Human beings do something really well. They buy what they wish they would have bought and they are spectacular at it.

The last time we had a record amount of money move to passive was in March 2000. Back then only 10% of the market was passive and today it is close to 40%.

These strategies (passive) must buy regardless of valuations. This causes valuations to get to extremes. When things go over the cliff, they go down that much faster. I think that’s the big risk today.

Current valuations are at the second highest level in history.

Mark Yusko, Morningstar Chicago ETF Conference

[drizzle]Last week, I promised I’d share some of my Morningstar conference notes. So let’s start there today. I hope that you find my notes helpful. I believe we investors should always be putting together a shopping list of best ideas so that we are in a position to act when the getting is good. To that end, I believe you will find some ideas below to start thinking about (if you haven’t already).

Personally, I walked away from the Best Ideas panel with a few ideas that I may include in my own portfolios. The China and India theme keeps bumping me on the head. I hope you enjoy this week’s post.

Included in this week’s On My Radar:

- Morningstar Best Ideas: Richard Bernstein, Mark Yusko and John West

- Charts That Matter

- Trade Signals – Sentiment Better, Risk On Remains

Morningstar Best Ideas: Richard Bernstein (Richard Bernstein Advisors), Mark Yusko (former UNC Endowment CIO and Founder, Morgan Creek Capital Management) and John West (Research Affiliates)

There is a lot of information to present so I’m going to present it in two parts over this week and next. And there were a number of very good ideas. The dialog was great. Following are my shared notes.

Best Ideas Panel – Part 1

Mark Yusko:

- Human beings do something really well. They buy what they wish they would have bought and they are spectacular at it.

- The last time we had a record amount of money move to passive was in March 2000.

- Back then only 10% of the market was passive and today it is close to 40%. These strategies must buy regardless of valuations. This causes valuations to get to extremes.

- When things go over the cliff, they go down that much faster. I think that’s the big risk today.

- Current valuations are at the second highest level in history.

Richard Bernstein:

- It is not March 2000 for the equity market, it is March of 2000 for the fixed income market.

- We are very close to something happening in the fixed income market. Why do I say that? Inflation expectations, while not rising dramatically, troughed last February.

- We are in a period where people are rushing into fixed income. And for the first time in a number of years, money growth is rising.

- We know that the consensus is always wrong. Look, the individual investor has never gotten it right.

- Pension funds are overweight bonds for the first time in God knows how long. Why do we now believe they’ve got it rig when inflation has troughed and money growth is beginning to expand?

- People are so worried about the equity market but what they are really missing is the March of 2000 in the bond market.

- The fact that inflation seems to have troughed and nobody seems to be aware of it is a worrisome factor.

John West:

- I like to think of the world in two ways: do we have equity markets bullish or bearish and do we have inflation expectations rising or falling.

- Most of the time in the last 30 years we’ve had falling inflation expectations and an equity bull market. However, that isn’t the only investment environment we are going to see in our investment lifetime.

- We can see bear markets that come with bits of inflation or we could have reflationary bear markets. Stocks and bonds are wonderful diversifiers against each other until you get periods of rising substantial inflation.

- Where are we today? Inflation expectations have fallen from 2 ½% to 1.2%. Now they are picking up again but they are still 40% lower than they were three years ago.

- Certain types of assets respond well to changes in inflation expectations. What we call strategic third pillar assets.

- A 25 or 50 bps change in inflation expectations could move these assets up 15% or 20%. Outside of TIPS, most inflation assets are particularly cheap.

- Especially some of the backdoor hedging asset credit categories like bank loan, high yield, certainly EM. They are priced to deliver a real return of 4% over the next ten years vs. a 60/40 priced to give you about 1% over the coming ten years.

Bernstein:

- The line several years ago was we are going to inflate away the debt. If you believe that, you want to buy all the companies that have all the debt. (Bernstein is not sure he believes this but if you do…)

- I do believe inflation is going to come back but maybe it goes from 1% to 2% or maybe 3%.

Yusko:

- Outlook for US stocks: Demographics is destiny!

- When you have a lot of people under age 25, you have high inflation and low productivity.

- When you have a lot of people between 45 and 65, you have high productivity and you have rising stock prices.

- When you have a lot of people between 65 and 85, you have declining productivity and low stock prices.

- Harry Dent wrote a book on this in 1993. He said in 2008 to 2023 we will have a 15 year period where bonds will outperform stocks.

- Since 2008 bonds have outperformed stocks.

- Since 2000 the return on U.S. equities is 3.50% compounded per year for 16 years. There is a technical term for that… that sucks.

- Bonds have been almost double that. EM has been almost double that.

- In 2000, as Warren Buffett wrote, valuations were stupid. They were… they were crazy.

- We have gone through this period now where everybody is saying, “Wow, the last five years have been great.” Because the previous 12 months were really crappy. 2008 was really bad.

Yusko: So, what do we do from here?

- Look, there are four risks we can take as investors:

- We can take the risk free rate. That is now 0%. We can take credit risk. We can buy a bond. You get 2% above risk free long term. You know the return over the next ten years. It is 2%. We know this. It is 100% correlated to the yield. (Note: If inflation is at 2%, the real return after inflation is 0%).

Yusko told a story about an advisor he met recently. He asked him why he was throwing so much money into bonds. The advisor said because he needs to make 7 ½% for his client. But you are going to make 2% Yusko told him. But my client needs to make 7 ½%! But you’re going to make 2%.

The advisor said, “No, no, no, over the last ten years I’ve made 7 ½%.” Yusko answered, “But ten years ago the yield was 7 ½% and 20 years ago it was 11% and 30 years ago it was 17%. Today the yield is less than 2%, you are going to make less than 2%.”

- You can take equity risk. Normally, you get 5% above bonds. That’s 7% above the risk free rate. The long-term risk free rate is 4%, bonds earn 6% and stocks earn 11%. Long term. The problem is the market is so grossly overvalued. Read Crestmont Research’s piece titled, Waiting for Average, and read how long it will take to compound at 10% annualized returns on stocks. I won’t ruin it for you but it is forever. The problem is today the risk premium is very low. Jeremy Grantham from GMO would say it’s negative. Research Affiliates would say it’s negative. We are going to have no return for U.S. stocks for the next seven to ten years (for the index). It doesn’t mean there won’t be pockets. Doesn’t mean that won’t be places that will produce returns.

- The third risk you can take is illiquidity risks. Private equity, private real estate, private energy, private debt. The long-term return on private equity is 16%. We think it is still going to be 13% or 14% over the next decade.

- The last risk you can take is structure. That’s just a fancy term for leverage. If you can get it, take advantage of it.

More from Yusko:

- The “Value of Value” – my recent quarterly letter. 65 pages but the point is just about everyone thinks value is dead. Nobody wants it. That’s when you want to get it.

- For the coming decade, 60/40 is dead money.

West:

- Value investing in our mind will provide 2% to 3% excess returns over the next ten years. All of this is a way of saying that if you want to make meaningful returns over the next five to ten years, you need to look at the things that did terrible over the last five or ten years. Today, they are priced to give very solid returns.

- Now, are they going to happen in the next 12-18 months? That’s anyone’s guess but over a longtime period you have a high amount of certainty that a collection of diversifying strategies; emerging markets, non U.S. stocks, credit categories and so forth have a high probability of beating the very comfortable and recently outperforming mainstream (60/40) portfolio.

Yusko jumps in:

- Can I give you some data to support that? From 1990 to 2000, Baupost (a deep value investment fund run by Seth Klarman) compounded at about 12%. Not terrible. But the market, compounded at 17%.

- Everybody said value is dead… Julian Robertson went out of business and Gary Brinson went out of business… value is dead.

- Over the decade, the prediction from Jeremy Grantham at the time was that the market would do -1.90% compounded per year annually for ten years. My board member from UNC said you aren’t allowed to use the letters GMO in a sentence ever again because he is always wrong.

- So for the next ten years, the market delivered -1% per year compounded per year for a decade…

- …Baupost was up 17% per year compounded with a deep value strategy.

Bernstein:

- In 1995 I wrote a book called Style Investing. It was the first book of its kind that actually looked at why value investing outperforms at a certain point in time and why growth investing outperforms at a certain point in time.

- What is large cap and small cap? What are the macro reasons why these styles outperform through time… (the overall point of the book)

- Basically, what the conclusion of the book was is that if you are a value investor you should be an optimist. Because what you are betting on is that earnings growth is going to come back to life.

- Your best opportunities come at deep discount and years of underperformance.

SB (Blumenthal) here:

- Bernstein sees value for the value investor today.

- Bernstein believes that growth will come.

- He believes that the corporate profit recession may be bottoming and earnings will expand.

- He believes that everyone is in fixed income and not many are in the equity markets.

- He recommends value investing.

- He believes we will not find people that are significantly overweight equities.

- To that last bullet point I’m not so sure.

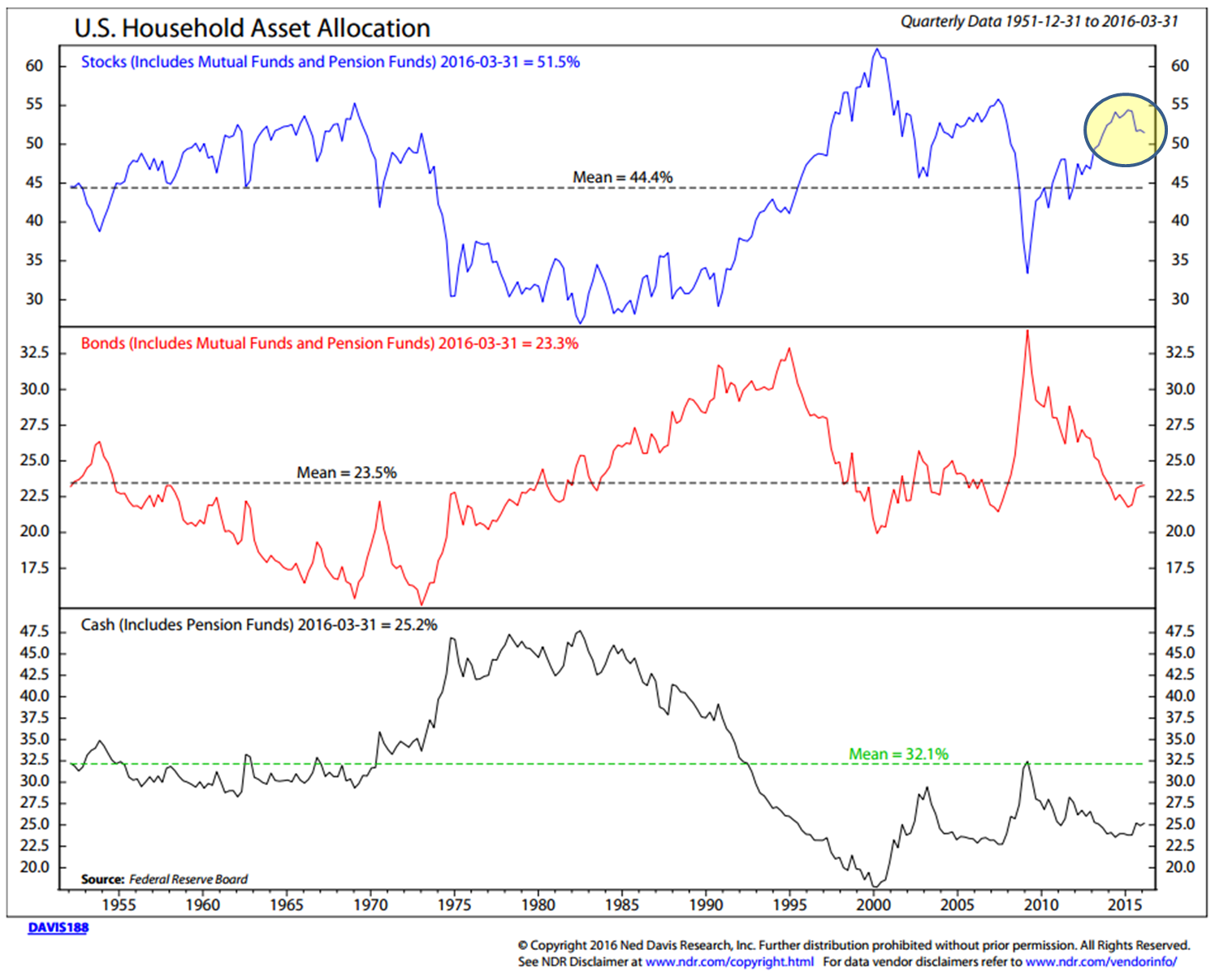

- Here is a picture that shows us where we are today (yellow circle):

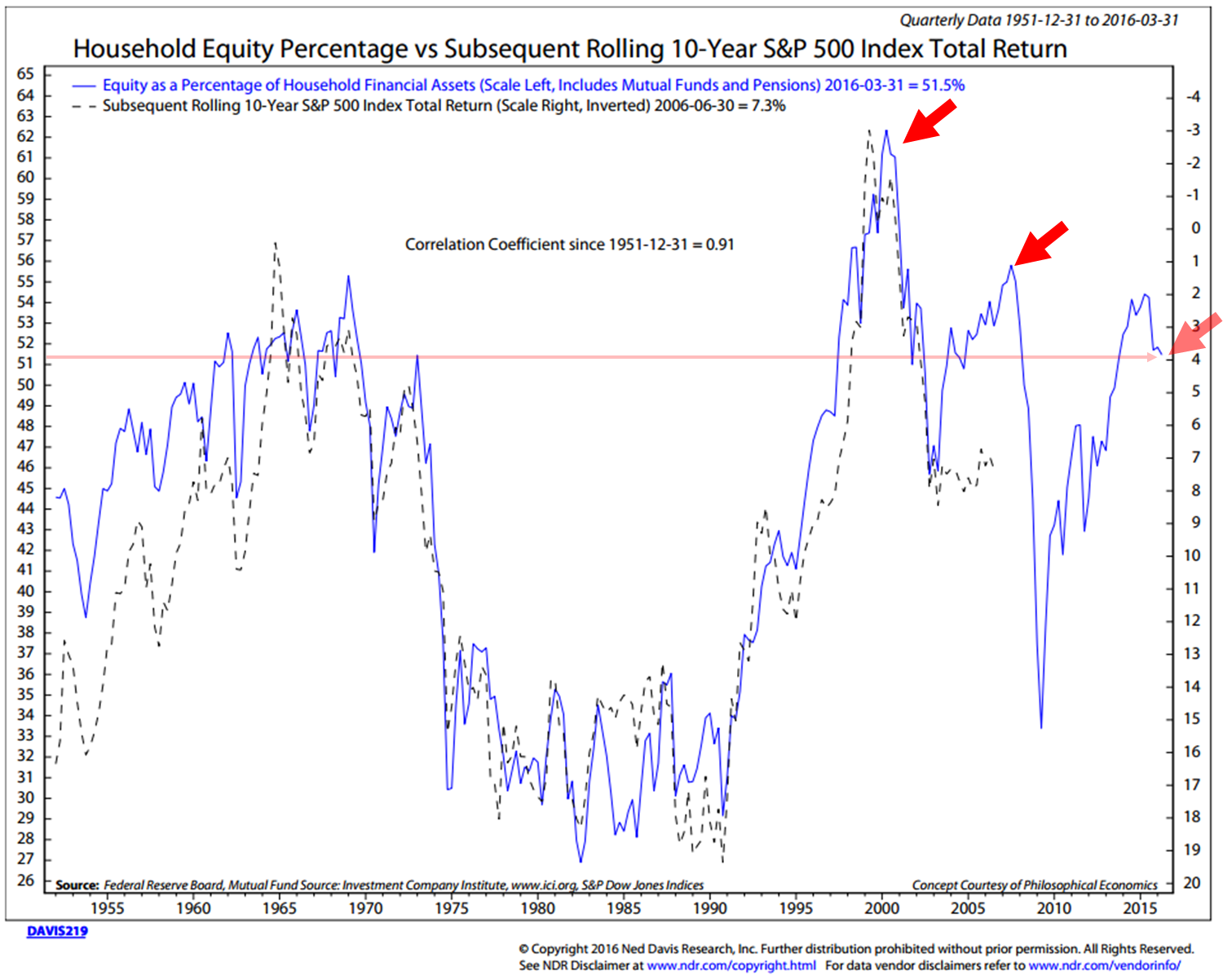

The next chart tells us what this means in regards to probable forward 10-year annualized returns (3% to 4% before inflation or 1% to 3% after inflation assuming a 2% rate of inflation):

SB again:

- What this data is telling us is that investors are overweight equities though not at the 2000 or 2007 bubble levels. Current levels compare with the 1966 bull market high.

- The chart data is from March 2016 quarter end. Some improvement from the recent high made last year but nothing in the forward return probabilities to get excited about.

- The cyclical trend is positive as you’ll see in Trade Signals and I agree that what is absent is a state of euphoria that typically marks bull market tops.

Bernstein:

- People may be shocked in that we have worked off the post deflationary shock that has occurred since the 2008 great financial crisis. He sees an economic growth recovery ahead.

- The worst of the profits recession and the worst of the global profits recession is behind us. We are at a point where profits are starting to recover.

SB interruption:

- I just don’t see the great growth story until we restructure the debt problem. We have reached the upper limits of how much we can borrow from tomorrow to spend today. Look at Japan, look at Europe. I think he is missing the size of the debt problem both in the U.S. and globally.

- To this point, let’s take a quick three minute detour on this subject. Bridgewater’s Dalio: There’s a ‘dangerous situation’ in the debt market now. We are at the end of a long-term debt cycle: Ray Dalio on CNBC

Yusko:

- If you look at the trends, what we are seeing is pretty negative trends in the developed world.

- It is the killer Ds: bad demographics, too much debt and you still have deflation rather than inflation.

- The new headwind that is really negative is this nationalism thing. Brexit and now the Italy referendum and the Austrian guy who is going to call for an Ausexit.

- And that’s a bad trend for profits.

- Europe looks really awful to us. Italy could go the wrong way with their referendum later this November or early December. One of my contacts has a particularly good track record for the last 17 years, so I listen. He is calling for a 40% market decline in Europe if that vote goes the wrong way.

- Japan has a problem. Their currency is strong but they need it to be weak. Kuroda is ripping his hair out and doesn’t know what to do. If they can’t get the Yen to weaken, profits in Japan are going to struggle.

- In the U.S. profits are going to be episodic.

- The place you are going to find profits is in emerging markets. EM are starting to boom again. Look at the recovery that is happening in Brazil. Nobody was long Brazil in January. And now Brazil is up 70% for the year and people are starting to say, OMG there is something to do in Brazil.

- There are interesting developments in profitability – Latin America in particular.

- Asia is booming in certain sectors. China is an area we absolutely love; particularly the five big sectors of consumption, which are staples, retail, health care, energy and technology and e-commerce.

- McKinsey did a study: The e-commerce segment in China for the next decade is going to grow at 26% compounded. The mobile component is going to grow at 52%.

- That market is going to be 66 times large. Alibaba could double from here, easy. And it’s up 60% in the last four months.

- People say it can’t double from here, it’s a fraud. Jim Chanos says it’s a fraud. It is not a fraud. It is the largest e-commerce company in the world, it is the largest cloud company in the world and it is the largest payments company in the world.

- It is a monster behemoth that people can’t comprehend. The middle class in China is bigger than the population of the U.S. and Europe combined.

- Every single day, 10,000 people in the U.S. and 10,000 people in Europe turn 65. It is not the same in emerging markets. 25% of all the people in the world below age 25 live in India.

- India is going to be in a bull market for the next decade.

SB ‘Part 1’ summary:

- The bubble of all bubbles is in the bond market.

- The value style factor is favorable and there are pockets of opportunity buuuut a better opportunity will present at much greater value.

- I would have preferred to buy a deep value fund after the 2000 and 2008 meltdowns. Active stock picking will come back in vogue.

- There is consensus on EM and some good ideas shared on China and India.

- Diversify to a number of flexible trading strategies, use trend following to trade fixed income exposure and hedge that equity exposure.

The above notes take us about halfway through the Best Ideas session. That’s a lot to digest for now. Let’s continue the second half next week. BTW – I promised you the audio recording and hope to have it soon.

Charts that Matter

Following are a few charts I came across this week that speak to some of Japan’s economic challenges as well as a picture on domestic debt (just to hit on the debt cycle point via picture).

By country (recall the Reinhart and Rogoff study – growth slows when debt to GDP reaches 90%). Excessive debt is our global problem…

When you borrow from tomorrow to spend today, that leveraged spending is good for growth. At some point, you reach an end to just how much debt you can take on. Reinhart and Rogoff suggest that threshold, based on hundreds of years of study, is 90% debt-to-gdp. At some point, you cross a line.

I believe we are in a low growth deflationary pressured world until we solve and reorganize the debt mess. A global debt jubilee? We have a serious problem to solve and there is little motivation at this point to get started. The markets may just force that hand.

Trade Signals – Extreme Investor Pessimism (S/T Bullish); Cyclical Bull Trend Remains

S&P 500 Index — 2,127

Despite rich valuations and advanced age, the cyclical trend for the equity markets remains bullish. Sentiment moved to a state of excessive pessimism, which historically is short-term bullish for stock prices.

Many, including DoubleLine Capital’s Jeff Gundlach, are saying that yields have bottomed and are now moving higher. That’s bad news for bond investors and, as noted above, bad news for the March 2000-like bubble in the bond market. I’m not so sure. Let trend following help keep you in line with the major cyclical trends.

While not perfect, I believe it is a far better process than following consensus estimates. Recall the 25 out of 25 Wall Street analysts that said rates would rise in 2014 and 2015. Not one thought rates would head lower. I was wrong, too; however, rates moved lower and I profited. Trend following kept me on sides.

I’m a Gundlach fan, but I think he’s too soon on this one. Right or wrong, I have great confidence that trend will confirm direction. I’ll be happy to be wrong as long as I’m making money. “Let the trend be your friend.”

I post the Zweig Bond Model (trend following) each week in Trade Signals. It remains in a trend “buy” signal.

Posted each Wednesday, Trade Signals looks at several of my favorite stock, investor sentiment and bond market indicators. It is my weekly risk management dashboard, designed to keep me better in sync with the major technical trends. I hope you find the information helpful in your work.

Click here for the most recent Trade Signals blog.

Personal Note

Early next Wednesday, I’ll be heading to Charlotte for a meeting I’m particularly excited about. I am playing golf at one of my bucket list courses, Quail Hollow. It’s a “business meeting” I tell Susan and the kids and it really is. But what fun.

This particular meeting is about technology. I know we hear about “robo” everywhere. My view is that we will all embrace the functionality of so-called “robo” and use it within our practices. I want to make sure I and my team understand what is going on.

Firms such as Envestnet, Adhesion, Sawtooth, FolioDynamix and, yes, Betterment, provide resources for you and me to deliver managed solutions and a better client experience. Betterment, despite their recent stumble, and other retail platforms like them will seek to work with advisors. People need people.

You can access third-party ETF strategists from a shelf of offerings and seamlessly weave the ones you like best into your portfolios. Technology is leverage: Portfolio management in scale across your hundreds of accounts, performance reporting, back-office solutions and a client-friendly goals-based interface.

To this end, the meeting in Denver with Mauldin and team was productive. He and I believe that the next correction will prove significant. Both in loss if you are caught on the wrong side of the move and in opportunity if you are able to cross over the bridge and get to that opportunity in good shape.

Mauldin believes you need a combination of global ETF strategists with flexible trading strategies that complement each other by their diverse processes. I’m biased, of course, but I concur. More on this soon.

Thursday morning I fly from Charlotte to Indianapolis where I’ll get to meet and present with Coach Lou Holtz. I have heard that close to 1,000 investors will be attending. Way to go Brian Hayes! Looking forward to hear what Coach Holtz has to say. I hear he is quite a humble guy. Coach will be talking about Xs and Os and I’ll be talking about getting over that bridge in good shape — the need for strong portfolio defense as well as good offense. (Ugh, sorry about that.) I’ll see if I can record the session and share it with you.

I’ll be attending the Bloomberg Markets Most Influential Summit on September 28 with a day of media on the 29th. What a great time of year to be in New York City. I’m looking forward to cocktails with hedge fund legend Julian Robertson on September 27 and I’m really looking forward to dinner with my daughter Brianna. Her company is doing something innovative in our space. I thoroughly enjoy our business discussions. Kind of really cool.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts via twitter that I feel may be worth your time. You can follow me @SBlumenthalCMG.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Susan and I sat outside last night and enjoyed a nice glass of wine. The moon was nearly full and the air was filled with that slight chill of fall. Grateful only begins to express what I feel!

Wishing you and those you love most the very best!

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

[/drizzle]