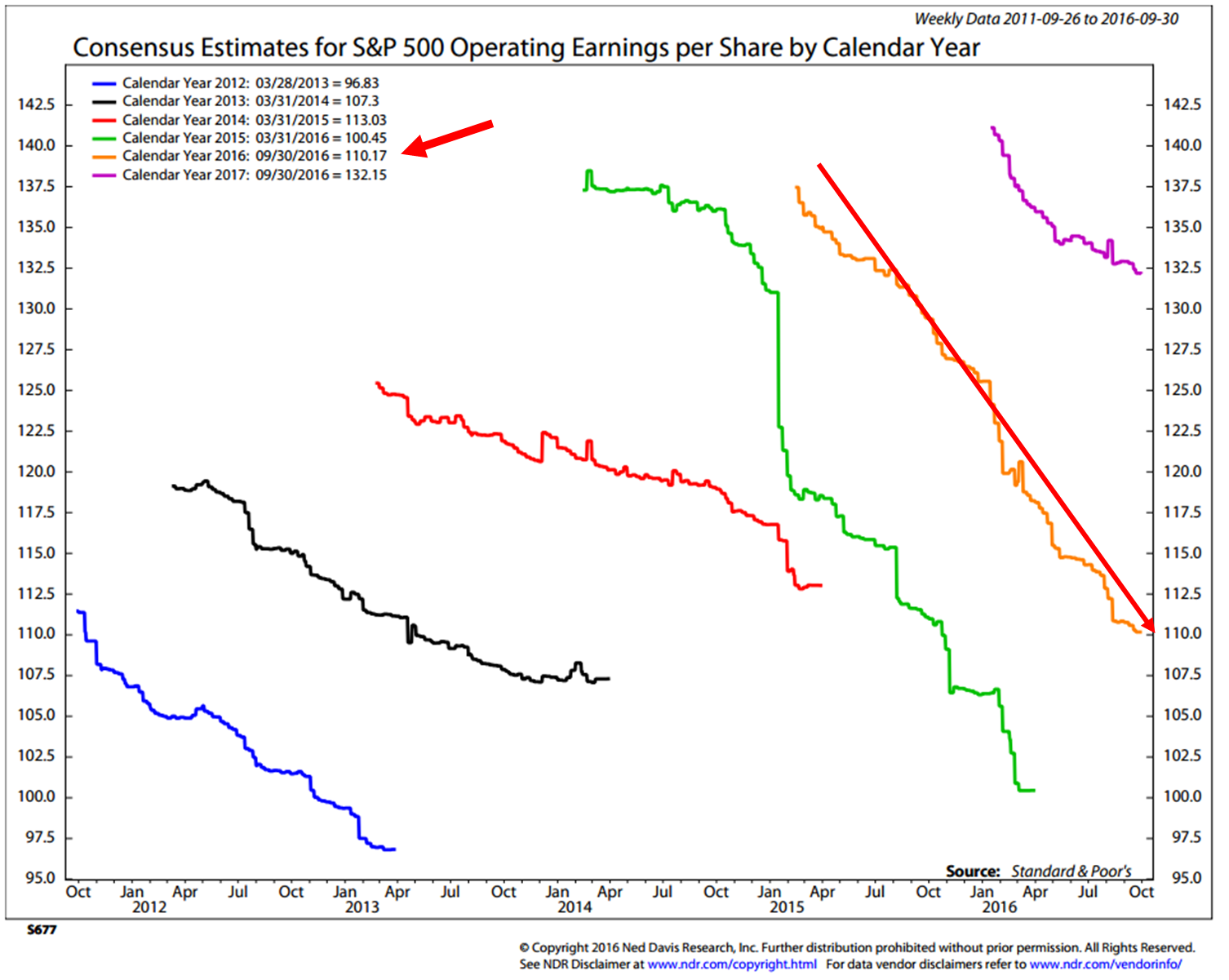

Reported Earnings – Not So Good

Wall Street Continues to Downgrade Earnings Expectations:

- As of September 30, 2016, actual reported TTM earnings were $90.74 per share. (Red circle above.)

- As of September 30, 2016, Wall Street “consensus earnings estimates” are forecasting $110.17 per share for the full year 2016. (Short red arrow below.)

- Importantly, look at just how bad they are at forecasting (the long red arrow shows what their 2016 estimates were last year and revised lower each quarter since).

- You can see that they are consistently bad in years past and also forward in 2017. Start high, revise down. Wash, rinse, repeat.

Source: NDR

How can you trust this? I can’t. That’s why I favor actual trailing 12-month (TTM) reported numbers. I then compare the current level to the historical median earnings. From there, we can gauge probable forward returns. Not perfect but pretty good as seen in the 2.2% real return “you are here” chart shown several charts above.

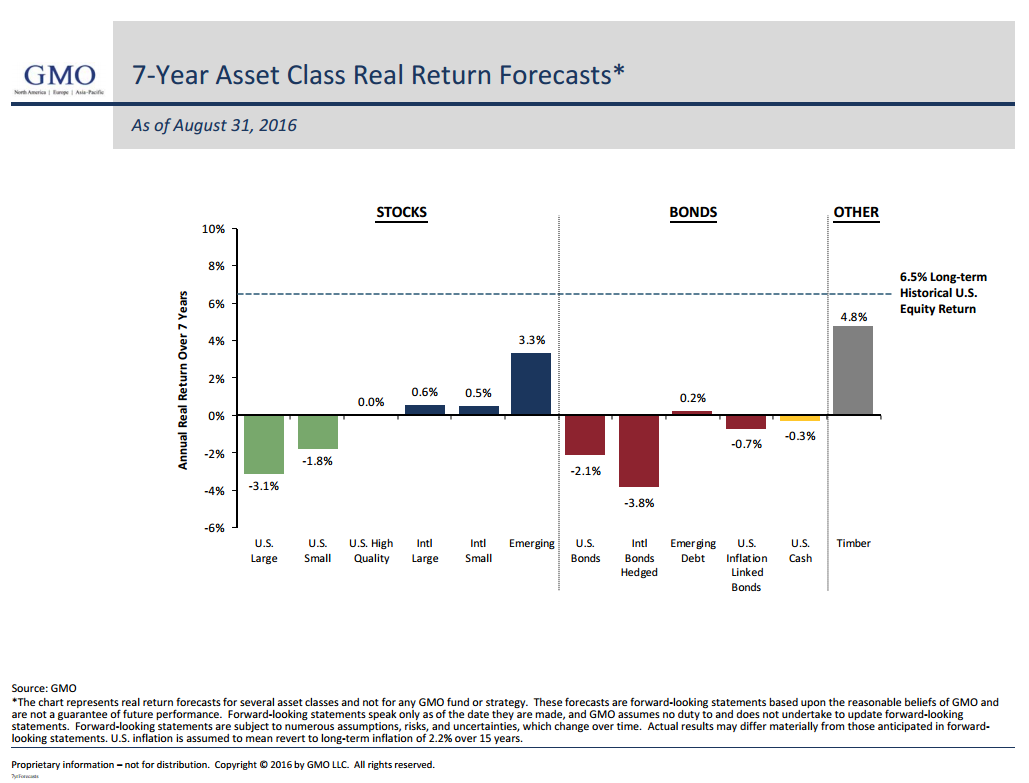

We looked at probable 10-year returns in that chart, let’s look at the coming seven-year forecast next from one of the all-time great investors, Jeremy Grantham.

Jeremy Grantham, GMO. Here is GMO’s most recent seven-year forward return expectations for equities, bonds and other:

- Note the -3.1% annualized real return forecast for U.S. Large Cap Equities

- Note the -2.1% annualized real return forecast for U.S. Bonds

Bond Market Valuations (High Grade and High Yield)

Yields are at 5,000-year lows.

71% of the world’s government bonds are yielding less than 1%. 33% yield less than 0%. In a picture it looks like this:

Since 2008, the Fed has dropped rates from 5.5% to 0%. Unprecedented.

This is what it looks like over time.

In the wake of the Financial Crisis, inflation has been low and the 10-year Treasury yield is about 23 basis points above its historic closing low of 1.37% in early July of 2016.

Risk is being overlooked in HY bonds. Yields on high yield debt is close to the same yield on less risky loans. The chase for yield has driven investors to riskier asset classes.

Zombie companies are being financed and kept alive. The next recession will flush out the bad.

I am anticipating a once-in-a-generation buying opportunity in HY bonds. While the trend this week is up, continue to invest with the trend. Move to the safety of cash or Treasury Bills when the trend crosses down.

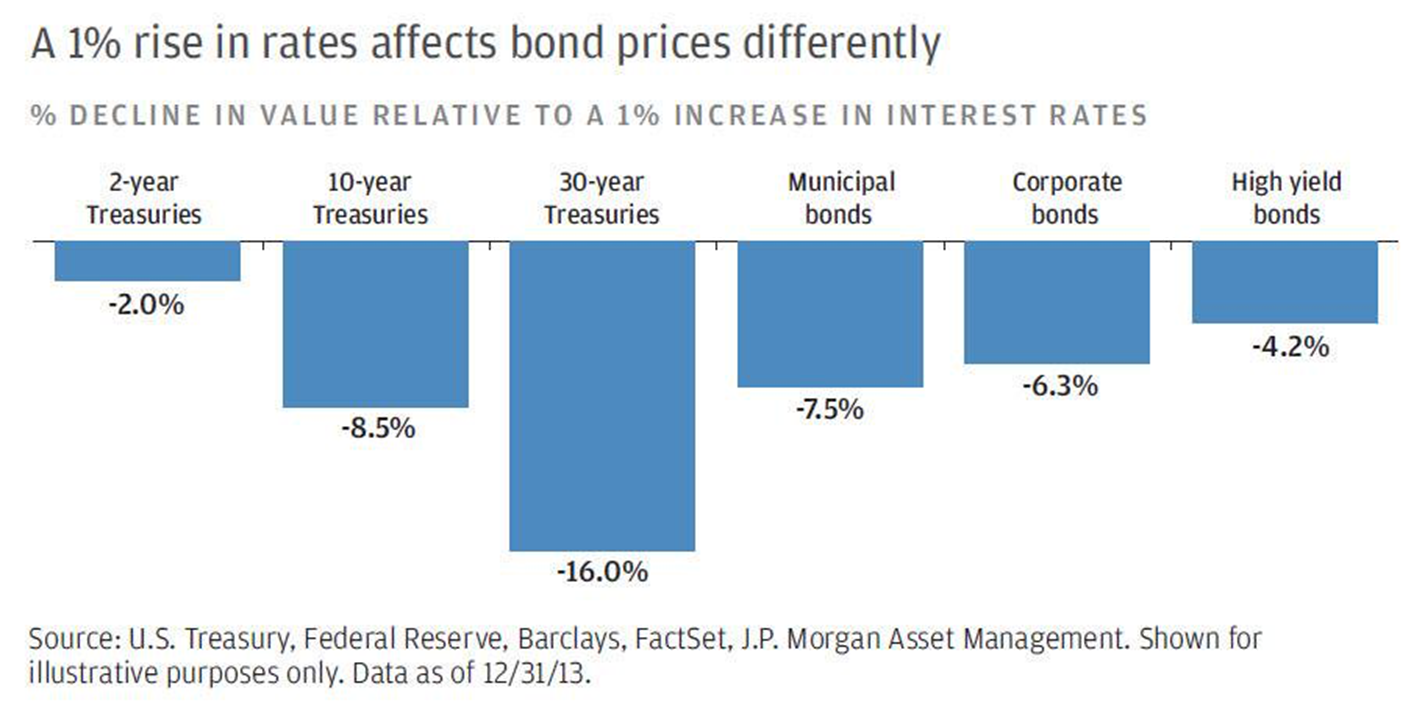

Show this next chart to your clients. It is what happens to the principal value when rates rise 1%. It is more than double the indicated loss when rates rise 2%. How about 3%?

When your starting place is where we are today, you can begin to see the bubble that is expanding in the bond market. And, unfortunately for many, that is where the majority of money is herding into.

Alright, that’s enough on valuations for now. The hamburgers are way too expensive and we are not getting as much as we’d like for our money. Grab a drink, be patient, preserve principal and know that a better value opportunity will present.

Trend following can help. Take a look at the most recent trend charts in Trade Signals.

Trade Signals – The Weight of Trend Evidence is Bullish for Equities and Bonds; Extreme Bearish Sentiment is S/T Bullish for Stocks (10-5-2016)

S&P 500 Index — 2,159 (10-5-16)

Posted each Wednesday, Trade Signals looks at several of my favorite stock, investor sentiment and bond market indicators. It is my weekly risk management dashboard, designed to keep me better in sync with the major technical trends. I hope you find the information helpful in your work.

Click here for the most recent Trade Signals blog.

Concluding Thought

“Avoiding where others go wrong is an important step in achieving investment success. In fact, it almost assures it.”

– Seth Klarman, The Baupost Group

With this Klarman quote in mind, it is pretty clear to me where others are going. Bond funds and other high dividend payers.

Investors are desperate for yield. 71% of the world’s government bonds are yielding less than 1%. 33% yield less than 0%. There is no value there.

Finally, and in conclusion – from Seth, “The hard parts of Value investing are Discipline, Patience, and Judgment. Investors need Discipline to avoid the many unattractive pitches that are thrown, Patience to wait for the right pitch, and Judgment to know when it is time to swing.”

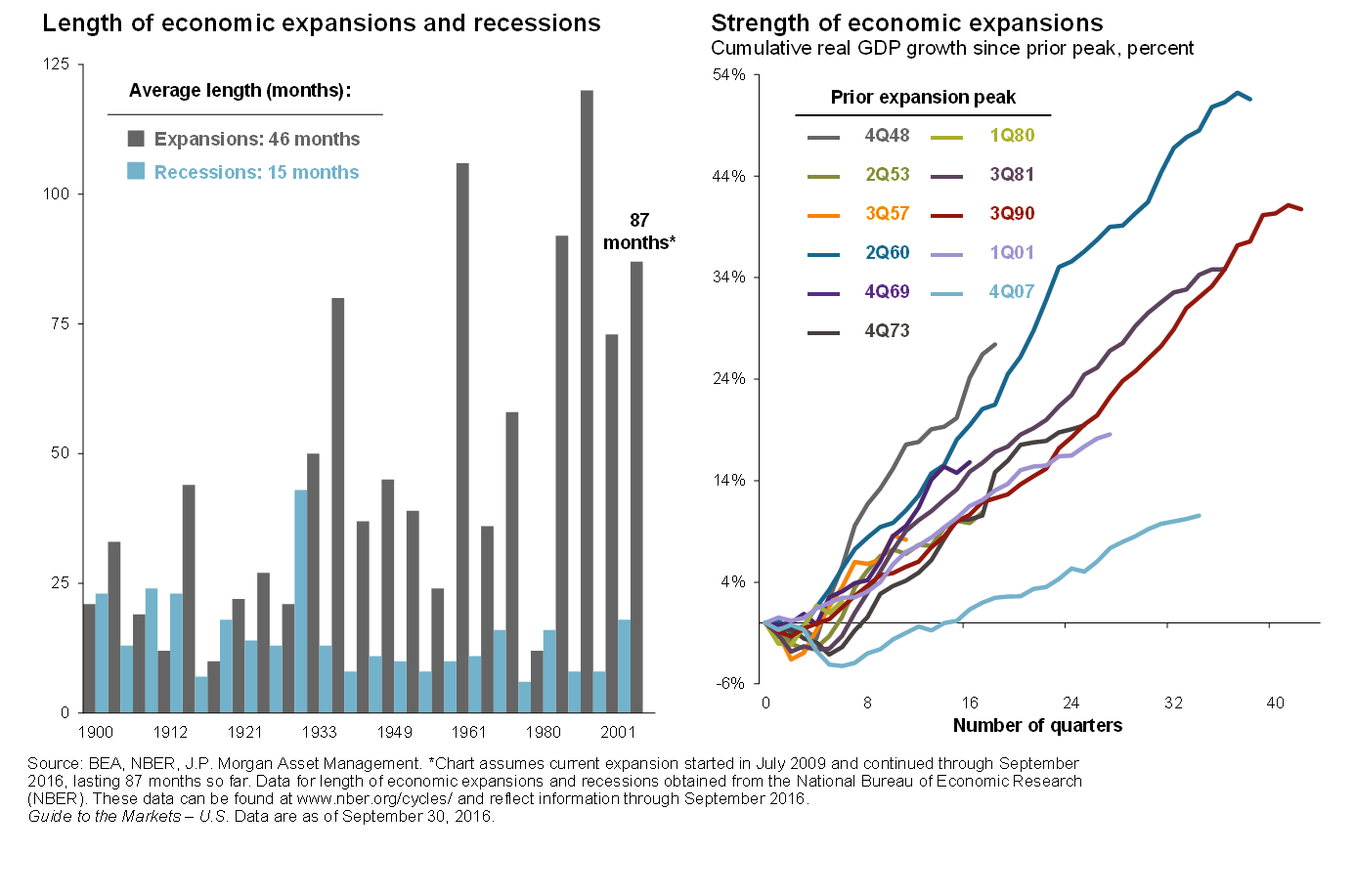

The really fat pitches come during times of recession. The average economic expansion lasts 46 months. We are 87 months into the current expansion.

Since 1900, only three were higher. The average recession lasts 15 months. Be mindful that they happen and they can provide great investment opportunity.

It is not the right time to swing. Let’s wait for the right pitch.

Until then, diversify amongst trading strategies that have the ability to get defensive. Utilize cash when the trend turns down. Allocate to disciplined and experienced managers. Tactically trade your fixed income in a way that enables a high margin of safety. Be mindful of risk.

Lowest risk presents at times that risk feels highest. Highest risk comes at times that risk feels lowest. Valuations really do matter. Seek value and be prepared to act when it presents. You and I will both be scared… It won’t be easy.

Here is the link to Mark Yusko’s Q2 2016 Client Market Letter. It’s a fantastic read. Print it out and come back to it from time to time.

Personal Note

Our thoughts and prayers go out to those that lost loved ones in the wake of the horrific hurricane. When we turned on the late night news and learned of the significant loss of life in Haiti, Susan and I watched the news last night and were shaken. Florida is in range now. Let’s hope the eye of the storm avoids the coast.

Did you watch the Ryder Cup last weekend? I spent most of Sunday glued to the TV with my boys by my side. It was like golf played in a football-like, fan-crazed atmosphere and what a finish. What fun and a great result for the U.S. side.

I think some exercise is needed after all of that couch time. The weekend is ahead and gym time is on my list – and the gutters, leaves and pond work. It is a good thing we have so many boys. They are not going to like this weekend’s chore list. Fall is here and the leaves are turning here in the Northeast. Beautiful. Hey, and my Philadelphia Eagles are showing some promise. Let’s go! Good luck to your favorite team as well.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts via Twitter that I feel may be worth your time. You can follow me @SBlumenthalCMG.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Wishing you and your family the very best!

Steve

Stephen B. Blumenthal

Chairman & CEO