“Davidson” submits:

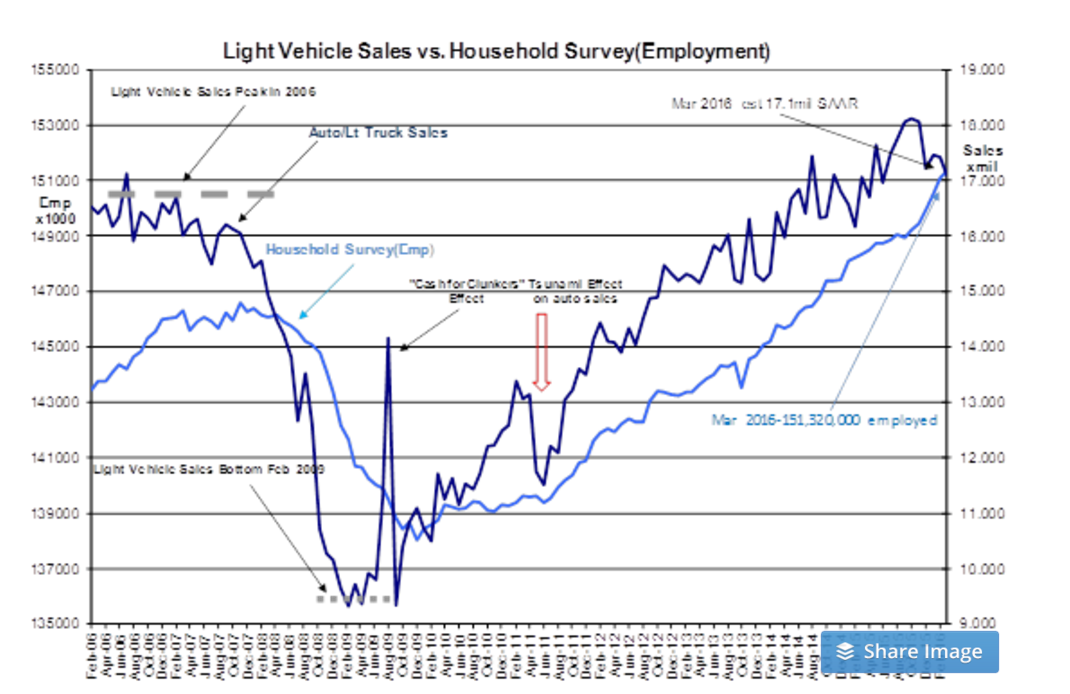

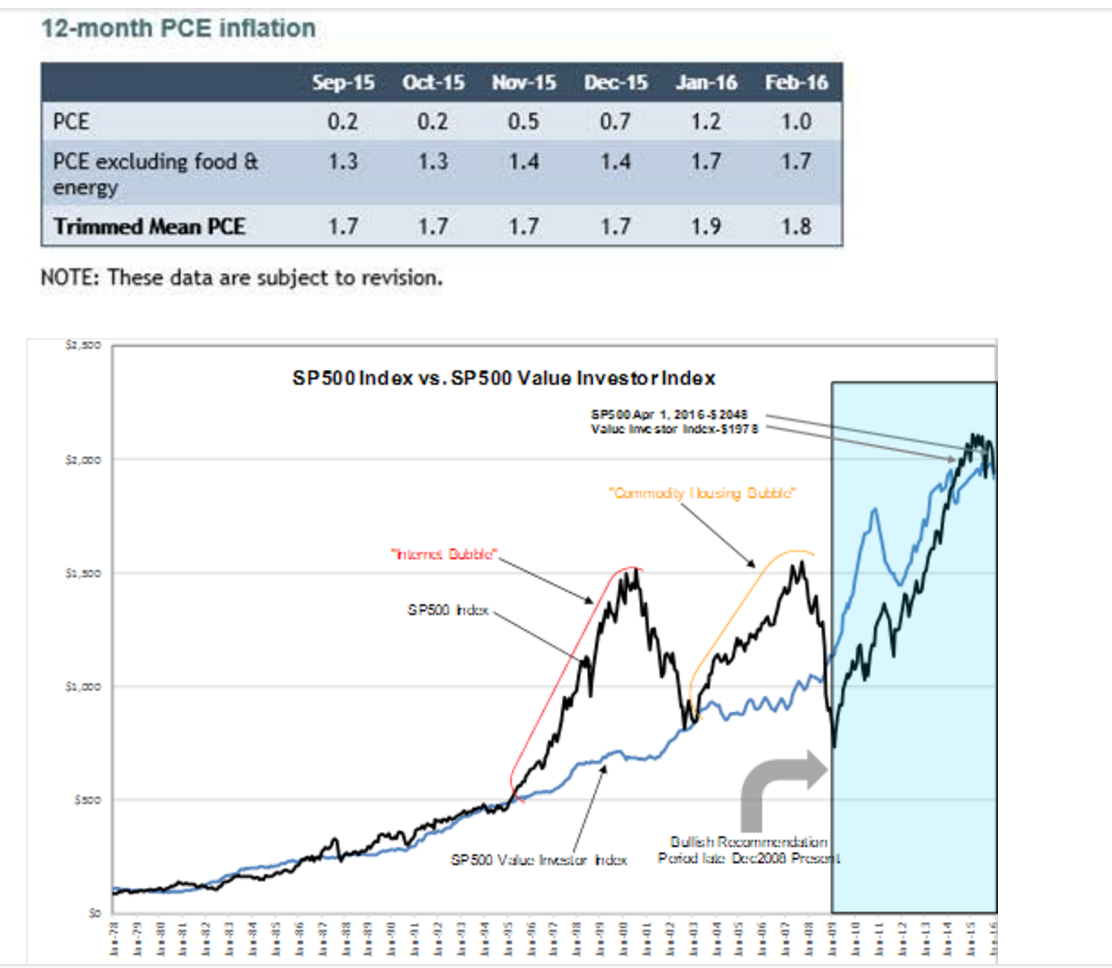

There is nothing from my perspective to argue about our economic trends since 2009. The trends continue higher with employment hitting new highs, 246,000 added to the March Household Survey, vehicle sales continue at record levels, 17.1 March SAAR (Seasonally Adjusted Annual Rate) and the Dallas Fed 12mo Trimmed Mean PCE for Feb reported at 1.8%. The SP500 Value Investor Index at $1,978 vs SP500 at $2,048 remain within 5% of each other which historically indicates that, even with the wild swings we have encountered the past several years, market speculation remains at muted levels.

While current economic activity reflects decent uptrends, pessimism remains, but there are signs that some may be turning more positive. A psychological swoon found its low early February 2016, as I pointed out in a recent note. One can see in the employment trend that one of the most fundamental measures of the direction of economic activity ignored February’s swoon. This is how one separates out false market psychology fears of recession vs those which are driven by economic activity. There remain several prominent investors still forecasting economic collapse in 2016 with more than 30% declines in market prices. Some even forecast a Dow Jones at 5,000, a huge decline from the 17,600 level today. One can never say that these forecasts will not occur. One can only say that, when this level of pessimism differs so much from economic fundamentals, it is the fundamentals which have always forced psychology to follow. Market psychology never leads long term economic fundamentals even though it certainly impacts prices short term.

The swings in market psychology make investing a confusing process because so many who seem so successful provide their advice in the media. Almost every forecast has urgency to ‘…take action now’ and of course to give your portfolio to them and pay their fees. Had you actually followed these calls, you would have traded your portfolio at least a dozen times since 2009. Your timing would have been exceptionally poor with similar returns.

Economic trends, if watched closely, provide plenty of warning of pending economic cycle tops and cycle bottoms in my experience. Market psychology as you should have learned by now, certainly by what you have experienced since 2009 and even the past 18mos, can be wild, is often wrong and certainly unpredictable. Market psychology has always turned back to being more positive if economic fundamentals remain so. It is not market psychology which drives the economy, even if many believe it to be true. These investors are price-trend followers, Momentum Investors. They control a lot of capital. Momentum Investors do not drive their decisions with economic fundamentals. They only use price trends. They do not see the correlation between fundamentals and prices because their time frames are short term. They do drive their investing with ‘Headlines’ of ‘Good News’ vs ‘Bad News’. Their pattern longer term is that news that is better than expected triggers Momentum Investors to invest. They believe better news than expected justifies higher prices and vice versa. Fundamental trends drive whether the news will be better or worse than many anticipate. This is why following economic fundamentals which trend at a relative ‘snails pace’ lets long term investors anticipate whether the ‘news’ is going to be better or worse than that anticipated by Momentum Investors. Using economic fundamentals is the Value Investor approach. I anticipate higher market prices because pessimism continues to dominate the news even in the face of decent economic growth.

I continue to recommend that investors focus on LgCap Domestic and Intl equities and have exposure to Natural Resources. As the US$ Trade Weighted Index continues to fall towards its historical levels, we should experience decent returns in these categories.