With all the attention on Valeant lately it has reminded me of Buffett’s Salomon adventure. No, I am not saying these two situations are “exactly” the same but there are a ton of similarities. For those who want the crib notes:

1- Buffett made his largest single investment ever in a company when he put $700M into Salomon (~$1.25B today)

2- That was 1987 and Buffett also took a seat on the Board

3- In 1990-91 Salomon traders broke the law in rigging Treasury auctions (details below)

4- Where it not for Buffett agreeing to help run it, Salomon would have probably filed Chapter 11 as the NY Fed was about to cut it off and his entire investment then lost as it was levered ~33-1 at the time (Lehman at its collapse was only 30-1).

From Fortune (full article here)

HOW IT BEGAN

That Sunday in August was a far cry from the commercialism of another Sunday, Sept. 27, 1987, when Buffett and John Gutfreund, then Salomon’s chairman and CEO, agreed that Berkshire Hathaway would buy $700 million of Salomon convertible preferred stock, which equated to a 12% stake in the company. The deal allowed Gutfreund to stave off takeover artist Ronald Perelman, who seemed poised to buy a large block of Salomon common stock from certain South African investors wanting to sell. With Berkshire’s $700 million, Gutfreund was able to strike a deal that allowed Salomon itself to buy the South African stock–and with that, Perelman was dispatched.

[drizzle]It was easy to see why Gutfreund welcomed Warren Buffett, White Knight. It was less easy to see why Buffett wanted to hook up with Salomon, much less trust it with this mint, $700 million–the largest amount he’d ever invested in a single company. Over the years, Buffett had derided investment bankers, deploring their enthusiasm for deals that provided huge fees but that were turkeys for their clients. He has also spoken often of wanting to work only with people he likes. So here he was, handing over mountains of Berkshire’s carefully accumulated and husbanded cash to the high-living, cigar-chomping, corner-cutting crowd soon to be made infamous in Liar’s Poker?

Several reasons explain the move, none of them really good enough in the light of what followed. One is that Buffett had been having trouble for a couple of years finding stocks he thought reasonably priced and was looking for fixed-income alternatives. A second is that the Salomon proposal came from John Gutfreund, whom Buffett had seen do principled, non-greedy, client-friendly work for GEICO, in which Berkshire was then a major stockholder (and which is now owned 100% by Berkshire). Buffett liked Gutfreund–still does, in fact.

A third explanation was simply that Buffett thought the terms of the deal worth accepting. In effect, convertible preferreds are fixed-income investments with lottery tickets attached. In this case, the security was to pay 9% and be convertible after three years into Salomon common stock at $38 a share–against the $30 for which the stock had been selling. If Buffett did not convert the stock, it was to be redeemed over five years beginning in 1995. To Buffett, it looked like a decent proposition. “It’s not ‘a triple,’ which is what you’d like to have,” he said to me in 1987, “but it could work out okay.”

To some of the brainy, mathematical types at Salomon, that appraisal would have qualified as the understatement of the year. From Day One, they thought–and let it be known to the press–that Buffett had exploited Gutfreund’s fear of Perelman and had secured a dream security, with a too-high dividend or a too-low conversion price or some combination thereof. Over the next few years, this opinion did not die at Salomon, and more than once executives of the firm (though never Gutfreund) came to Buffett with propositions for deep-sixing the preferred.

It’s fair to say that Buffett might have taken those offers more seriously had he known that ahead lay the business-wrecking, profit-shredding scandal that broke in August 1991–and that turned the world upside down for both Salomon and him.

A little stage setting here: Before the crisis hit, Salomon was on its way to an excellent business year, marred only by a Treasury investigation into a May T-bill auction in which Salomon was thought perhaps to have engineered a short squeeze. Despite that sticky matter, Salomon’s stock had climbed to $37 a share, a price very near Buffett’s conversion point of $38.

THE PHONE CALL

For the story of what then happened, we may begin with Buffett in Reno. Yes, Reno, which was the spot two executives of a Berkshire subsidiary had picked for an annual getaway with Buffett. Arriving in Reno on the afternoon of Thursday, Aug. 8, Buffett checked with his office and found that John Gutfreund, en route at that moment from London to New York, wanted to talk to him that evening. Gutfreund’s office said he’d then be at Salomon’s principal law firm, Wachtell Lipton Rosen & Katz, and Buffett agreed to call him there at 10:30 P.M. New York time.

Mulling this over, Buffett concluded that it couldn’t be bad news, because Gutfreund hadn’t been in New York to attend to it. Maybe, he thought, Gutfreund had made a deal to sell Salomon and needed a quick okay from the directors. Heading out to dinner in Lake Tahoe, Buffett actually told his group that he might be hearing “good news” before the evening was out–a characterization indicating Buffett was ready to bail from this supposedly plummy deal he’d got into four years earlier.

At the appointed time, breaking from dinner, Buffett stood at a pay phone to make his call. After a delay, he was put through to Salomon’s president, Tom Strauss, and its inside lawyer, Donald Feuerstein, who told him that because Gutfreund’s plane had been held up, they would instead brief Buffett on “a problem” that had arisen. Speaking calmly, they said that a Wachtell Lipton investigation commissioned by Salomon had discovered that two of its government securities traders, including the top gun, managing director Paul Mozer (a name Buffett didn’t know), had broken the Treasury’s bidding rules on more than one occasion in 1990 and 1991.

Mozer and his colleague, said Strauss and Feuerstein, had been suspended, and the firm was now moving to notify its regulators and put out a press release. Feuerstein then read a draft of the release to Buffett and added that earlier in the day he had talked at some length to Salomon director Charles T. Munger, Berkshire’s vice-chairman and Buffett’s sidekick in everything important.

The release contained only a few details about Mozer’s sins. But a fuller account dribbled out over the next few days, depicting a man at war with the Treasury over bidding rules that he despised. A new rule, promulgated in 1990 to prevent such behemoths as Salomon from cornering the market, said that a single firm could not bid for more than 35% of the Treasury securities being offered in a given auction. In December 1990 and again in February 1991, Mozer simply made hash of this rule by, first, bidding for Salomon’s allowable of 35%; second, submitting, without authorization, separate bids for certain customers; and, third, simply stuffing the securities that these bidders won into Salomon’s own account, never telling the customers a word about the whole exercise. From all this, Salomon emerged with more than 35% of the auctioned securities and with increased power to swing its weight around.

It was so bad at the time Buffett had to do a mea culpa before Congress.

Solomon recovered and was later sold to Travelers for $9B in 1997 (Buffett’s stake more than doubled).

It matters here because Valeant, for all of it issues has not broken any laws. We can make moral judgements all we want about drug pricing but the fact remains laws were not broken and they are at very little risk of a Chapter 11 filing. Sure, the media will make a huge deal out of the April 29th deadline but they will file before then and this risk is removed…

Remember folks, the media cares very little about the reality of any situation, they care most about ratings and nothing gets ratings like potentially huge drama.

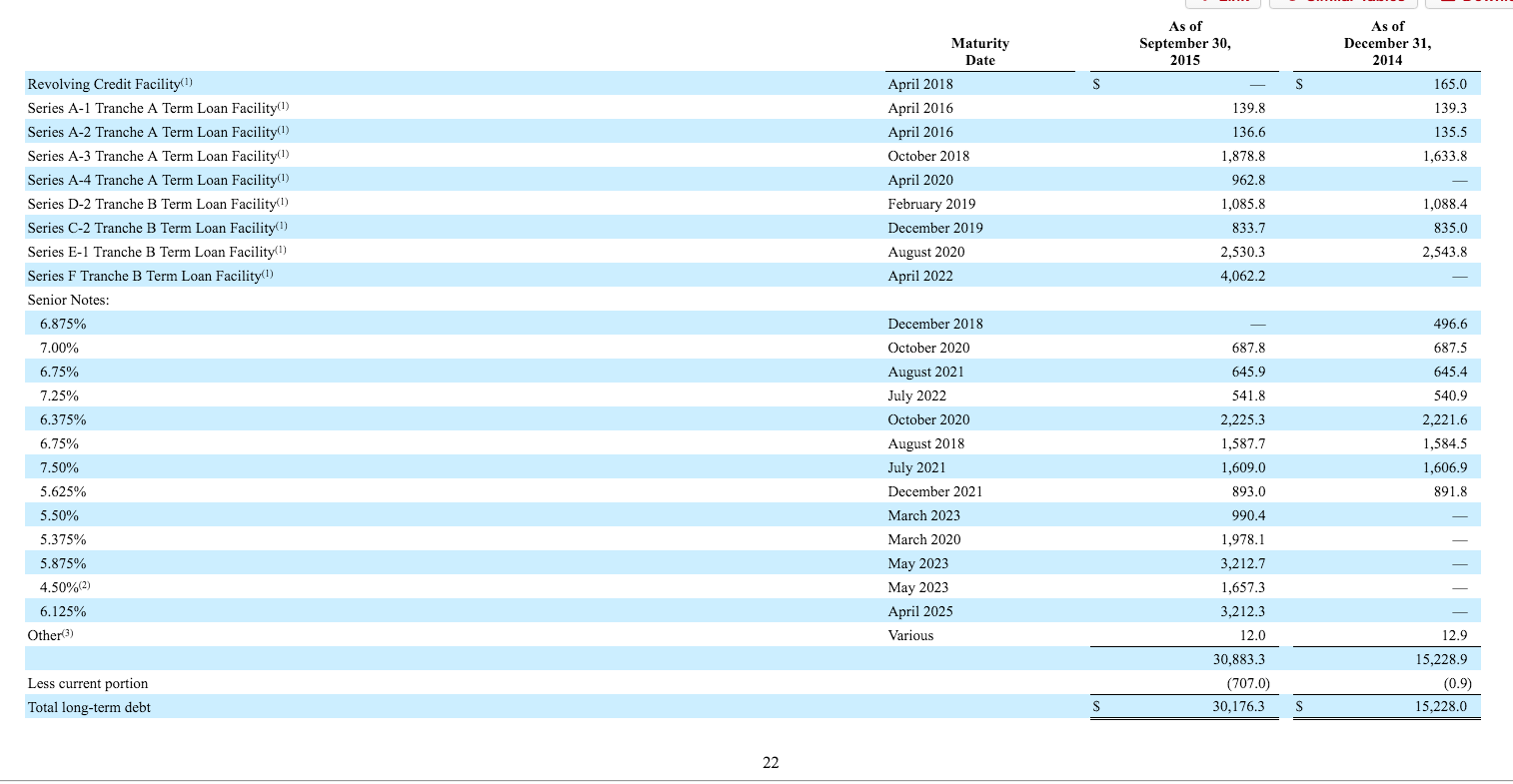

So, Valeant files it 10k and default risk is removed. So, where are we then? They have ~$1B in cash and practically no debt maturing in 2016, none in 2017 and ~$3.5B in 2018. Along the way they bring in ~$6B in EBITDA in 2016 and let’s call the annual number for 2017, 2018 flat so they earn roughly $15B EBITDA between now and before the first debt is due in August 2018 ($1.6B). Even if results fall, it would have to be an utter collapse for there to be debt issues. Additionally, all of this assumes they do not sell something between now and then to pay down debt early.

Then they have nothing until 2020.

The bottom line is they have a very long time to get their act together.

Valeant is looking compelling here. The stock collapse has stopped, the largest investor in on the Board now and there is a new CFO and CEO coming in. A top notch CEO with industry cred (think Hunter Harrison at Canadian Pacific) could turn sentiment about the company around instantly. We have to remember, even with its current issues, it is still a very profitable company for those buying shares here.

Whenever a big investor takes a hit, there are those who love to pile on and take their shots at them. From those who manage a pittance compared to these guys who even after their worst year have track records that soundly trounced those piling on, to the media who only manage maybe a checkbook to those bloggers whose sole existence in the world is telling us how everyone and everything just sucks (fortunately these are the minority of bloggers) it is their “Super Bowl of Schadenfreude”. It comes with the turf for those who manage billions. If you want to be at the top, you have to deal with those who only mission in life is to try to knock you off. Your choice is that or essentially hide like Seth Klarman does (anyone know his $LNG investment is down ~50% the last year?). They are no different that QB’s in football, when they do well, they are heros, when they stumble, they are bums. They are blamed for every action within the company when things go wrong. If a football team loses because a safety blows a coverage in the final seconds and the opponent scores to win the losing team’s QB “can’t win the big one”.

Likewise we are told Ackman should have known this or that about Valeant (even though he did not have a board seat until yesterday) and had social media been as pervasive in 1991 as it is today, these same people would have been claiming that since Buffett was on the Board at Salomon he must have known about the Treasury bid rigging and probably even endorsed it. At the very least these same folks would have painted him as utterly incompetent and derelict for not catching it. This of course would have been in spite of 99% of them having never stepped foot inside a corporate boardroom.

All that said, for value investors this piling on does provide opportunity. The cascade of opinion and coverage drives prices well below where they would have fallen without the incessant negative drumbeat (and conversely higher when everyone loves something). In times of fear or confusion, every negative article is given a “fact first” opinion until otherwise proven wrong. Separating the credible from the junk takes time and effort and selling a stock is far easier. So people sell. But again, this creates opportunity.

Wading in at prices far far below even a reasonable valuation gives one a huge safety net. People are convinced that default is a probable risk for Valeant now. I think in the case of Valeant simply filing a 10k by April 29th could be a huge positive for the stock. We do not even at this point have to get into debt repayment in 2020, drug pricing in 2017 and beyond or potential divestitures. At prices where they are, just hiring a CEO who has respect and filing a 10k can make you money….

[/drizzle]