June 17, 2016

By Steve Blumenthal

“Everyone focuses on the Fed’s balance sheet – the $3 trillion dollars and the problems that creates. Don’t forget there is another balance sheet – that’s the balance sheet of us in the market that sold them the bonds and were forced into the risk assets that they’re so desperate to have us in. We have been forced into securities at subsidized prices. And when those subsidies are removed, those prices will adjust and they will do so immediately and they will do it on no volume… I predict from the beginning to the exit, the wealth effect of QE will have been negative.”

-Stanley Druckenmiller, CNBC 2013

(Note: The Fed balance sheet today is over $5 trillion. Yikes!)

-Danielle DiMartino Booth

Nearly halfway through 2016, most of the issues we faced at the beginning of the year remain today. With little overall market movement, the two most popular averages, the S&P 500 and DJIA, are little changed on the year – both up a small yet positive 1.5%.

The S&P 500 is lower than it was in December 2014. Perhaps not so coincidently, the Fed ended QE3 in October 2014.

At the same time, the global central banks continue to message, we’ve got your back, yet there are signs our collective faith in their power is waning.

I would feel much more at ease if valuations were reasonable. Unfortunately, they are not. At the end of May 2016, median price-to-earnings ratio (P/E) stood at 23.23. This compares to a 52.3 year average of 16.9. The median P/E was 22.0 on December 31, 2015 and it was 11.0 at the last crisis low in 2009. Here is a look once again at a few select periods in time. Buy low, sell high you say? Have a look at some evidence.

So let’s handicap the trading range this way. Fair value puts the S&P 500 Index at 1526.59. Undervalued (as measured by a one standard deviation move below fair value) puts the downside risk at 1061.03. Overvalued (a one standard deviation move above fair value) puts the upside target at 1991.21. We are trading near 2075 at the time of this writing.

Trading range:

Upside overvalued target: 1991.21

Fair Value: 1526.50

June 16, 2016 close: 2078 (4.4% above fair value)

The macro issues remain large (debt, deflation and aging demographics). Much of the developed world is in recession though not yet here in the U.S. Recessions matter to our collective wealth. That is typically when the large market dislocations occur and I believe one is nearing (2017 or sooner). So we stand watch.

Keep your eye on these six key recession points:

- Global trade has gone negative – that has never happened without a recession.

- The year-over-year change in Wall Street consensus 12-month earnings forecasts goes negative. When this happened in the past, a recession always occurred. It went negative at December 2015 quarter-end.

- Copper is signaling the global economy is in trouble.

- We have now had six consecutive quarters in earnings decline (year-over-year) – signaling recession.

- In the “not yet but we must watch closely” category: Recession occurs when the S&P 500 falls below its five-month smoothed moving average line by -4.8%. Since 1950, that measure has predicted 9 of the 11 recessions at or near the recession’s start.

- In the “not yet but we must watch closely” category: A negative yield curve has always signaled recession.

Risk is high and I believe we should be thinking a lot more about wealth preservation and a lot less about stretching for that extra base. Can the market trend higher? Sure. But at some point, investors are going to have that very difficult argument with reality. Let’s not be one of them.

My son Matthew was asking me about the economy. He’ll be interning at CMG this summer and I have to say it is so much fun having kids that ask really great questions about the economy and the markets. Entering the program, we have our interns read Ray Dalio’s 300-page letter on How the Economic Machine Works. Google it. It’s great! Share it with everyone you know. Matt is reading it now.

Try explaining to your teenager how the economic machine works, the role of the Fed, the meaning of Brexit (and related risks), global capital flows, what trillion means and how the various players in the game (you, me, institutions, politicians, central bankers, hedge funds, advisors, etc.) are going to behave. Or start with what is an ETF. A bit of a foreign language. So imagine how most of our clients must feel. Confusing stuff.

I’ve been doing a lot of writing about the Fed recently. In short, we are in an environment where it really is, “All ‘bout that Fed” and the global central bankers. But that will last until confidence is lost and, to that end, cracks are beginning to appear.

Over the last few weeks I’ve shared my conference notes with you. Click here for my summary of former Dallas Fed President Richard Fisher’s presentation. I walked away from my close interactions with Fisher and his analyst of many years, Danielle DiMartino Booth, a bit numb. Yes, I think numb is the right word. It was a peek behind the great Fed curtain with many beliefs confirmed.

“Unfortunately for the global economy, the inmates running the central banks’ insane asylums don’t get it.”

A reader sent me his market commentary this week and I shared it with Matt. I told him we’ll look back one day and say that the Fed was calling their plays from the wrong play book. Here is what I mean… as expressed exceptionally well in Jeffrey Miller’s letter… read on:

“There is a mountain of overvalued debt in the world and folks are beginning to wonder how long it can exist before it washes out to sea. About $8 trillion in debt around the world is currently trading at a negative interest rate, implying that the holders of this debt expect deflation for the foreseeable future. Smart, rational investors around the world are bemoaning the stupidity of this situation in increasing numbers, but central bankers push onward with their quest to drive rates even lower, in the hope (wrongly) that lower rates will spur lending by banks and investing by companies.

Yes, you read that right – the geniuses in Brussels think that lower rates will make banks want to lend more. Why? Because that’s what their broken models tell them. Don’t believe me? Watch this video on the inner workings of the ECB’s bond buying operations. Skip ahead to the 2:30 mark for the explanation of why they are doing it, but be sure you’re alone, because if you think about what he says, you’re going to want to scream. If you want to understand the crazy distortions in bond markets today, take 3½ minutes to check it out.

These economists all follow the Keynesian theory that we have a consumption problem – i.e., that consumers aren’t buying enough stuff to create scarcity and drive up inflation to their preferred target. For some reason, they think that lower rates will drive consumption, despite the fact that ultra-low rates for the past seven years have failed to do just that. They think that consumption is a borrowing-cost problem, when in reality it’s an income problem. (Emphasis mine).

And they are the ones that are creating it. How? By stripping massive amounts of interest income out of the economy. When the Fed buys bonds and artificially lowers interest rates below their natural market-level, they are stripping income from the economy. That 5% in interest payments that the government used to pay to savers, insurance companies and pension plans is now under 2% and mostly paid to the Fed. What does the Fed do with its interest payments? Nothing. It simply gives it back to the Treasury.

All that income is taken out of the system. Sure, some investors move on to other yield investments, which explains the overvaluation of income stocks like utilities and telecoms, but there is more uncertainty in these securities, more volatility in their prices, and therefore a lower propensity to spend the income they generate – so savers hoard their assets instead of spending the income. This explains the really low velocity of money in the U.S. economy, because when savers, like retirees in Florida, can’t earn enough income from bank CDs and Treasuries, but are forced into risky assets they really don’t want to own just to earn enough income to pay the rent and food, they aren’t going to be out there spending on anything but the basics. That new outfit? It can wait. New golf clubs? Fancy meals out? I’ll stay home and cook instead.”

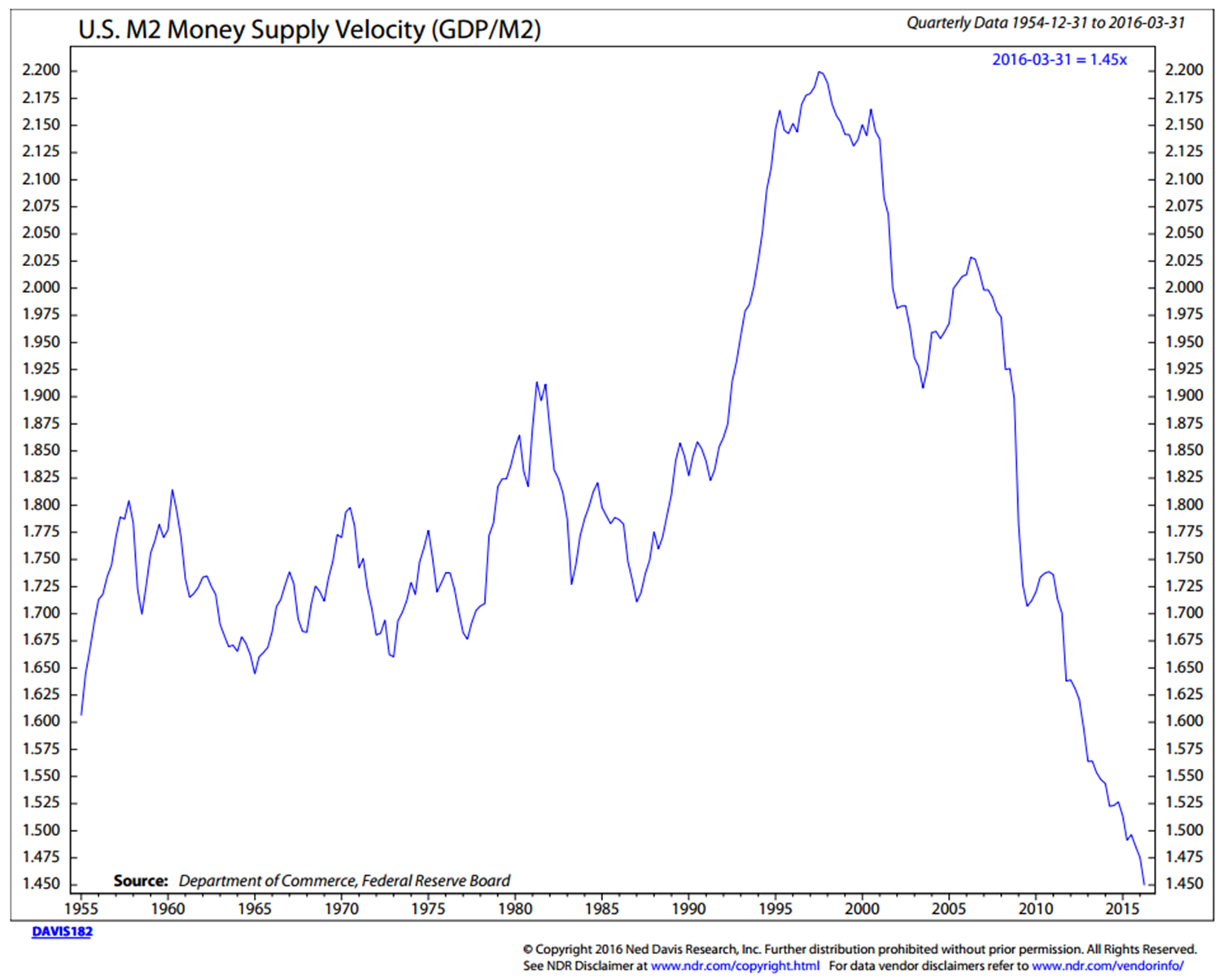

A quick timeout… Here is what this looks like in a picture (the following chart looks at the velocity of money since 1955. It has fallen off a cliff):

The velocity of money is the rate at which money is exchanged from one transaction to another and how much a unit of currency is used in a given period of time. It is how much money is going around and around in the system. We collectively cut down on our spending and M2 slows. Look at that history. We have never seen anything like this.

Ok, back to Jeffrey’s comments:

“So when these savers fail to spend, the Fed, and its 750 Ph.Ds. decide that well, our models show that lower rates should boost spending (how? they never explain, because it doesn’t work), so we’re going to just lower them more, or put off raising them, despite the evidence (see Japan) that low rates do not create inflation or more spending – they kill it.

If you want to create more spending and monetary velocity, you need to increase consumers’ income. You need to get them more income today than they had yesterday and they need to feel confident that the increase in income is safe and sustainable. Want to increase spending at restaurants in Florida? Take Fed Funds to 6% again. Want to make pension plans solvent? Take Fed Funds to 6% again. Want to see banks falling all over themselves to make loans to small businesses again? Take Fed Funds to 6%. It’s simple.

Don’t believe me? Give every saver with $500,000 in investable assets an additional $25,000 a year in income and see what happens. The Fed has the power to increase incomes tomorrow if it wanted, but it doesn’t really understand that. Incomes create spending, which will create the inflation they want.

Don’t believe me? Give every person of working age in the U.S. one million dollars tomorrow and see what happens to inflation – there will be lines out the door of every Best Buy and auto dealer in the country. Too simple? Maybe. But directionally, that’s how it works. Unfortunately, for the global economy, the inmates running the central banks’ insane asylums don’t get it.

The global hunt for yield has created some really risky securities, which investors would do well to avoid seeing in their portfolios despite the fact that they have been some of the best performing sectors in the U.S. stock market recently. In particular, utilities, telecoms and consumer durables stocks are trading at ridiculously high valuations as investors try to hide in “low vol” stocks and yield plays. Unfortunately, those needing safety and income the most are the ones most at risk in this market as these stocks are pricing in all future returns today.

Quoting John Hussman’s latest letter:

An extended period of modest interest rates encourages investors to forget what I often call the “Iron Law of Valuation”: the higher the price an investor pays for a given set of future cash flows, the lower the long-term investment return one can expect. With every increase in price, what was “expected future return” only a moment earlier is immediately transformed into “realized past return,” leaving less and less future return on the table. Investors over-adapt to low short-term interest rates by chasing yields and driving up the valuations of much riskier securities (mortgage securities during the housing bubble, equities, corporate debt, and covenant-lite junk securities in the current episode). The rising asset prices also convince investors that risky assets really aren’t actually risky, and a self-reinforcing bubble results. Ultimately, low interest rates aren’t followed by high investment returns at all. Rather, low interest rates encourage concurrent yield-seeking speculation for a while, but after an extended period of yield-seeking, the overvaluation is followed by awful subsequent outcomes over the completion of the market cycle.

Lots of smart investors are saying markets are at unsustainably high levels and are preparing for a selloff. Bill Gross warned of a bond market “supernova.” Soros is taking down his firm’s equity exposure and buying gold. Same for Druckenmiller.”

Excerpts above from: “Blowin’ In the Wind” by Jeffrey Miller, Eight Bridges Capital Management. You can find the full piece here.

Raising the Fed Funds rate to 6% is not going to happen. Though I am in the raise the interest rate camp. Yellen was again dovish (the economy is not strong) this past Wednesday.

This week let’s take the Federal Reserve theme one short step further with sound advice from a former Fed insider. Danielle says, “Raise the floor on interest rates to two percent and vow to never again breach that raised floor.”

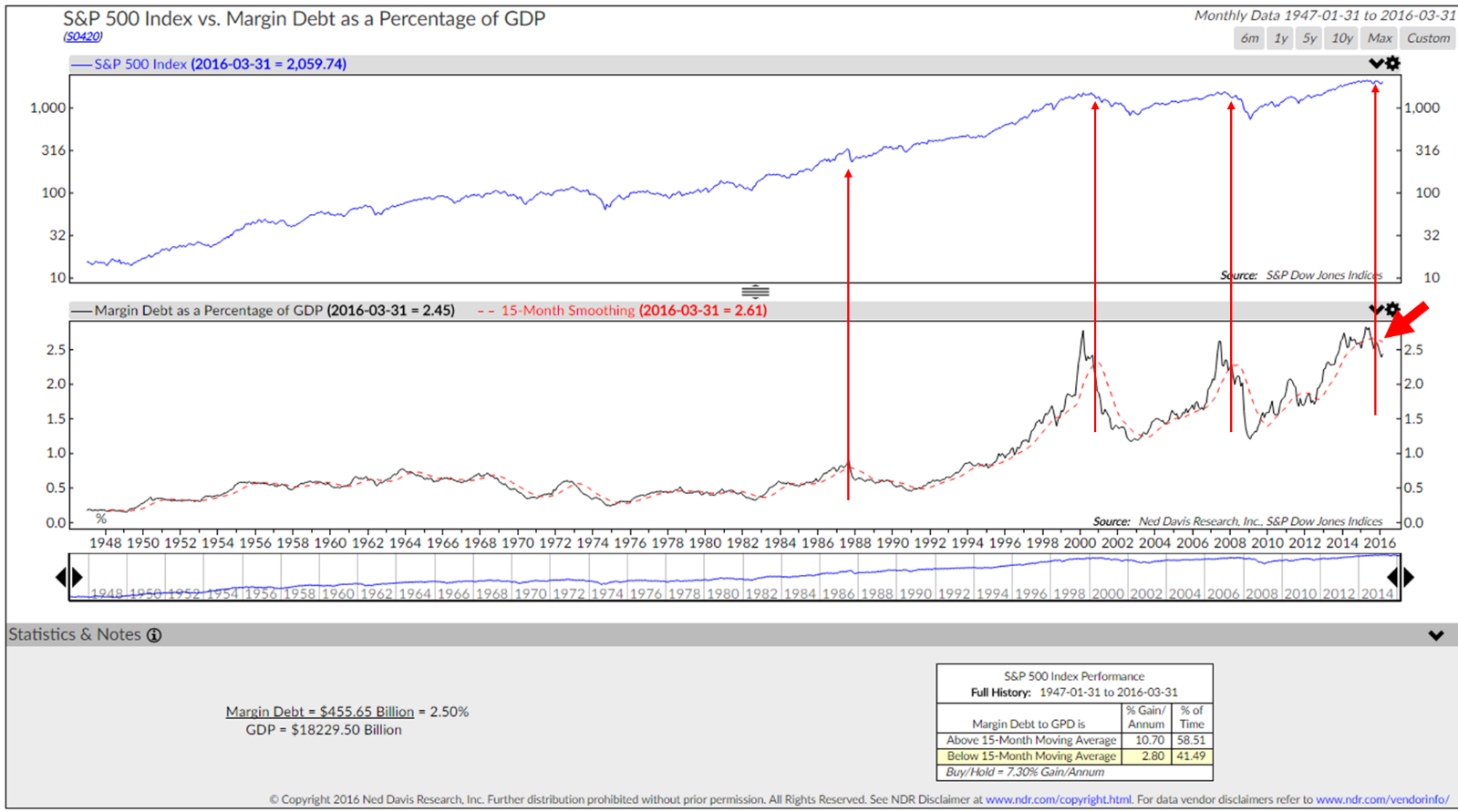

Let’s also take a quick look at margin debt (record highs) and stockholder ownership (higher than in 2007). Yep – the chips on the table are pushed to the center. Investors are all in.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Included in this week’s On My Radar:

- The Vanity of Central Bankers and the Common Sense Rule

- A Look at Total Margin Debt and Stock Ownership

- Trade Signals – Gold Shines, HY Sells and S&P 500 Remains Lower than it was in December 2014

The Vanity of Central Bankers and the Common Sense Rule – Danielle DiMartino Booth

I very much enjoy reading Danielle’s weekly blog. She is creative, bright and highly critical of the Fed’s current path. “Vanity” and “Common Sense.” Her post this week didn’t disappoint. Following is her conclusion with the link to the full piece below.

“Raise the floor on interest rates to two percent and vow to never again breach that raised floor.” (Emphasis mine)

Will such a radical commitment ever come to pass? It’s impossible to say. But it would be a refreshing change from the norm that’s prevailed for near on 30 years. And wouldn’t it be a relief to return to a rules-based discipline instead of the smoke and mirrors of today’s undisciplined approach where contrived language, convoluted math and the always popular throwing spaghetti against the wall to see what sticks are employed with disastrous results?

Acknowledge that there is no single certainty in this world other than that of uncertainty. Or as Taylor himself wisely observed, “Uncertainty exists in the real world; you can’t ignore it whether you use rules or discretion.”

Waiting for the Godot of central banking has caused this nation undue harm by anesthetizing U.S. politicians and households to the inherent dangers of over-indebtedness. Period. End.

That said, with all deference to Ron Paul and his acolytes, the Fed does not need to be ended. We are not, nor ever shall be, a third world banana republic. Therefore, a central bank in some form is a given.

That is not to deny that the Fed is sorely in need of reform. In fact, a total re-engineering would seem to be in order, applying the same methods many of us learned in business school. Who said that in order to exact meaningful change, one must first create chaos? Let’s do just that.

Vanity has no place in central banking, nor should it. But that very weak and vainglorious predilection seems to have nevertheless crept into a group of leaders tasked with staying above the fray. We can hope that public outrage tempers the hubris driving our current monetary policymakers to such extremes. We can hold out for Common Sense ruling the day. Let there not be those among us “So Vain” that they believe it is all about them and not “We The People.”

Click here for Danielle’s blog.

A Look at Total Margin Debt and Stock Ownership

As you can see in this next chart. Margin debt is excessive. I’m not sure if individuals are borrowing from their stock accounts or buying 2x stock with every 1x dollar. Either way, too much margin debt is a bad thing when it unwinds. Note the “Excessive Speculation” in the upper right hand section of the chart.

It is when margin debt peaks and begins to decline that we should move to higher alert. That is what is happening now (large red arrow shows that total margin debt as a percentage of GDP is now below its 15-month smoothing. The thin red arrows mark prior periods when margin debt dropped below its smoothing):

Source: NDR

When margin debt is high and markets decline, margin calls get triggered, which can lead to more forced margin call selling – and would-be buyers simply step aside. That is why markets dislocate from time to time. Leverage works well in up markets. Excessive speculation drives prices higher (like 2000 and 2007) and can be measured by total margin debt. Today, as indicated above, margin debt is very high and trending lower.

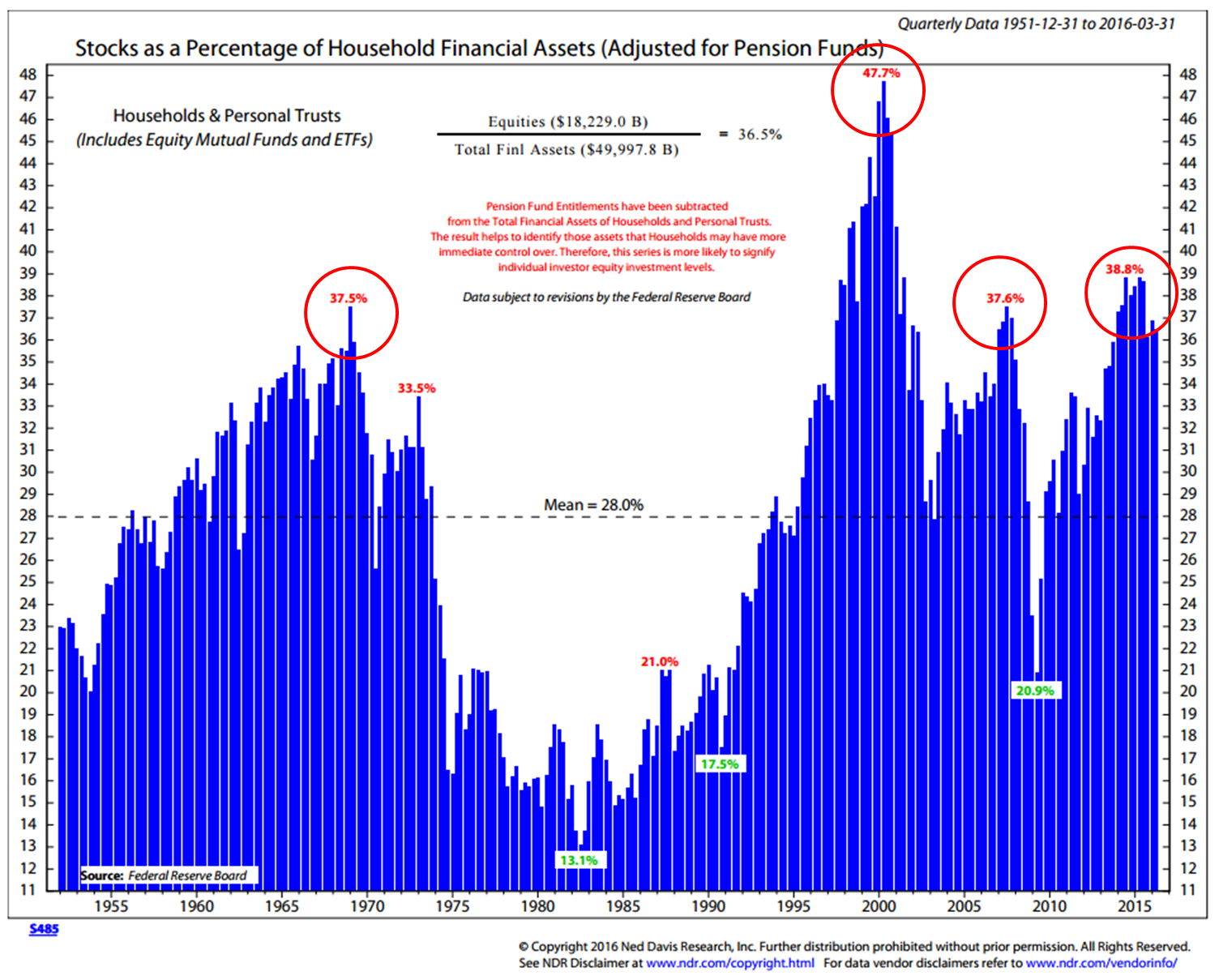

I often hear that individuals are not in the market. That there is now excessive speculation. But as you can see in these next few charts, individuals are nearly as fully invested as they were in 2000 and 2007. Cash levels are low. There is just not as much fuel in the tank to do more buying. This too suggests caution.

Circled in this next chart is the 1965 secular bull market peak, the 2000, 2007 and 2014 recent peak in individual’s stock ownership.

Note too where stock ownership was after the corrections occurred. 13.1% when the bull market started in 1982. 28% at the 2002 low. 20.9% at the 2009 low.

Corporations have been large buyers of stocks. That has helped lift prices. Foreigners own a large amount of U.S. equities as do U.S. pension and insurance companies but yet they could buy more. Will foreign capital flow to U.S. equities seeking a safer home? Maybe but if that is my investment thesis, then I’d rank the probability low.

Concluding Thoughts – Kumbaya, My Friend, Kumbaya

Market commentators are saying that a partnership between the Fed, elected officials and private business must be forged – not just in the U.S. but in the balance of the developed world.

Our collective hope may just rest in a kumbaya moment where the ECB, BOJ, China and the Fed all hold hands together with their respective elected officials and invent a global debt forgiveness jubilee. Prevented is a currency war unless you are one of the smaller emerging countries who will get stepped on if this song is sung.

Sing with me… “Kumbaya, my lord, kumbaya.”

Mohamed El-Erian believes we have reached a t-juncture. We have come to a “T” in the road. We have two options. We can turn left or we can turn right. One turn is the road where we do little. The other turn is the kumbaya road where the central bankers work in partnership with the legislators who have the power to do the heavy lifting.

What are the odds of a U.S. kumbaya moment? What are the odds of an EU kumbaya moment? Japan? What are the odds of a unified U.S., EU, BOJ and China moment? You tell me… I believe it is not a high probability outcome. And if kumbaya comes to be, will it work? Maybe…

The Brexit vote is up next (June 23) – it is no small event. “Oh lord, kumbaya.”

As Danielle said, “Waiting for the Godot of central banking has caused this nation undue harm by anesthetizing U.S. politicians and households to the inherent dangers of over-indebtedness. Period. End.” To this I most agree.

There are short-term debt cycles and there are long-term debt cycles. Long-term cycles are different. We’ve had them before; however, few of us have experienced them. Think 1930s. Know that they are different.

Hedge that equity exposure, diversify, stay tactical and stay extremely alert.

Trade Signals – Gold Shines, HY Sells and S&P 500 Remains Lower than it was in December 2014

Click through to find the most recent trade signals. HY moved back to a sell signal early in the week. We are seeing a move toward more fixed income in our tactical all asset strategy. High quality bonds remain in a buy signal as indicated by the Zweig Bond Model. Trades Signals is posted each Wednesday. Here is a link to the Trade Signals blog page.

Personal Note – Father’s Day

I’ll be in New York next Thursday and on Friday Susan and I are flying to Dana Point, California. I’ll be speaking at the 21st Annual Global Indexing & ETFs Conference. The plan is for a few days on the beach before the conference begins. Sunsets with red wine in hand. That will be nice. (Let me know if you are attending the conference…)

Chicago follows on July 20-22 for a large advisor client conference. For now, August is quiet and in September I’ll be speaking at the Morningstar ETF Conference about portfolio construction.

Father’s Day is Sunday. On that score, I love being a father. Uncle Jim is in for a few days. Brianna is coming home from New York and we’ll have the whole gang together. One of the things I look forward to most is our cookouts and dinner on the back patio. That’s the plan for this evening as we kick off the weekend with an early Father’s Day celebration.

And I’m going to toast my dad on Sunday as I watch the U.S. Open with my guys. Miss him.

Importantly, here’s a toast to you and your father!

From my family to yours, Happy Father’s Day!

Thanks for reading. I’m humbled that you take the time each week. I truly hope you find the information thought provoking and helpful in your work with your clients.

Tell a friend… they can sign up for the free letter by clicking the “subscribe here” link that follows:

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Wishing you the very best.

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.