Christmas Edition: 2015 in Review

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Christmas is my favorite holiday, as I’m sure it is for many of you reading this. We probably all agree that 2015 had more than its fair share of pain and tragedy around the world. But during Christmas, love and charity triumph—if only for a day—helping us recharge as we approach the new year.

I remember accompanying my mum, who was a social worker in downtown Toronto, as she delivered what we call “Star boxes” to needy children on Christmas Eve. Named after the Toronto Daily Star, which still operates the Santa Claus Fund that started in 1906, the purpose of the gift parcels remains the same: to make sure that no child in Toronto under 13 is overlooked by Santa Claus.

Delivering these packages was more instructive than any textbook. It helped me keep my own family’s financial struggles in perspective and encouraged me to count my blessings. Although we didn’t have much, things could have been many times more challenging. I was grateful to have lots of love and plenty to eat when so many had neither during the cold, snowy Canadian winters.

The experience also showed me that love, family and friends should all be cherished much more highly than any material things. Having money is important, but real happiness can be found only in helping to spread happiness to others.

Merry Christmas: President Signs $680 Billion Business Investment Deal

Before we reach 2016, I want to reflect back on 2015. Everyone is talking about interest rates and monetary policy right now, but the role fiscal policy plays is just as important—if not more so. As I always say, government policy is a precursor to change, and very recently we saw this firsthand.

Only a day after President Barack Obama signed the spending deal Tuesday that lifted the oil export restriction that’s been in place since the mid-1970s, West Texas Intermediate (WTI) crude oil rallied $2 and is now trading higher than its European counterpart, Brent, oil for the first time since 2010.

click to enlarge

Time and again, when regulations are rolled back and markets are allowed to act freely, we see constructive moves such as the WTI rally. It’s much more significant than a 0.25 percent rate hike.

|

Along with $1.1 trillion, the bipartisan deal includes $680 billion in tax cuts over the next decade, which should help accelerate the velocity of money and lead to the creation of new jobs. This is a positive development that wouldn’t have happened without the much-needed leadership of the new Speaker of the House, Paul Ryan.

It’s important for investors to follow the money in this case, just as it was important in February 2009 when the $800 billion stimulus package was signed into law. House Speaker Ryan was able to negotiate a reasonable extension to government spending and usher in a substantive tax incentive program as we head into 2016, an election year.

Top 10 Frank Talk Posts of 2015

As we head into the final days of 2015, I want to share with you the 10 most popular Frank Talks of the year. Among other things, they tell the story that gold, despite being oversold, managed to hold its value better than many other investments deemed “safe.” I’m optimistic to see what 2016 has in store for the yellow metal.

10. Show Me the Stocks, Not the Cash, Say Optimistic CEOs (May 4)

A growing trend among chief executives of successful companies is to be compensated in company stock rather than cash. In May we learned that American Airlines CEO Doug Parker elected to do just that.

“This is the right way for my compensation to be set,” Parker wrote, “at risk, based entirely on the results achieved.”

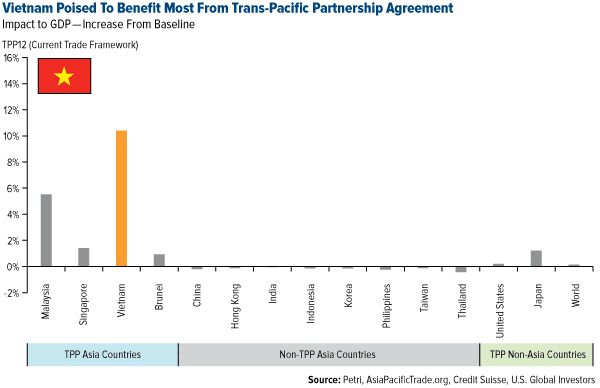

9. How These 12 TPP Nations Could Forever Change Global Growth (October 12)

One of the most significant news stories to come out of 2015 was the signing of the Trans-Pacific Partnership (TPP) by 12 participating Pacific Rim nations, the United States among them. Many analysts believe that Vietnam is poised to see the biggest upside potential, as precipitously high tariffs on its important textiles, apparel and footwear exports will vanish.

click to enlarge

8. China to Take Reins in Funding Regional Infrastructure Projects (March 31)

A similar development that’s likely to have huge global consequences is the establishment of the China-led Asian Infrastructure Investment Bank (AIIB), designed as a competitor to the U.S.-led International Monetary Fund (IMF), World Bank and Asian Development Bank (ADB).

Part of the reasoning behind China’s creation of the bank was to firm up the renminbi as a preferred global reserve currency on par with the U.S. dollar. And indeed, in late November the IMF voted to include the renminbi, also known as the yuan, in its Special Drawing Rights (SDR) currency basket.

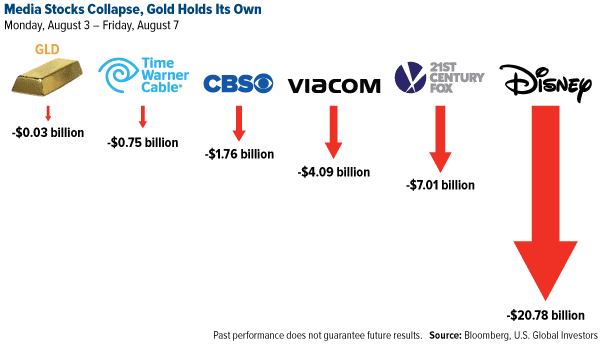

7. Gold Holds Its Own Against These Media Darlings (August 10)

July 2015 was the seventh-worst-performing month for commodities going back to January 1970. Gold in particular was hit hard. But then in the week ended August 7, U.S. media companies took a huge dive, losing $60 billion for shareholders. Compared to that amount, gold managed to hold up well.

click to enlarge

6. Currency Wars Heat up as Central Banks Race to Cut Rates (February 2)

After Switzerland unexpectedly unpegged its currency from the euro in mid-January, it became clear that 2015 would be the year of the central banks. In that month alone, 14 countries cut interest rates and loosened borrowing standards. The U.S. stands as the only major economy, in fact, that has started to tighten its monetary policy.

5. Why We Invest in Royalty Companies (February 26)

One reason gold royalty companies have outperformed over the years is because, simply put, they’re not the ones getting their hands dirty. Their only obligation is to lend capital to the producers. Since its initial public offering (IPO) in 2007, Franco-Nevada, the world’s largest gold royalty company, has torn past both spot gold and most gold equity benchmarks.

click to enlarge

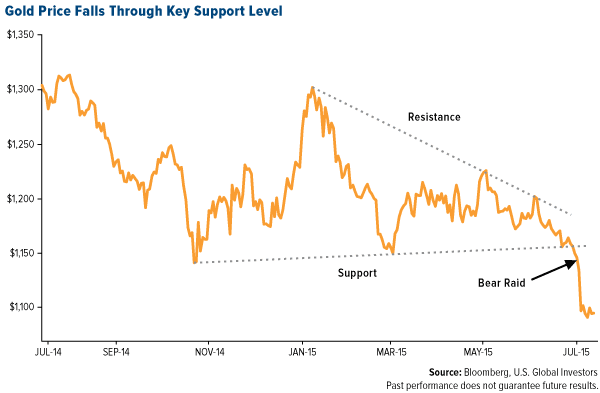

4. Gold on Sale, Says the Rational Investor (August 3)

In late July, gold experienced its first “flash crash” in 18 months after five tonnes of the metal appeared on the Shanghai market. In what many called a “bear raid,” gold fell through its key support of around $1,150 and began to look extremely oversold.

click to enlarge

3. Will Gold Finish 2015 with a Gain? (October 19)

In October, two events occurred almost simultaneously: The U.S. dollar signaled a “death cross”—meaning its 50-day moving average fell below its 200-day moving average—while gold broke above its 200-day moving average. At the time, it appeared as if gold might have a chance at doing something it hasn’t done since 2012—end the year in positive territory.

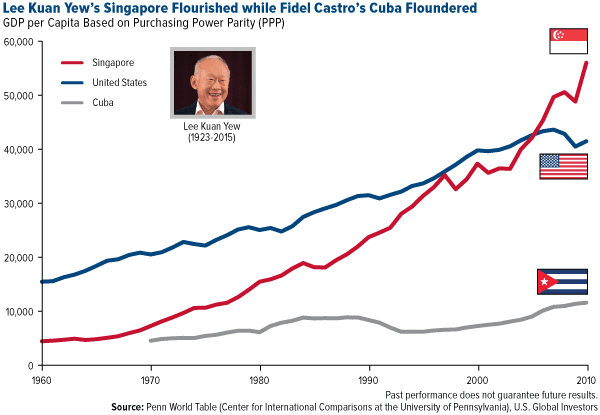

2. A Tale of Two Economies: Singapore and Cuba (March 28)

It’s almost impossible to believe now, but Cuba was once a wealthier nation than Singapore. But in 1959, Fidel Castro and Lee Kuan Yew both assumed power and took their countries in very different ideological and economic directions.

Yew, who passed away in March 2015, emphasizes free trade and competitive tax rates, which helped transform Singapore from an impoverished third world country into a bustling metropolis and leading global financial hub.

click to enlarge

1. Gold in the Age of Soaring Debt (June 18)

The world now sits beneath a mountain of debt worth an astonishing $200 trillion. That’s greater than twice the global GDP, which is currently $75 trillion. If we were to distribute this amount equally to every man, woman and child on the face of the earth, we would each owe around $28,000.

More surprising is that if gold—at its June 2015 price level—backed total global debt 100 percent, it would be valued at $33,900 per ounce.

Make sure to check out our most popular interactive favorites from 2015:

- The Periodic Table of Commodities Returns

- The Periodic Table of Emerging Markets

- Gold Through the Ages

- 21 Emerging Europe Countries Poised for Growth

- Name the Currency’s Country

To all of our readers around the world, to our investors and shareholders, and to our friends and family, I wish you happiness and good health this Christmas and prosperity in the new year!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.32 percent. The S&P 500 Stock Index rose 0.93 percent, while the Nasdaq Composite grew 0.92 percent. The Russell 2000 small capitalization index gained 1.71 percent this week.

- The Hang Seng Composite gained 1.25 percent this week, while Taiwan was up 0.06 percent and the KOSPI rose 0.64 percent.

- The 10-year Treasury bond yield rose two basis points to 2.24 percent.

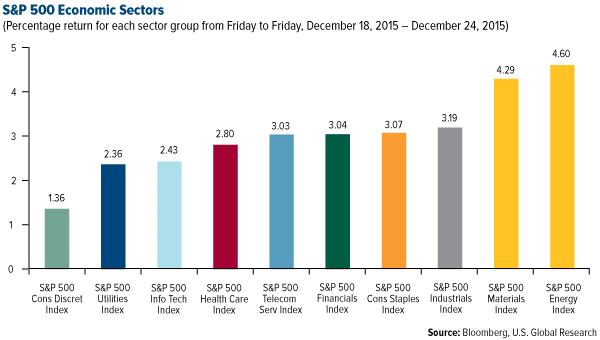

Domestic Equity Market

click to enlarge

Strengths

- ONEOK was the best-performing stock in the S&P 500 Index, returning 27.24 percent. The company was recently upgraded by Oppenheimer, which says management impressed investors with its solid 2016 outlook expecting growth in EBITDA (earnings before interest, taxes depreciation and amortization) and distributable cash flow despite the weak energy environment.

- The best-performing sector this week was energy, which gained 4.6 percent, compared to a 2.79 percent gain by the S&P 500 overall.

- This week, oil explorers in the U.S. climbed the most in four months as WTI crude oil prices recovered from a 2015 low experienced during the previous week. Exploration and production companies in the S&P 500 rose as much as 7.3 percent this week, marking the biggest jump sinceAugust 27.

Weaknesses

- Chipotle Mexican Grill was the worst-performing stock in the S&P 500, returning a negative 8.5 percent, following investigations that linked almost 500 E. coli-contaminated customers around the country to the restaurant chain.

- The worst-performing sector in the S&P 500 was the consumer discretionary sector, which advanced 1.36 percent.

- Analysts have begun forecasting a slowdown in iPhone sales in 2016 based on various supply chain data and an apparent saturation by the product in developed markets. During the past month, Apple has fallen 8.48 percent.

Opportunities

- As personal income advanced more than expected during October and overall prices remained unchanged, consumers are starting to spend about as much as they make, which indicates consumer confidence is improving as the job market strengthens. These factors give households the confidence to hold less cash as a precaution against hard times.

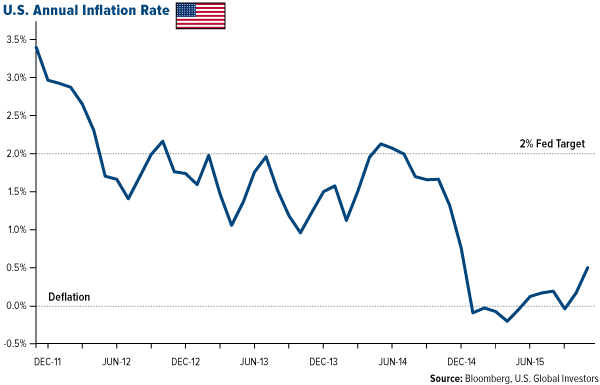

- According to BCA Research, deflation now plagues more than half of the groups covered, as 32 of the 60 industries are currently having to cut selling prices. Six other industries can’t raise prices by more than 0.5 percent per annum, while another seven are stuck below 2 percent, which is the rate of overall core consumer price inflation. In other words, two thirds of the industries cannot keep pace with core inflation rates. The telecommunications and consumer staples sectors have not seen their pricing power deteriorate, suggesting that defensive and domestically-focused sectors and industries continue to hold the upper hand.

- SunEdison climbed as much as 14 percent after the renewable power company said it’s been in talks about securing new financing. The world’s largest renewables developer has been in talks since earlier this month regarding a second lien worth as much as $650 million, in an effort to own and operate solar and wind farms.

Threats

- Although lower gas prices have led to a pickup in travel, BCA Research notes that North American revenue per room is on the cusp of contraction, while global revenue per room is already shrinking. Additionally, recent surges in wage growth among those working in the hotel industry has caused hotels’ profit margins to erode, and it is important to keep in mind that profit downturns can be a much more accurate indicator of industry health than simple price-to-earnings ratios.

- There’s a risk of oil refining margins narrowing, as refiners continue to operate at nearly full capacity, despite consumption growth slowing down.

- According to Bloomberg, investors pulled more money from U.S. mutual funds last week than they have in any seven-day period in the past two and a half years, furthering a series of net redemptions every month since July. Investors withdrew $11.1 billion from stock funds, $12 billion from bond funds and $5.6 billion from funds that buy a mix of stocks and bonds.

December 21, 2015The Fed Awakens: A New Hike |

December 16, 2015Chinese Railway Stays On Track |

December 14, 2015This Industry Is Set to Post Record Profits on Lower Fuel Costs |

The Economy and Bond Market

Strengths

- In a quiet, holiday-shortened week of trading, the third reading of United States gross domestic product came in at 2.0 percent, slightly weaker than the prior reading of 2.1 percent but still ahead of analysts’ expectations of 1.9 percent.

- Sleepy global markets continued uneventfully to digest last week’s widely-expected rate hike from the Federal Reserve, and U.S. government bond prices traded down just slightly. The relative serenity with which markets have accepted the Fed’s move signals not only that the Fed adequately telegraphed its intentions but also that markets widely agree with the hike, a sign of continued stability and underlying strength in the U.S. economy.

- Initial jobless claims came in slightly better than estimated at 267,000, just ahead of an expected 270,000, again marking the slow, steady progress in the U.S. economic recovery.

Weaknesses

- Core durable goods orders for November came in lighter than expected, with capital goods down 0.4 percent and worse than analysts’ expectations for a milder decline of 0.2 percent.

- Existing home sales declined almost 11 percent to a 4.76 million annualized rate, down from a prior reading of 5.32 million. The slower annualized rate marks a 19-month low.

- New home sales also declined more than expected, coming in at 490,000 versus expectations of 505,000. The prior reading was also revised down from 495,000 to 470,000.

Opportunities

- China’s leaders signaled that they will take further steps to support growth, including widening the fiscal deficit and stimulating the housing market. According to statements released at the end of the government’s Central Economic Work Conference by the official Xinhua News Agency, monetary policy must be more “flexible” and fiscal policy more “forceful” as leaders create “appropriate monetary conditions for structural reforms.”

- The University of Michigan’s Consumer Sentiment index has advanced from its September low due primarily to labor market gains and the slump in energy prices. Consumers’ upbeat mood may continue if energy prices continue to stay low.

- The Chicago Purchasing Manager Index data will be reported next week for December and is expected to cross above the 50 level that separates growth from contraction. Investors value this indicator because the Chicago region somewhat reflects the United States overall in its distribution of manufacturing and non-manufacturing activity.

Threats

- Existing home sales fell 11 percent in November to 4.76 million annualized rate from 5.32 million previously, due to buyers adapting to new regulations. The National Association of Realtors said new regulations have disrupted the purchase pipeline and extended the closing process by about five days.

- According to BCA’s publication from December 22, “Deflation Still Prevails,” deflation remains the dominant stock market threat after the Federal Reserve hiked its rates by 25 basis points last week. Domestic goods prices continue to plunge. China’s exchange rate devaluation will continue to export deflation to the rest of the world.

click to enlarge

- The U.S. Dollar Index is heading for its biggest monthly decline since April, reflecting speculations that the Fed will raise rates slowly. The U.S. Dollar declined 1.8 percent month-to-date.

Gold Market

For the holiday-shortened week, spot gold closed at $1,075.88, up $9.73 per ounce, or 0.91 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, rose 5.44 percent. Junior miners underperformed seniors for the week as the S&P/TSX Venture Index climbed only 3.10 percent. The U.S. Trade-Weighted Dollar Index fell 0.79 percent since last Friday.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-24 | Initial Jobless Claims | 270k | 267k | 272k |

| Dec-28 | Exports YoY | -2.6% | — | -3.7% |

| Dec-29 | Consumer Confidence Index | 93.8 | — | 90.4 |

| Dec-31 | Initial Jobless Claims | 273k | — | 267k |

Strengths

- The best-performing precious metal this week was platinum, climbing 3.03 percent. Absent any real market moving news, the lift was likely from short covering as platinum prices have been off as much as 30 percent this year.

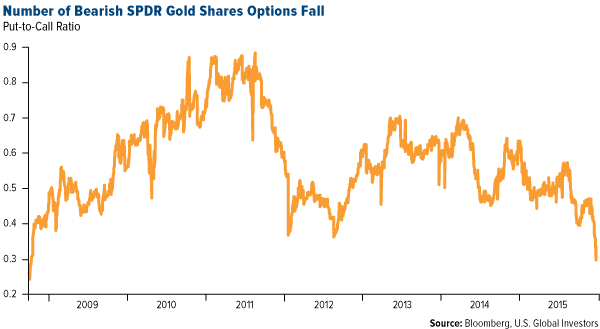

- After the losses seen in gold following the Federal Reserve’s rate hike last week, Bloomberg reports that some traders closed their bearish positions on the metal before year-end on speculation that physical purchases may pick up. Further, Bloomberg notes that the put-to-call ratio on SPDR Gold Shares has reached its lowest level since 2008, perhaps indicating that investors who were betting on further declines in gold prices are losing enthusiasm for this trade. Hedge funds reduced bets for a third week that the dollar would advance, according to Bloomberg. The currency is headed for its biggest monthly decline since April. According to Shane Oliver of AMP Capital Investors: “The bet is over for the U.S. dollar.”

click to enlarge

- Finland’s foreign minister, Timo Soini, announced that his country should never have joined the euro, according to a Brown Brothers Harriman report. Soini announced during a press conference that Finland could have weakened its currency had it not adopted the euro, adding that organizing a referendum on the currency means that the debate “will gather steam.”

Weaknesses

- The worst-performing precious metal this week was palladium, recording just a 0.09 percent gain. Bloomberg noted that car sales in China, which rebounded in October due to a tax cut, have not led to any price strength in palladium.

- Three months after announcing its interest in redeveloping a gold mine in Ghana, Randgold Resources has pulled out of the Obuasi plan. Following the completion of a due diligence exercise into the mine, the company decided not to go through with its planned joint venture with South African firm AngloGold Ashanti. Randgold determined that the development plan doesn’t satisfy its internal investment requirements.

- Yamana Gold announced its decision to suspend the monetization of its Brio Gold subsidy, based on the context of current market conditions. In November, Yamana had announced it commenced a private placement of Brio common shares, according to a Canaccord Genuity report, which consisted of a primary offering by Brio and a secondary offering by Yamana. Cannacord’s valuation assessment of Yamana’s suspension reasons that “the lower multiple reflects the inability to conclude the monetization of Brio Gold.”

Opportunities

- The mine supply issue is coming to a head, according to Credit Suisse’s 2015 Year-End Preview report. Reserve life has fallen from 14 to 10 years since 2011, and grades processed are 9 percent above reserve grade in 2015. The report continues by noting that gold is positioned to outperform the commodity complex next year as two more Fed hikes are priced in, physical demand should continue to be a source of strength and central banks will continue buying.

- HSBC Research says there are two catalysts for gains in platinum in 2016, after touching seven-year lows: improved automobile and investment demand. Both platinum and palladium should benefit from limited supply growth and a weaker U.S. dollar, according to HSBC’s report, as ample stockpiles may curb rallies.

- Both Scotiabank and Paradigm Capital released initiation reports this week for Klondex Mines, following the company’s announcement last week of its acquisition of the Rice Lake Mine near Bissett, Manitoba. Paradigm’s report calls Klondex a “Four G Winner,” highlighting grade, growth, geology and geopolitics, and concluding with a “buy rating” for the company. Scotia noted that investors can “Weather the Storm with This High-Grade Gold Producer” and went with a “Sector Outperform” rating.

Threats

- In its analysis of the broad U.S. equity market this week, BCA Research explains that deflation now plagues more than half of the groups that they cover. An update on industry group pricing power shows that 32 out of 60 industries have had to cut selling prices, up from 26 in BCA’s last update. To further illustrate the underperformance of the economy, BCA provided a chart that shows each successive real GDP forecast made in the Conference Board Budget Outlook from 2007 through 2015 compared to actual real GDP.

click to enlarge

- According to Financial Post data, 2015 could go down as the biggest year ever for metal streaming deals, as miners have raised $4.2 billion from 11 stream sales this year. This is almost double the amount raised in 2013, $2.2 billion, which was the second biggest year on record. One argument surrounding the dark side of metal streaming deals is that streams can eliminate exploration upside from a mine. In addition, John Ing, president and gold analyst at Maison Placements Canada, believes streaming is reminiscent of hedging. (This was all the rage in the gold industry in the 1990s, but has since become a huge liability).

- Bank of America Merrill Lynch released a report on the high-yield gold industry, starting with its overview of select high-yield gold credits: Eldorado Gold, IAMGOLD and New Gold. After its consideration regarding production, asset quality, credit and financial strength, along with relative value, BAML says it is “hard to get excited about any of the names we discussed.” The report continues by stating that, “given our BAML Commodity Team’s view of headwinds facing gold prices, we do not find a compelling reason to own any gold miners’ debt heading into 2016.”

Energy and Natural Resources Market

Strengths

- Crude oil prices posted their biggest weekly gain in months after a U.S. Energy Information Administration (EIA) report showed a greater-than-expected drop in oil inventories. Although U.S. crude stockpiles continue to be at near-record levels, and production levels remain high despite the nearly 70 percent drop in active oil rigs, the bullish inventory report helped oil prices close at their highest in three weeks.

- Base metal stocks were the best-performing sector for the week, with the TSX Metals and Mining Index rising in excess of 15 percent for the week. Analysts have attributed the rally to positive comments out of China suggesting increased consumption is likely for 2016. VTB Capital expects all base metals, with the exception of aluminum, to be in supply deficit in 2016.

- First Quantum was the best-performing stock for the week, rebounding from an oversold condition as copper prices and copper stocks rallied on optimistic news coming out of China. The stock rallied 26 percent in Canada, leading a rally in the sector.

Weaknesses

- West Texas Intermediate (WTI) crude oil is now trading above its European counterpart, Brent, for the first time since 2010, boosted by Congress lifting the US oil exports ban. Overall, the reaction appears overdone and, according to London-based analysts, may ultimately be negative for WTI as it will incentivize Brent barrels to make landfall in the U.S. Gulf Coast.

- Corn was the worst-performing commodity for the week, dropping under 3 percent, as bids for spot supplies at Gulf Coast slumped, and competition from Argentinean exports weighed on prices. In addition, U.S. Department of Agriculture (USDA) figures show commitments for U.S. exports are running 23 percent below last year’s pace.

- Smurfit Kappa, an Ireland-based container and packaging company, fell over 2 percent for the week and was the worst-performing stock in the S&P Global Natural Resources Index. Earlier this month, Back of America warned of possible weakness in the sector following strong share performance earlier in the year and softening of prices in some container markets.

Opportunities

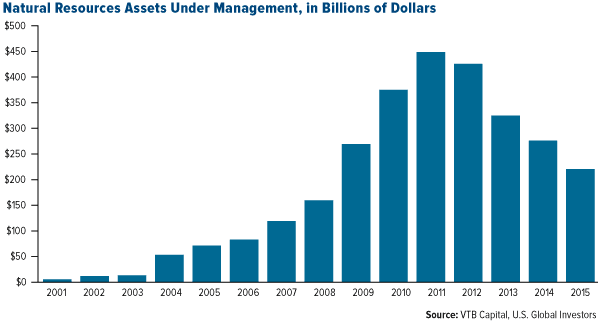

- Based on latest estimates, the total short exposure in commodities has reached $200 billion. This unprecedented buildup in fund shorts has created a major headwind for commodity prices in the short-term. However, when considering the size of total managed long commodity assets, which has declined to about $200 billion, very close to the total commodity shorts, any partial unwinding of the short trade should bode well for commodities during 2016.

click to enlarge

- This year has seen bearish sentiment in natural gas, as prices continue to diminish year-to-date and weather forecasts continue to show above average temperatures. However, the current contango is one of the widest since 2005, with the 12-month contract at more than 40 percent above spot. According to Raymond James, statistical analysis suggests that this level of contango has led to significant price increases in the past, thus reinforcing the bullish case for natural gas in 2016.

- Activism is on the rise in the natural resources sector. This week, Dominion Diamond, a Canadian diamond miner, rose around 20 percent after a set of activist investors approached the company to express their discontent with current management. After a number of successful activist moves in the space this year, activist investors are likely to continue to exploit opportunities in the space into 2016.

Threats

- Despite the sustained pressure from WTI prices, the Baker Hughes rig count was up 17 last week, marking the first sizeable increase during the past five months. This, however, proved to be a temporary jump, reflecting activity following the short-lived rallies during November. Given December’s weakening oil prices, it is expected for the rig count to resume its decline.

- Steel producers have rallied significantly over the past week as Chinese authorities suggest they will continue to support steel producers in the country. Nevertheless, according to a report released this week by the U.S. Department of Commerce, steel imports from China were sold at unfairly low prices and a 256 percent import duty will be applied. This may result in volumes dropping in the near future.

- After Yamana Gold announced that it believed it could complete a monetization of its Brio Gold subsidiary in order to reduce its debt levels, investors were highly disappointed with the recent announcement that revealed the suspension of its monetization efforts. In the current environment, Yamana has been unable to find a suitable offer for its assets, meaning its debt levels are likely to remain high.

China Region

Strengths

- Philippines was the best-performing market in Asia this week, as investors reallocated to one of the best-shielded Asian economies from Federal Reserve’s interest rate cycle in a holiday-shortened week. The Philippines Stock Exchange PSEi Index gained 1.97 percent this week.

- Energy was the best-performing sector in Asia this week, as crude oil prices staged the largest weekly rebound in two months. Aggregate U.S. weekly crude oil inventories unexpectedly declined and drilling rigs decreased as well. The MSCI Asia Pacific ex Japan Energy Index advanced 3.90 percent this week.

- The Indonesian rupiah was the best-performing currency in Asia this week, strengthening by 1.99 percent, as the Indonesian central bank cited positive foreign inflow to local currency bonds and the government planned to allow the private sector to enter formerly state-owned oil refining businesses.

Weaknesses

- Thailand was the worst-performing market in Asia this week, as the country’s largest wireless telecommunications carriers failed to win licenses to provide 4G services at last week’s auction amid fears of new entrants into the industry. The Stock Exchange of Thai Index lost 0.06 percent this week.

- Telecommunications was the worst-performing sector in Asia this week, led by a significant retreat of major Thai telecom carriers after last week’s unsuccessful bid for 4G licenses. The MSCI Asia Pacific ex Japan Telecom Services Index finished up only 0.44 percent this week.

- The Malaysian ringgit was the worst-performing currency in Asia this week, weakening by 0.44 percent, as the country’s consumer price index came out higher than expected in November at 2.6 percent year-over-year, lending investors the incremental rationale to sell the currency.

Opportunities

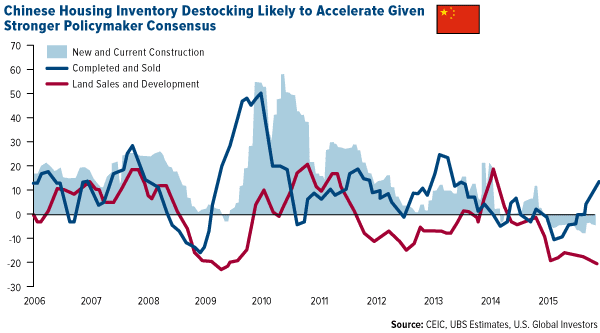

- Positive investor sentiment toward Chinese property developers should be sustainable in the near term, especially since a stronger consensus seems to have been reached within China’s top policymaking circle upon conclusion of the country’s annual Central Economic Work Conference. The consensus is that, to avoid a hard handing in the real economy, it is essential to facilitate and accelerate the destocking process of domestic housing inventory via government policy assistance. Quality Chinese residential property developers trading below historical average valuation should continue to outperform.

click to enlarge

- South Korean equities should prove relatively resilient following the U.S. rate hike, given the country’s robust fiscal status, recovering domestic demand, rising shareholder returns and attractive valuation. Indeed, index-dominant technology exporters in Korea are likely to benefit from potential further strength in the U.S. dollar, and based on the last five years, according to Morgan Stanley, a weaker Korean won against the U.S. dollar tends to correlate with outperformance of Korean equities versus the rest of Asia, with a three-month time lag.

- As global investor risk appetite retrenches after the Federal Reserve’s decision to hike interest rates and Baltic dry bulk shipping rates hovers around all-time lows, cash as the ultimate defensive asset class may once again outperform. Volatility has picked up in various asset classes around the world.

Threats

- At least two thirds of Macau casino companies are still ranked in the bottom 10 percent of actively-traded companies in Hong Kong, sorted by trailing 12-month price performance. Therefore, they remain vulnerable to further selling by long-only institutional investors keen on “window dressing” going into year end. Lingering uncertainties about Macau casinos’ business model against rising new gaming supply amid unabated demand pressure from slower Chinese economy, weaker Chinese currency and lengthier anticorruption campaigns should continue to weigh on casino stocks next year.

- Luxury goods companies listed in Hong Kong may continue to underperform next year, not only because China’s anticorruption campaign would remain a discouragement for conspicuous consumption, but also because luxury brands which underwent significant store expansion in recent years may have to resort to price cuts and store closures to adapt to today’s reality. This means profit margins for luxury brands are likely to deteriorate while valuations stay unattractive.

- The local economy of Hong Kong, which has synchronized monetary policy with the U.S. because of a pegged Hong Kong dollar, is likely to be more vulnerable than during the 2004-2006 Federal Reserve tightening cycle, given over 200 percent private sector debt to GDP, a peaking property cycle and a continuously slowing Chinese economy. Equities of Hong Kong real estate and retail-oriented sectors might bear the brunt of any negative impact from even a gradual pace of interest rate hikes.

Emerging Europe

Strengths

- Turkey was the best-performing market this week, gaining 2.2 percent. Deputy Prime Minister Mehmet ?im?ek sees higher-than-expected 3.5 to 4 percent growth this year. In a press conference, he further said that souring relations with Russia after Turkey downed a Russian jet had not resulted in a serious economic impact so far.

- The Polish z?oty was the best-performing currency this week, gaining 1.5 percent against the dollar. Year-to-date, the Polish currency lost more than 8 percent, but it has been strengthening since the beginning of December along with the euro.

- The utility sector was the best-performing sector among Eastern European markets this week.

Weaknesses

- Hungary and Greece were the worst-performing markets this week, losing 50 basis points each. According to the Standard Eurobarometer survey conducted on behalf of the European Commission, 97 percent of Greeks are dissatisfied with the country’s economy, while 70 percent expect deterioration in the coming 10 months. Hungary’s December consumer confidence index (CCI) was reported at -19.2 versus a prior -19.6, indicating a slight improvement in consumer optimism. The latest reading, however, is well below an all-time high of 89.82 in December 2014.

- The Turkish lira was the worst-performing currency, losing 40 basis points against the dollar.

- The health care sector was the worst-performing sector among Eastern European markets this week.

Opportunities

- Consumer confidence in eurozone nations ticked upward in December to a better-than-expected -5.7 percent, beating estimates of -5.9 percent. The index reached its highest level since June and is more than seven points above its long-term average.

- The MSCI Emerging Market Stock Index is set to report double digit losses this year and extend its losing streak from two years to three. Emerging stocks in 2015 have underperformed their developed peers for a fifth straight year. However, some economists see a rebound approaching. Arjen van Dijkhuizen of ABN Amro, a Dutch state-owned bank, predicts modest economic recovery in emerging markets next year as commodity prices stabilize, as well as trade pickups and Chinese import improvements. The Federal Reserve’s gradual rate hikes may boost investors’ confidence and create an appetite for cheap emerging markets, especially in the commodity and oil sectors.

- Greece looks as if it is pushing forward its reforms and on a path to recovery. Greek government passed a budget earlier this month, recapitalized banks and is making plans to sell state-owned assets and deal with country’s bad debt.

Threats

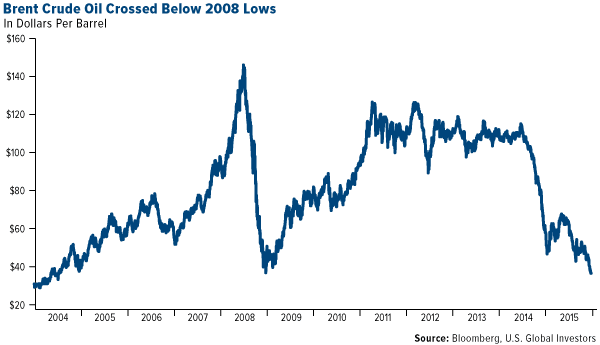

- Russia continued to extract oil at a post-Soviet record high of 10.78 million barrels per day in November despite dropping oil prices. Some banks such as Goldman Sachs predict oil prices could fall to as low as $20 per barrel as the world produces more oil than it consumes. The Russian central bank is preparing a risk scenario with oil prices at $35 per barrel for the next three years, and is predicting that gross domestic product will contract by 2 to 3 percent in 2016.

click to enlarge

- The European Union (EU) has renewed its economic sanctions against Russia for six months after concluding that Moscow has failed to fully respect a peace agreement in eastern Ukraine. Sanctions imposed on the country and falling oil prices continue to put pressure on its economy.

- The Central Bank of the Republic of Turkey unexpectedly left its main interest unchanged at 7.5 percent despite prior indications of a rate hike after the Federal Reserve’s first rate hike. The bank’s decision to keep the rate unchanged added more fuel to concerns regarding the credibility of the central bank.

- Finland’s foreign prime minister, Timo Soini, stated during a press conference in Helsinki that his country should never have adopted the euro. He noted that Finland would otherwise have been able to weaken its currency. Many EU members are “euroskeptics,” including France, the United Kingdom and Poland, which elected a euroskeptic government in October.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| DJIA | 17,552.17 | +56.33 | +0.32% |

| S&P 500 | 2,060.98 | +19.09 | +0.93% |

| S&P Energy | 458.67 | +12.93 | +2.90% |

| S&P Basic Materials | 278.29 | +7.89 | +2.92% |

| Nasdaq | 5,048.49 | +45.94 | +0.92% |

| Russell 2000 | 1,154.75 | +19.39 | +1.71% |

| Hang Seng Composite Index | 3,048.69 | +37.63 | +1.25% |

| Korean KOSPI Index | 1,990.65 | +12.69 | +0.64% |

| S&P/TSX Canadian Gold Index | 135.27 | +9.88 | +7.88% |

| XAU | 47.81 | +4.60 | +10.65% |

| Gold Futures | 1,076.30 | +26.70 | +2.54% |

| Oil Futures | 38.24 | +3.29 | +9.41% |

| Natural Gas Futures | 2.02 | +0.27 | +15.21% |

| 10-Yr Treasury Bond | 2.24 | +0.02 | +0.81% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| DJIA | 17,552.17 | -260.02 | -1.46% |

| S&P 500 | 2,060.98 | -28.16 | -1.35% |

| S&P Energy | 458.67 | -45.23 | -8.98% |

| S&P Basic Materials | 278.29 | -9.59 | -3.33% |

| Nasdaq | 5,048.49 | -54.32 | -1.06% |

| Russell 2000 | 1,154.75 | -34.06 | -2.87% |

| Hang Seng Composite Index | 3,048.69 | -68.37 | -2.19% |

| Korean KOSPI Index | 1,990.65 | -25.64 | -1.27% |

| S&P/TSX Canadian Gold Index | 135.27 | +9.92 | +7.91% |

| XAU | 47.81 | +1.66 | +3.60% |

| Gold Futures | 1,076.30 | +3.00 | +0.28% |

| Oil Futures | 38.24 | -4.63 | -10.80% |

| Natural Gas Futures | 2.02 | -0.18 | -8.09% |

| 10-Yr Treasury Bond | 2.24 | +0.00 | +0.13% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| DJIA | 17,552.17 | +1,350.85 | +8.34% |

| S&P 500 | 2,060.98 | +128.74 | +6.66% |

| S&P Energy | 458.67 | +3.09 | +0.68% |

| S&P Basic Materials | 278.29 | +25.17 | +9.94% |

| Nasdaq | 5,048.49 | +314.01 | +6.63% |

| Russell 2000 | 1,154.75 | +17.22 | +1.51% |

| Hang Seng Composite Index | 3,048.69 | +140.78 | +4.84% |

| Korean KOSPI Index | 1,990.65 | +43.55 | +2.24% |

| S&P/TSX Canadian Gold Index | 135.27 | +6.49 | +5.04% |

| XAU | 47.81 | -0.08 | -0.17% |

| Gold Futures | 1,076.30 | -78.30 | -6.78% |

| Oil Futures | 38.24 | -6.67 | -14.85% |

| Natural Gas Futures | 2.02 | -0.57 | -21.96% |

| 10-Yr Treasury Bond | 2.24 | +0.11 | +5.36% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned above were held by one or more accounts managed by U.S. Global Investors as of 9/30/2015:

First Quantum Materials Ltd.

Yamana Gold Inc.

Franco-Nevada Corp.

Time Warner Cable Inc.

Randgold Resources Ltd.

Klondex Mines Ltd.

AngloGold Ashanti Ltd.

Eldorado Gold Corp

IAMGOLD Corp.

New Gold Inc.

Apple Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The Consumer Confidence Index (CCI) is an indicator which measures consumer confidence in the Economy.

The S&P Global Natural Resources Index includes 90 of the largest publicly-traded companies in natural resources and commodities businesses that meet specific investability requirements, offering investors diversified, liquid and investable equity exposure across 3 primary commodity-related sectors: Agribusiness, Energy, and Metals & Mining.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets.

The S&P/TSX Capped Metals and Mining Index is a capitalization-weighted index.

The University of Michigan Confidence Index is a survey of consumer confidence conducted by the University of Michigan. The report, released on the tenth of each month, gives a snapshot of whether or not consumers are willing to spend money.

The National Association of Purchasing Management’s Chicago PMI measures manufacturing activity in the Chicago area.

The U.S. Dollar Index is an index of the value of the United States dollar relative to a basket of foreign currencies.

The Philippine Stock Exchange PSEi Index is composed of stocks representative of the industrial, properties, services, holding firms, financial and mining & oil sectors of the Philippines Stock Exchange.

MSCI Asia Pacific ex Japan Telecom Services Index measures the performance of the telecom services sector across all stock markets of China, Hong Kong, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand, India and Pakistan.