By Steve Blumenthal

“We’ve been bulls on 30-year Treasury bonds since 1981 when we stated, “We’re entering the bond rally of a lifetime.”

“Their yields back then were 15.2%, but our forecast called for huge declines in inflation and, with it, a gigantic fall in bond yields to our then-target of 3%.”

“It’s still under way, in our opinion.”

– A. Gary Shilling

Let’s take a look today at just how attractive U.S. interest rates are relative to most of the world. To wit, the title of today’s piece, “The Best Looking Dude at the Dance.” Who in their right mind could have imagined that 1.50% would be attractive? We’ll look at the comparisons today and consider the implications. Lower for longer? Dr. A. Gary Shilling says yes. I’m getting concerned that too many are now in that camp (yours truly among them).

The bond market seems to have forgotten last Friday’s strong employment report. The worry about “What Would Janet Do” (raise interest rates) has subsided. The yield on the 10-year Treasury jumped from 1.49% to 1.58% back down to 1.50%. What is this telling us? One thing that’s apparent to me is that the global capital flow advantage goes to the U.S.

WWJD – here is what the CBOE’s Fed Watch tool is saying the probabilities are for a September 21 rate hike:

Source: CBOE

Further, the Fed meets on November 2 and December 14. CBOE puts the probabilities of a 25 bps to 50 bps FOMC rate hike at 86.2% in November and 57.4% in December (as of 10:45 am this morning). (This doesn’t mean they will hike each time.)

And what does this mean for you and me? I invited my banker to the golf course yesterday. He offered me a 2.75% for a 15-year mortgage. I hit that offer. Done – thanks Al. With many tuition payments to cover, the savings for me and my family is meaningful. For the record, I don’t think the Fed hikes. In my view, the debt drag and perfectly correlated low gross domestic product (GDP) growth are the main reasons.

Real GDP (ex. inflation) increased at an annual rate of 1.2 percent in the second quarter of 2016, according to the “advance” estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP increased 0.8 percent (revised).

All recessions since 1948 started with an average growth rate greater than the current 1.2% rate. There are three instances where the one-year growth rate was below the current level and recession did not occur. Two of those were 2011 and 2012, where weak growth was met with renewed rounds of extraordinary stimulus (QE). Only 18% of all observations going back to 1948 are below the current 1.2% growth rate level. Of that, 94% occurred during or within a calendar quarter of a recession. Source @michaellebowitz.

Goldman Sachs says the poor GDP showing was due to cutbacks in inventories. They noted the longest stretch in nearly 60 years. They say inventory restocking will contribute positively in the second half. Let’s hope so. An economy compounding below 2% is not good for us in the long term.

This post crisis recovery is, as Trump might say, “terrible, terrible”:

What about inflation? U.S. inflation (as measured by the PCE index) remains benign:

For now, I remain in the lower for longer camp and believe more extraordinary central bank measures remain ahead.

Turning to the stock market, the S&P 500 Index has a 2.2% dividend yield. Investors may be feeling that stocks are the “new bonds.” The S&P 500 Index hit another record (as well as the Dow and the NASDAQ indices). Technology is leading the charge. That’s good news for the CMG Opportunistic All Asset ETF Strategy as we are overweight tech. It’s good news for high yield bonds (which act much like stocks at times) and it is good news for long-term Treasury bond ETFs, such as EDV and TLT.

More on the lower-for-longer interest rate front. The Johnson Redbook Index (see definition in the following chart) fell below the lowest level since 2009:

Other assets have rallied aggressively YTD, such as gold (“GLD” +25.8%), silver (“SLV” +43.7%), utilities (“XLU” +19.3%) and high dividend payers (“NOBL” +14.2%). “Sell stocks and buy gold,” Stan Druckenmiller advised several months ago. Few can take such a highly concentrated bet. Few have that speculator’s gene, conviction, knowledge, passion and time. Generally, we continue to advise investors to diversify their portfolios among several risks. To concentrate one’s portfolio with only one or two big risks makes that person a speculator. In my view, one cannot be both an investor (diversified) and a speculator.

OK – enough rambling on my part. Grab a coffee and take a look at what Gary Shilling has to say in a piece he recently wrote, “The Bond Rally of a Lifetime.” You’ll see below that he continues to recommend long-term Treasury bonds.

I also share a few thoughts on Europe and its advancing sovereign debt crisis. Italian banks are in trouble (bail in or bail out is on the horizon) and something is troubling at Deutsche Bank. Click the orange link below.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Included in this week’s On My Radar:

- The Bond Rally of a Lifetime, by Gary Shilling

- 2016 Outlook Update – Italian Banks and Deutsche Bank

- The Best Looking Dude at the Dance

- Charts for the Beach 2016, by Richard Bernstein

- Trade Signals – Feels Like 1997 Absent the Cab Drivers Speculating on Stocks

The Bond Rally of a Lifetime, by Gary Shilling

In June, I wrote about Gary Shilling and shared some highlights from his presentation given at the Mauldin Strategic Investment Conference. In short, he sees too much debt globally, slow growth and U.S. interest rates heading even lower.

Early in my career, I worked for Merrill Lynch. In those days, we listened to the research team each day over what was called a “squawk box.” The great Bob Farrell, Stan Salvigsen, Chuck Clough and Richard Bernstein. Just before my start in early 1984, Gary Shilling was ML’s Chief Economist. He lost his job because he called for a recession. He was told that we sell only good news on Wall Street. His research turned out to be right. I’ve followed Gary for years.

Yesterday morning, the following came to me from John Mauldin (and to you also if you are a subscriber to his free letter, Outside the Box).

Here is what John said as he introduced the latest A. Gary Shilling letter:

In 1981, as inflation and Treasury yields were screaming to new heights, good friend Gary Shilling had the audacity to announce, ‘We’re entering the bond rally of a lifetime.’ He was right, as that bond rally is already 35 years old and I think it will see a few more birthdays. Gary’s with us today to assert that the rally is still underway – and to back up that assertion with a rather compelling case for Treasuries and for the “long bond” (the 30-year) in particular.

Gary recalls his famous public debate on stocks versus bonds with Professor Jeremy Siegel of Wharton, in 2006 – just before the Great Recession kicked in and sent Treasury prices sky-high. Siegel remarked to the audience of 500, ‘I don’t know why anyone in their right mind would tie up their money for 30 years for a 4.75% yield’ (the then-yield on the 30-year Treasury). When it was Gary’s turn, he asked the audience, ‘What’s the maturity on stocks?’ He got no answer, but pointed out that unless a company merges or goes bankrupt, the maturity on its stock is infinity – it has no maturity. His follow-up question was, ‘What is the yield on stocks?’ to which someone correctly replied, ‘It’s 2% on the S&P 500.’

Gary continued, ‘I don’t know why anyone would tie up money for infinity for a 2% yield. I’ve never, never, never bought Treasury bonds for yield, but for appreciation, the same reason that most people buy stocks. I couldn’t care less what the yield is, as long as it’s going down since, then, Treasury prices are rising.’

Gary admits that ‘It’s a lot more interesting at a cocktail party to talk about the unlimited potential of a new online retailer that sells dog food to Alaskan dogsledders than to discuss the different trading characteristics of a Treasury of 20- compared to 30-year maturity’; but in today’s OTB [Outside the Box] he gives us a whole list of excellent reasons to give Treasurys the respect they so richly deserve. Be sure to note Gary’s special offer of his monthly INSIGHT, at the conclusion of the article.

Gary believes the 10-year yield will drop to 1% and the 30-year yield will drop to 2%. Here is a chart he shared showing what will happen in regards to return. Note when rates drop 1% from a low rate of 3%, the principal gain on the bond investment (or ETF) is greater than if the yield drops from 6% to say 5%. Keep in mind, so is the loss should rates rise.

At such low yield levels, the risk/reward dynamic is greater. It’s dicey here folks. Shilling has a few educational pointers on how bonds work. It is well worth the read. Click here for the full piece and information on how to subscribe to Gary’s INSIGHT newsletter.

2016 Outlook Update – Italian Banks and Deustche Bank

Keep what is going on in Europe on your radar. I continue to feel that one of the large systematic risks is a European sovereign debt crisis. Here is what I wrote onDecember 31:

2016 Outlook: neutral on equities and neutral on fixed income. Nothing exciting there, but like the Fed, I’ll hedge and say it is “data dependent.” Following are the significant risks I see:

- Global Recession – Likely underway

- S. Recession – Possible in 2016. Probable in 2017.

- High-yield bond defaults – Rising in 2016, peaking in 2017 (tactically trade HY)

- European sovereign debt crisis – The EU banks are loaded up on that debt (shorting EU banks or buying out-of-the-money put options may be a good equity hedge).

- Emerging Market dollar denominated debt crisis

- Watch the Fed, ECB, JCB and Chinese central bankers

- Tax and structural reform would be a positive for the markets, but unlikely in 2016

A quick year-to-date review:

Score a big one for that “short” EU banks idea. Have you been watching what is going on with the Italian banks? The news seems to be swept under the rug. How about the stock price of one of Germany’s largest banks, Deutsche Bank (down 44% YTD)?

High yield defaults are rising but that doesn’t seem to be a party stopper. It’s been a bumpy year but a good one overall for high yield. And it seems to be off to the races again. Being the HY trend following manager that I am, well, happy. Hopefully, not too happy… you know how that goes.

Global recession may not be underway but concerns remain. A U.S. recession, in my view, remains unlikely this year.

The biggie on the watch list is a European sovereign debt crisis. The pressures there are building.

The Best Looking Dude at the Dance

The best looking dude, the cleanest shirt in the laundry pile. The… you get the picture.

Here are a few more charts:

Government bonds in Europe are issued at deeper and deeper negative yields:

Yield compression in India and China and most EM countries:

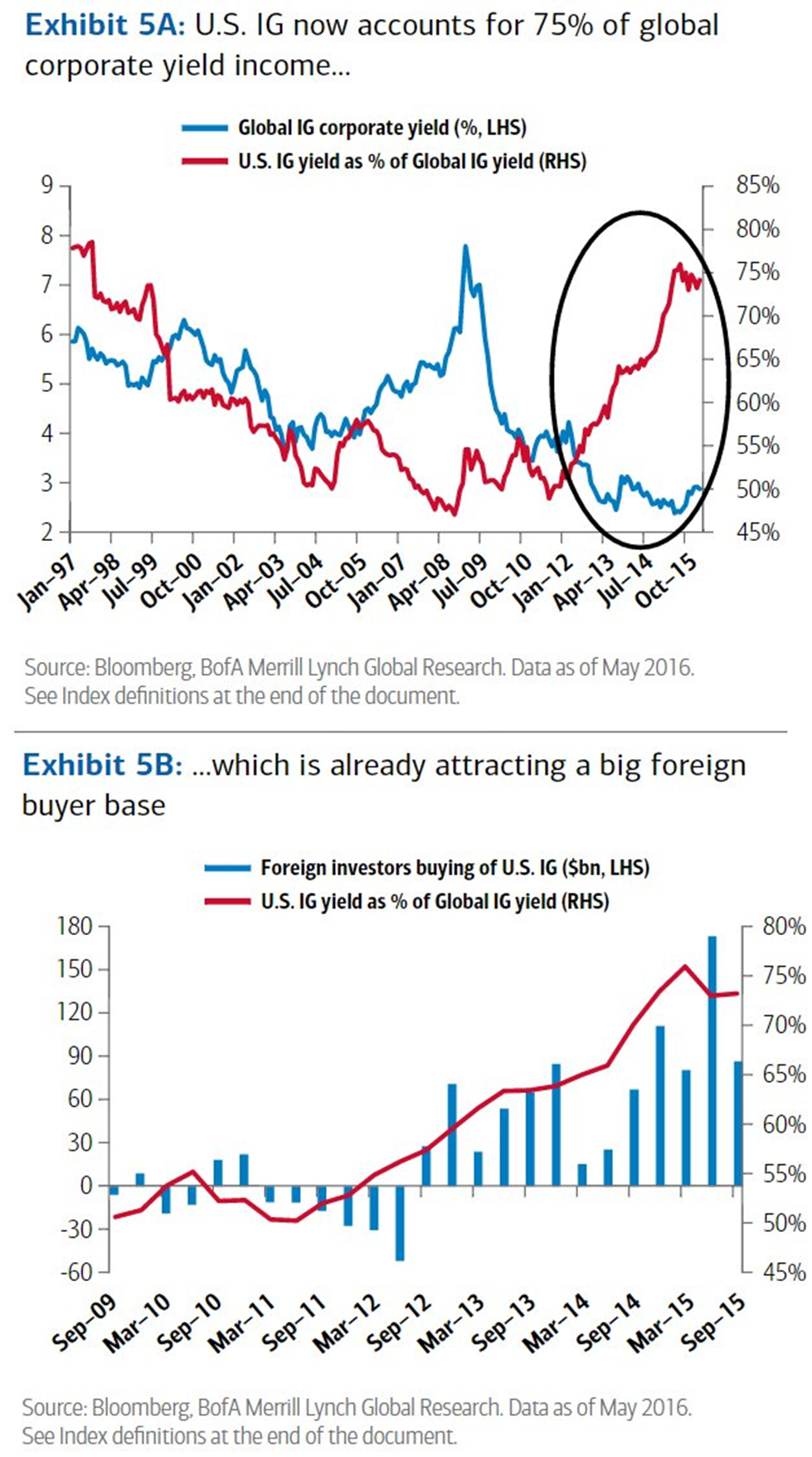

Huge foreign demand for the U.S. 10-year Treasury Note:

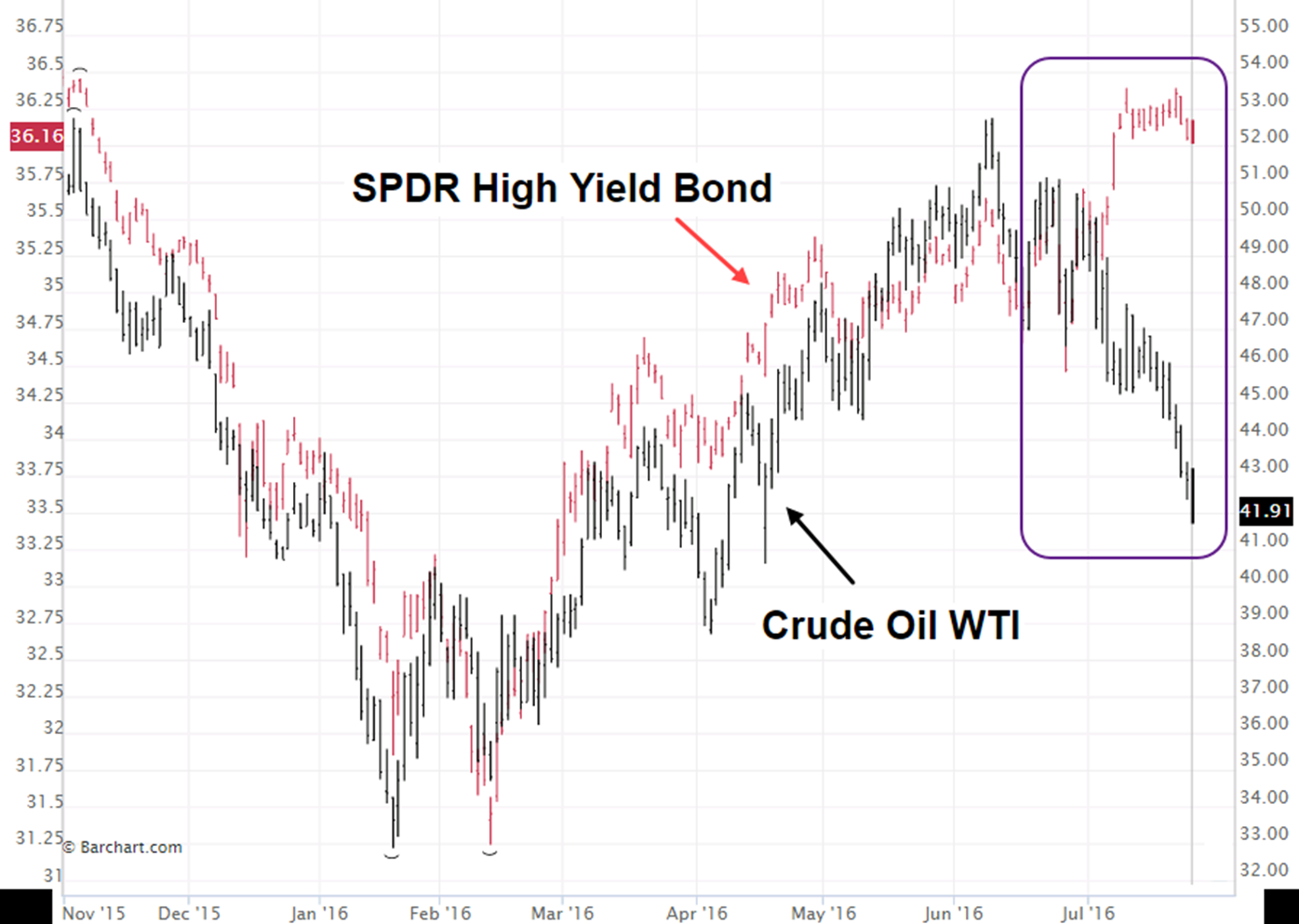

And two last charts on HY that make me happy – look at the drop in yield (which makes prices rise):

HY seems to care little about oil. Note that it no longer tracks the price of oil.

Charts for the Beach 2016, by Richard Bernstein

Every August, Richard posts his annual “Charts for the Beach.” Following Richard shares five of his favorite charts that highlight what he believes consensus is currently missing.

- Not the end of the world

Our first table compares the current market environment with that of 1999/2000, and one will note the stark differences between the characteristics of a true “bubble” and today’s market. For example, the S&P 500®’s PE [price-to-earnings] ratio in 1999 was 31 and the 10-year T-note was at 6.4%. Today, the PE is high by some standards (24), but the 10-year note is a mere 1.5%.

Source: Richard Bernstein Advisors LLC, Standard & Poor’s, Bloomberg Finance L.P.

*TMT = Technology, Media, Telecom

- Inflation expectations may have bottomed

The 5-year forward breakeven, supposedly the Fed’s favorite measure of inflation expectations, may have bottomed last February. Most equity and fixed-income portfolios seem incorrectly positioned if inflation expectations do indeed continue to increase. Anyone see the irony that “lower for longer” is now the widely accepted interest rate forecast at a time when inflation expectations might be troughing?

Source: Bloomberg Finance L.P.

- Everyone hates equities

Our Wall Street Sentiment Indicator, which is a measure of the consensus recommended asset allocation by Wall Street firms, continues to show that Wall Street prefers other asset classes to equities. Importantly, this was true throughout the entire bull market of the 1980s and 1990s. The only times in the last 30 years Wall Street recommended overweighting equities was just prior to the “lost decade” in equities and in early 2007, just before the onset of the bear market. Today, Wall Street is back to the bullish sign of suggesting that investors underweight equities.

Source: Richard Bernstein Advisors, LLC

- Is anything positive about Brexit?

The precipitous fall in the British Pound could help the earnings of UK multinational companies. That positive idea though is being buried in the symphony of comments on Brexit’s negative effects.

Source: Bloomberg Finance L.P.

- U.S. stocks are fairly valued

Richard Bernstein Associates remains quite out of consensus in our view that the U.S. equity market is not overvalued. One must keep in mind that it is not seven years ago and the market is not dirt cheap. However, our work suggests that the market is roughly fair value when the current S&P 500® earnings yield is compared to the current 1.5% 10-year note.

Source: Richard Bernstein Advisors LLC, Standard & Poor’s, Bloomberg Finance L.P.

Source and disclosures here.

Concluding Thoughts

Capital is a confidence game. Home country bias is the norm but it really is a global game and capital flows to where it is treated best. Lost confidence accelerates the pace. Money will run to safety. The U.S. capital market is currently the “Best Looking Dude at the Dance.”

That sovereign debt issue in Europe seems to be stepping center stage. Worry? Yes. But what about the Fed and the ECB you say? Yup, it seems like they’ve got our backs. Though, as Mohamed El-Erian writes in his book, The Only Game in Town, the central bankers are losing their effectiveness. Tax and structural reform is needed. I’m not sure when that fine gift is coming. We bet on continued effectiveness and politicians getting their acts together.

Back to Italy and back to that giant German bank, Deutsche Bank. Can you imagine the conversations that must be advancing behind closed doors at the ECB, the Fed and the IMF?

Remember the early news of that failed Bear Sterns hedge fund? The economy is just fine, they said. Housing has never declined, they quipped. No bubble, no way, they said. The Bear Sterns hedge fund collapse was a small ripple in the water until it was clear it was just the tip of a gigantic iceberg. Let’s not turn a blind eye.

The big problem globally is debt. We’ve promised too much and we need to restructure the great big fat mess. No small task. It can be done but I’m not so sure we have the Lee Iacocca-like talent in place at this time.

So risk remains. A sovereign debt crisis in Europe appears to be nearing. The EU banks are in trouble. Keep it on your radar. But the risk-on trade remains in place and we ride that wave.

Let’s cross our fingers, cross our hearts and pray that the guys with the big money-creating bazookas have big enough bazookas. I have my doubts that this time is any different.

Trade Signals – Feels Like 1997 Absent the Cab Drivers Speculating on Stocks

Click through to find the most recent Trade Signals. Here is a link to the Trade Signals blog page.

Personal Note

I was in NYC last Monday and had dinner with my beautiful daughter Brianna. A few bottles of yummy red wine and business discussions with my buddy John Mauldin and popular radio personality and good friend Josh Jalinski.

Great news on the personal front. Just after I hit the publish button, my job is to pack the cars. Well, that’s actually the bad news. The good news is that Susan and I are heading to the beach early tomorrow morning with our six kids. A week in Stone Harbor is ahead. And needed. But first, three cars, many bags, boogie boards, two surf boards, soccer balls, volley balls and the most current, most popular family game, Spike Ball, stuffed into the cars. And if I can find a case of the Troëgs Perpetual Grapefruit IPA, it gets packed too –even if one surf board has to go.

When I was a kid, my dad would rent a U-Haul, squeeze four kids in the back seat and we would pray that mom and dad would crack the windows so we didn’t have to choke on their cigarette smoke. But we couldn’t wait to get to Grandmom’s NJ beach house. Every day dad would lay out that ugly dark gray wool blanket on the sand with that silver transistor radio propped up in the corner. Baseball mitts, footballs and soccer balls. We’d body surf most of the day.

I’ll be speaking on portfolio construction using ETFs at the Morningstar ETF Conference on September 7-9 in Chicago. Please let me know if you will be attending. Denver follows on September 13-15 where I’ll be attending a one-day S&P Indexing Conference.

Wishing you and your family the very best! Relax. Have fun and don’t let the high valuations and low yields get you down. As Art Cashin says, “Stick with the drill – stay wary, alert and very, very nimble.”

If you find the On My Radar weekly research letter helpful, please tell a friend … they can sign up for the letter by clicking the “subscribe here” link that follows:

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, On My Radar. Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.